The SATS Algorithm

- Experts

- Version: 1.0

- Activations: 20

The SATS Algorithm represents a highly sophisticated algorithmic trading engine built for the MetaTrader 5 platform. SATS stands for the SuperTrend Adaptive Trading System. Unlike traditional automated trading systems that rely on static parameters and rigid logic, this system is engineered to dynamically adapt to shifting market environments. The core philosophy of this algorithm is centered entirely around capital preservation, strict risk management, and the avoidance of toxic trading methodologies.

This system does not utilize grid trading, martingale scaling, or arbitrage techniques. Every single execution initiated by the system is protected by a hard Stop Loss and a predefined Take Profit level. The architecture is designed to handle modern market complexities, including sudden volatility spikes, broker execution delays, and unpredictable macroeconomic events.

The development of the SATS Algorithm focused heavily on addressing the common points of failure in automated trading. By integrating multi-layered defense mechanisms, advanced statistical sizing models, and volume-based trend verification, the system operates as a complete, self-contained trading module capable of managing a portfolio of instruments simultaneously from a single chart instance.

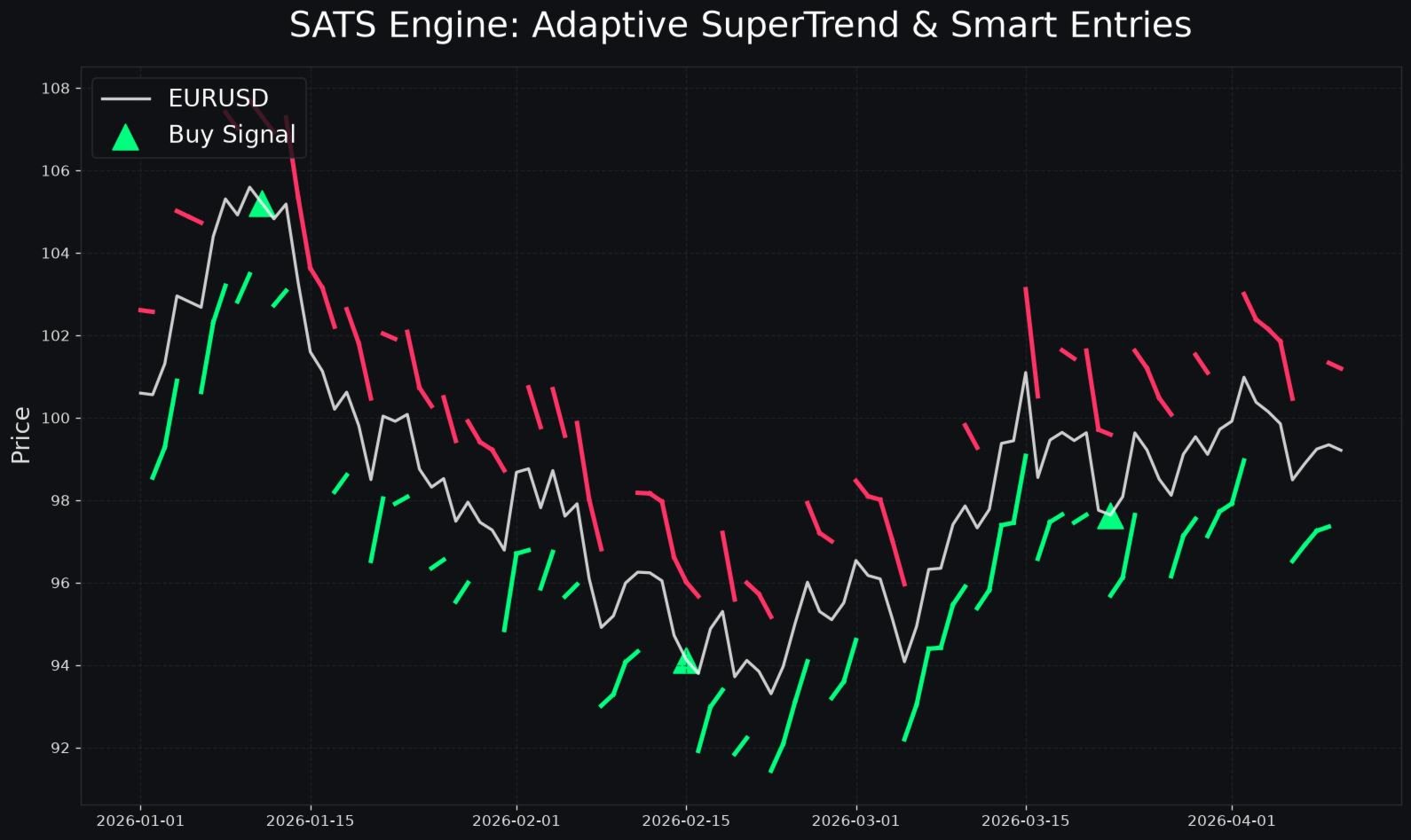

Core Trading Strategy: Adaptive SuperTrend

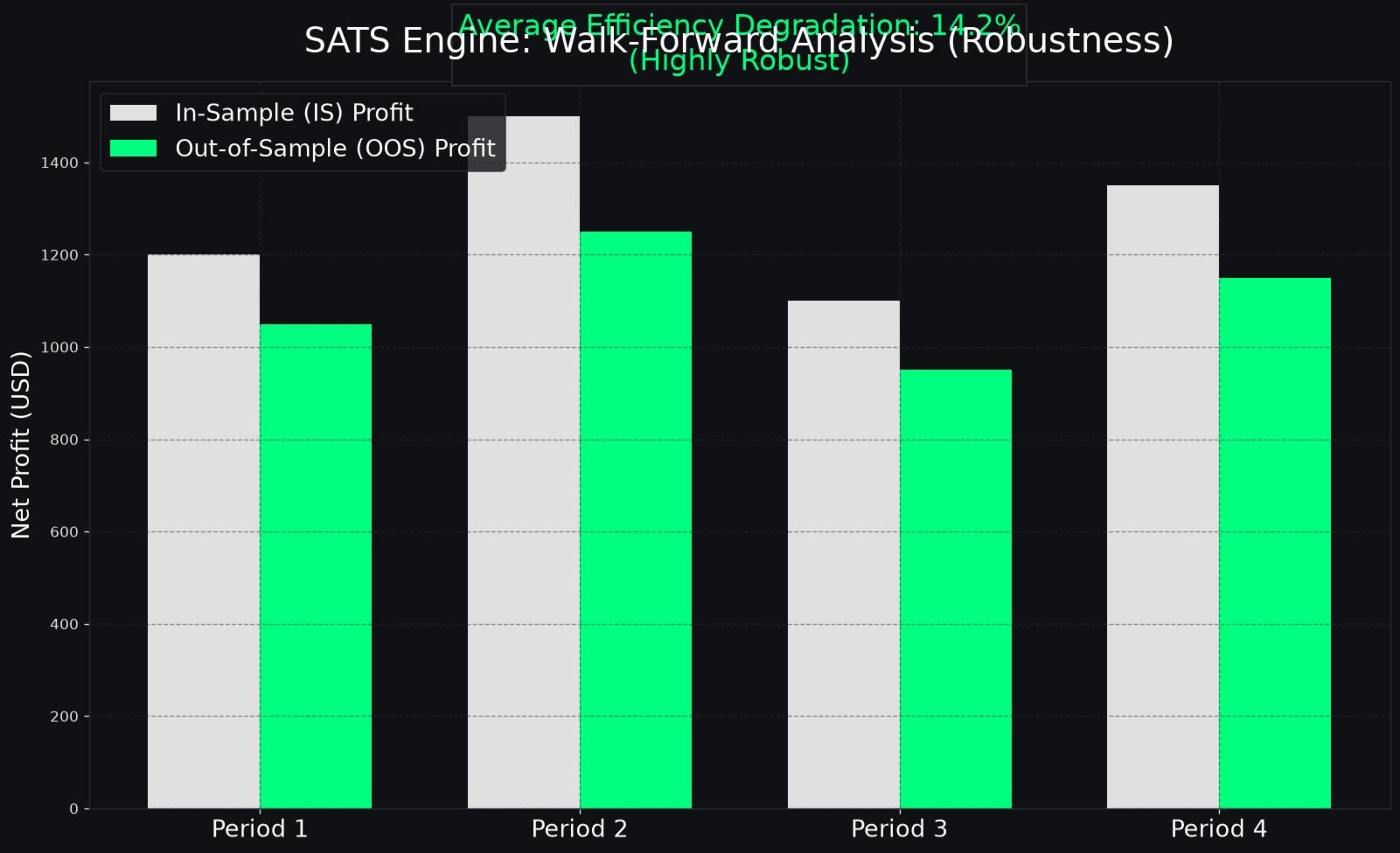

The foundation of the entry logic is built upon an advanced iteration of the classic SuperTrend indicator. However, rather than using a fixed multiplier and period, the SATS Algorithm utilizes an adaptive calibration module. This module constantly analyzes recent historical price action and adjusts its internal baseline parameters to align with the current market rhythm.

