Neural Networks in Trading: Hierarchical Dual-Tower Transformer (Final Part)

Introduction

In the previous article, we reviewed the theoretical aspects of the Hidformer framework, developed specifically for analyzing and forecasting complex multivariate time series. The model demonstrates high effectiveness in processing dynamic and volatile data thanks to its unique architecture.

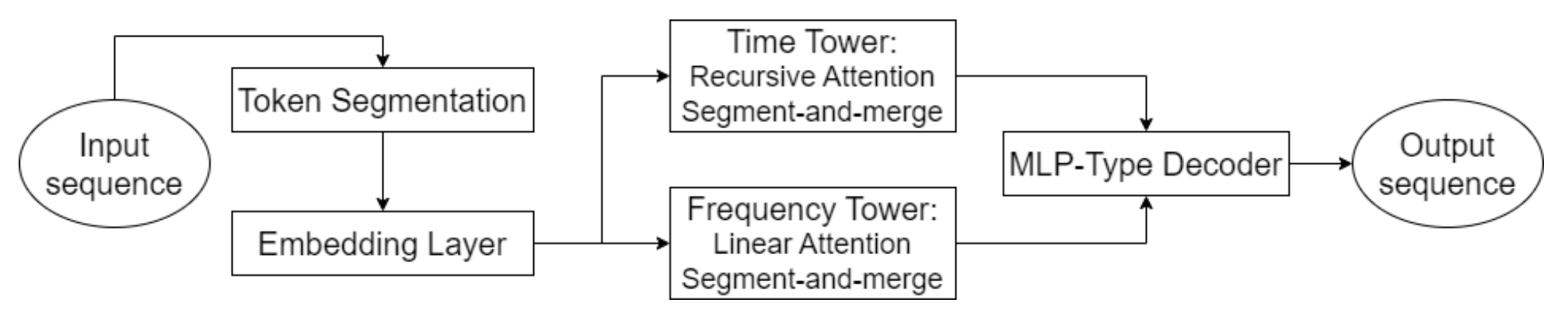

A key element of Hidformer is the use of advanced attention mechanisms that make it possible not only to identify explicit dependencies in the data but also to uncover deep, latent relationships. To achieve this, the model employs a two-tower encoder, with each tower performing an independent analysis of the raw data. One tower specializes in analyzing the temporal structure, identifying trends and patterns, while the second examines the data in the frequency domain. This approach provides a comprehensive understanding of market dynamics, enabling the model to account for both short-term and long-term changes in price series.

An innovative aspect of the model is the use of a recursive attention mechanism to analyze temporal dependencies, allowing it to sequentially accumulate information about complex dynamic patterns of the financial instrument being studied. Combined with the linear attention mechanism used for analyzing the frequency spectrum of the input data, this approach optimizes computational costs and ensures training stability. This allows the Hidformer framework to effectively adapt to the multidimensionality and nonlinearity of the input data, providing more reliable forecasts in conditions of high market volatility.

The model's decoder, built on a multilayer perceptron, enables prediction of the entire sequence of prices in a single step, minimizing the accumulation of errors typical for step-by-step forecasting. This significantly improves the quality of long-term forecasts, making the model especially valuable for practical applications in financial analysis.

The original visualization of the Hidformer framework is provided below.

In the practical section of the previous article, we completed the preparatory work and implemented our own versions of the recursive and linear attention algorithms. Today, we continue the development of the approaches proposed by the authors of the Hidformer framework.

Time Series Analysis

The authors of the Hidformer framework proposed a two-tower encoder architecture, which we adopted as our foundation. In our implementation, each encoder tower is represented as a separate object, allowing for flexible adaptation of the model to various tasks. However, unlike the original framework, we introduced several modifications driven by the specifics of the problem our model aims to solve. Initially, the framework was designed to forecast the continuation of the analyzed time series, but we took it a step further.

Drawing on the experience gained from implementing the MacroHFT and FinCon frameworks, we repurposed the encoder towers as independent agents that generate possible scenarios for upcoming trading operations. This significantly expands the system’s functional capabilities.

As in the original Hidformer architecture, our agents analyze market data in the form of multivariate time series and their frequency characteristics. The recursive attention mechanism allows the model to capture dependencies within multivariate time series, while frequency spectrum analysis is performed using linear attention modules. This approach enables a deeper understanding of structural patterns in the data and allows the model to adapt to changing market conditions in real time - particularly important in high-frequency and algorithmic trading.

Additionally, each agent is equipped with a module for recurrent analysis of previously made decisions, allowing it to evaluate them in the context of the evolving market situation. This module provides the ability to analyze past decisions, identify the most effective strategies, and adapt the model to changing market conditions.

