Articles on data analysis and statistics in MQL5

Articles on mathematical models and laws of probability are interesting for many traders. Mathematics is the basis of technical indicators, and statistics is required to analyze trading results and develop strategies.

Read about the fuzzy logic, digital filters, market profile, Kohonen maps, neural gas and many other tools that can be used for trading.

Add a new article

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

MQL5 Trading Tools (Part 34): Replacing Native Chart Objects with an Interactive Canvas Drawing Layer

We replace native MetaTrader chart objects with a canvas-based drawing engine that renders tools pixel-by-pixel on a full-chart bitmap layer. The article implements persistent object storage with per-tool style memory, precise hit testing, selection, whole-object dragging, and handle manipulation. It also adds new line tools, a reorganized category system with a one-click delete action, and a rubber-band preview for multi-click placement.

Seasonality Indicator by Hours, Days of the Week, and Days of the Month

The article explains how to develop a tool for analyzing recurring price patterns in financial markets — by day of the month (1-31), day of the week (Monday-Sunday), or hour of the day (0-23). The indicator analyzes historical data, calculates the average return for each period, and displays the results as a histogram with a forecast. It includes customizable parameters: seasonality type, number of bars analyzed, display as percentages or absolute values, chart colors.

Backtracking Search Algorithm (BSA)

What if an optimization algorithm could remember its past journeys and use that memory to find better solutions? BSA does just that – balancing exploration with revisiting the tried and true. In this article, we reveal the secrets of the algorithm. A simple idea, minimum parameters and a stable result.

Market Simulation (Part 22): Getting Started with SQL (V)

Before you give up and decide to abandon learning SQL, allow me to remind you, dear readers, that here we are still using only the most basic elements. We have not yet looked at some of SQL's capabilities. Once you understand them, you will see that SQL is far more practical than it seems. Although, most likely, we will eventually change the direction of what we are building, because the creation process is dynamic. We will show a little more about creating different things in SQL, because this is truly important and useful for you. Simply thinking that you are more capable than an entire community of programmers and developers will only lead to wasted time and opportunities. Do not worry, because what comes next will be even more interesting.

Analyzing Price Time Gaps in MQL5 (Part I): Building a Basic Indicator

Time gap analysis helps traders identify potential market reversal points. The article discusses what a time gap is, how to interpret it, and how it can be used to detect large volume influxes into the market.

Dolphin Echolocation Algorithm (DEA)

In this article, we take a closer look at the DEA algorithm, a metaheuristic optimization method inspired by dolphins' unique ability to find prey using echolocation. From mathematical foundations to practical implementation in MQL5, from analysis to comparison with classical algorithms, we will examine in detail why this relatively new method deserves a place in the arsenal of researchers facing optimization problems.

Market Simulation (Part 21): First Steps with SQL (IV)

Many of you may have far more experience working with databases than I do, and therefore may have a different opinion. Since it was necessary to explain why databases are designed the way they are, and why SQL has the form it does—especially why primary and foreign keys emerged—some things had to remain somewhat abstract.

MQL5 Wizard Techniques you should know (Part 92): Using B-Tree Indexing and a Bayesian NN in a Custom Signal Class

In this article we present yet another custom MQL5 Signal Class that we are labelling ‘CSignalBTreeBayesian’. We are marrying the algorithm of a balanced tree with a neural network that is built on Bayesian principles to formulate yet another custom signal testable independently or with other signals thanks to the MQL5 Wizard.

Beyond GARCH (Part IV): Partition Analysis in MQL5

In this article, we shift from Python research to native MQL5 engineering. We build the first module of the MMAR library: a shared constants header, an SVD-based OLS regression class, a Generalized Hurst Exponent estimator, and the partition analysis engine that computes the partition function, extracts tau(q), estimates H via zero-crossing interpolation, and scores multifractality through three diagnostic tests. Tested on 500,000 bars of EURUSD M10, the engine correctly classifies the data as multifractal in under four seconds. Part 4 of an eight-part series. Part 5 fits the tau(q) curve to four candidate distributions via the Legendre transform.

