MetaTrader 5 Machine Learning Blueprint (Part 7): From Scattered Experiments to Reproducible Results

Introduction

Throughout this series, we've covered crucial components of machine learning for trading: data structures, labeling and meta-labeling, sample weighting and purged cross-validation. But these techniques, powerful as they are individually, reach their full potential only when integrated into a cohesive research system. In this article, I'll demonstrate how to assemble these building blocks into a production-grade pipeline that transforms ad-hoc experiments into reproducible, auditable research and builds on the caching architecture developed in my previous article.

The code we'll explore isn't just another example, it's a major aspect of the system I use for developing trading models. It handles everything from raw tick data to ONNX models ready for deployment in MetaTrader 5, with comprehensive logging, caching, and analysis reports generated automatically along the way. For the sake of clarity, I will ignore some critical topics for now, such as feature importance analysis, and the selection of optimal barriers for the triple-barrier method, among others. This article assumes that these preceding research steps have already occurred, and as such focuses on the creation of reproducible pipelines. What makes a research system "production-grade"?

- Reproducibility: Run the same code twice, get identical results

- Traceability: Know exactly what data trained each model

- Efficiency: Cache expensive computations, never repeat work

- Validation: Catch errors before they reach live trading

- Documentation: Automatic reports that explain every decision

The Problem: Research Chaos

Before we dive into the solution, let's acknowledge the problem. Most trading ML research looks like this:

# Somewhere in notebook cell 47... df = load_data("EURUSD", "2020-01-01", "2023-12-31") features = calculate_indicators(df) X_train, y_train = features[:-1000], labels[:-1000] model = RandomForestClassifier(n_estimators=100) model.fit(X_train, y_train) # Score: 0.67 - is that good? What parameters did I use? # When did I run this? Which data version?

Three months later, you can't reproduce these results. The data has changed. You don't remember which features you used. The model file has no metadata. You're back to square one.

Not only is this inconvenient, it's dangerous. In live trading, irreproducible research means you can't trust your backtest. You can't debug failures. You can't iterate confidently.

The Solution: A Principled Pipeline

Our research system addresses these problems through four key principles:

- Time-Aware Caching: Never let future data leak into training, but cache everything safely

- Automatic Documentation: Generate comprehensive reports at every stage

- Organized Storage: Navigate your experiments by strategy, symbol, and parameters

- Validation First: Catch errors in research, not in production

Here's the high-level architecture:

Every stage is cached, every decision is logged, every output is validated.

I reiterate, this is a high-level architecture that is in no way meant to cover all steps in the development process.

Intelligent Data Architecture: Why Tick RAM Cache + Parquet Bars Changes Everything

Before we dive into the pipeline stages, let's examine a crucial architectural decision that makes the entire system practical: the data handling strategy.

The Tick Data Dilemma

When developing trading strategies, you face a classic optimization problem:

| Option 1: Load bars directly from broker (MetaTrader 5) | Option 2: Cache everything to disk | Option 3: Hybrid approach (the solution) |

|---|---|---|

|

|

|

Let me show you why this third approach is brilliant.

The TickDataLoader: RAM Caching Done Right

Here's the key insight: tick data should live in RAM, not on disk, because it's the source material you transform in multiple ways. The TickDataLoader class keeps track of all data already loaded in the current session. If we begin our model development with EURUSD data from 2023, and later decide to add 2021-2022 data, only the missing portion is loaded—the cache is extended seamlessly. Instead, TickDataLoader only obtains what was not in the cache and appends it to the preloaded data. The code below is a snippet from the TickDataLoaderclass. For the full code see the attached model_development.py.