The time-series analysis agent is implemented as the CNeuronHidformerTSAgent object. Its structure is shown below.

class CNeuronHidformerTSAgent : public CResidualConv { protected: CNeuronBaseOCL caRole[2]; CNeuronRelativeCrossAttention cStateToRole; CNeuronS3 cShuffle; CNeuronRecursiveAttention cRecursiveState; CResidualConv cResidualState; CNeuronRecursiveAttention cRecursiveAction; CNeuronMultiScaleRelativeCrossAttention cActionToState; //--- virtual bool feedForward(CNeuronBaseOCL *NeuronOCL) override; virtual bool calcInputGradients(CNeuronBaseOCL *NeuronOCL) override; virtual bool updateInputWeights(CNeuronBaseOCL *NeuronOCL) override; public: CNeuronHidformerTSAgent(void) {}; ~CNeuronHidformerTSAgent(void) {}; //--- virtual bool Init(uint numOutputs, uint myIndex, COpenCLMy *open_cl, uint window, uint window_key, uint units_count, uint heads, uint stack_size, uint action_space, ENUM_OPTIMIZATION optimization_type, uint batch); //--- virtual int Type(void) override const { return defNeuronHidformerTSAgent; } //--- virtual bool Save(int const file_handle) override; virtual bool Load(int const file_handle) override; //--- virtual bool WeightsUpdate(CNeuronBaseOCL *source, float tau) override; virtual void SetOpenCL(COpenCLMy *obj) override; //--- virtual bool Clear(void) override; };

As the parent class, we use a convolutional block with feedback, which serves as the FeedForward block of one of the internal attention modules.

It is worth noting that the presented structure includes a wide spectrum of diverse components, each performing its own unique function in the organization of this new class of algorithms. These elements ensure a multifaceted approach, enabling the model to adapt to various scenarios of information processing and analysis of complex patterns. We will examine each of these components in more detail during the construction of the class methods.

All objects are declared statically, allowing us to leave the class constructor and destructor empty. Initialization of all inherited and declared objects is implemented in the Init method. This method accepts several constant parameters that clearly define the architecture of the created object.

bool CNeuronHidformerTSAgent::Init(uint numOutputs, uint myIndex, COpenCLMy *open_cl, uint window, uint window_key, uint units_count, uint heads, uint stack_size, uint action_space, ENUM_OPTIMIZATION optimization_type, uint batch) { if(!CResidualConv::Init(numOutputs, myIndex, open_cl, 3, 3, (action_space + 2) / 3, optimization_type, batch)) return false;

Initialization begins with a call to the corresponding method of the parent class, which already contains the necessary control points and initialization procedures for inherited objects. It should be kept in mind that the interfaces of the parent object must produce outputs consistent with the intended behavior of the agent. In this case, the agent is expected to output a tensor of trading operations, where each operation is represented by three key parameters: trade volume, stop-loss level, and take-profit level. Buy and sell operations are represented as separate rows of this matrix. Thus, when calling the initialization method of the parent class, we set the window size of both the input data and the output results equal to 3, and set the sequence length to one third of the agent's action vector.

After the successful execution of the parent class operations, we initialize the newly introduced internal objects. First, we initialize the structures responsible for forming the agent-role tensor. We adapted this concept from the FinCon framework and adjusted it to the current task. The main advantage of this concept lies in dividing the responsibilities for analyzing the input data among several parallel agents, enabling them to focus on specific aspects of the analyzed sequence.

//--- Role int index = 0; if(!caRole[0].Init(10 * window_key, index, OpenCL, 1, optimization, iBatch)) return false; caRole[0].getOutput().Fill(1); index++; if(!caRole[1].Init(0, index, OpenCL, 10 * window_key, optimization, iBatch)) return false;

Next, we initialize the relative cross-attention module, which highlights key properties of the input data in accordance with the agent’s assigned role.

//--- State to Role index++; if(!cStateToRole.Init(0, index, OpenCL, window, window_key, units_count, heads, window_key, 10, optimization, iBatch)) return false;

Following the initial processing of the raw data, we return to the original Hidformer architecture, which includes a segmentation step before feeding data into the encoder. It is important to note that segmentation is performed independently in each tower, which helps avoid unwanted correlations between different data streams and improves the model's adaptability to heterogeneous input sequences.

In our modified version, we expanded the agent’s functionality by replacing the classical segmentation mechanism with a specialized S3 module. This module not only performs segmentation but also implements a mechanism of learnable segment shuffling. Such an approach makes it possible to better identify latent relationships between different parts of the sequence. As a result, the agent can form more robust and generalized representations.

