MetaTraderプログラムを簡単かつ迅速に開発するためのライブラリ(第25部): 取引サーバから返されたエラーの処理

内容

概念

ターミナル、口座、取引銘柄パラメータ有効性の検証、無効な取引注文パラメータの自動修正は既に実装しています。後は、送信された取引注文に対するサーバからの応答の処理を実装するだけです。

サーバに取引注文を送信した後は、応答を確認する必要があります。サーバからの応答はエラーがないことを示す場合、または、処理する必要があるエラーコードを示す場合があります。

サーバからの応答は、無効な取引注文パラメータとまったく同じ方法で処理します。

- エラーなし — 注文は実行のために正常にキューに追加されている

- EAの取引を無効にする - 例: サーバ側からの取引操作の完全な禁止

- 取引メソッドの終了 — 例: サーバに注文を正常に送信できない、ポジションが既に決済されている、未決注文が削除されている

- 取引リクエストパラメーターを修正して繰り返す — 取引注文パラメータに無効な値がある。ほとんどの場合、サーバリクエストの準備時にデータが変更されており、適切な調整が必要になっている。

- データを更新して繰り返す — サーバのデータは変更されたが、取引リクエストの値を調整する必要はない

- 待機して繰り返す —

待機が必要。たとえば、価格がポジションストップレベルのいずれかに近い場合、ストップ注文が既にアクティブになっている可能性があるため、FreezeLevelパラメータは変更を無効にする。待機により、ストップ注文のアクティブ化と取引リクエストのキャンセル、または価格がフリーズエリアを離れるのを待つことができるため、注文がサーバーに正常に送信される

- 未決取引リクエストの作成 — 次の記事で説明します。

戻りコードには、取引注文で発生する可能性のあるエラーを修正するために実装されていないものが数多くあります。また、すべてのコードを修正してリクエストを繰り返すことができるわけではありません。修正可能なエラーを除外するために、エラーを処理して取引注文に返送しようとします。

取引リクエストを送信するメソッドでは、取引リクエストを送信するメソッドでサーバに取引注文を再送信するためのループを配置します。言い換えると、サーバへの最初のリクエストの後にエラーを受け取った場合、取引クラスに対して定義された取引の試行回数を上限として、または、注文がサーバに正常に送信されるまで、試行が行われます。

サーバへの注文の送信がすべて失敗した場合、取引メソッドからfalseを返します。この場合、呼び出し元プログラムの最後のエラーコードを確認できます。コードは取引サーバによって返されるため、エラーの処理は自分で決定できます。

ここで実装します。

実装

Account.mqhファイルのCAccount口座クラス内で、口座オブジェクトプロパティに簡単にアクセスするためのブロックにヘッジ勘定で作業するフラグを返すメソッドを追加します。

//+------------------------------------------------------------------+ //| Methods of a simplified access to the account object properties | //+------------------------------------------------------------------+ //--- Return the account's integer properties ENUM_ACCOUNT_TRADE_MODE TradeMode(void) const { return (ENUM_ACCOUNT_TRADE_MODE)this.GetProperty(ACCOUNT_PROP_TRADE_MODE); } ENUM_ACCOUNT_STOPOUT_MODE MarginSOMode(void) const { return (ENUM_ACCOUNT_STOPOUT_MODE)this.GetProperty(ACCOUNT_PROP_MARGIN_SO_MODE); } ENUM_ACCOUNT_MARGIN_MODE MarginMode(void) const { return (ENUM_ACCOUNT_MARGIN_MODE)this.GetProperty(ACCOUNT_PROP_MARGIN_MODE); } long Login(void) const { return this.GetProperty(ACCOUNT_PROP_LOGIN); } long Leverage(void) const { return this.GetProperty(ACCOUNT_PROP_LEVERAGE); } long LimitOrders(void) const { return this.GetProperty(ACCOUNT_PROP_LIMIT_ORDERS); } long TradeAllowed(void) const { return this.GetProperty(ACCOUNT_PROP_TRADE_ALLOWED); } long TradeExpert(void) const { return this.GetProperty(ACCOUNT_PROP_TRADE_EXPERT); } long CurrencyDigits(void) const { return this.GetProperty(ACCOUNT_PROP_CURRENCY_DIGITS); } long ServerType(void) const { return this.GetProperty(ACCOUNT_PROP_SERVER_TYPE); } long FIFOClose(void) const { return this.GetProperty(ACCOUNT_PROP_FIFO_CLOSE); } bool IsHedge(void) const { return this.MarginMode()==ACCOUNT_MARGIN_MODE_RETAIL_HEDGING; } //--- Return the account's real properties

Defines.mqhファイルに、取引クラスの取引試行のデフォルト回数を指定するマクロ置換を追加します。

本稿では、保留中リクエストの作成を準備するため、取引クラスのタイマーが必要です。

したがって、今すぐ取引クラスのタイマーパラメータを書きましょう。

//+------------------------------------------------------------------+ //| マクロ置換 | //+------------------------------------------------------------------+ //--- Describe the function with the error line number #define DFUN_ERR_LINE (__FUNCTION__+(TerminalInfoString(TERMINAL_LANGUAGE)=="Russian" ? ", Page " : ", Line ")+(string)__LINE__+": ") #define DFUN (__FUNCTION__+": ") // "Function description" #define COUNTRY_LANG ("Russian") // Country language #define END_TIME (D'31.12.3000 23:59:59') // End date for account history data requests #define TIMER_FREQUENCY (16) // Minimal frequency of the library timer in milliseconds #define TOTAL_TRY (5) // Default number of trading attempts //--- Standard sounds #define SND_ALERT "alert.wav" #define SND_ALERT2 "alert2.wav" #define SND_CONNECT "connect.wav" #define SND_DISCONNECT "disconnect.wav" #define SND_EMAIL "email.wav" #define SND_EXPERT "expert.wav" #define SND_NEWS "news.wav" #define SND_OK "ok.wav" #define SND_REQUEST "request.wav" #define SND_STOPS "stops.wav" #define SND_TICK "tick.wav" #define SND_TIMEOUT "timeout.wav" #define SND_WAIT "wait.wav" //--- Parameters of the orders and deals collection timer #define COLLECTION_ORD_PAUSE (250) // Orders and deals collection timer pause in milliseconds #define COLLECTION_ORD_COUNTER_STEP (16) // Increment of the orders and deals collection timer counter #define COLLECTION_ORD_COUNTER_ID (1) // Orders and deals collection timer counter ID //--- Parameters of the account collection timer #define COLLECTION_ACC_PAUSE (1000) // Account collection timer pause in milliseconds #define COLLECTION_ACC_COUNTER_STEP (16) // Account timer counter increment #define COLLECTION_ACC_COUNTER_ID (2) // Account timer counter ID //--- Symbol collection timer 1 parameters #define COLLECTION_SYM_PAUSE1 (100) // Pause of the symbol collection timer 1 in milliseconds (for scanning market watch symbols) #define COLLECTION_SYM_COUNTER_STEP1 (16) // Increment of the symbol timer 1 counter #define COLLECTION_SYM_COUNTER_ID1 (3) // Symbol timer 1 counter ID //--- Symbol collection timer 2 parameters #define COLLECTION_SYM_PAUSE2 (300) // Pause of the symbol collection timer 2 in milliseconds (for events of the market watch symbol list) #define COLLECTION_SYM_COUNTER_STEP2 (16) // Increment of the symbol timer 2 counter #define COLLECTION_SYM_COUNTER_ID2 (4) // Symbol timer 2 counter ID //--- Trading class timer parameters #define COLLECTION_REQ_PAUSE (300) // Trading class timer pause in milliseconds #define COLLECTION_REQ_COUNTER_STEP (16) // Trading class timer counter increment #define COLLECTION_REQ_COUNTER_ID (5) // Trading class timer counter ID //--- Collection list IDs #define COLLECTION_HISTORY_ID (0x7779) // Historical collection list ID #define COLLECTION_MARKET_ID (0x777A) // Market collection list ID #define COLLECTION_EVENTS_ID (0x777B) // Event collection list ID #define COLLECTION_ACCOUNT_ID (0x777C) // Account collection list ID #define COLLECTION_SYMBOLS_ID (0x777D) // Symbol collection list ID //--- Data parameters for file operations #define DIRECTORY ("DoEasy\\") // Library directory for storing object folders #define RESOURCE_DIR ("DoEasy\\Resource\\") // Library directory for storing resource folders //--- Symbol parameters #define CLR_DEFAULT (0xFF000000) // Default color #define SYMBOLS_COMMON_TOTAL (1000) // Total number of working symbols //+------------------------------------------------------------------+

取引サーバエラー処理メソッドでのフラグのリストに未決注文価格エラーのフラグとストップリミット注文価格エラーのフラグの2つのフラグを追加します。また、エラーと取引サーバの戻りコードを処理するメソッドに取引注文パラメータを修正するメソッドを追加します。