Building Volatility Models in MQL5 (Part III): Implementing the SLSQP Algorithm for Model Estimation

An SLSQP optimizer is implemented in MQL5 to resolve parameter discrepancies between a volatility library and Python's ARCH module. The article details constraint handling, gradient options, configuration, and convergence controls and shows how to integrate the solver into existing code. Practical examples and comparisons demonstrate matched log‑likelihoods and parameters on shared datasets.

Application of the Grey Model in Technical Analysis of Financial Time Series

This article explores the grey model, a promising tool that can expand trader's capabilities. We will look at some options for applying this model to technical analysis and building trading strategies.

Joint Recurrence Quantification Analysis (JRQA) in MQL5: Detecting Simultaneous Recurrence in Two Series

We extend the RQA library for MetaTrader 5 with JRQA, which detects when two series simultaneously revisit their own past states. The article covers the joint recurrence matrix, twelve JRQA metrics (including TREND and COMPLEXITY), dual-epsilon configuration, and a rolling-window engine with OpenCL acceleration and automatic CPU fallback. A practical indicator plots JRR, JDET, JLAM, JENTR, and JTREND for any symbol pair with timestamp alignment and normalization.

Covariance Matrix Adaptation Evolution Strategy (CMA-ES)

The article explores one of the most interesting non-gradient optimization algorithms, which learns to understand the geometry of the objective function. We will focus on the classical implementation of CMA-ES with a slight modification - replacing the normal distribution with the power one. We will thoroughly examine the math behind the algorithm, as well as practical implementation, and check where CMA-ES is unbeatable and where it should be avoided.

How to Detect and Normalize Chart Objects in MQL5 (Part 1): Building a Chart Object Detection Engine

This article addresses the interpretative gap between visual chart objects and algorithmic execution. You will build a systematic detector that iterates over all chart objects, identifies analytical types, and normalises their geometric data (time and price coordinates) into a structured SChartObjectInfo array. The implementation uses raw MQL5 functions, a filter‑extract‑store pipeline, and a timer‑driven test EA, resulting in a reusable framework for rule‑based trading inputs.

Market Microstructure in MQL5 (Part 3): Estimating ARFIMA d with GPH

A GPH‑based estimator for d, the key ARFIMA parameter, is added to MicroStructure_Foundation.mqh. GPHEstimator() computes d via log‑periodogram regression, while PopulateARFIMAAnalysis() stores d with an R² confidence score and validates the theoretical relationship H = d + 0.5. An empirical study on 72 US100 M1 sessions confirms pooled d = −0.006, consistent with the random walk boundary established in Part 2.

An Introduction to the Study of Fractal Market Structures Using Machine Learning

The article attempts to examine financial time series from the perspective of self-similar fractal structures. Since we have too many analogies that confirm the possibility of considering market quotes as self-similar fractals, this allows us to think about the forecasting horizons of such structures.

MQL5 Wizard Techniques you should know (Part 91): Using Skip Lists and a Hopfield Network in a Custom Trailing Class

For our next Exploration on notions that are testable with the MQL5 Wizard we examine if Skip Lists and the Hopfield Network can give us a profit-guarding trailing strategy. Trailing Stop Management, as already argued, can be overlooked in most trading systems at the expense of Entry Signals or even Money Management. Trailing stops can make all the difference in certain situations such as trending markets, and thus we test this out with GBP USD.

Overcoming Accessibility Problems in MQL5 Trading Tools (Part IV): Remote voice trading

Learn a practical way to execute MetaTrader 5 trades from Telegram voice notes using a Python middleware and an MQL5 EA acting as an HTTP client. The article covers architecture, WebRequest polling, in-memory queuing, JSON parsing with null-terminator stripping, and a constrained command grammar with a 0.001-lot default. You will configure the environment and validate round‑trip latency suitable for mobile data connections.