//--- State index++; if(!cShuffle.Init(0, index, OpenCL, window, window * units_count, optimization, iBatch)) return false;

The data prepared in the previous steps is fed into the encoder, consisting of a recursive attention module and a convolutional block with feedback.

index++; if(!cRecursiveState.Init(0, index, OpenCL, window, window_key, units_count, heads, stack_size, optimization, iBatch)) return false; index++; if(!cResidualState.Init(0, index, OpenCL, window, window, units_count, optimization, iBatch)) return false;

Such an encoder allows us to analyze the input sequence in the context of the latest price, identifying likely support and resistance levels or areas of stable pattern formation.

At the next stage, we again deviate from the original Hidformer version and add a module for analyzing the agent's previously taken actions. First, we recursively analyze the latest action in the context of its historical sequence.

//--- Action index++; if(!cRecursiveAction.Init(0, index, OpenCL, 3, window_key, (action_space + 2) / 3, heads, stack_size, optimization, iBatch)) return false;

Then, we use a multi-scale cross-attention module to analyze the agent's policy in the context of dynamic market conditions.

index++; if(!cActionToState.Init(0, index, OpenCL, 3, window_key, (action_space + 2) / 3, heads, window, units_count, optimization, iBatch)) return false; //--- return true; }

The functionality of the FeedForward block is implemented through the capabilities of the parent class.

After successful initialization of all internal objects, we return the logical result of the operations to the calling program and complete the method.

We now proceed to designing the forward-pass algorithm, implemented within the feedForward method. The method parameters include a pointer to the object containing the input data.

bool CNeuronHidformerTSAgent::feedForward(CNeuronBaseOCL *NeuronOCL) { if(bTrain && !caRole[1].FeedForward(caRole[0].AsObject())) return false;

Inside the method, we begin by generating the tensor describing the agent's current role. However, this operation is performed only during model training. It is easy to see that during model inference, a fixed role tensor will be generated at each iteration of the feed-forward pass. This this step is redundant. Therefore, we first check the current operating mode and only then call the forward pass of the internal fully connected layer responsible for generating the role tensor. This approach eliminates unnecessary operations and reduces decision-making latency.

We then proceed to processing the received input data. First, we extract the elements relevant to the agent's role. This is done through the cross-attention module.

//--- State to Role if(!cStateToRole.FeedForward(NeuronOCL, caRole[1].getOutput())) return false;

Next, the enhanced environment state is segmented and shuffled.

//--- State if(!cShuffle.FeedForward(cStateToRole.AsObject())) return false;

It is then processed by the recursive attention module, which enriches the representation of the environment state with information about prior price-movement dynamics.

if(!cRecursiveState.FeedForward(cShuffle.AsObject())) return false; if(!cResidualState.FeedForward(cRecursiveState.AsObject())) return false;

At the next stage, we perform an in-depth analysis of the agent's behavior policy. First, the latest decision is analyzed in the context of previous actions stored in the memory of the recursive attention module.

//--- Action if(!cRecursiveAction.FeedForward(AsObject())) return false;

Then, we analyze the agent's policy in the context of the evolving market environment using the multi-scale cross-attention module.

if(!cActionToState.FeedForward(cRecursiveAction.AsObject(), cResidualState.getOutput())) return false;

You can see that the architecture of the action-analysis module is borrowed from the classical Transformer decoder. A classical decoder sequentially uses the modules Self-Attention → Cross-Attention → FeedForward. In our case, the Self-Attention module was replaced by a recursive attention module in accordance with the Hidformer framework. Following the same logic, we replaced multi-head Cross-Attention with multi-scale attention. The remaining component is the FeedForward block. It is implemented via the parent class. However, before using it, we must note that the input to this decoder-like structure consists of the results of the previous feed-forward pass of our method. For the correct execution of the backpropagation pass, we need to store this information. Therefore, we temporarily redirect the inherited data-buffer pointers and only then call the feed-forward method of the parent class.

if(!SwapBuffers(Output, PrevOutput)) return false; //--- return CResidualConv::feedForward(cActionToState.AsObject()); }

The logical result of these operations is returned to the calling program, and the method concludes.

The next step is constructing the backpropagation algorithms. The backpropagation pass in our objects is represented by two methods: calcInputGradients and updateInputWeights. The former ensures correct distribution of the error gradient among all objects involved in the decision-making process, proportionally to their influence on the final output. The latter performs optimization of the model's trainable parameters to minimize the total error. The updateInputWeights method is usually straightforward. It typically consists of calling the corresponding methods of internal objects containing trainable parameters, passing along the data saved during the feed-forward pass. The gradient-distribution method, however, is closely related to the feed-forward information flows and requires a more detailed explanation.