class TickDataLoader: """ Loader for tick-level bid/ask data with intelligent local caching. Features: 1. Smart caching that checks if requested date range is within cached ranges 2. Handles partial overlaps by reusing available cached data 3. Memory management with cache size limits 4. Cache statistics tracking Notes ----- - Typical performance: ~0.5s for cached retrieval - Memory usage: ~100MB per 1M ticks """ def __init__(self, max_cache_size_mb: int = 3000, max_cached_symbols: int = 20): """ Initialize the tick data loader. Parameters ---------- max_cache_size_mb : int, optional Maximum cache size in MB (default: 5000MB) max_cached_symbols : int, optional Maximum number of symbols to keep in cache (default: 20) """ self._cache: Dict[Tuple[str, str], pd.DataFrame] = {} # (symbol, account_name) -> DataFrame self._cache_metadata: Dict[Tuple[str, str], Dict] = {} # (symbol, account_name) -> metadata self.max_cache_size_mb = max_cache_size_mb self.max_cached_symbols = max_cached_symbols self.cache_stats = { "hits": 0, "misses": 0, "partial_hits": 0, "total_loaded": 0, } def get_tick_data( self, symbol: str, start_date: str, end_date: str, account_name: str ) -> pd.DataFrame: """ Retrieve tick-level bid/ask data with intelligent caching. Parameters ---------- symbol : str Trading instrument symbol (e.g., 'EURUSD') start_date : str Start date in 'YYYY-MM-DD' format end_date : str End date in 'YYYY-MM-DD' format account_name : str MT5 account identifier for data retrieval Returns ------- pd.DataFrame Tick data with columns ['bid', 'ask'] indexed by timestamp Notes ----- - Checks if cached data fully covers requested date range - If partial coverage exists, loads only missing data - Merges cached and newly loaded data seamlessly """ cache_key = (symbol, account_name) start_dt, end_dt = date_conversion(start_date, end_date) # Check if we have cached data for this symbol/account if cache_key in self._cache: cached_df = self._cache[cache_key] metadata = self._cache_metadata[cache_key] cached_start, cached_end = date_conversion(metadata["start_date"], metadata["end_date"]) # Check if cached data fully covers requested range if cached_start <= start_dt and cached_end >= end_dt: self.cache_stats["hits"] += 1 logger.debug(f"Cache hit for {symbol} {start_date} to {end_date}") # Return subset of cached data mask = (cached_df.index >= start_dt) & (cached_df.index <= end_dt) return cached_df[mask].copy() # Check if there's partial overlap if cached_end >= start_dt and cached_start <= end_dt: self.cache_stats["partial_hits"] += 1 logger.debug(f"Partial cache hit for {symbol}") return self._load_with_partial_cache( symbol, start_date, end_date, account_name, cache_key ) # No cache hit, load all data self.cache_stats["misses"] += 1 logger.debug(f"Cache miss for {symbol} {start_date} to {end_date}") return self._load_and_cache_data(symbol, start_date, end_date, account_name, cache_key)

The system handles three scenarios intelligently:

Below is an example of using the TickDataLoader class:

# Initialize the loader once per session from ..production.model_development import TickDataLoader loader = TickDataLoader( max_cache_size_mb=3000, # 3GB RAM limit max_cached_symbols=20, # Cache up to 20 symbols ) # First request - loads from disk/MT5 and caches ticks = loader.get_tick_data( symbol="EURUSD", start_date="2023-01-01", end_date="2023-12-31", account_name="FUNDEDNEXT_STLR2_6K" ) # Takes ~30 seconds (first load) # Second request - same data, instant from RAM ticks = loader.get_tick_data( symbol="EURUSD", start_date="2023-01-01", end_date="2023-12-31", account_name="FUNDEDNEXT_STLR2_6K" ) # Takes ~0.5 seconds (cache hit) # Partial request - subset is instant ticks = loader.get_tick_data( symbol="EURUSD", start_date="2023-01-01", end_date="2023-03-31", account_name="FUNDEDNEXT_STLR2_6K" ) # Takes ~0.5 seconds (subset from cache) ticks = loader.get_tick_data( symbol="EURUSD", start_date="2022-01-01", end_date="2023-12-31", account_name="FUNDEDNEXT_STLR2_6K" ) # Takes ~15 seconds (only 2022 data)

And below are features that use tick data:

# Example of features that use tick data

from ..util.volatility import two_time_scale_realized_vol

def two_time_scale_realized_vol(

tick_prices: pd.Series, slow_freq: str = "5min"

) -> float:

"""

Two-Time-Scale Realized Volatility Estimator

Advanced estimator for tick data that removes microstructure noise while

preserving information. Combines high-frequency and low-frequency sampling

to extract true volatility signal.

