HV Models

- Indicators

- Version: 1.2

- Updated: 16 December 2018

- Activations: 5

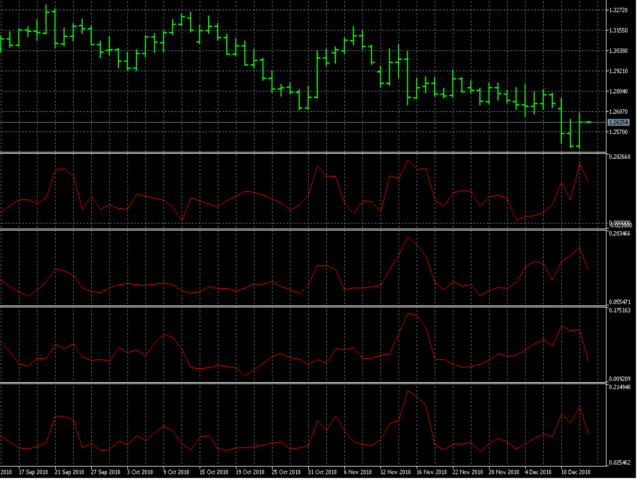

HV Models is an Indicator that containes 4 methods for calculating historical volatility of the selected asset.

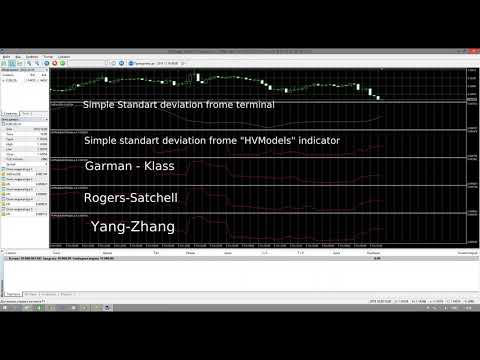

Volatility is one of the fundamental values describing changes in the underlying asset. In statistics, it usualy describes as a standard deviation. The price chart has 4 values (Open High Low Close) when we calculate volatility using a standard indicator, only one of these values is used as a result we get one-sided volatility picture. The presented indicator uses 4 volatility calculation formulas developed specifically for financial markets:

Simple:

When choosing this mode, first of all we calculate logrifmic increments by closing price which allows filtering out the trend, seasonality and other inclusions that spoil the volatility picture. then calculates standard deviation - volatility by logrifmic increments.

Garman - Klass:

This variant of volatility takes into account intraday fluctuations in price, unlike the previous version, it focuses on the measurement of candlestick volatility.

This variant just like the previous version of volatility takes into account the measurement of candle volatility, however this method, compared to the previous one emphasis is placed on measuring each of the price fluctuations (H / C, H / O, LC, LO) - which gives more detailed measurement.

Yang-Zhang

This method combines all the previously described types of volatility calculations. It measures volatility both within the day and in relation to the previous day.

The indicator allows to recalculate volatility from the current timeframe to another one. For example to get annual volatility frome daily volatility parameter "Calendar Amendment" must be equals to 365 (dayse per year). To recalculate minute volatility to one year volatiolity paranetr Calendar Amendment mast be equal to 525600. This number was found using following formula: (24 (hours per day) * 60 (minutes per hour) * 365 (days per year)). If this parameter equals 1, the recalculation is not performed and the volatility is shown for the selected timeframe.

For those who will use the indicator in EA - the indicator has 2 buffers, however the indicator itself is stored in a buffer with a zero index.