3D Visualization Without External Libraries: How MetaTrader 5 Reveals Optimization Results via MQL5 + DX11

The article describes the practical application of DirectX 11 and built-in MQL5 tools for creating 3D visualizations and interactive interfaces in MetaTrader 5. The focus is on cognitive efficiency - the ability of 3D charts and guided scenes to help in understanding optimization data, liquidity clusters, and multi-dimensional trading scenarios. The basics of the DX pipeline, working with shaders, binding mouse and keyboard events, and objective technological limitations are discussed in detail. The article is intended for MQL5 developers and algorithmic traders who are ready to transform strategy metrics into understandable 3D analytical landscapes, where the visual layer accelerates decision-making.

Market Microstructure in MQL5 (Part 2): Measuring long memory in MQL5 with Hurst estimators

Part 2 focuses on practical long-memory detection for intraday data. Three complementary Hurst estimators are implemented and combined into a confidence‑weighted composite, with confidence tied to valid regression scales. The final H and confidence populate the shared analysis struct, enabling indicators to act only when H departs from the neutral 0.40–0.60 band and to select trend‑following above 0.60 or mean‑reversion below 0.40.

Evaluating the Quality of Forex Spread Trading Based on Seasonal Factors in MetaTrader 5

The article examines the quality of a seasonal trading approach on a daily timeframe, both for individual symbols and for spreads. Particular attention is paid to identifying recurring monthly cycles and the possibilities of their application in trading within the current year.

From "Best Pass" to Robust Solutions: Exploring the Optimization Surface in MetaTrader 5

The article examines an engineering approach to optimizing an Expert Advisor in MetaTrader 5: from collecting custom metrics through Optimization Frames to parameter surface analysis. A simple event-driven EMA/RSI model demonstrates CSV export, smoothing, and local stability assessment in Python. The goal is to find stable areas of configurations and validate them with forward optimization for reliable implementation.

MetaTrader 5: Build a Market to Suit Your Strategy — Renko/Range/Volume, Synthetics, and Stress Tests on Custom Symbols

In this article, we demonstrate how to use API of the MetaTrader 5 custom symbols to transform your terminal into a data constructor for generating timeless Renko, Range, and Equal-Volume charts and assembling synthetic instruments. We will analyze tick aggregation and history modification for stress tests (spread widening, stop level changes) taking into account platform limitations. Besides, you will get some practice of handling CiCustomSymbol and routing orders to a real symbol through the CustomOrder wrapper with ready-made code fragments.

Beyond GARCH (Part III): Building the MMAR and the Verdict

With the multifractal parameters from Part 2 in hand, this article builds the full MMAR process. We construct the multiplicative cascade for trading time, generate Fractional Brownian Motion via Davies-Harte FFT, and combine both into X(t) = B_H[theta(t)]. A 100-path Monte Carlo simulation produces the volatility forecast, which we then pit against GARCH on the same EURUSD M5 data. Does Mandelbrot's fractal architecture outforecast Engle's conditional variance framework? Part 3 of a eight-part series leading to a native MQL5 library and Expert Advisor.

MQL5 Wizard Techniques you should know (Part 90): Fenwick Tree Money Management with 1D CNN in MQL5

This article implements a Fenwick Tree (Binary Indexed Tree) for volume-aware money management inside an MQL5 Wizard Expert Advisor. We structure cumulative volume in O(log n) and apply four scaling modes—linear, conservative, aggressive, and mean-reversion—optionally gated by a lightweight 1D CNN. Practical tests compare the algorithm alone versus the CNN‑filtered approach to illustrate adaptive lot sizing and risk control under varying volume topologies.

Eagle Strategy (ES)

Eagle Strategy is an algorithm that mimics the eagle's two-phase hunting strategy: global search via Levy flights using Mantegna method, alternating with intense local exploitation using the firefly algorithm, a mathematically sound approach to balancing exploration and exploitation, and a bioinspired concept that combines two natural phenomena into a single computational method.