**What it measures:**

- True underlying volatility from noisy tick data

- Removes bid-ask bounce and other microstructure effects

- Preserves information lost in simple low-frequency sampling

**Mathematical foundation:**

- TSRV = RV_slow - (n_slow/n_fast) * (RV_fast - RV_slow)

- Uses ratio of observation counts to properly scale noise estimate

- Asymptotically consistent under jump-diffusion models

**Best used for:**

- High-frequency trading strategies

- When you have access to tick data

- Precision-critical applications (research, risk management)

- Markets with significant microstructure noise

**Advantages:**

- Most accurate volatility estimate for tick data

- Removes upward bias from microstructure noise

- Retains more information than sparse sampling

- Theoretically well-founded

**Computational considerations:**

- More intensive than simple realized volatility

- Requires choice of slow sampling frequency

- Benefits increase with data quality and frequency

**Typical slow frequencies:**

- 1 minute: Very liquid assets, high precision needed

- 5 minutes: Most common, good noise reduction

- 15-30 minutes: Less liquid assets

:param tick_prices: (pd.Series) Tick-level price data, datetime indexed

:param slow_freq: (str) Slow sampling frequency ('5min', '1min', etc.)

:return: (float) Two-time-scale realized volatility estimate

"""

# Fast scale (tick-by-tick)

tick_returns = np.log(tick_prices / tick_prices.shift(1)).dropna()

rv_fast = (tick_returns**2).sum()

n_fast = len(tick_returns)

# Slow scale (e.g., 5-minute)

slow_prices = tick_prices.resample(slow_freq).last().dropna()

slow_returns = np.log(slow_prices / slow_prices.shift(1)).dropna()

rv_slow = (slow_returns**2).sum()

n_slow = len(slow_returns)

# Two-time-scale estimator with proper scaling

if n_fast > 0 and n_slow > 0:

tsrv = rv_slow - (n_slow / n_fast) * (rv_fast - rv_slow)

return max(tsrv, 0) # Ensure non-negative result

else:

return rv_slow

two_time_scale_vol = two_time_scale_realized_vol(tick_prices=ticks["bid"], slow_freq="5min") Why RAM Instead of Disk?

Think about your typical research workflow:

# You might experiment with: tick_bars_M1 = make_bars(ticks, "tick", "M1", "mid_price") tick_bars_M5 = make_bars(ticks, "tick", "M5", "mid_price") volume_bars = make_bars(ticks, "volume", 1000, "mid_price") dollar_bars = make_bars(ticks, "dollar", 5000, "mid_price") # And different price types: tick_bars_bid = make_bars(ticks, "tick", "M1", "bid") tick_bars_ask = make_bars(ticks, "tick", "M1", "ask")You're creating 6 different bar types from the same tick data. If you cached ticks to disk and bars to disk, you'd be storing the same base data multiple times in slightly different aggregations. That's wasteful. You might also decide that you want to create microstructural features (which need tick data). For these reasons, it is best to keep tick data in RAM incase you need it down the road.

Instead:

- Ticks live in RAM (fast access, cleared between sessions)

- Each unique bar configuration gets cached to Parquet (persistent, compact)

- The tick data serves as the "source of truth" for the session

- Parquet files serve as the "compiled artifacts" for long-term storage

The TickDataLoader + Parquet architecture works because it recognizes a fundamental truth about machine learning research:

Raw data should be fast (RAM), processed data should be persistent (Parquet), and you should never duplicate what you can regenerate.

This data architecture scales from individual research to team collaboration. When everyone works with Parquet files, you get:

- Consistent data types (no more "it works on my machine")

- Efficient storage (version control friendly)

- Fast iteration (the cost of experiments approaches zero)

- Reproducibility (Parquet files are binary-stable)

Compare this to CSV-based workflows where you're constantly fighting with:

- Inconsistent date parsing

- Float precision issues

- Encoding problems

- Slow load times

- Large file sizes

- Schema validation headaches

The initial investment in setting up Parquet-based storage pays dividends every single day. And when you combine it with intelligent RAM caching of source data (ticks), you get a system that's both fast and efficient—no compromises necessary.