//+------------------------------------------------------------------+ //| Flags indicating the trading request error handling methods | //+------------------------------------------------------------------+ enum ENUM_TRADE_REQUEST_ERR_FLAGS { TRADE_REQUEST_ERR_FLAG_NO_ERROR = 0, // No error TRADE_REQUEST_ERR_FLAG_FATAL_ERROR = 1, // Disable trading for an EA (critical error) - exit TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR = 2, // Library internal error - exit TRADE_REQUEST_ERR_FLAG_ERROR_IN_LIST = 4, // Error in the list - handle (ENUM_ERROR_CODE_PROCESSING_METHOD) TRADE_REQUEST_ERR_FLAG_PRICE_ERROR = 8, // Placement price error TRADE_REQUEST_ERR_FLAG_LIMIT_ERROR = 16, // Limit order price error }; //+------------------------------------------------------------------+ //| The methods of handling errors and server return codes | //+------------------------------------------------------------------+ enum ENUM_ERROR_CODE_PROCESSING_METHOD { ERROR_CODE_PROCESSING_METHOD_OK, // No errors ERROR_CODE_PROCESSING_METHOD_DISABLE, // Disable trading for the EA ERROR_CODE_PROCESSING_METHOD_EXIT, // Exit the trading method ERROR_CODE_PROCESSING_METHOD_CORRECT, // Correct trading request parameters and repeat ERROR_CODE_PROCESSING_METHOD_REFRESH, // Update data and repeat ERROR_CODE_PROCESSING_METHOD_PENDING, // Create a pending request ERROR_CODE_PROCESSING_METHOD_WAIT, // Wait and repeat }; //+------------------------------------------------------------------+

Datas.mqhファイルに、新しいメッセージインデックスを書きます。

//--- CTrading MSG_LIB_TEXT_TERMINAL_NOT_TRADE_ENABLED, // Trade operations are not allowed in the terminal (the AutoTrading button is disabled) MSG_LIB_TEXT_EA_NOT_TRADE_ENABLED, // EA is not allowed to trade (F7 --> Common --> Allow Automated Trading) MSG_LIB_TEXT_ACCOUNT_NOT_TRADE_ENABLED, // Trading is disabled for the current account MSG_LIB_TEXT_ACCOUNT_EA_NOT_TRADE_ENABLED, // Trading on the trading server side is disabled for EAs on the current account MSG_LIB_TEXT_REQUEST_REJECTED_DUE, // Request was rejected before sending to the server due to: MSG_LIB_TEXT_INVALID_REQUEST, // Invalid request: MSG_LIB_TEXT_NOT_ENOUTH_MONEY_FOR, // Insufficient funds for performing a trade MSG_LIB_TEXT_MAX_VOLUME_LIMIT_EXCEEDED, // Exceeded maximum allowed aggregate volume of orders and positions in one direction MSG_LIB_TEXT_REQ_VOL_LESS_MIN_VOLUME, // Request volume is less than the minimum acceptable one MSG_LIB_TEXT_REQ_VOL_MORE_MAX_VOLUME, // Request volume exceeds the maximum acceptable one MSG_LIB_TEXT_CLOSE_BY_ORDERS_DISABLED, // Close by is disabled MSG_LIB_TEXT_INVALID_VOLUME_STEP, // Request volume is not a multiple of the minimum lot change step gradation MSG_LIB_TEXT_CLOSE_BY_SYMBOLS_UNEQUAL, // Symbols of opposite positions are not equal MSG_LIB_TEXT_SL_LESS_STOP_LEVEL, // StopLoss violates requirements for symbol's StopLevel MSG_LIB_TEXT_TP_LESS_STOP_LEVEL, // TakeProfit violates requirements for symbol's StopLevel MSG_LIB_TEXT_PRICE_LESS_STOP_LEVEL, // Order distance in points is less than a value allowed by symbol's StopLevel parameter MSG_LIB_TEXT_LIMIT_LESS_STOP_LEVEL, // Limit order distance in points relative to a stop order is less than a value allowed by symbol's StopLevel parameter MSG_LIB_TEXT_SL_LESS_FREEZE_LEVEL, // The distance from the price to StopLoss is less than a value allowed by symbol's FreezeLevel parameter MSG_LIB_TEXT_TP_LESS_FREEZE_LEVEL, // The distance from the price to TakeProfit is less than a value allowed by symbol's FreezeLevel parameter MSG_LIB_TEXT_PR_LESS_FREEZE_LEVEL, // The distance from the price to an order activation level is less than a value allowed by symbol's FreezeLevel parameter MSG_LIB_TEXT_UNSUPPORTED_SL_TYPE, // Unsupported StopLoss parameter type (should be 'int' or 'double') MSG_LIB_TEXT_UNSUPPORTED_TP_TYPE, // Unsupported TakeProfit parameter type (should be 'int' or 'double') MSG_LIB_TEXT_UNSUPPORTED_PR_TYPE, // Unsupported price parameter type (should be 'int' or 'double') MSG_LIB_TEXT_UNSUPPORTED_PL_TYPE, // Unsupported limit order price parameter type (should be 'int' or 'double') MSG_LIB_TEXT_UNSUPPORTED_PRICE_TYPE_IN_REQ, // Unsupported price parameter type in a request MSG_LIB_TEXT_TRADING_DISABLE, // Trading disabled for the EA until the reason is eliminated MSG_LIB_TEXT_TRADING_OPERATION_ABORTED, // Trading operation is interrupted MSG_LIB_TEXT_CORRECTED_TRADE_REQUEST, // Correcting trading request parameters MSG_LIB_TEXT_CREATE_PENDING_REQUEST, // Creating a pending request MSG_LIB_TEXT_NOT_POSSIBILITY_CORRECT_LOT, // Unable to correct a lot MSG_LIB_TEXT_FAILING_CREATE_PENDING_REQ, // Failed to create a pending request MSG_LIB_TEXT_TRY_N, // Trading attempt # };

メッセージテキストも書きます。

{"Дистанция установки ордера в пунктах меньше разрешённой параметром StopLevel символа","Distance to place order in points less than allowed by symbol's StopLevel"},

{"Дистанция установки лимит-ордера относительно стоп-ордера меньше разрешённой параметром StopLevel символа","Distance to place limit order relative to stop order less than allowed by symbol's StopLevel"},

{"Дистанция от цены до StopLoss меньше разрешённой параметром FreezeLevel символа","Distance from price to StopLoss less than allowed by symbol's FreezeLevel"},

{"Дистанция от цены до TakeProfit меньше разрешённой параметром FreezeLevel символа","Distance from price to TakeProfit less than allowed by symbol's FreezeLevel"},

{"Дистанция от цены до цены срабатывания ордера меньше разрешённой параметром FreezeLevel символа","Distance from price to order triggering price less than allowed by symbol's FreezeLevel"},

{"Неподдерживаемый тип параметра StopLoss (необходимо int или double)","Unsupported StopLoss parameter type (int or double required)"},

{"Неподдерживаемый тип параметра TakeProfit (необходимо int или double)","Unsupported TakeProfit parameter type (int or double required)"},

{"Неподдерживаемый тип параметра цены (необходимо int или double)","Unsupported price parameter type (int or double required)"},

{"Неподдерживаемый тип параметра цены limit-ордера (необходимо int или double)","Unsupported type of price parameter for limit order (int or double required)"},

{"Неподдерживаемый тип параметра цены в запросе","Unsupported price parameter type in request"},

{"Торговля отключена для эксперта до устранения причины запрета","Trading for expert disabled till this ban eliminated"},

{"Торговая операция прервана","Trading operation aborted"},

{"Корректировка параметров торгового запроса ...","Correction of trade request parameters ..."},

{"Создание отложенного запроса","Create pending request"},

{"Нет возможности скорректировать лот","Unable to correct lot"},

{"Не удалось создать отложенный запрос","Failed to create pending request"},

{"Торговая попытка #","Trading attempt #"},

};

TradeObj.mqh基本取引オブジェクトファイルに小さな変更が加えられました。

未決注文を出すメソッドでは実行を定義する注文タイプパラメータがあります(以前はデフォルトが使用されていました)。

//--- Place an order bool SetOrder(const ENUM_ORDER_TYPE type, const double volume, const double price, const double sl=0, const double tp=0, const double price_stoplimit=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE);