When the market enters a state of low volatility consolidation, the system tightens its parameters to reduce false breakout signals. Conversely, when the market transitions into a high volatility trending phase, the system expands its parameters to capture larger price swings without being prematurely stopped out by standard market noise. This continuous calibration ensures that the core entry logic remains relevant across various trading sessions and market cycles.

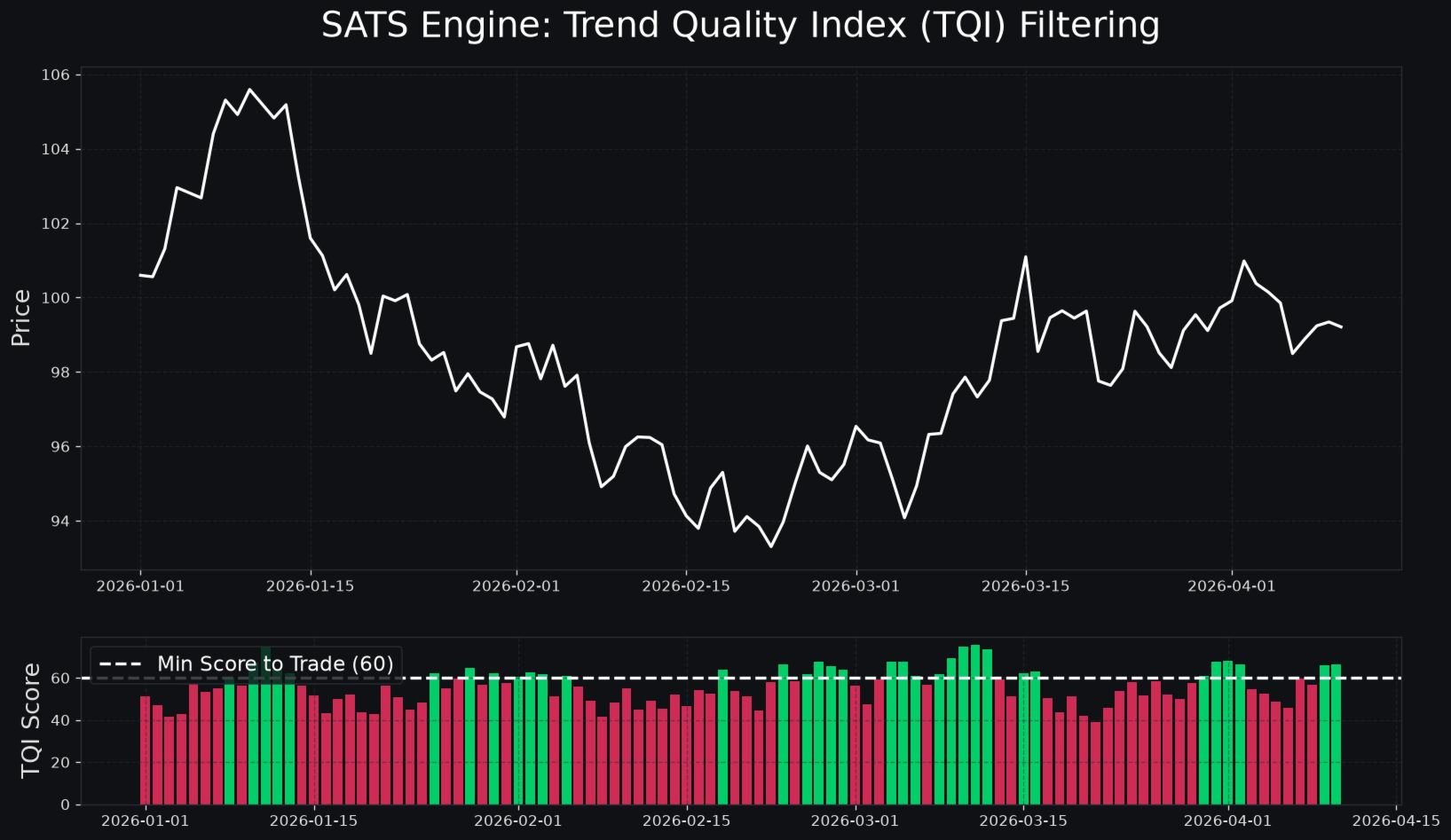

Trend Verification: The Trend Quality Index

A major vulnerability in standard trend-following systems is the inability to distinguish between a genuine trend and a false breakout driven by low liquidity. To combat this, the SATS Algorithm introduces the Trend Quality Index. This proprietary internal metric evaluates multiple underlying market factors to grade the current trend on a scale from zero to one hundred.