The Workflow

Let me walk you through a real example: developing a Bollinger Band reversal strategy for EURUSD. We'll see exactly what happens at each stage and what artifacts get generated.

Stage 1: Configuration

Everything starts with configuration. Not scattered parameters across multiple files, but a single source of truth:

from model_development import ModelDevelopmentPipeline from strategies import BollingerBandStrategy # Data configuration data_config = { "symbol": "EURUSD", "train_start": "2023-01-01", "train_end": "2023-12-31", "account_name": "FUNDEDNEXT_STLR2_6K", "bar_type": "tick", "bar_size": "M1", # Will be converted to tick count "price": "mid_price" } # Feature configuration feature_config = { "func": calculate_bollinger_features, "params": { "window": 20, "num_std": 2.0 } } # Triple-barrier labeling target_config = { "func": get_daily_vol, "params": {"lookback": 20} } label_config = { "profit_target": 1.0, "stop_loss": 2.0, "max_holding_period": {"days": 1}, "min_ret": 0.0, "vertical_barrier_zero": True, "filter_as_series": False } # Model training parameters model_params = { "pipe_clf": RandomForestClassifier( criterion="entropy", class_weight="balanced_subsample", min_weight_fraction_leaf=0.05 ), "param_grid": { "n_estimators": [100, 200, 300], "max_depth": [3, 5, 7, 10], "min_samples_split": [2, 5, 10] }, "cv_splits": 5, "bagging_n_estimators": 10, "n_jobs": -1, "random_state": 42 } # Initialize strategy strategy = BollingerBandStrategy( window=20, std=2.0, )

Notice how every parameter is explicit and documented. Three months from now, you'll know exactly what you did.

Stage 2: Pipeline Initialization

Now we create the pipeline with intelligent file management:

pipeline = ModelDevelopmentPipeline(

strategy=strategy,

data_config=data_config,

feature_config=feature_config,

target_config=target_config,

label_config=label_config,

model_params=model_params,

base_dir="Models"

)

Behind the scenes, this creates a structured directory: Models/ └── BollingerBandStrategy/ └── EURUSD/ └── FUNDEDNEXT_STLR2_6K/ └── tick/ └── M1/ └── 20230101_20231231/ └── a3f7b2e9/ # Config hash ├── config.json ├── logs/ ├── plots/ └── reports/Every configuration gets its own directory. No more "model_v2_final_REALLY_FINAL.pkl".

Stage 3: Execution

With configuration complete, we run the entire pipeline:

model, features, metrics, config = pipeline.run( generate_reports=True, save=True, export_onnx=True, verbose=True )Now the magic happens. Let's see what occurs at each stage:

Step 1: Data Loading (with Smart Caching)

[Step 1/7] Loading training data...

✓ Cache hit for EURUSD 2023-01-01 to 2023-12-31

✓ Retrieved 15,847,392 ticks in 0.4s

✓ Constructed 262,800 M1 bars

The system checks if we've already loaded this data. If so, it's retrieved from cache in milliseconds rather than minutes. But here's the crucial part: the caching is time-aware. It tracks what data was accessed when, preventing future data from leaking into your training set.

# From model_development.py @cacheable(time_aware=True) def load_and_prepare_training_data(symbol, start_date, end_date, ...): tick_df = loader.get_tick_data(symbol, start_date, end_date, account_name) data = make_bars(tick_df, bar_type, bar_size, price) # Log data access for contamination tracking log_data_access( dataset_name=f"{symbol}_{bar_type}_{bar_size}_{price}".lower(), start_date=data.index[0], end_date=data.index[-1], purpose="train" ) return dataStep 2: Feature Engineering

✓ Generated 47 features

- 12 Bollinger Band features

- 15 momentum features

- 8 volume features

- 12 time-based features

@cacheable(time_aware=True) def create_feature_engineering_pipeline(data, feature_config, data_config): func = feature_config["func"] features = func(data, **feature_config["params"]) time_feat = get_time_features(data, timeframe=data_config["bar_size"]) return features.join(time_feat).dropna()If your feature function changes, the cache automatically invalidates. If only the data changes, features are recomputed efficiently.