渡された値が-1を超える場合、メソッドに渡された値が使用されます。その他の場合は、デフォルトパラメータ値が適用されます。

//+------------------------------------------------------------------+ //| Set an order | //+------------------------------------------------------------------+ bool CTradeObj::SetOrder(const ENUM_ORDER_TYPE type, const double volume, const double price, const double sl=0, const double tp=0, const double price_stoplimit=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { ::ResetLastError(); //--- If an invalid order type has been passed, write the error code and description, send the message to the journal and return 'false' if(type==ORDER_TYPE_BUY || type==ORDER_TYPE_SELL || type==ORDER_TYPE_CLOSE_BY #ifdef __MQL4__ || type==ORDER_TYPE_BUY_STOP_LIMIT || type==ORDER_TYPE_SELL_STOP_LIMIT #endif ) { this.m_result.retcode=MSG_LIB_SYS_INVALID_ORDER_TYPE; this.m_result.comment=CMessage::Text(this.m_result.retcode); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_INVALID_ORDER_TYPE),OrderTypeDescription(type)); return false; } //--- Clear the structures ::ZeroMemory(this.m_request); ::ZeroMemory(this.m_result); //--- Fill in the request structure this.m_request.action = TRADE_ACTION_PENDING; this.m_request.symbol = this.m_symbol; this.m_request.magic = (magic==ULONG_MAX ? this.m_magic : magic); this.m_request.volume = volume; this.m_request.type = type; this.m_request.stoplimit = price_stoplimit; this.m_request.price = price; this.m_request.sl = sl; this.m_request.tp = tp; this.m_request.expiration = expiration; this.m_request.type_time = (type_time>WRONG_VALUE ? type_time : this.m_type_time); this.m_request.type_filling= (type_filling>WRONG_VALUE ? type_filling : this.m_type_filling); this.m_request.comment = (comment==NULL ? this.m_comment : comment); //--- Return the result of sending a request to the server #ifdef __MQL5__ return(!this.m_async_mode ? ::OrderSend(this.m_request,this.m_result) : ::OrderSendAsync(this.m_request,this.m_result)); #else ::ResetLastError(); int ticket=::OrderSend(m_request.symbol,m_request.type,m_request.volume,m_request.price,(int)m_request.deviation,m_request.sl,m_request.tp,m_request.comment,(int)m_request.magic,m_request.expiration,clrNONE); ::SymbolInfoTick(this.m_symbol,this.m_tick); if(ticket!=WRONG_VALUE) { this.m_result.retcode=::GetLastError(); this.m_result.ask=this.m_tick.ask; this.m_result.bid=this.m_tick.bid; this.m_result.order=ticket; this.m_result.price=(::OrderSelect(ticket,SELECT_BY_TICKET) ? ::OrderOpenPrice() : this.m_request.price); this.m_result.volume=(::OrderSelect(ticket,SELECT_BY_TICKET) ? ::OrderLots() : this.m_request.volume); this.m_result.comment=CMessage::Text(this.m_result.retcode); return true; } else { this.m_result.retcode=::GetLastError(); this.m_result.ask=this.m_tick.ask; this.m_result.bid=this.m_tick.bid; this.m_result.comment=CMessage::Text(this.m_result.retcode); return false; } #endif } //+------------------------------------------------------------------+

取引注文の価格も修正されました。以前は、チャートがLast価格に基づいていた場合、取引注文の価格はAskとLastに設定されていましたが、チャートの作成に使用される価格に関係なく、常にAskとBidになりました。

その他の小さな変更は以下に添付されているファイルで参照できるので、ここでは説明しません。

Trading.mqhファイルでは、CTrading取引クラスのprivateセクションに、保留中リクエストのリストと取引試行回数を保存する変数を追加します。

//+------------------------------------------------------------------+ //| Trading class | //+------------------------------------------------------------------+ class CTrading { private: CAccount *m_account; // Pointer to the current account object CSymbolsCollection *m_symbols; // Pointer to the symbol collection list CMarketCollection *m_market; // Pointer to the list of the collection of market orders and positions CHistoryCollection *m_history; // Pointer to the list of the collection of historical orders and deals CArrayObj m_list_request; // List of pending requests CArrayInt m_list_errors; // Error list bool m_is_trade_disable; // Flag disabling trading bool m_use_sound; // The flag of using sounds of the object trading events uchar m_total_try; // Number of trading attempts ENUM_LOG_LEVEL m_log_level; // Logging level MqlTradeRequest m_request; // Trading request prices ENUM_TRADE_REQUEST_ERR_FLAGS m_error_reason_flags; // Flags of error source in a trading method ENUM_ERROR_HANDLING_BEHAVIOR m_err_handling_behavior; // Behavior when handling error

将来的には、取引リクエストのリストを使用して、保留中リクエストクラスのオブジェクトを保存し、m_total_try変数には、コンストラクタで取引クラスにデフォルトで設定された取引試行回数が含まれます。

//+------------------------------------------------------------------+ //| コンストラクタ | //+------------------------------------------------------------------+ CTrading::CTrading() { this.m_list_errors.Clear(); this.m_list_errors.Sort(); this.m_list_request.Clear(); this.m_list_request.Sort(); this.m_total_try=TOTAL_TRY; this.m_log_level=LOG_LEVEL_ALL_MSG; this.m_is_trade_disable=false; this.m_err_handling_behavior=ERROR_HANDLING_BEHAVIOR_CORRECT; ::ZeroMemory(this.m_request); } //+------------------------------------------------------------------+

ここで、保留中リクエストのリストをクリアし、リストのソート済みフラグを設定します。

StopLimit型の注文のリミット注文の価格を、StopLevelに相対した価格を確認するメソッドのパラメータに追加します。

bool CheckPriceByStopLevel(const ENUM_ORDER_TYPE order_type,const double price,const CSymbol *symbol_obj,const double limit=0);

確認はメソッドそのものに追加します。

//+------------------------------------------------------------------+ //| Return the flag checking the validity of the distance | //| from the price to the placement level by StopLevel | //+------------------------------------------------------------------+ bool CTrading::CheckPriceByStopLevel(const ENUM_ORDER_TYPE order_type,const double price,const CSymbol *symbol_obj,const double limit=0) { double lv=symbol_obj.TradeStopLevel()*symbol_obj.Point(); double pr=(this.DirectionByActionType((ENUM_ACTION_TYPE)order_type)==ORDER_TYPE_BUY ? symbol_obj.Ask() : symbol_obj.Bid()); return (limit==0 ? //--- Order placement prices relative to the price ( order_type==ORDER_TYPE_SELL_STOP || order_type==ORDER_TYPE_SELL_STOP_LIMIT || order_type==ORDER_TYPE_BUY_LIMIT ? price<(pr-lv) : order_type==ORDER_TYPE_BUY_STOP || order_type==ORDER_TYPE_BUY_STOP_LIMIT || order_type==ORDER_TYPE_SELL_LIMIT ? price>(pr+lv) : true ) : //--- Limit order placement prices relative to the stop order price ( order_type==ORDER_TYPE_BUY_STOP_LIMIT ? limit<(price-lv) : order_type==ORDER_TYPE_SELL_STOP_LIMIT ? limit>(price+lv) : true ) ); } //+------------------------------------------------------------------+

ここで、リミット注文価格がゼロに等しい場合は、ストップおよびリミット注文の価格を確認し、そうでない場合はストップリミット注文価格を確認します(ストップリミット注文に相対したストップリミット注文に相対したリミット注文価格)。

エラーの処理方法を返すメソッドにエラーコードを渡し 、エラー修正メソッドで取引オブジェクトへのポインタを追加します。

//--- Return the error handling method ENUM_ERROR_CODE_PROCESSING_METHOD ResultProccessingMethod(const uint result_code); //--- Correct errors ENUM_ERROR_CODE_PROCESSING_METHOD RequestErrorsCorrecting(MqlTradeRequest &request,const ENUM_ORDER_TYPE order_type,const uint spread_multiplier,CSymbol *symbol_obj,CTradeObj *trade_obj);

ポジションを開くメソッドと注文するメソッドは複数ありますが、すべてがほぼ同じです。違いは、ポジションと注文の種類のみです。

各メソッドに同じコードを記述しないようにするには、 ポジションを開くメソッドと指値注文を出すメソッドの2つのプライベートメソッドを宣言して実装します。

//--- (1) Open a position, (2) place a pending order template<typename SL,typename TP> bool OpenPosition(const ENUM_POSITION_TYPE type, const double volume, const string symbol, const ulong magic=ULONG_MAX, const SL sl=0, const TP tp=0, const string comment=NULL, const ulong deviation=ULONG_MAX); template<typename PS,typename PL,typename SL,typename TP> bool PlaceOrder( const ENUM_ORDER_TYPE order_type, const double volume, const string symbol, const PS price_stop, const PL price_limit=0, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); public: //--- コンストラクタ

クラスのpublicセクションで、保留中リクエストの操作に必要となるタイマー、保留中リクエストを返すメソッド、取引の試行回数を設定するメソッドを宣言します。

public: //--- コンストラクタ CTrading(); //--- タイマー void OnTimer(void); //--- Get the pointers to the lists (make sure to call the method in program's OnInit() since the symbol collection list is created there) void OnInit(CAccount *account,CSymbolsCollection *symbols,CMarketCollection *market,CHistoryCollection *history) { this.m_account=account; this.m_symbols=symbols; this.m_market=market; this.m_history=history; } //--- Return the list of (1) errors and (2) pending requests CArrayInt *GetListErrors(void) { return &this.m_list_errors; } CArrayObj *GetListRequests(void) { return &this.m_list_request;} //--- Set the number of trading attempts void SetTotalTry(const uchar number) { this.m_total_try=number; } //--- Check limitations and errors

決済ボリュームでポジションを決済するメソッドの仕様を改善しましょう。デフォルトはWRONG_VALUE (完全決済)、さもなければ指定されたボリュームによる部分決済です。

bool ClosePosition(const ulong ticket,const double volume=WRONG_VALUE,const string comment=NULL,const ulong deviation=ULONG_MAX);

未決注文を出すメソッドの仕様で、超過注文の種類を追加します。以前は、クラスに設定されたデフォルト値が使用されていましたが、注文実行タイプの値は、メソッドに渡された値に基づいて選択されるようになりました。WRONG_VALUEの場合は、指定された値はデフォルトで設定され、そうでない場合はメソッドに渡された値が適用されます。

//--- Set (1) BuyStop, (2) BuyLimit, (3) BuyStopLimit pending order template<typename PS,typename SL,typename TP> bool PlaceBuyStop(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); template<typename PS,typename SL,typename TP> bool PlaceBuyLimit(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); template<typename PS,typename PL,typename SL,typename TP> bool PlaceBuyStopLimit(const double volume, const string symbol, const PS price_stop, const PL price_limit, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); //--- Set (1) SellStop, (2) SellLimit, (3) SellStopLimit pending order template<typename PS,typename SL,typename TP> bool PlaceSellStop(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); template<typename PS,typename SL,typename TP> bool PlaceSellLimit(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); template<typename PS,typename PL,typename SL,typename TP> bool PlaceSellStopLimit(const double volume, const string symbol, const PS price_stop, const PL price_limit, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); //--- Modify a pending order template<typename PS,typename PL,typename SL,typename TP> bool ModifyOrder(const ulong ticket, const PS price=WRONG_VALUE, const SL sl=WRONG_VALUE, const TP tp=WRONG_VALUE, const PL limit=WRONG_VALUE, datetime expiration=WRONG_VALUE, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE);