The Trend Quality Index analyzes the volume delta, comparing the intensity of buying pressure against selling pressure at key structural levels. It also measures cumulative volume divergence to ensure that price action is supported by actual market participation rather than algorithmic spoofing.

Before any trade is authorized by the SuperTrend module, the Trend Quality Index must evaluate the setup. If the composite score falls below the user-defined minimum threshold, the system will classify the market as low quality and suppress the trading signal. This filter drastically reduces the frequency of trades taken during suboptimal market conditions, preserving capital for high probability setups.

Advanced Money Management Systems

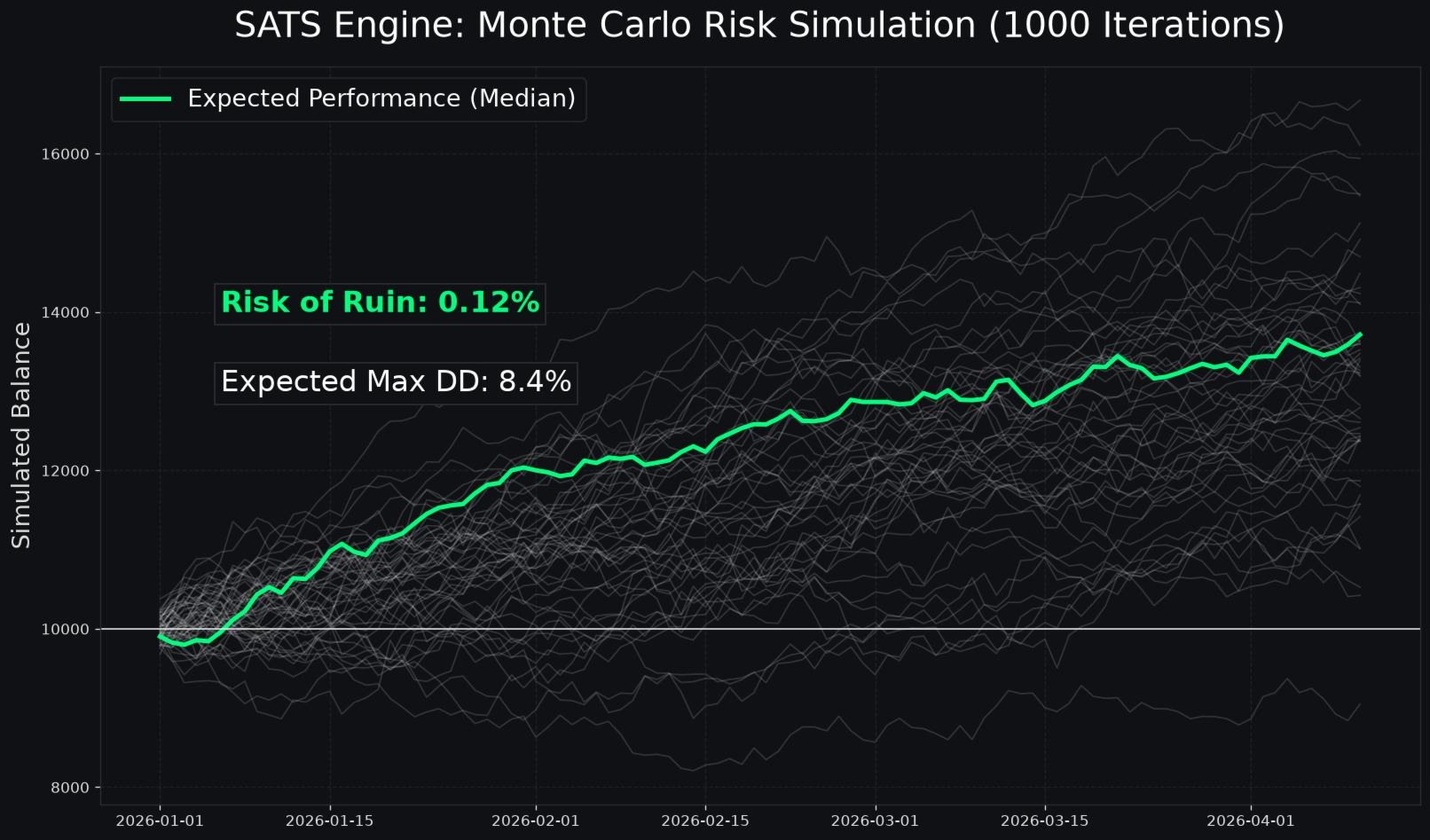

The SATS Algorithm incorporates statistical money management models typically reserved for institutional quantitative desks. These systems ensure that position sizing is mathematically optimized for long-term growth while strictly controlling the risk of ruin.

Volatility Adjusted Lot Sizing

Standard trading systems often risk a fixed percentage of the account balance per trade, regardless of the current market environment. The SATS Algorithm can dynamically scale its lot size based on the current Average True Range of the traded asset. When market volatility is exceptionally high, the system will automatically reduce the lot size to maintain a consistent monetary risk per trade. When volatility is low, the system will proportionately increase the lot size. This normalizes the risk profile across all trades.

The Kelly Criterion

For users seeking mathematically optimized compounding, the system includes an optional Fractional Kelly sizing module. The algorithm continuously tracks its own historical win rate and payoff ratio. Using these statistics, it calculates the optimal fraction of capital to risk on the next trade to maximize long-term geometric growth rates. To ensure safety, the system uses a heavily fractionalized version of the Kelly formula, preventing over-leveraging during inevitable statistical drawdowns.