The parameters of the calcInputGradients method include a pointer to the input-data object. This is the same object that was passed during the feed-forward pass. This time, however, we must send into it the error gradient corresponding to the influence of the input data on the model's output. Obviously, a valid pointer is required to transfer this information. Therefore, inside the method, we immediately check the pointer's validity.

bool CNeuronHidformerTSAgent::calcInputGradients(CNeuronBaseOCL *NeuronOCL) { if(!NeuronOCL) return false;

After this small control block, we proceed to constructing the gradient-distribution algorithm.

The information flows of gradient distribution mirror the flows of the feed-forward pass but in reverse. The feed-forward pass ended with a call to the parent class method. Accordingly, gradient distribution begins by using inherited mechanisms. At this stage, we call the relevant method of the parent class, passing the error downward to the module responsible for multi-scale cross-attention over both the agent's policy and market dynamics.

if(!CResidualConv::calcInputGradients(cActionToState.AsObject())) return false;

Next, we must divide the resulting gradient between two information flows: analysis of the agent's policy and analysis of the environment state represented by the multivariate time series.

if(!cRecursiveAction.calcHiddenGradients(cActionToState.AsObject(), cResidualState.getOutput(), cResidualState.getGradient(), (ENUM_ACTIVATION)cResidualState.Activation())) return false;

First, we distribute the gradient along the policy-analysis branch. To do this, we must pass it through the recursive attention module responsible for processing the agent's previous actions. Note that the inputs to this block were the results of the previous feed-forward pass of our object. We previously saved them in a separate data buffer. For proper gradient distribution, we must temporarily restore these values to the result buffer while preserving the current results. Therefore, we once again substitute the buffer pointers.

Moreover, during gradient distribution, the values in the corresponding interface buffers will be overwritten. This is undesirable because these values are still needed for parameter updates. Thus, we also redirect the error-gradient buffer.

Only after ensuring the preservation of all necessary data do we perform the gradient-distribution operations through the recursive attention module. After successful execution, the buffer pointers are restored to their original state.

//--- Action CBufferFloat *temp = Gradient; if(!SwapBuffers(Output, PrevOutput) || !SetGradient(cRecursiveAction.getPrevOutput(), false)) return false; if(!calcHiddenGradients(cRecursiveAction.AsObject())) return false; if(!SwapBuffers(Output, PrevOutput)) return false; Gradient = temp;

We then proceed to gradient distribution along the multivariate time-series analysis path. First, we propagate the gradients to the level of the recursive attention module analyzing the environment state.

//--- State if(!cRecursiveState.calcHiddenGradients(cResidualState.AsObject())) return false;

Next, the gradient is passed to the segmentation and shuffling block.

if(!cShuffle.calcHiddenGradients(cRecursiveState.AsObject())) return false;

Following this branch further, we transmit the gradient to the cross-attention module analyzing the raw data in the context of the agent's role.

if(!cStateToRole.calcHiddenGradients(cShuffle.AsObject())) return false;

From this point, the gradient again splits into two flows: toward the input data object and toward the agent role formation branch.

if(!NeuronOCL.calcHiddenGradients(cStateToRole.AsObject(), caRole[1].getOutput(), caRole[1].getGradient(), (ENUM_ACTIVATION)caRole[1].Activation())) return false; //--- return true; }

It is worth noting that no further gradient propagation occurs along the role formation branch. The first layer of this MLP is fixed, and only the second neural layer contains trainable parameters, to which we have already passed the error signal.

Finally, we return the logical result of the execution to the calling program and complete the method.

This concludes our discussion of the algorithms used to build the methods of the time-series analysis agent for the environment state. You can find the full code of this object and all its methods in the attachments.

Working with the Frequency Domain

The next stage is to construct an agent for analyzing the frequency characteristics of the analyzed signal. It should be noted that the structure of this agent is quite similar to the previously created time-series analysis agent. At the same time, it has distinct features associated with transforming the input signal into the frequency domain. To isolate the high- and low-frequency components of the environment state signal, we implemented a discrete wavelet transform, borrowed from the Multitask-Stockformer framework.

The frequency-domain agent algorithms are implemented as the CNeuronHidformerFreqAgent object. Its structure is shown below.