Step 3: Label Generation

[Step 3/7] Generating events...

✓ Generated 89,247 events

✓ Label distribution:

- Long (1): 38,562 (43.2%)

- None (0): 24,891 (27.9%)

- Short (-1): 25,794 (28.9%)

@cacheable() def generate_events_triple_barrier(data, strategy, target_config, profit_target, stop_loss, ...): # Calculate dynamic barriers based on volatility close = data["close"] fn = target_config["func"] params = target_config["params"] target = fn(close, **params) # Get entry signals from strategy side, t_events = get_entries(strategy, data, target.mean()) # Apply triple-barrier method vb = add_vertical_barrier(t_events, close, **max_holding_period) events = triple_barrier_labels(close, target, t_events, vertical_barrier_times=vb, side_prediction=side, pt_sl=[profit_target, stop_loss], ...) # Add sample weights events = get_event_weights(events, close) return events

Step 4: Sample Weight Optimization

Here's where it gets interesting. Rather than guessing at sample weights, we search for the optimal weighting scheme:

Testing weighting schemes:

- unweighted + linear decay

- unweighted + exponential decay

- return-based + linear decay

- return-based + exponential decay

- uniqueness + linear decay

- uniqueness + exponential decay

✓ Best scheme: uniqueness_linear_0.7428 (CV Score: 0.6847)

The system tries multiple weighting approaches and picks the one that performs best on purged cross-validation:

@cacheable() def get_optimal_sample_weight( data_index: pd.DatetimeIndex, events: pd.DataFrame, features: pd.DataFrame, cv_splits: int = 5, n_iter: int = 10, ) -> pd.Series: """ Compute best sample weight with time decay. Parameters ---------- data_index: pd.DatetimeIndex Price data index. events : pd.DataFrame Event labels with uniqueness weights. features: pd.DataFrame Training features cv_splits : int, optional Number of cross-validation splits (default: 5). n_iter : int, optional Number of random search iterations (default: 10). Returns ------- weights : pd.Series Computed sample weights. cv_results : dict Cross-validation results. """ valid_index = features.index.intersection(events.index) cont = events.loc[valid_index] X = features.loc[valid_index] y = cont["bin"] classifier = RandomForestClassifier( criterion="entropy", class_weight="balanced_subsample", max_samples=cont["tW"].mean(), max_depth=4, min_weight_fraction_leaf=0.05, ) scoring = "f1" if set(y.unique()) == {0, 1} else "neg_log_loss" cv_gen = PurgedKFold(n_splits=cv_splits, t1=cont["t1"], pct_embargo=0.02) weights = [ ("return", cont["w"]), ("unweighted", pd.Series(1.0, index=cont.index)), ("uniqueness", cont["tW"]), ] best_score = 0 cv_results = pd.DataFrame() for scheme, weight in tqdm(weights, desc="Analyzing weighting schemes", total=len(weights)): scores = ml_cross_val_score( classifier, X, y, cv_gen, sample_weight_train=weight, sample_weight_score=weight, scoring=scoring, ) score = scores.mean() cv_results[scheme] = scores if not np.isinf(score) and score > best_score: best_score = score best_weight = weight best_scheme = scheme est = weighted_estimator(classifier, cont, data_index) param_distributions = { "scheme": [best_scheme], "decay": uniform(0, 1), # decay factor between 0 and 1 inclusive "linear": [True, False], } gs = RandomizedSearchCV( estimator=est, param_distributions=param_distributions, n_iter=n_iter, cv=cv_gen, scoring=scoring, n_jobs=-1, random_state=42, refit=False, ) gs.fit(X, y) scheme, decay, linear = [gs.best_params_[k] for k in ["scheme", "decay", "linear"]] best_scheme = f"{scheme}_{'linear' if linear else 'exp'}_{decay}" logger.info(f"Best sample weight scheme: {best_scheme}") decay_vec = get_weights_by_time_decay_optimized( triple_barrier_events=cont, close_index=data_index, last_weight=decay, linear=linear, av_uniqueness=cont["tW"], ) best_weight *= decay_vec cv_results = { "best_score": best_score, "cv_results_scheme": cv_results, "cv_results": pd.DataFrame(gs.cv_results_), "scoring": scoring, "best_scheme": best_scheme, } return best_weight, cv_results

In this manner, you discover which weighting scheme actually helps your specific strategy.