タイマーを実装しましょう。これまで、保留中リクエストのリストを処理するワークピースを準備します。

//+------------------------------------------------------------------+ //| Timer | //+------------------------------------------------------------------+ void CTrading::OnTimer(void) { int total=this.m_list_request.Total(); for(int i=total-1;i>WRONG_VALUE;i--) { } } //+------------------------------------------------------------------+

以下は、取引サーバの戻りコードを処理する方法を返すメソッドの実装です。

//+------------------------------------------------------------------+ //| Return the error handling method | //+------------------------------------------------------------------+ ENUM_ERROR_CODE_PROCESSING_METHOD CTrading::ResultProccessingMethod(const uint result_code) { switch(result_code) { #ifdef __MQL4__ //--- Malfunctional trade operation case 9 : //--- Account disabled case 64 : //--- Invalid account number case 65 : return ERROR_CODE_PROCESSING_METHOD_DISABLE; //--- No error but result is unknown case 1 : //--- General error case 2 : //--- Old client terminal version case 5 : //--- Not enough rights case 7 : //--- Market closed case 132 : //--- Trading disabled case 133 : //--- Order is locked and being processed case 139 : //--- Buy only case 140 : //--- The number of open and pending orders has reached the limit set by the broker case 148 : //--- Attempt to open an opposite order if hedging is disabled case 149 : //--- Attempt to close a position on a symbol contradicts the FIFO rule case 150 : return ERROR_CODE_PROCESSING_METHOD_EXIT; //--- Invalid trading request parameters case 3 : //--- Invalid price case 129 : //--- Invalid stop levels case 130 : //--- Invalid volume case 131 : //--- Not enough money to perform the operation case 134 : //--- Expirations are denied by broker case 147 : return ERROR_CODE_PROCESSING_METHOD_CORRECT; //--- Trade server is busy case 4 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- No connection to the trade server case 6 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Too frequent requests case 8 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)10000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- No price case 136 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Broker is busy case 137 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Too many requests case 141 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)10000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Modification denied because the order is too close to market case 145 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Trade context is busy case 146 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)1000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Trade timeout case 128 : //--- Price has changed case 135 : //--- New prices case 138 : return ERROR_CODE_PROCESSING_METHOD_REFRESH; //--- MQL5 #else //--- Auto trading disabled by the server case 10026 : return ERROR_CODE_PROCESSING_METHOD_DISABLE; //--- Request canceled by a trader case 10007 : //--- Request expired case 10012 : //--- Trading disabled case 10017 : //--- Market closed case 10018 : //--- Order status changed case 10023 : //--- Request unchanged case 10025 : //--- Request blocked for handling case 10028 : //--- Transaction is allowed for live accounts only case 10032 : //--- The maximum number of pending orders is reached case 10033 : //--- Reached the maximum order and position volume for this symbol case 10034 : //--- Invalid or prohibited order type case 10035 : //--- Position with the specified ID already closed case 10036 : //--- A close order is already present for a specified position case 10039 : //--- The maximum number of open positions is reached case 10040 : //--- Request to activate a pending order is rejected, the order is canceled case 10041 : //--- Request is rejected, because the rule "Only long positions are allowed" is set for the symbol case 10042 : //--- Request is rejected, because the rule "Only short positions are allowed" is set for the symbol case 10043 : //--- Request is rejected, because the rule "Only closing of existing positions is allowed" is set for the symbol case 10044 : //--- Request is rejected, because the rule "Only closing of existing positions by FIFO rule is allowed" is set for the symbol case 10045 : return ERROR_CODE_PROCESSING_METHOD_EXIT; //--- Requote case 10004 : //--- Request rejected case 10006 : //--- Prices changed case 10020 : return ERROR_CODE_PROCESSING_METHOD_REFRESH; //--- Invalid request case 10013 : //--- Invalid request volume case 10014 : //--- Invalid request price case 10015 : //--- Invalid request stop levels case 10016 : //--- Insufficient funds for request execution case 10019 : //--- Invalid order expiration in a request case 10022 : //--- The specified type of order execution by balance is not supported case 10030 : //--- Closed volume exceeds the current position volume case 10038 : return ERROR_CODE_PROCESSING_METHOD_CORRECT; //--- No quotes to process the request case 10021 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT; //--- Too frequent requests case 10024 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)10000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- An order or a position is frozen case 10029 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)10000; // ERROR_CODE_PROCESSING_METHOD_WAIT; //--- Request handling error case 10011 : return ERROR_CODE_PROCESSING_METHOD_PENDING; //--- Auto trading disabled by the client terminal case 10027 : return ERROR_CODE_PROCESSING_METHOD_PENDING; //--- No connection to the trade server case 10031 : return ERROR_CODE_PROCESSING_METHOD_PENDING; //--- Order placed case 10008 : //--- Request executed case 10009 : //--- Request executed partially case 10010 : #endif //--- "OK" default: break; } return ERROR_CODE_PROCESSING_METHOD_OK; } //+------------------------------------------------------------------+

ここではすべてが簡単です。メソッドは、取引リクエストを送信した後にサーバから取得したコードを受け取ります。次に、エラーを修正できることを示すコードがエラー修正メソッドで処理され、データの更新とリクエストの再送信が必要なコードは適切に処理されます。