class CNeuronHidformerFreqAgent : public CResidualConv { protected: CNeuronTransposeOCL cTranspose; CNeuronLegendreWaveletsHL cLegendre; CNeuronTransposeRCDOCL cHLState; CNeuronLinerAttention cAttentionState; CResidualConv cResidualState; CNeuronS3 cShuffle; CNeuronRecursiveAttention cRecursiveAction; CNeuronMultiScaleRelativeCrossAttention cActionToState; //--- virtual bool feedForward(CNeuronBaseOCL *NeuronOCL) override; virtual bool calcInputGradients(CNeuronBaseOCL *NeuronOCL) override; virtual bool updateInputWeights(CNeuronBaseOCL *NeuronOCL) override; public: CNeuronHidformerFreqAgent(void) {}; ~CNeuronHidformerFreqAgent(void) {}; //--- virtual bool Init(uint numOutputs, uint myIndex, COpenCLMy *open_cl, uint window, uint filters, uint units_count, uint heads, uint stack_size, uint action_space, ENUM_OPTIMIZATION optimization_type, uint batch); //--- virtual int Type(void) override const { return defNeuronHidformerFreqAgent; } //--- virtual bool Save(int const file_handle) override; virtual bool Load(int const file_handle) override; //--- virtual bool WeightsUpdate(CNeuronBaseOCL *source, float tau) override; virtual void SetOpenCL(COpenCLMy *obj) override; //--- virtual bool Clear(void) override; };

In the presented structure, one can easily notice similarities in the names of internal objects, indicating a related structure between the time-domain and frequency-domain agents. However, there are also differences, which we will examine in more detail when constructing the methods for this new class.

All internal objects are declared statically, which allows us to leave the constructor and destructor of the object empty. Initialization of all newly declared and inherited objects is performed within the Init method.

bool CNeuronHidformerFreqAgent::Init(uint numOutputs, uint myIndex, COpenCLMy *open_cl, uint window, uint filters, uint units_count, uint heads, uint stack_size, uint action_space, ENUM_OPTIMIZATION optimization_type, uint batch) { if(!CResidualConv::Init(numOutputs, myIndex, open_cl, 3, 3, (action_space + 2) / 3, optimization_type, batch)) return false;

The method parameters include a set of constants that allow unambiguous interpretation of the architecture of the object being created. Within the method, we first call the relevant method of the parent class, which already implements the necessary control points and initialization of inherited objects and interfaces. It should be noted that, despite the difference in data domains, the agent is expected to output the same trading-operations tensor. Therefore, the approaches described above for calling the parent class initialization method in the time-series agent are equally applicable here.

Next, we initialize the newly declared objects. Pay attention to a distinction in the design of agents for different domains. The frequency-domain agent does not have a role-generation module. In our implementation, we do not plan to use a large number of frequency-domain agents.

Additionally, the segmentation block has been replaced by a discrete wavelet transform module. The transformation from the time domain to the frequency domain is performed on unit sequences. For convenient handling of these sequences, we first transpose the input-data matrix.

int index = 0; if(!cTranspose.Init(0, index, OpenCL, units_count, window, optimization, iBatch)) return false;

The univariate time series are divided into equal segments. A discrete wavelet transform is applied to each segment, allowing us to extract significant structural components of the temporal dependencies. The minimum segment size is limited to five elements, striking a balance between analysis accuracy and computational cost.

index++; uint wind = (units_count>=20 ? (units_count + 3) / 4 : units_count); uint units = (units_count + wind - 1) / wind; if(!cLegendre.Init(0, index, OpenCL, wind, wind, units, filters, window, optimization, batch)) return false;

It should be noted that the output of the discrete wavelet transform module is a tensor containing both the high- and low-frequency components of the signal. The high-frequency component immediately follows the low-frequency component of each segment, and the data can be represented as a three-dimensional tensor [Segment, [Low, High], Filters].

For further analysis, it is important to separate the data into the respective components. However, since identical operations are applied to both signal types, it is more efficient to process them in parallel. Therefore, we do not explicitly split the signal into separate objects; instead, we transpose the tensor, which allows more efficient use of computational resources and accelerates data processing.

index++; if(!cHLState.Init(0, index, OpenCL, units * window, 2, filters, optimization, iBatch)) return false;

As provided by the authors of the Hidformer framework, we then apply a linear attention algorithm. In our case, we perform separate analyses of the high- and low-frequency components, enabling the identification of the most significant patterns and adaptive adjustment of the signal-processing strategy according to their frequency characteristics.

index++; if(!cAttentionState.Init(0, index, OpenCL, filters, filters, units* window, 2, optimization, iBatch)) return false;

The resulting outputs are passed through a convolutional block with feedback, serving as the FeedForward module of our frequency-domain encoder.

index++; if(!cResidualState.Init(0, index, OpenCL, filters, filters, 2 * units * window, optimization, iBatch)) return false;

Next, we initialize the agent-policy analysis block, analogous to that used in the construction of the time-series agent. But there is one caveat. For the linear attention module, the order of segments is irrelevant, since the analysis is applied to the entire sequence at once. When using the multi-scale cross-attention module, however, we must address the prioritization of segments, as this module was designed for time-series sequences and prioritizes the most recent elements.