Step 5: Meta-Features

✓ Added 8 meta-features

- rolling_accuracy_20, rolling_accuracy_50

- rolling_precision_20, rolling_precision_50

- rolling_recall_20, rolling_recall_50

- rolling_f1_20, rolling_f1_50

These features tell the model how well it's been doing recently, which can improve meta-labeling performance. The calculation is optimized with Numba for speed:

@njit(parallel=True, fastmath=True, cache=True) def _rolling_metrics_numba(y_true, y_pred, weights, window): """Numba-accelerated rolling metrics calculation.""" n = len(y_true) accuracy = np.full(n, np.nan) precision = np.full(n, np.nan) recall = np.full(n, np.nan) f1 = np.full(n, np.nan) for i in prange(window - 1, n): start = i - window + 1 tp = fp = tn = fn = 0.0 # Inner loop for window for j in range(start, i + 1): if y_true[j] == 1 and y_pred[j] == 1: tp += weights[j] elif y_true[j] == 0 and y_pred[j] == 1: fp += weights[j] elif y_true[j] == 0 and y_pred[j] == 0: tn += weights[j] elif y_true[j] == 1 and y_pred[j] == 0: fn += weights[j] total = tp + fp + tn + fn if total > 0: accuracy[i] = (tp + tn) / total denom_prec = tp + fp if denom_prec > 0: precision[i] = tp / denom_prec denom_rec = tp + fn if denom_rec > 0: recall[i] = tp / denom_rec if not np.isnan(precision[i]) and not np.isnan(recall[i]): denom_f1 = precision[i] + recall[i] if denom_f1 > 0: f1[i] = 2 * (precision[i] * recall[i]) / denom_f1 return accuracy, precision, recall, f1

Step 6: Model Training with Hyperparameter Search

This is the heart of the system—intelligent hyper-parameter optimization with proper cross-validation:

[Step 6/7] Training model with cross-validation...

Grid Search Progress: Testing 81 parameter combinations

Using 5-fold purged cross-validation

Embargo: 1% between folds

[████████████████████████████████████] 81/81 (100%)

✓ Best parameters found:

- n_estimators: 200

- max_depth: 7

- min_samples_split: 5

✓ Cross-validation scores:

- Mean F1: 0.6847 ± 0.0234

- Fold 0: 0.6923

- Fold 1: 0.6801

- Fold 2: 0.6889

- Fold 3: 0.6712

- Fold 4: 0.6912

✓ Training bagged ensemble (10 estimators)...

✓ Model training complete

The hyper-parameter search uses purged k-fold cross-validation to prevent leakage:

def train_model_with_cv( features: pd.DataFrame, events: pd.DataFrame, sample_weight: np.ndarray, pipe_clf: Union[ClassifierMixin, Pipeline], param_grid: Dict, cv_splits: int = 5, bagging_n_estimators: int = 0, bagging_max_samples: float = 1.0, bagging_max_features: float = 1.0, rnd_search_iter: int = 0, n_jobs: int = -1, pct_embargo: float = 0.02, random_state: int = None, verbose: int = 0, ) -> Tuple[RandomForestClassifier, Dict]: """ Train model with cross-validation using cached hyperparameter search. Parameters ---------- features : pd.DataFrame Feature matrix. events : pd.DataFrame Event labels. sample_weight : np.ndarray Sample weights aligned with events. pipe_clf : sklearn.Pipeline Pipeline including classifier. param_grid : dict Hyperparameter grid for search. cv_splits : int, default=5 Number of CV splits. bagging_n_estimators : int, default=0 Number of bagging estimators. bagging_max_samples : float, default=1.0 Max samples for bagging. bagging_max_features : float, default=1.0 Max features for bagging. rnd_search_iter : int, default=0 Randomized search iterations. n_jobs : int, default=-1 Parallel jobs. pct_embargo : float, default=0.02 Embargo percentage for purging CV splits. random_state : int, optional Random seed. verbose : int, default=0 Verbosity flag. Returns ------- best_model : RandomForestClassifier Trained best model. cv_results : dict Cross-validation results. """ valid_index = features.index.intersection(events.index) cont = events.loc[valid_index] X = features.loc[valid_index] y = cont["bin"] t1 = cont["t1"] w = sample_weight.loc[valid_index] best_model, cv_results = clf_hyper_fit( features=X, labels=y, t1=t1, pipe_clf=pipe_clf, param_grid=param_grid, cv=cv_splits, bagging_n_estimators=bagging_n_estimators, bagging_max_samples=bagging_max_samples, bagging_max_features=bagging_max_features, rnd_search_iter=rnd_search_iter, n_jobs=n_jobs, pct_embargo=pct_embargo, random_state=random_state, verbose=verbose, sample_weight=w, ) return best_model, cv_results