MQL5およびMQL4サーバは異なるエラーコードを返すため、このメソッドはMQL4およびMQL5の条件付きコンパイルを特長としています。

同じタイプの処理を必要とするすべてのコードは、switch演算子の単一のcaseにグループ化され、取引サーバの戻りコードを処理する統一されたメソッドを返します。

以下は、取引サーバエラーを処理するメソッドの実装です。

//+------------------------------------------------------------------+ //| Correct errors | //+------------------------------------------------------------------+ ENUM_ERROR_CODE_PROCESSING_METHOD CTrading::RequestErrorsCorrecting(MqlTradeRequest &request, const ENUM_ORDER_TYPE order_type, const uint spread_multiplier, CSymbol *symbol_obj, CTradeObj *trade_obj) { //--- The empty error list means no errors are detected, return success int total=this.m_list_errors.Total(); if(total==0) return ERROR_CODE_PROCESSING_METHOD_OK; //--- Trading is disabled for the current account //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_ACCOUNT_NOT_TRADE_ENABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_ACCOUNT_NOT_TRADE_ENABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Trading on the trading server side is disabled for EAs on the current account //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_ACCOUNT_EA_NOT_TRADE_ENABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_ACCOUNT_EA_NOT_TRADE_ENABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Trading operations are disabled in the terminal //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_TERMINAL_NOT_TRADE_ENABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_TERMINAL_NOT_TRADE_ENABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Trading operations are disabled for the EA //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_EA_NOT_TRADE_ENABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_EA_NOT_TRADE_ENABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Disable trading on a symbol //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_TRADE_MODE_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_TRADE_MODE_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Close only //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_TRADE_MODE_CLOSEONLY)) { trade_obj.SetResultRetcode(MSG_SYM_TRADE_MODE_CLOSEONLY); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Market orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_MARKET_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_MARKET_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Limit orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_LIMIT_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_LIMIT_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Stop orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_STOP_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_STOP_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- StopLimit orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_STOP_LIMIT_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_STOP_LIMIT_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Sell only //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_TRADE_MODE_SHORTONLY)) { trade_obj.SetResultRetcode(MSG_SYM_TRADE_MODE_SHORTONLY); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Buy only //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_TRADE_MODE_LONGONLY)) { trade_obj.SetResultRetcode(MSG_SYM_TRADE_MODE_LONGONLY); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- CloseBy orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_CLOSE_BY_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_CLOSE_BY_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Exceeded maximum allowed aggregate volume of orders and positions in one direction //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_MAX_VOLUME_LIMIT_EXCEEDED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_MAX_VOLUME_LIMIT_EXCEEDED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Close by is disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_CLOSE_BY_ORDERS_DISABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_CLOSE_BY_ORDERS_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Symbols of opposite positions are not equal //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_CLOSE_BY_SYMBOLS_UNEQUAL)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_CLOSE_BY_SYMBOLS_UNEQUAL); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Unsupported price parameter type in a request //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_UNSUPPORTED_PRICE_TYPE_IN_REQ)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_UNSUPPORTED_PRICE_TYPE_IN_REQ); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Trading disabled for the EA until the reason is eliminated //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_TRADING_DISABLE)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_TRADING_DISABLE); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- The maximum number of pending orders is reached //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(10033)) { trade_obj.SetResultRetcode(10033); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Reached the maximum order and position volume for this symbol //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(10034)) { trade_obj.SetResultRetcode(10034); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Correcting trading request parameters //--- Price, according to which stop orders are placed double price_set=(this.IsPresentErrorFlag(TRADE_REQUEST_ERR_FLAG_PRICE_ERROR) ? request.price : request.stoplimit); //--- First, adjust stop orders relative to the order/position level if(this.IsPresentErorCode(MSG_LIB_TEXT_SL_LESS_STOP_LEVEL)) request.sl=this.CorrectStopLoss(order_type,price_set,request.sl,symbol_obj,spread_multiplier); if(this.IsPresentErorCode(MSG_LIB_TEXT_TP_LESS_STOP_LEVEL)) request.tp=this.CorrectTakeProfit(order_type,price_set,request.tp,symbol_obj,spread_multiplier); //--- Pending orders price double shift=0; if(this.IsPresentErrorFlag(TRADE_REQUEST_ERR_FLAG_PRICE_ERROR)) { price_set=request.price; request.price=this.CorrectPricePending(order_type,price_set,0,symbol_obj,spread_multiplier); shift=request.price-price_set; //--- If this is not a stop limit order, move stop orders by the calculated correcting order level shift if(request.stoplimit==0) { if(request.sl>0) request.sl=this.CorrectStopLoss(order_type,request.price,request.sl+shift,symbol_obj,spread_multiplier); if(request.tp>0) request.tp=this.CorrectTakeProfit(order_type,request.price,request.tp+shift,symbol_obj,spread_multiplier); } } //--- The specified type of order execution by balance is not supported if(this.IsPresentErorCode(10030)) request.type_filling=symbol_obj.GetCorrectTypeFilling(); //--- Invalid order expiration in a request - if(this.IsPresentErorCode(10022)) { //--- if the expiration type is not supported as set by the expiration date and the expiration data is defined, reset the expiration date if(!symbol_obj.IsExpirationModeSpecified() && request.expiration>0) request.expiration=0; } //--- View the list of remaining errors and correct trading request parameters for(int i=0;i<total;i++) { int err=this.m_list_errors.At(i); if(err==NULL) continue; switch(err) { //--- Correct an invalid volume and disabling stop levels in a trading request case MSG_LIB_TEXT_REQ_VOL_LESS_MIN_VOLUME : case MSG_LIB_TEXT_REQ_VOL_MORE_MAX_VOLUME : case MSG_LIB_TEXT_INVALID_VOLUME_STEP : request.volume=symbol_obj.NormalizedLot(request.volume); break; case MSG_SYM_SL_ORDER_DISABLED : request.sl=0; break; case MSG_SYM_TP_ORDER_DISABLED : request.tp=0; break; //--- If unable to select the position lot, return "abort trading attempt" since the funds are insufficient even for the minimum lot case MSG_LIB_TEXT_NOT_ENOUTH_MONEY_FOR : request.volume=this.CorrectVolume(request.price,order_type,symbol_obj,DFUN); if(request.volume==0) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_NOT_POSSIBILITY_CORRECT_LOT); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; break; } //--- No quotes to process the request case 10021 : trade_obj.SetResultRetcode(10021); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT - wait 5 seconds //--- No connection to the trade server case 10031 : trade_obj.SetResultRetcode(10031); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT - wait 5 seconds //--- Proximity to the order activation level is handled by five-second waiting - during this time, the price may go beyond the freeze level case MSG_LIB_TEXT_SL_LESS_FREEZE_LEVEL : case MSG_LIB_TEXT_TP_LESS_FREEZE_LEVEL : case MSG_LIB_TEXT_PR_LESS_FREEZE_LEVEL : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT - wait 5 seconds default: break; } } //--- No errors - return ОК trade_obj.SetResultRetcode(0); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_OK; } //+------------------------------------------------------------------+

メソッドリストのコードコメントには、取引サーバから返されたエラーの処理を目的としたすべてのアクションが含まれています。

ポジションを開くためのプライベートメソッドを実装します。

//+------------------------------------------------------------------+ //| Open a position | //+------------------------------------------------------------------+ template<typename SL,typename TP> bool CTrading::OpenPosition(const ENUM_POSITION_TYPE type, const double volume, const string symbol, const ulong magic=ULONG_MAX, const SL sl=0, const TP tp=0, const string comment=NULL, const ulong deviation=ULONG_MAX) { //--- Set the trading request result as 'true' and the error flag as "no errors" bool res=true; this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_NO_ERROR; ENUM_ORDER_TYPE order_type=(ENUM_ORDER_TYPE)type; ENUM_ACTION_TYPE action=(ENUM_ACTION_TYPE)order_type; //--- Get a symbol object by a symbol name. If failed to get CSymbol *symbol_obj=this.m_symbols.GetSymbolObjByName(symbol); //--- If failed to get - write the "internal error" flag, display the message in the journal and return 'false' if(symbol_obj==NULL) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_ERROR_FAILED_GET_SYM_OBJ)); return false; } //--- get a trading object from a symbol object CTradeObj *trade_obj=symbol_obj.GetTradeObj(); //--- If failed to get - write the "internal error" flag, display the message in the journal and return 'false' if(trade_obj==NULL) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_ERROR_FAILED_GET_TRADE_OBJ)); return false; } //--- Set the prices //--- If failed to set - write the "internal error" flag, set the error code in the return structure, //--- display the message in the journal and return 'false' if(!this.SetPrices(order_type,0,sl,tp,0,DFUN,symbol_obj)) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; trade_obj.SetResultRetcode(10021); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(10021)); // No quotes to process the request return false; } //--- Write the volume to the request structure this.m_request.volume=volume; //--- Get the method of handling errors from the CheckErrors() method while checking for errors in the request parameters ENUM_ERROR_CODE_PROCESSING_METHOD method=this.CheckErrors(this.m_request.volume,symbol_obj.Ask(),action,order_type,symbol_obj,trade_obj,DFUN,0,this.m_request.sl,this.m_request.tp); //--- In case of trading limitations, funds insufficiency, //--- if there are limitations by StopLevel or FreezeLevel ... if(method!=ERROR_CODE_PROCESSING_METHOD_OK) { //--- If trading is completely disabled, set the error code to the return structure, //--- display a journal message, play the error sound and exit if(method==ERROR_CODE_PROCESSING_METHOD_DISABLE) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_TRADING_DISABLE); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRADING_DISABLE)); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); return false; } //--- If the check result is "abort trading operation" - set the last error code to the return structure, //--- display a journal message, play the error sound and exit if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { int code=this.m_list_errors.At(this.m_list_errors.Total()-1); if(code!=NULL) { trade_obj.SetResultRetcode(code); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); } if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRADING_OPERATION_ABORTED)); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); return false; } //--- If the check result is "waiting" - set the last error code to the return structure and display the message in the journal if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { int code=this.m_list_errors.At(this.m_list_errors.Total()-1); if(code!=NULL) { trade_obj.SetResultRetcode(code); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); } if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_CREATE_PENDING_REQUEST)); //--- Instead of creating a pending request, we temporarily wait the required time period (the CheckErrors() method result is returned) ::Sleep(method); //--- after waiting, update all data symbol_obj.Refresh(); } //--- If the check result is "create a pending request", do nothing temporarily if(this.m_err_handling_behavior==ERROR_HANDLING_BEHAVIOR_PENDING_REQUEST) { if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_CREATE_PENDING_REQUEST)); } } //--- In the loop by the number of attempts for(int i=0;i<this.m_total_try;i++) { //--- Send the request res=trade_obj.OpenPosition(type,this.m_request.volume,this.m_request.sl,this.m_request.tp,magic,comment,deviation); //--- If the request is executed successfully or the asynchronous order sending mode is set, play the success sound //--- set for a symbol trading object for this type of trading operation and return 'true' if(res || trade_obj.IsAsyncMode()) { if(this.IsUseSounds()) trade_obj.PlaySoundSuccess(action,order_type); return true; } //--- If the request is not successful, play the error sound set for a symbol trading object for this type of trading operation else { if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRY_N),string(i+1),". ",CMessage::Text(MSG_LIB_SYS_ERROR),": ",CMessage::Text(trade_obj.GetResultRetcode())); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); //--- Get the error handling method method=this.ResultProccessingMethod(trade_obj.GetResultRetcode()); //--- If "Disable trading for the EA" is received as a result of sending a request, enable the disabling flag and end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_DISABLE) { this.SetTradingDisableFlag(true); break; } //--- If "Exit the trading method" is received as a result of sending a request, end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { break; } //--- If "Correct the parameters and repeat" is received as a result of sending a request - //--- correct the parameters and start the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_CORRECT) { this.RequestErrorsCorrecting(this.m_request,order_type,trade_obj.SpreadMultiplier(),symbol_obj,trade_obj); continue; } //--- If "Update data and repeat" is received as a result of sending a request - //--- update data and start the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_REFRESH) { symbol_obj.Refresh(); continue; } //--- If "Wait and repeat" is received as a result of sending a request - //--- in this implementation, we wait the number of milliseconds equal to the 'method' value and move on to the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_WAIT) { ::Sleep(method); continue; } //--- If "Create a pending request" is received as a result of sending a request - //--- create a pending request with the trading request parameters and end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_PENDING) { break; } } } //--- Return the result of sending a trading request in a symbol trading object return res; } //+------------------------------------------------------------------+このメソッドは、コードで直接詳細にコメントされており、買いおよび売りのポジションを開くために使用されます。