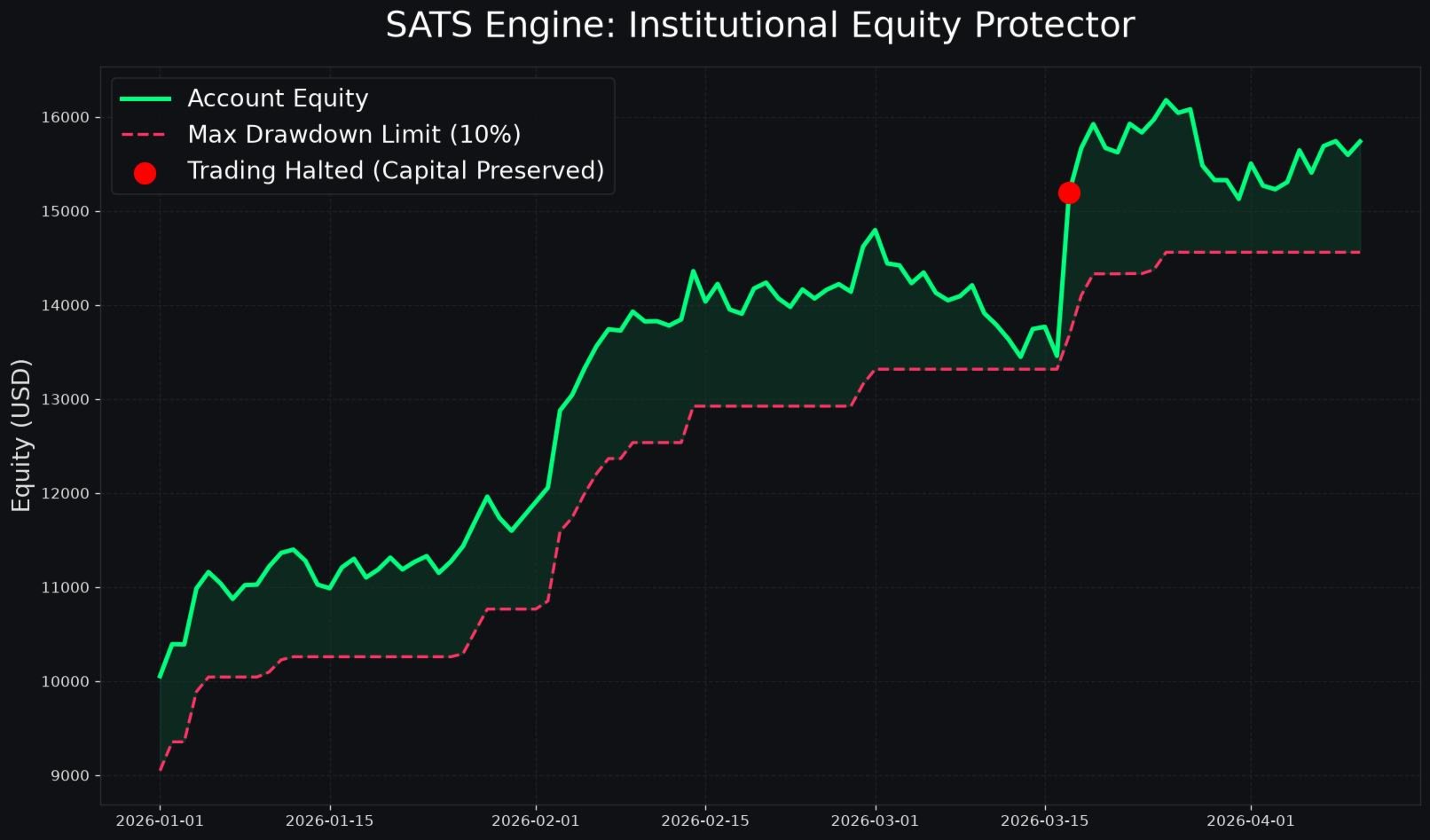

Comprehensive Risk Management

Protecting the core account balance is the highest priority of the SATS Algorithm. The system includes an overarching Equity Protector module that functions completely independent of the standard Stop Loss mechanisms.

The user can define a strict Maximum Daily Loss limit as a percentage of the total account equity. If the floating or realized loss for the current trading day reaches this limit, the system will immediately close all open positions, cancel all pending orders, and completely halt trading operations until the next trading day begins.

Additionally, the system features an absolute Maximum Drawdown limit. If the account equity ever falls below this critical threshold from its highest recorded peak, the algorithm engages a total system lockdown to prevent any further capital depletion.

Broker Defense Architecture

Live trading environments often present challenges that do not exist in historical backtesting. Spread widening, execution latency, and broker-side margin adjustments can severely impact algorithmic performance. The SATS Algorithm is equipped with multiple layers of defense to mitigate these risks.

Stealth Mode Operations

When enabled, Stealth Mode completely hides the true Stop Loss and Take Profit levels from the broker server. The system opens trades with no attached stops and manages the exit logic entirely on the local terminal. If the market price crosses the virtual stop level, the system instantly transmits a market execution to close the position. This prevents malicious stop-hunting practices.

Ping and Latency Guard