Beyond GARCH (Part II): Measuring the Fractal Dimension of Markets

Building on the partition function analysis from Part 1, this article deepens the theoretical foundation before completing the analytical pipeline. We first give a full treatment of the Hurst exponent: what it measures, what it implies about market memory, and why it matters for the MMAR. This is followed by an intuitive exploration of multifractal spectra and what f(α) reveals about volatility heterogeneity. We then move to implementation: extracting the scaling function τ(q), estimating H via R/S analysis, and fitting the multifractal spectrum across four candidate distributions. By the end, we have the complete parameter set needed to construct the MMAR process in Part 3. Part 2 of an eight-part series.

Determining Fair Exchange Rates Using PPP and IMF Data

Building a purchasing power parity (PPP)-based exchange rate analysis system using Python. The author developed an algorithm with 5 methods for calculating fair exchange rates using IMF data. A practical guide to fundamental currency analysis, economic data processing, and integration with trading systems. Full code in open source.

Cross Recurrence Quantification Analysis (CRQA) in MQL5: Building a Complete Analysis Library

This article extends the MQL5 RQA library to Cross-Recurrence Quantification Analysis (CRQA) for comparing two time series. We implement dual‑series embedding, cross‑recurrence matrix construction, adapted metrics (CRR, CDET, CLAM, CENTR, and others), and rolling‑window analysis, with optional GPU acceleration via OpenCL. A ready-to-use indicator compares two symbols in real time, supporting timestamp alignment and normalization for practical inter-market analysis.

MQL5 Wizard Techniques you should know (Part 89): Using Bitwise Vectorization with Perceptron Classifiers

This article presents a custom MQL5 signal class, CSignalBitwisePerceptron, for ultra-lightweight entry logic. It packs 64 bars into a single uint64 via bitwise vectorization and evaluates them with a perceptron that sums weights only for active bits. A two-gate flow (algorithmic hash map plus neural threshold) minimizes array iteration and heavy math. Readers get a practical template to cut latency and refine entry validation.

Beyond GARCH (Part I): Mandelbrot's MMAR versus Engle's GARCH

This article starts the MMAR pipeline on EURUSD M5 data. We load market data via the MetaTrader5 Python API and run partition-function analysis with non-overlapping intervals to test for multifractal scaling. The result is an evidence-based decision on fractality, a prerequisite for building MMAR and for choosing whether to proceed beyond GARCH.

Downloading International Monetary Fund Data Using Python

Downloading international monetary fund data in Python: Mining IMF data for use in macroeconomic currency strategies. How can macroeconomics help an ordinary and an algorithmic trader?

Biogeography-Based Optimization (BBO)

Biogeography-Based Optimization (BBO) is an elegant global optimization method inspired by natural processes of species migration between islands within archipelagos. The algorithm is based on a simple yet powerful idea: high-quality solutions actively share their characteristics, while low-quality ones actively adopt new features, creating a natural flow of information from the best solutions to the worst. A unique adaptive mutation operator provides an excellent balance between exploration and exploitation. BBO demonstrates high efficiency on a variety of tasks.

Gaussian Processes in Machine Learning: Regression Model in MQL5

We will review the basics of Gaussian processes (GP) as a probabilistic machine learning model and demonstrate its application to regression problems using synthetic data.

Exploring Conformal Forecasting of Financial Time Series

In this article, we will consider conformal predictions and the MAPIE library that implements them. This approach is one of the most modern ones in machine learning and allows us to focus on risk management for existing diverse machine learning models. Conformal predictions, by themselves, are not a way to find patterns in data. They only determine the degree of confidence of existing models in predicting specific examples and allow filtering for reliable predictions.

MetaTrader 5 and the MQL5 Economic Calendar: How to Turn News into a Reproducible Trading System

The article presents a systematic approach to news trading in MetaTrader 5 using the built-in economic calendar: data structure, API functions, time synchronization rules, and event filtering. Methods of caching and incremental updating without overloading the server are described. The article also provides a working mechanism for exporting history to an .EX5 resource for deterministic testing using the same algorithm.