//+------------------------------------------------------------------+ //| Open Buy position | //+------------------------------------------------------------------+ template<typename SL,typename TP> bool CTrading::OpenBuy(const double volume, const string symbol, const ulong magic=ULONG_MAX, const SL sl=0, const TP tp=0, const string comment=NULL, const ulong deviation=ULONG_MAX) { //--- Return the result of sending a trading request from the OpenPosition() method return this.OpenPosition(POSITION_TYPE_BUY,volume,symbol,magic,sl,tp,comment,deviation); } //+------------------------------------------------------------------+ //| Open a Sell position | //+------------------------------------------------------------------+ template<typename SL,typename TP> bool CTrading::OpenSell(const double volume, const string symbol, const ulong magic=ULONG_MAX, const SL sl=0, const TP tp=0, const string comment=NULL, const ulong deviation=ULONG_MAX) { //--- Return the result of sending a trading request from the OpenPosition() method return this.OpenPosition(POSITION_TYPE_SELL,volume,symbol,magic,sl,tp,comment,deviation); } //+------------------------------------------------------------------+

開かれたポジションタイプを示すポジションを開くための一般的なプライベートメソッドは、これらのメソッドで単に呼び出されます。

以下は、指値注文を出すためのプライベートメソッドの実装です。

//+------------------------------------------------------------------+ //| Place a pending order | //+------------------------------------------------------------------+ template<typename PS,typename PL,typename SL,typename TP> bool CTrading::PlaceOrder(const ENUM_ORDER_TYPE order_type, const double volume, const string symbol, const PS price_stop, const PL price_limit=0, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { bool res=true; this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_NO_ERROR; ENUM_ACTION_TYPE action=(ENUM_ACTION_TYPE)order_type; //--- Get a symbol object by a symbol name CSymbol *symbol_obj=this.m_symbols.GetSymbolObjByName(symbol); if(symbol_obj==NULL) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_ERROR_FAILED_GET_SYM_OBJ)); return false; } //--- Get a trading object from a symbol object CTradeObj *trade_obj=symbol_obj.GetTradeObj(); if(trade_obj==NULL) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_ERROR_FAILED_GET_TRADE_OBJ)); return false; } //--- Set the prices //--- If failed to set - write the "internal error" flag, set the error code in the return structure, //--- display the message in the journal and return 'false' if(!this.SetPrices(order_type,price_stop,sl,tp,price_limit,DFUN,symbol_obj)) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; trade_obj.SetResultRetcode(10021); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(10021)); // No quotes to process the request return false; } //--- In case of trading limitations, funds insufficiency, //--- there are limitations on StopLevel - play the error sound and exit this.m_request.volume=volume; this.m_request.type_filling=type_filling; this.m_request.type_time=type_time; this.m_request.expiration=expiration; ENUM_ERROR_CODE_PROCESSING_METHOD method=this.CheckErrors(this.m_request.volume, this.m_request.price, action, order_type, symbol_obj, trade_obj, DFUN, this.m_request.stoplimit, this.m_request.sl, this.m_request.tp); if(method!=ERROR_CODE_PROCESSING_METHOD_OK) { //--- If trading is completely disabled if(method==ERROR_CODE_PROCESSING_METHOD_DISABLE) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_TRADING_DISABLE); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRADING_DISABLE)); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); return false; } //--- If the check result is "abort trading operation" - set the last error code to the return structure, //--- display a journal message, play the error sound and exit if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { int code=this.m_list_errors.At(this.m_list_errors.Total()-1); if(code!=NULL) { trade_obj.SetResultRetcode(code); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); } if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRADING_OPERATION_ABORTED)); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); return false; } //--- If the check result is "waiting" - set the last error code to the return structure and display the message in the journal if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { int code=this.m_list_errors.At(this.m_list_errors.Total()-1); if(code!=NULL) { trade_obj.SetResultRetcode(code); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); } if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_CREATE_PENDING_REQUEST)); //--- Instead of creating a pending request, we temporarily wait the required time period (the CheckErrors() method result is returned) ::Sleep(method); symbol_obj.Refresh(); } //--- If the check result is "create a pending request", do nothing temporarily if(this.m_err_handling_behavior==ERROR_HANDLING_BEHAVIOR_PENDING_REQUEST) { if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_CREATE_PENDING_REQUEST)); } } //--- In the loop by the number of attempts for(int i=0;i<this.m_total_try;i++) { //--- Send the request res=trade_obj.SetOrder(order_type, this.m_request.volume, this.m_request.price, this.m_request.sl, this.m_request.tp, this.m_request.stoplimit, magic, comment, this.m_request.expiration, this.m_request.type_time, this.m_request.type_filling); //--- If the request is executed successfully or the asynchronous order sending mode is set, play the success sound //--- set for a symbol trading object for this type of trading operation and return 'true' if(res || trade_obj.IsAsyncMode()) { if(this.IsUseSounds()) trade_obj.PlaySoundSuccess(action,order_type); return true; } //--- If the request is not successful, play the error sound set for a symbol trading object for this type of trading operation else { if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRY_N),string(i+1),". ",CMessage::Text(MSG_LIB_SYS_ERROR),": ",CMessage::Text(trade_obj.GetResultRetcode())); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); method=this.ResultProccessingMethod(trade_obj.GetResultRetcode()); //--- If "Disable trading for the EA" is received as a result of sending a request, enable the disabling flag and end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_DISABLE) { this.SetTradingDisableFlag(true); break; } //--- If "Exit the trading method" is received as a result of sending a request, end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { break; } //--- If "Correct the parameters and repeat" is received as a result of sending a request - //--- correct the parameters and start the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_CORRECT) { this.RequestErrorsCorrecting(this.m_request,order_type,trade_obj.SpreadMultiplier(),symbol_obj,trade_obj); continue; } //--- If "Update data and repeat" is received as a result of sending a request - //--- update data and start the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_REFRESH) { symbol_obj.Refresh(); continue; } //--- If "Wait and repeat" is received as a result of sending a request - //--- in this implementation, we wait the number of milliseconds equal to the 'method' value and move on to the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_WAIT) { Sleep(method); continue; } //--- If "Create a pending request" is received as a result of sending a request - //--- create a pending request with the trading request parameters and end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_PENDING) { break; } } } //--- Return the result of sending a trading request in a symbol trading object return res; } //+------------------------------------------------------------------+

このメソッドは、コードで直接詳細にコメントされており、さまざまな種類の指値注文を設定するために使用されます。

//+------------------------------------------------------------------+ //| Place BuyStop pending order | //+------------------------------------------------------------------+ template<typename PS,typename SL,typename TP> bool CTrading::PlaceBuyStop(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_BUY_STOP,volume,symbol,price,0,sl,tp,magic,comment,expiration,type_time,type_filling); } //+------------------------------------------------------------------+ //| Place BuyLimit pending order | //+------------------------------------------------------------------+ template<typename PS,typename SL,typename TP> bool CTrading::PlaceBuyLimit(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_BUY_LIMIT,volume,symbol,price,0,sl,tp,magic,comment,expiration,type_time,type_filling); } //+------------------------------------------------------------------+ //| Place BuyStopLimit pending order | //+------------------------------------------------------------------+ template<typename PS,typename PL,typename SL,typename TP> bool CTrading::PlaceBuyStopLimit(const double volume, const string symbol, const PS price_stop, const PL price_limit, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { #ifdef __MQL5__ //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_BUY_STOP_LIMIT,volume,symbol,price_stop,price_limit,sl,tp,magic,comment,expiration,type_time,type_filling); //--- MQL4 #else return true; #endif } //+------------------------------------------------------------------+ //| Place SellStop pending order | //+------------------------------------------------------------------+ template<typename PS,typename SL,typename TP> bool CTrading::PlaceSellStop(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_SELL_STOP,volume,symbol,price,0,sl,tp,magic,comment,expiration,type_time,type_filling); } //+------------------------------------------------------------------+ //| Place SellLimit pending order | //+------------------------------------------------------------------+ template<typename PS,typename SL,typename TP> bool CTrading::PlaceSellLimit(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_SELL_LIMIT,volume,symbol,price,0,sl,tp,magic,comment,expiration,type_time,type_filling); } //+------------------------------------------------------------------+ //| Place SellStopLimit pending order | //+------------------------------------------------------------------+ template<typename PS,typename PL,typename SL,typename TP> bool CTrading::PlaceSellStopLimit(const double volume, const string symbol, const PS price_stop, const PL price_limit, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { #ifdef __MQL5__ //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_SELL_STOP_LIMIT,volume,symbol,price_stop,price_limit,sl,tp,magic,comment,expiration,type_time,type_filling); //--- MQL4 #else return true; #endif } //+------------------------------------------------------------------+

残りのメソッドは、ポジションを決済して未決注文を削除するために必要です。ポジションと注文を変更するメソッドは、ポジションを開く/未決注文を出すプライベートメソッドに似ています。すべてのメソッドコードには詳細なコメントがあります。すべてのファイルは以下に添付されています。

これで、この段階での取引クラスでのすべての作業が完了します。

後は、ライブラリのCEngine基本オブジェクトクラスに変更を加えるだけです。

最小ストップおよび指値注文レベル(StopLevel)の変動性を考慮すると、特定の値を乗じたスプレッドがしばしば許容可能なストップ注文距離を指定するために使用されるため、スプレッド乗数を設定する必要があります。これは、取引クラスのスプレッド乗数を設定できるメソッドが必要であることを意味します。

クラスのpublicセクションで以下のメソッドを宣言します。

//--- Set the spread multiplier for symbol trading objects in the symbol collection void SetSpreadMultiplier(const uint value=1,const string symbol=NULL) { this.m_trading.SetSpreadMultiplier(value,symbol); } //--- Open (1) Buy, (2) Sell position