Algorithmic execution requires low latency connections to the trade server. The Ping Guard continuously monitors the connection speed in milliseconds. If the server latency exceeds the user-defined maximum limit, the system will pause new entries to prevent severe slippage.

High Margin Requirement Guard

During periods of global geopolitical tension, brokers often arbitrarily increase margin requirements, which can trigger unexpected margin calls. The system continuously monitors the required margin per lot. If the broker increases the margin requirement beyond a predefined multiplier of the standard baseline, the system suspends new trading activity until normal margin conditions are restored.

Trade Execution and Pacing

The method by which an algorithm enters the market is just as critical as the logic generating the signal. The SATS Algorithm avoids using standard market orders, which are highly susceptible to slippage during volatile periods.

Instead, the system utilizes adaptive limit orders. When a valid signal is generated, the system calculates a retracement offset based on current price action and places a pending limit order. This ensures that the system only enters the market at a favorable price, drastically improving the overall risk-to-reward ratio of the strategy.

To prevent overtrading and commission erosion during erratic sideways markets, the algorithm enforces strict Trade Pacing Limits. The user can specify a hard cap on the maximum number of trades permitted per day. Furthermore, the system enforces a cooldown timer after every closed position. This mandatory resting period prevents the system from immediately re-entering the market during chaotic price whipsaws.