Three MACD Filters on US_TECH100: Five Years of Broker Data

This article tests three common filters on a standard MACD crossover for US_TECH100 H1 using five years of broker-native data. Filters are layered incrementally: regime, higher timeframe (HTF) alignment, and US session timing, to isolate each one's marginal impact. Results show session timing contributes far more than indicator refinements, while regime and HTF add little on their own. Includes a reproducible MQL5 regime classifier.

How to implement AutoARIMA forecasting in MQL5

This article presents an MQL5 implementation of AutoARIMA that builds ARIMA models without manual tuning. It estimates d via a variance-based heuristic, fits ARMA(p,q) by gradient optimization with Adam, and selects p and q using AICc. The code returns a one-step-ahead price forecast by differencing, model estimation, and integration back to price level, ready to call on a Close series.

MQL5 Wizard Techniques you should know (Part 88): Using Blooms Filter with a Custom Trailing Class

Our next focus in these series on ideas that can be rapidly prototyped with the MQL5 Wizard, is a Custom Trailing class that uses the Blooming Filter. Trailing Stop systems are an optional but very resourceful part to any trading system that we want to explore more in these series besides the traditional Entry Signals.

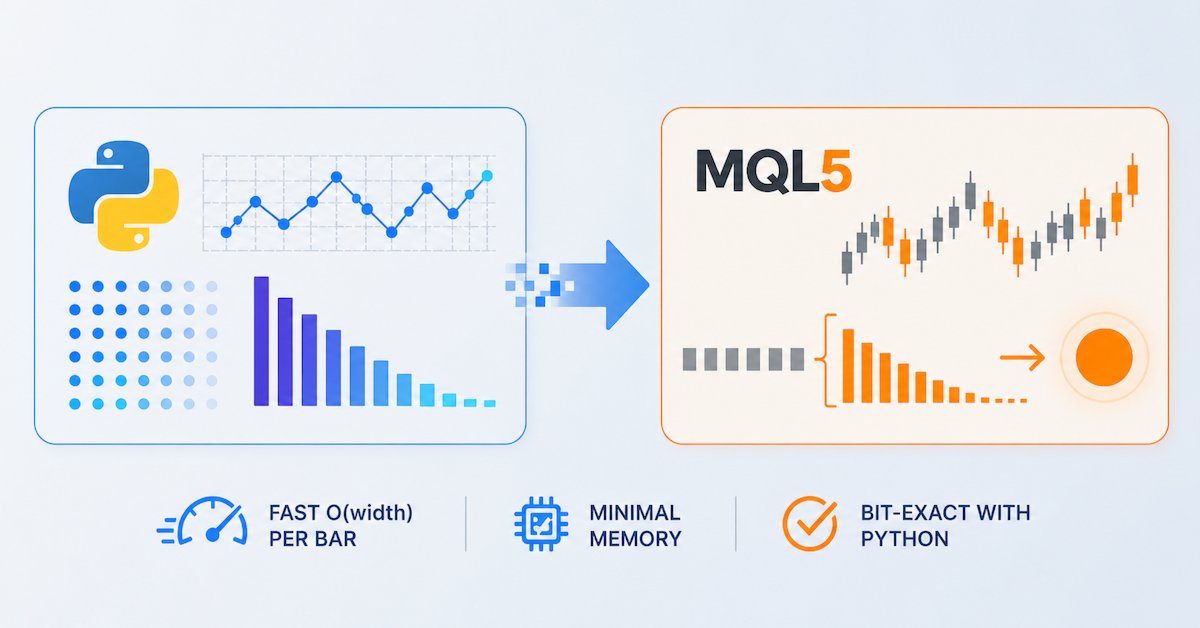

Feature Engineering for ML (Part 2): Implementing Fixed-Width Fractional Differentiation in MQL5

This article delivers a production-grade MQL5 implementation of fixed-width fractional differentiation for live MetaTrader 5 feeds. We introduce a header-only CFFDEngine that precomputes weights without a fixed cap, performs O(width) per-bar updates, and avoids per-tick allocations. The FFD.mq5 indicator supports all ENUM_APPLIED_PRICE types and prev_calculated optimization. Validation scripts confirm numerical equivalence with the standard Python frac diff_ffd pipeline.