このメソッドは、以前に調査した前の記事で既に調べた同じ名前の取引クラスメソッドを呼び出すだけで、使用するすべての銘柄に単一の共通乗数と指定した銘柄に個別の乗数の両方を設定できます。

取引クラスはすぐにタイマーを使用して保留中リクエストを処理するため、CEngineクラスコンストラクタで 取引クラスの新しいタイマーカウンターを作成します

//+------------------------------------------------------------------+ //| CEngineコンストラクタ | //+------------------------------------------------------------------+ CEngine::CEngine() : m_first_start(true), m_last_trade_event(TRADE_EVENT_NO_EVENT), m_last_account_event(WRONG_VALUE), m_last_symbol_event(WRONG_VALUE), m_global_error(ERR_SUCCESS) { this.m_is_hedge=#ifdef __MQL4__ true #else bool(::AccountInfoInteger(ACCOUNT_MARGIN_MODE)==ACCOUNT_MARGIN_MODE_RETAIL_HEDGING) #endif; this.m_is_tester=::MQLInfoInteger(MQL_TESTER); this.m_list_counters.Sort(); this.m_list_counters.Clear(); this.CreateCounter(COLLECTION_ORD_COUNTER_ID,COLLECTION_ORD_COUNTER_STEP,COLLECTION_ORD_PAUSE); this.CreateCounter(COLLECTION_ACC_COUNTER_ID,COLLECTION_ACC_COUNTER_STEP,COLLECTION_ACC_PAUSE); this.CreateCounter(COLLECTION_SYM_COUNTER_ID1,COLLECTION_SYM_COUNTER_STEP1,COLLECTION_SYM_PAUSE1); this.CreateCounter(COLLECTION_SYM_COUNTER_ID2,COLLECTION_SYM_COUNTER_STEP2,COLLECTION_SYM_PAUSE2); this.CreateCounter(COLLECTION_REQ_COUNTER_ID,COLLECTION_REQ_COUNTER_STEP,COLLECTION_REQ_PAUSE); ::ResetLastError(); #ifdef __MQL5__ if(!::EventSetMillisecondTimer(TIMER_FREQUENCY)) { ::Print(DFUN_ERR_LINE,CMessage::Text(MSG_LIB_SYS_FAILED_CREATE_TIMER),(string)::GetLastError()); this.m_global_error=::GetLastError(); } //---__MQL4__ #else if(!this.IsTester() && !::EventSetMillisecondTimer(TIMER_FREQUENCY)) { ::Print(DFUN_ERR_LINE,CMessage::Text(MSG_LIB_SYS_FAILED_CREATE_TIMER),(string)::GetLastError()); this.m_global_error=::GetLastError(); } #endif //--- } //+------------------------------------------------------------------+

CEngineクラスタイマーに、取引クラスタイマーを使用するブロックを追加します。

//+------------------------------------------------------------------+ //| CEngineタイマー | //+------------------------------------------------------------------+ void CEngine::OnTimer(void) { //--- 過去の注文と取引、および成行注文とポジションの収集のタイマー int index=this.CounterIndex(COLLECTION_ORD_COUNTER_ID); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If unpaused, work with the order, deal and position collections events if(counter.IsTimeDone()) this.TradeEventsControl(); } //--- If this is a tester, work with collection events by tick else this.TradeEventsControl(); } } //--- Account collection timer index=this.CounterIndex(COLLECTION_ACC_COUNTER_ID); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If unpaused, work with the account collection events if(counter.IsTimeDone()) this.AccountEventsControl(); } //--- If this is a tester, work with collection events by tick else this.AccountEventsControl(); } } //--- Timer 1 of the symbol collection (updating symbol quote data in the collection) index=this.CounterIndex(COLLECTION_SYM_COUNTER_ID1); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If the pause is over, update quote data of all symbols in the collection if(counter.IsTimeDone()) this.m_symbols.RefreshRates(); } //--- In case of a tester, update quote data of all collection symbols by tick else this.m_symbols.RefreshRates(); } } //--- Timer 2 of the symbol collection (updating all data of all symbols in the collection and tracking symbl and symbol search events in the market watch window) index=this.CounterIndex(COLLECTION_SYM_COUNTER_ID2); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If the pause is over if(counter.IsTimeDone()) { //--- update data and work with events of all symbols in the collection this.SymbolEventsControl(); //--- When working with the market watch list, check the market watch window events if(this.m_symbols.ModeSymbolsList()==SYMBOLS_MODE_MARKET_WATCH) this.MarketWatchEventsControl(); } } //--- If this is a tester, work with events of all symbols in the collection by tick else this.SymbolEventsControl(); } } //--- Trading class timer index=this.CounterIndex(COLLECTION_REQ_COUNTER_ID); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If unpaused, work with the list of pending requests if(counter.IsTimeDone()) this.m_trading.OnTimer(); } //--- In case of the tester, work with the list of pending orders by tick else this.m_trading.OnTimer(); } } } //+------------------------------------------------------------------+

ポジションの完全決済のメソッドをわずかに変更します。

//+------------------------------------------------------------------+ //| Close a position in full | //+------------------------------------------------------------------+ bool CEngine::ClosePosition(const ulong ticket,const string comment=NULL,const ulong deviation=ULONG_MAX) { return this.m_trading.ClosePosition(ticket,WRONG_VALUE,comment,deviation); } //+------------------------------------------------------------------+

現在、完全決済と部分決済の両方に共通のポジション決済メソッドがあるため、完全なポジション決済のポジション決済ボリュームとして-1を渡す必要があります。

これで、取引サーバの戻りコードの処理に必要な変更と改善が完了しました。

テスト

取引サーバから返されたエラーの処理を確認するには、実行遅延など、エラーの原因となる取引条件を設定するのが合理的です。遅延中に、価格が変化して適切なエラーが発生します。

テストを実行するには、前の記事のEAを使用して、 \MQL5\Experts\TestDoEasy\Part25\でTestDoEasyPart25.mq5として保存します。

EAを変更せずに起動できますが、最初にいくつかの改善を行ってみましょう。

EA入力のブロックで、デフォルトのスリッページをゼロから5ポイントに変更し、スプレッド乗数を追加します。

//--- 入力変数 input ulong InpMagic = 123; // Magic number input double InpLots = 0.1; // Lots input uint InpStopLoss = 50; // StopLoss in points input uint InpTakeProfit = 50; // TakeProfit in points input uint InpDistance = 50; // Pending orders distance (points) input uint InpDistanceSL = 50; // StopLimit orders distance (points) input uint InpSlippage = 5; // Slippage in points input uint InpSpreadMultiplier = 1; // Spread multiplier for adjusting stop-orders by StopLevel sinput double InpWithdrawal = 10; // Withdrawal funds (in tester) sinput uint InpButtShiftX = 40; // Buttons X shift sinput uint InpButtShiftY = 10; // Buttons Y shift input uint InpTrailingStop = 50; // Trailing Stop (points) input uint InpTrailingStep = 20; // Trailing Step (points) input uint InpTrailingStart = 0; // Trailing Start (points) input uint InpStopLossModify = 20; // StopLoss for modification (points) input uint InpTakeProfitModify = 60; // TakeProfit for modification (points) sinput ENUM_SYMBOLS_MODE InpModeUsedSymbols = SYMBOLS_MODE_CURRENT; // Mode of used symbols list sinput string InpUsedSymbols = "EURUSD,AUDUSD,EURAUD,EURCAD,EURGBP,EURJPY,EURUSD,GBPUSD,NZDUSD,USDCAD,USDJPY"; // List of used symbols (comma - separator) sinput bool InpUseSounds = true; // Use sounds

ライブラリ初期化関数で、使用されているすべての銘柄のすべての取引オブジェクトにスプレッド乗数を設定して銘柄パラメータ値の増加に対するブロック設定制御をコメントアウトして追跡および