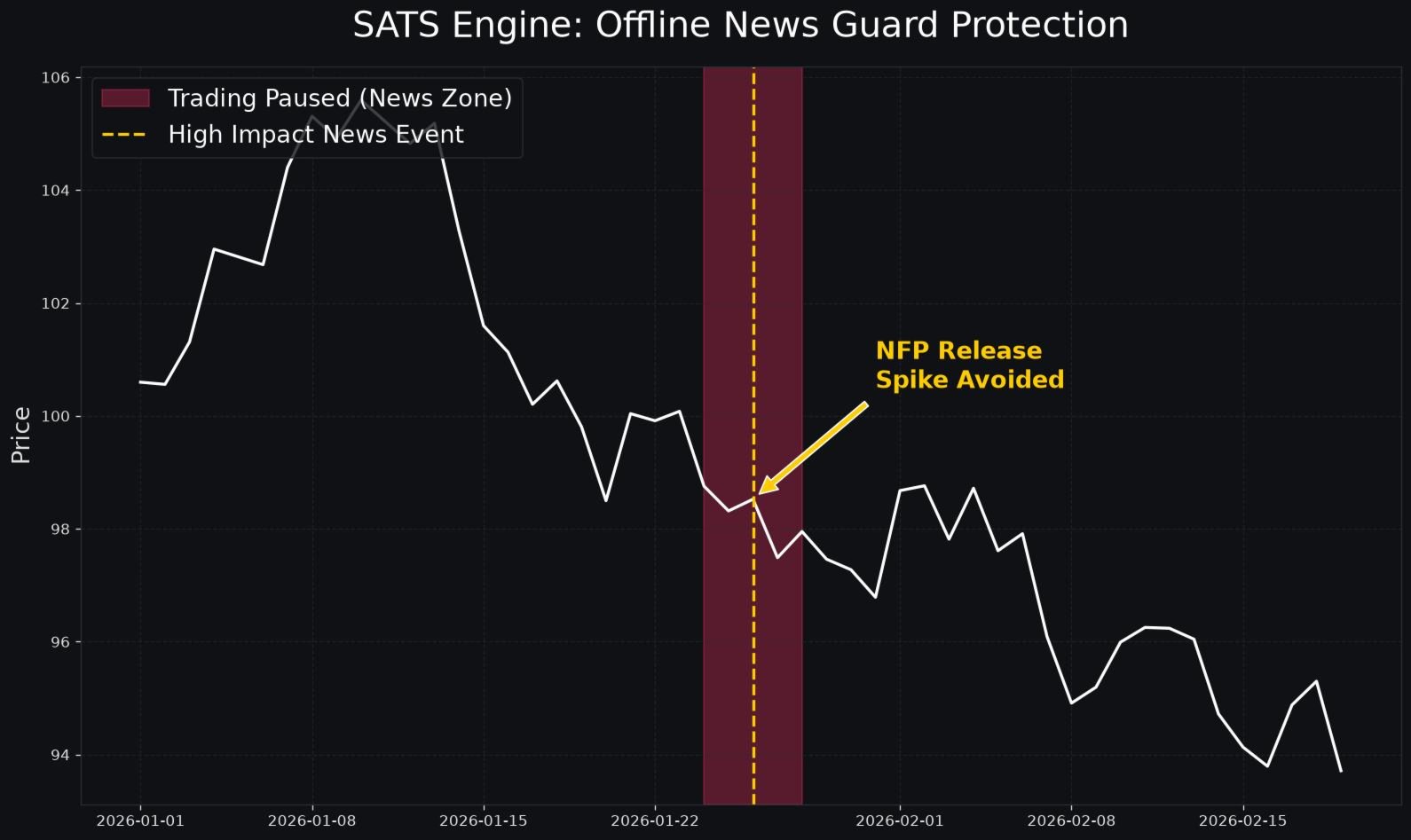

Offline Economic News Guard

Macroeconomic data releases consistently cause unpredictable volatility spikes and severe liquidity voids. To protect open positions and prevent entering the market during these chaotic events, the SATS Algorithm features a fully integrated Offline News Guard.

This module connects directly to the native MetaTrader 5 economic calendar. The user can filter news events by their expected impact level, such as high, medium, or low. The system allows the user to define a specific blackout window, measured in minutes, before and after the scheduled news release. During this blackout window, the system will pause all new trade entries, delete pending orders, and optionally tighten the trailing stops on existing open positions to lock in profits before the volatility hits.

Detailed Parameter Glossary

The SATS Algorithm provides extensive customization options, allowing users to tailor the system to their specific risk tolerance and trading objectives. Below is a comprehensive explanation of every input parameter available in the system.

Core Engine Parameters

- Symbols to Trade: A comma-separated string containing the exact names of the financial instruments the system should trade. This allows the EA to manage multiple assets from a single chart window. Example: EURUSD,GBPUSD,XAUUSD.

- Base Magic Number: The primary identification number assigned to all orders generated by the EA. This ensures the system only manages its own trades and does not interfere with manual trades or other expert advisors on the account.