To solve this problem, we use the segmenting and shuffling object. In this case, our data is already segmented, and the key focus is the learnable shuffling of segments. This allows the model to independently learn segment priority based on the training data.

index++; if(!cShuffle.Init(0, index, OpenCL, filters, cResidualState.Neurons(), optimization, iBatch)) return false;

We will not elaborate further on the functionality of objects used by the agent-policy analysis module, as the approaches described for the time-series agent are preserved.

//--- Action index++; if(!cRecursiveAction.Init(0, index, OpenCL, 3, filters, (action_space + 2) / 3, heads, stack_size, optimization, iBatch)) return false; index++; if(!cActionToState.Init(0, index, OpenCL, 3, filters, (action_space + 2) / 3, heads, filters, 2 * units * window, optimization, iBatch)) return false; //--- return true; }

Once all internal objects are successfully initialized, we complete the method, returning a logical result to the calling program.

To reduce article length, the methods for feed-forward and backpropagation passes are left for independent study. Their algorithms follow the same principles as those described for the time-series agent. The full code for both agents and their methods is provided in the attachment.

Top-Level Object

After constructing the objects of the multivariate time-series and frequency-domain towers, the next step in building the complete Hidformer framework is to combine them into a single structure and add a decoder. The authors of Hidformer used an MLP as a decoder for forecasting the expected continuation of the analyzed time series. Despite our modification of the task, a perceptron can still be used to generate the final decision. However, we went a step further, borrowing the concept of a hyper-agent from the MacroHFT framework. Inspired by this idea, we created the CNeuronHidformer object having the following structure.

class CNeuronHidformer : public CNeuronBaseOCL { protected: CNeuronTransposeOCL cTranspose; CNeuronHidformerTSAgent caTSAgents[4]; CNeuronHidformerFreqAgent caFreqAgents[2]; CNeuronMacroHFTHyperAgent cHyperAgent; CNeuronBaseOCL cConcatenated; //--- virtual bool feedForward(CNeuronBaseOCL *NeuronOCL) override; virtual bool updateInputWeights(CNeuronBaseOCL *NeuronOCL) override; virtual bool calcInputGradients(CNeuronBaseOCL *NeuronOCL) override; public: CNeuronHidformer(void) {}; ~CNeuronHidformer(void) {}; //--- virtual bool Init(uint numOutputs, uint myIndex, COpenCLMy *open_cl, uint window, uint window_key, uint units_count, uint heads, uint layers, uint stack_size, uint nactions, ENUM_OPTIMIZATION optimization_type, uint batch); //--- virtual int Type(void) override const { return defNeuronHidformer; } //--- virtual bool Save(int const file_handle) override; virtual bool Load(int const file_handle) override; //--- virtual bool WeightsUpdate(CNeuronBaseOCL *source, float tau) override; virtual void SetOpenCL(COpenCLMy *obj) override; //--- virtual bool Clear(void) override; };

In this architecture, one can clearly see the structural similarity to the CNeuronMacroHFT class from the MacroHFT framework. Essentially, the new structure represents a modified version of it, retaining the core design principles while introducing targeted changes to improve data-processing efficiency.

A key difference lies in the configuration of environment-analysis agents. In this version, six specialized agents are used: four for analyzing multivariate time series and two for processing input data in the frequency domain. To ensure a balanced analysis, all agents are evenly distributed between processing the direct and transposed representations of the input data. This architecture allows for a more detailed exploration of various aspects of the input data, revealing hidden patterns and adaptively adjusting the processing strategy.

Overall, the modifications to the agent structure introduce only minor adjustments to the algorithms of the object's methods. The main logic remains unchanged, and all key operational principles of the model are preserved. Therefore, we leave it to the reader to study the construction algorithms of the methods independently. The full code for this object and all its methods is provided in the attachment.

Model Architecture

A few words about the architecture of the trainable model. As you may have noticed, our constructed architecture is a synergy of the Hidformer and MacroHFT frameworks. The architecture of the trainable model and its training methods are no exception. We replicated the model architecture from the MacroHFT framework, modifying only a single layer.

//--- layer 2 if(!(descr = new CLayerDescription())) return false; descr.type = defNeuronHidformer; //--- Windows { int temp[] = {BarDescr, 120, NActions}; //Window, Stack Size, N Actions if(ArrayCopy(descr.windows, temp) < int(temp.Size())) return false; } descr.count = HistoryBars; descr.window_out = 32; descr.step = 4; // Scales descr.layers =3; descr.batch = 1e4; descr.activation = None; descr.optimization = ADAM; if(!actor.Add(descr)) { delete descr; return false; }

Otherwise, the operational architecture remained unchanged, including the use of the risk-management agent. A complete description of the model architecture, as well as the full code for the training and testing routines, is provided in the attachment, transferred unchanged from the previous article.