テスタージャーナルへの冗長エントリの送信を避けます。

//+------------------------------------------------------------------+ //| Initializing DoEasy library | //+------------------------------------------------------------------+ void OnInitDoEasy() { //--- Check if working with the full list is selected used_symbols_mode=InpModeUsedSymbols; if((ENUM_SYMBOLS_MODE)used_symbols_mode==SYMBOLS_MODE_ALL) { int total=SymbolsTotal(false); string ru_n="\nКоличество символов на сервере "+(string)total+".\nМаксимальное количество: "+(string)SYMBOLS_COMMON_TOTAL+" символов."; string en_n="\nNumber of symbols on server "+(string)total+".\nMaximum number: "+(string)SYMBOLS_COMMON_TOTAL+" symbols."; string caption=TextByLanguage("Внимание!","Attention!"); string ru="Выбран режим работы с полным списком.\nВ этом режиме первичная подготовка списка коллекции символов может занять длительное время."+ru_n+"\nПродолжить?\n\"Нет\" - работа с текущим символом \""+Symbol()+"\""; string en="Full list mode selected.\nIn this mode, the initial preparation of the collection symbols list may take a long time."+en_n+"\nContinue?\n\"No\" - working with the current symbol \""+Symbol()+"\""; string message=TextByLanguage(ru,en); int flags=(MB_YESNO | MB_ICONWARNING | MB_DEFBUTTON2); int mb_res=MessageBox(message,caption,flags); switch(mb_res) { case IDNO : used_symbols_mode=SYMBOLS_MODE_CURRENT; break; default: break; } } //--- Fill in the array of used symbols used_symbols=InpUsedSymbols; CreateUsedSymbolsArray((ENUM_SYMBOLS_MODE)used_symbols_mode,used_symbols,array_used_symbols); //--- Set the type of the used symbol list in the symbol collection engine.SetUsedSymbols(array_used_symbols); //--- Displaying the selected mode of working with the symbol object collection Print(engine.ModeSymbolsListDescription(),TextByLanguage(". Number of used symbols: ",". Number of symbols used: "),engine.GetSymbolsCollectionTotal()); //--- Create resource text files engine.CreateFile(FILE_TYPE_WAV,"sound_array_coin_01",TextByLanguage("Звук упавшей монетки 1","Falling coin 1"),sound_array_coin_01); engine.CreateFile(FILE_TYPE_WAV,"sound_array_coin_02",TextByLanguage("Звук упавших монеток","Falling coins"),sound_array_coin_02); engine.CreateFile(FILE_TYPE_WAV,"sound_array_coin_03",TextByLanguage("Звук монеток","Coins"),sound_array_coin_03); engine.CreateFile(FILE_TYPE_WAV,"sound_array_coin_04",TextByLanguage("Звук упавшей монетки 2","Falling coin 2"),sound_array_coin_04); engine.CreateFile(FILE_TYPE_WAV,"sound_array_click_01",TextByLanguage("Звук щелчка по кнопке 1","Button click 1"),sound_array_click_01); engine.CreateFile(FILE_TYPE_WAV,"sound_array_click_02",TextByLanguage("Звук щелчка по кнопке 2","Button click 2"),sound_array_click_02); engine.CreateFile(FILE_TYPE_WAV,"sound_array_click_03",TextByLanguage("Звук щелчка по кнопке 3","Button click 3"),sound_array_click_03); engine.CreateFile(FILE_TYPE_WAV,"sound_array_cash_machine_01",TextByLanguage("Звук кассового аппарата","Cash machine"),sound_array_cash_machine_01); engine.CreateFile(FILE_TYPE_BMP,"img_array_spot_green",TextByLanguage("Изображение \"Зелёный светодиод\"","Image \"Green Spot lamp\""),img_array_spot_green); engine.CreateFile(FILE_TYPE_BMP,"img_array_spot_red",TextByLanguage("Изображение \"Красный светодиод\"","Image \"Red Spot lamp\""),img_array_spot_red); //--- Pass all existing collections to the trading class engine.TradingOnInit(); //--- Set synchronous passing of orders for all used symbols engine.TradingSetAsyncMode(false); //--- Set standard sounds for trading objects of all used symbols engine.SetSoundsStandart(); //--- Set the general flag of using sounds engine.SetUseSounds(InpUseSounds); //--- Set the spread multiplier for symbol trading objects in the symbol collection engine.SetSpreadMultiplier(InpSpreadMultiplier); //--- Set controlled values for symbols //--- Get the list of all collection symbols CArrayObj *list=engine.GetListAllUsedSymbols(); if(list!=NULL && list.Total()!=0) { //--- In a loop by the list, set the necessary values for tracked symbol properties //--- By default, the LONG_MAX value is set to all properties, which means "Do not track this property" //--- It can be enabled or disabled (by setting the value less than LONG_MAX or vice versa - set the LONG_MAX value) at any time and anywhere in the program /* for(int i=0;i<list.Total();i++) { CSymbol* symbol=list.At(i); if(symbol==NULL) continue; //--- Set control of the symbol price increase by 100 points symbol.SetControlBidInc(100000*symbol.Point()); //--- Set control of the symbol price decrease by 100 points symbol.SetControlBidDec(100000*symbol.Point()); //--- Set control of the symbol spread increase by 40 points symbol.SetControlSpreadInc(400); //--- Set control of the symbol spread decrease by 40 points symbol.SetControlSpreadDec(400); //--- Set control of the current spread by the value of 40 points symbol.SetControlSpreadLevel(400); } */ } //--- Set controlled values for the current account CAccount* account=engine.GetAccountCurrent(); if(account!=NULL) { //--- Set control of the profit increase to 10 account.SetControlledValueINC(ACCOUNT_PROP_PROFIT,10.0); //--- Set control of the funds increase to 15 account.SetControlledValueINC(ACCOUNT_PROP_EQUITY,15.0); //--- Set profit control level to 20 account.SetControlledValueLEVEL(ACCOUNT_PROP_PROFIT,20.0); } } //+------------------------------------------------------------------+

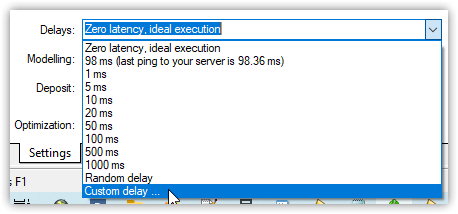

ストラテジーテスターで4秒の実行遅延を設定します。

これを行うには、ドロップダウンメニューで[カスタム遅延...]を選択します

新しい入力フィールドには4000ミリ秒を入力します。

![]()

これで、サーバに送信されたすべての取引注文がテスターで4秒間遅延します。

EAをビジュアルモードで起動し、いくつかのポジションを開いてから、高速市場でそれらを閉じます。

ご覧のとおり、再クォートを取得するときに常にポジションを開けるとは限りません。EAは必要な回数の取引を試行します(デフォルトは5回以下です)。これは、試行回数を指定し、「再クォート」の明確化を特徴とする「取引試行」エントリによって確認されます。ポジションを同時に決済する場合、再クォートを再度取得します。5回試行した後の最後のポジションが決済されることはありません。何回か失敗した後、手動で決済しました。とにかく、EAは、指定された回数の取引試行でライブラリに組み込まれたアルゴリズムを実行しました。

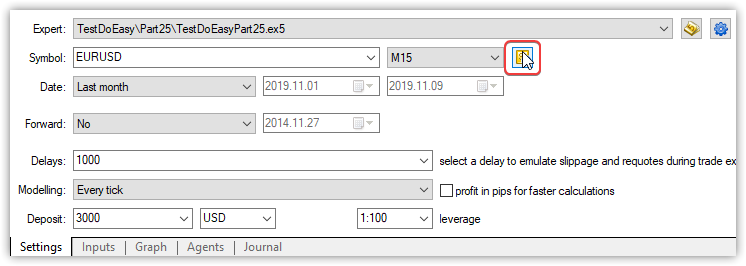

ビルド2201以降のMetaTrader 5の最新バージョンでは、テスターはテストが実行される銘柄のパラメータを設定する機能を備えています。したがって、銘柄に取引制限を設定し、銘柄制限が検出されたときにライブラリの動作をテストすることができます。

銘柄設定ウィンドウを呼び出すには、テストされた時間枠の選択の右側にあるボタンをクリックします。

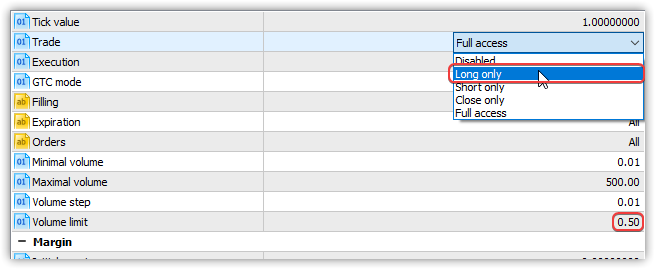

銘柄に対してのみロングポジションを開くことを許可し、同時に開かれたポジションと一方向の未決注文のボリューム制限を0.5に設定します。

したがって、ロングポジションのみを使用することができ、市場での買いポジションと注文の最大合計ボリュームは0.5ロット以下になります。言い換えると、0.1のロットでポジションを開く場合、5つのポジションのみを開くか、単一の買い指値注文を発行して4つのポジションを開くことができます。

より信頼性を高めるために、指定された利益を超えたときにポジションの自動決済を無効にすることができます。ただし、ショートポジションを開けなかったことがわかり、銘柄では買いポジションのみが許可されているという警告を受け取りました。さらに、総ボリュームが0.5ロットを超えるポジションを複数開こうとすると、ポジションと注文の最大総ボリュームを一方向に超えたためにポジションを開けないというメッセージが表示されます。

これと銘柄パラメータに関連する他の多くの機能はビルド2201以降のターミナルベータバージョンテスターでテストできます。

ターミナルの最新ベータ版を入手するには、MetaQuotes-Demoに接続し、[ヘルプ]メニューで[最新ベータ版]を選択します。

次の段階

次の記事では、未決取引リクエストを実装します。

現在のバージョンのライブラリのすべてのファイルは、テスト用EAファイルと一緒に以下に添付されているので、テストするにはダウンロードしてください。

質問、コメント、提案はコメント欄にお願いします。

シリーズのこれまでの記事:

第1部: 概念、データ管理

第2部:

過去の注文と取引のコレクション

第3部: 注文と取引のコレクション、検索と並び替え

第4部:

取引イベント概念

第5部: 取引イベントのクラスとコレクション取引イベントのプログラムへの送信

第6部:

ネッティング勘定イベント

第7部: StopLimit注文発動イベント、注文およびポジション変更イベントの機能の準備

第8部:

注文とポジションの変更イベント

第9部: MQL4との互換性 - データの準備

第10部:

MQL4との互換性 - ポジションオープンイベントと指値注文発動イベント