- Custom Magic Numbers: Allows the user to assign unique magic numbers to specific symbols for detailed tracking and reporting purposes.

Equity Protection Parameters

- Max Daily Loss Percent: The maximum percentage of the account balance that can be lost in a single twenty-four hour period. If this threshold is breached, all trading halts until the next day.

- Max Total Drawdown Percent: The absolute maximum peak-to-valley drawdown allowed. If the account equity drops by this percentage from its highest watermark, the system ceases all operations permanently to preserve the remaining capital.

Offline News Guard Parameters

- Enable MT5 Calendar News Guard: A boolean toggle to activate or deactivate the integration with the MetaTrader 5 economic calendar.

- Minimum News Impact: A dropdown selection to determine which tier of news events should trigger the blackout protocol. Options typically include High impact only, or Medium and High impact.

- Pause Before News Mins: The number of minutes prior to a scheduled news event during which the system will reject all new trading signals.

- Pause After News Mins: The number of minutes following a news event during which the system will remain paused, allowing the market to digest the data and return to normal liquidity conditions.

Market Regime and Session Parameters

- Enable Market Regime Detection: Activates the internal market phase analysis module, allowing the system to differentiate between ranging consolidation and directional trends.

- Session Start Hour: The specific hour of the day, according to the broker server time, when the algorithm is authorized to begin scanning for trade setups.

- Session End Hour: The specific hour of the day when the algorithm must stop generating new entries. Existing open positions will continue to be managed normally.

Pending Orders and Entry Parameters

- Use Limit Orders instead of Market: Forces the system to enter trades exclusively via pending limit orders to secure exact entry prices and eliminate slippage.

- Limit Order Retracement Offset Pips: The precise distance in pips from the current market price where the pending limit order will be placed.

- Expand RRR in Trending Regimes: A dynamic feature that automatically increases the Take Profit distance when the Market Regime module detects a strong, sustained trend, aiming to capture maximum market extension.

Adaptive SuperTrend and TQI Parameters

- SuperTrend Period: The number of historical bars used to calculate the baseline volatility for the SuperTrend indicator.

- SuperTrend Base Multiplier: The multiplier applied to the Average True Range to calculate the distance of the SuperTrend line from the median price.

- TQI Calculation Period: The lookback window used by the Trend Quality Index to evaluate volume and divergence metrics.

- Minimum Composite Score: The strict numerical threshold from zero to one hundred that the Trend Quality Index must meet or exceed to validate a trading signal.

- Filter signals using Volume Delta: Enables the analysis of buying volume versus selling volume to confirm the direction of the trend.

- Filter signals using CVD Divergence: Activates the cumulative volume divergence check, ensuring that price action is not diverging from underlying market volume.

Risk and Money Management Parameters

- Base Risk per Trade Percent: The standard percentage of the current account balance to risk on a single trade. The system uses this to automatically calculate the precise lot size based on the Stop Loss distance.

- Custom Risk: Allows the user to override the base risk percentage for specific symbols, allocating more risk to stable pairs and less risk to volatile assets.

- RRR TP1: The reward-to-risk ratio for the first take profit target. For example, a value of 1.5 means the take profit distance is 1.5 times the stop loss distance.

- RRR TP2: The reward-to-risk ratio for the second scale-out target.

- RRR TP3: The reward-to-risk ratio for the final take profit target.

- Use Kelly Fractional Bet Sizing: Activates the statistical money management module that scales lot sizes based on the historical win rate of the algorithm.

- Use Volatility Adjusted Lot Sizing: Enables the dynamic reduction of lot sizes when the Average True Range exceeds historical baselines.

Stealth Mode and Defenses Parameters

- Hide SL and TP from broker: Activates Stealth Mode, keeping all stop loss and take profit parameters strictly within the local terminal memory and hiding them from the broker server.

- Max allowed spread Pips: The absolute maximum spread in pips that the system will accept. If the current market spread exceeds this value, all trade entries are suspended.

- Enable High Margin Req Guard: Activates the margin monitoring defense to protect the account from sudden broker-initiated leverage reductions.

- Enable Ping and Latency Guard: Activates the execution speed defense, ensuring trades are only placed when the connection to the server is optimal.

Trade Pacing Parameters

- Max Trades Per Day: A hard limit on the total number of new positions the system is allowed to open within a single twenty-four hour period.

- Cooldown after closed trade mins: The mandatory resting period in minutes that the system must observe after a position is closed before it is allowed to process a new signal for that specific symbol.