Testing

We have completed substantial work in implementing our interpretation of the approaches proposed by the Hidformer authors. We now arrive at the crucial stage: evaluating the effectiveness of our solutions on real historical data. In our implementation, we borrowed extensively from the MacroHFT framework. Therefore, it's logical to compare the new model performance with it. So, we train the new model on the training dataset previously compiled for training the MacroHFT-based implementation.

That training dataset was collected from historical data for the entire year of 2024 for the EURUSD currency pair on the M1 timeframe. All indicator parameters were set to their default values.

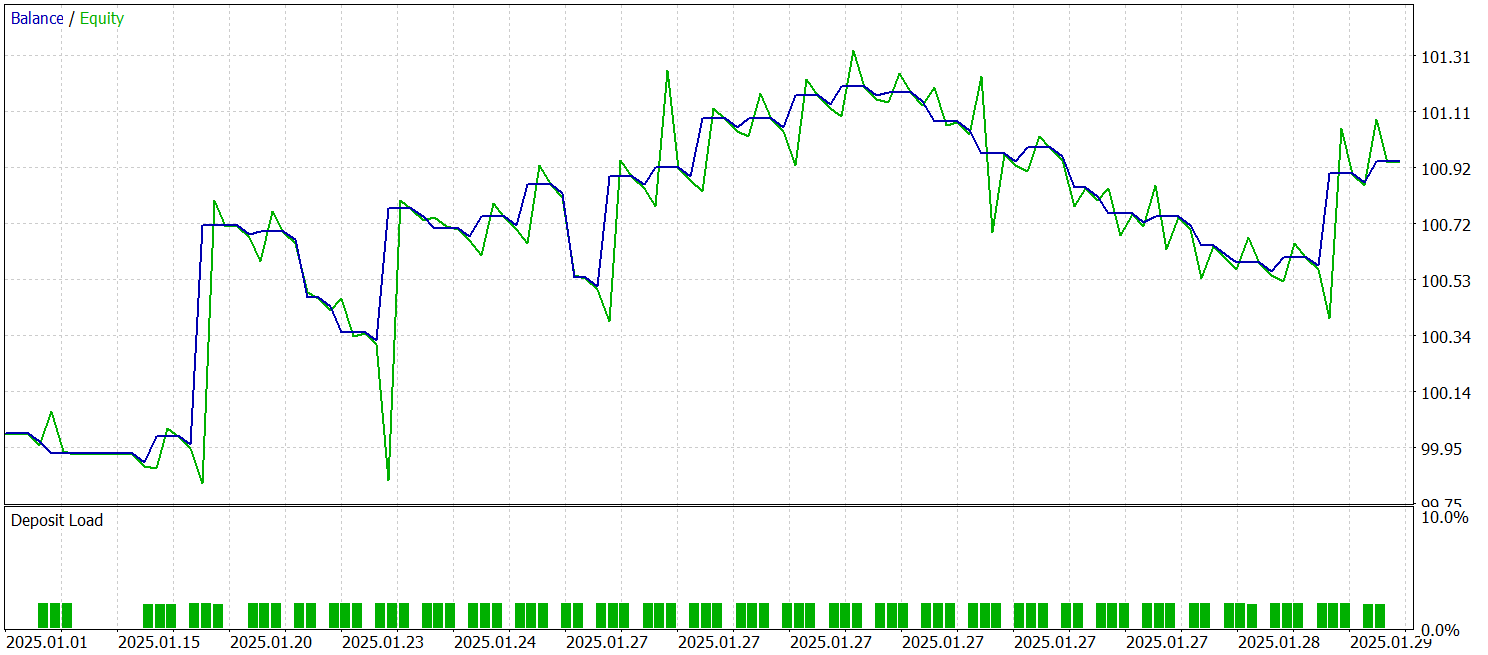

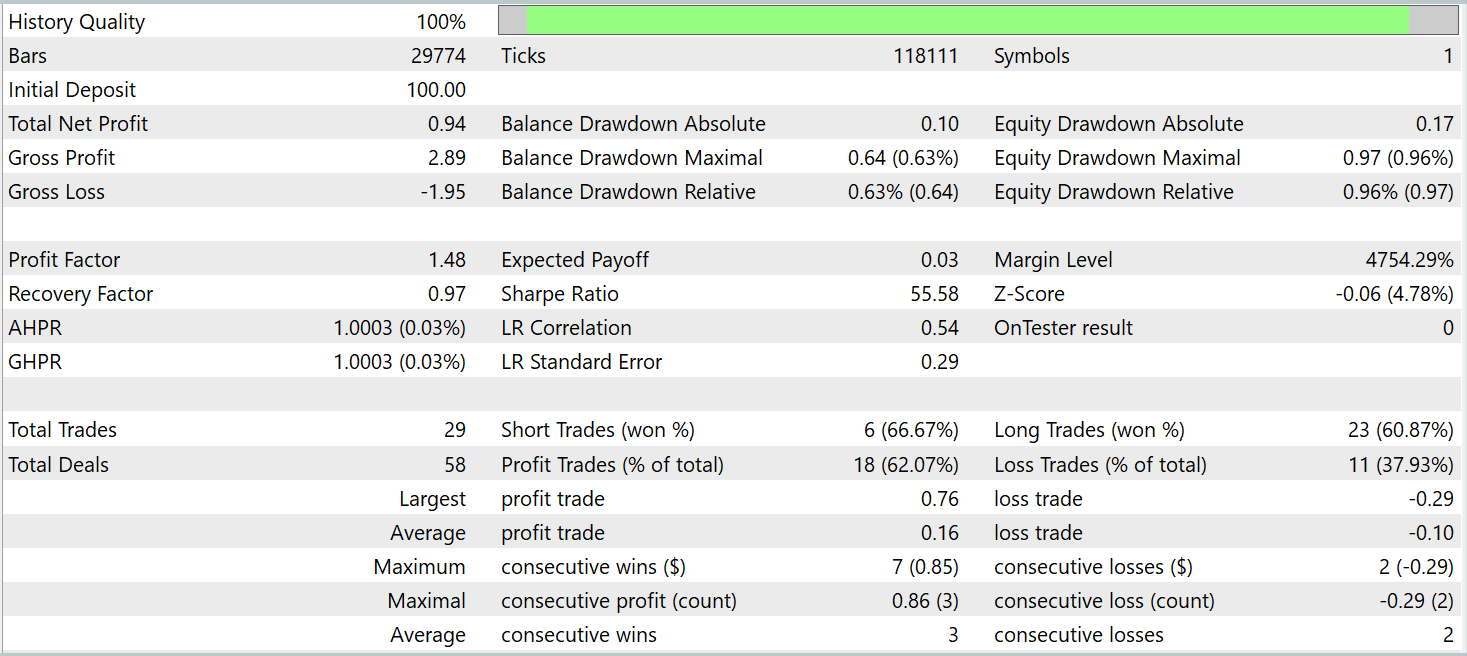

The same Expert Advisors are used for training and testing the model. Testing was conducted on historical data from January 2025, maintaining all other parameters. The test results are presented below.

The results show that the model achieved profit on historical data outside the training dataset. Overall, during the calendar month, the model executed 29 trades. This makes slightly more than one trade per trading day, which is not enough for high-frequency trading. At the same time, more than 60% of the trades were profitable, and the average profitable trade exceeded the average losing trade by 60%.

Conclusion

We explored the Hidformer framework, designed for analyzing and forecasting complex multivariate time series. The model demonstrates high efficiency thanks to its unique dual-tower encoder architecture. One tower analyzes the temporal structure of the input data, while the other operates in the frequency domain. The recursive attention mechanism uncovers complex price-change patterns, while linear attention reduces the computational complexity of analyzing long sequences.

In the practical part of this work, we implemented our own interpretation of the proposed approaches using MQL5. We trained the model on real historical data and tested it on out-of-sample data. The test results demonstrate the model's potential. However, before deploying it in live trading, the model must be trained on a more representative dataset, followed by comprehensive testing.

References

- Hidformer: Transformer-Style Neural Network in Stock Price Forecasting

- Hidformer: Hierarchical dual-tower transformer using multi-scale mergence for long-term time series forecasting

- Other articles from this series

Programs used in the article

| # | Name | Type | Description |

|---|---|---|---|

| 1 | Research.mq5 | Expert Advisor | Expert Advisor for collecting examples |

| 2 | ResearchRealORL.mq5 | Expert Advisor | Expert Advisor for collecting samples using the Real-ORL method |

| 3 | Study.mq5 | Expert Advisor | Model training Expert Advisor |

| 4 | Test.mq5 | Expert Advisor | Model testing Expert Advisor |

| 5 | Trajectory.mqh | Class library | System state and model architecture description structure |

| 6 | NeuroNet.mqh | Class library | A library of classes for creating a neural network |

| 7 | NeuroNet.cl | Library | OpenCL program code |

Translated from Russian by MetaQuotes Ltd.

Original article: https://www.mql5.com/ru/articles/17104

Warning: All rights to these materials are reserved by MetaQuotes Ltd. Copying or reprinting of these materials in whole or in part is prohibited.

This article was written by a user of the site and reflects their personal views. MetaQuotes Ltd is not responsible for the accuracy of the information presented, nor for any consequences resulting from the use of the solutions, strategies or recommendations described.

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use