- Performance distribution across all parameter combinations

- Score vs stability scatter plot

- Score vs training time analysis

- Parameter importance rankings

- Cross-validation fold consistency

Step 7: Feature Importance Analysis

[Step 7/7] Analyzing feature importance... 2025-12-16 11:18:21 [info ] pipeline_step duration_seconds=0.1509995460510254 metrics={'top_feature': 'rolling_accuracy_20'} status=completed step=feature_analysis Top 10 Features: feature importance rolling_accuracy_20 0.166330 rolling_f1_20 0.132372 rolling_accuracy_50 0.131260 rolling_f1_50 0.109463 spread 0.029035 d1_vol 0.025773 hour_cos_h2 0.022493 ret_1_lag_1 0.022391 parkinson_vol_10 0.019278 london_session_vol 0.018018

Feature importance helps us understand what the model learned and identify potential issues.

Stage 4: Automated Report Generation

After training completes, the system automatically generates comprehensive analysis reports. This is what the output after completion looks like:

2025-12-16 11:14:08 | afml.production.model_development | INFO | Starting pipeline for EURUSD 2025-12-16 11:14:08 | afml.production.model_development | INFO | Training period: 2022-01-01 to 2023-12-31 2025-12-16 11:14:08 | afml.production.model_development | INFO | Output directory: Models\Bollinger_w10_std1_5\EURUSD\FUNDEDNEXT_STLR2_6K\time\M1\20220101_20231231\bdad004f ====================================================================== PRODUCTION MODEL DEVELOPMENT PIPELINE ====================================================================== Configuration -------------------------------------------------- strategy Bollinger_w10_std1.5 symbol EURUSD training_start 2022-01-01 training_end 2023-12-31 account_name FUNDEDNEXT_STLR2_6K bar_type time bar_size M1 price mid_price target_lookback 10 profit_target 1 stop_loss 2 max_holding_period {'days': 1} min_ret 0 vertical_barrier_zero True filter_as_series False 2025-12-16 11:14:09 [info ] pipeline_step status=started step=pipeline_start strategy=Bollinger_w10_std1.5 symbol=EURUSD train_period=2022-01-01_2023-12-31 [Step 1/7] Loading training data... 2025-12-16 11:14:09 | afml.cache.unified_cache_system | DEBUG | Cache HIT: afml.production.model_development.load_and_prepare_training_data (key: d890725d...) 2025-12-16 11:14:09 [info ] pipeline_step duration_seconds=0.10399937629699707 metrics={'samples': 738824} status=completed step=data_loading ✓ Loaded 738,824 samples [Step 2/7] Computing features... 2025-12-16 11:14:09 | afml.cache.unified_cache_system | DEBUG | Cache HIT: afml.production.model_development.create_feature_engineering_pipeline (key: 4e32ea77...) 2025-12-16 11:14:09 [info ] pipeline_step duration_seconds=0.699995756149292 metrics={'features_generated': 68} status=completed step=feature_engineering ✓ Generated 68 features [Step 3/7] Generating events... 2025-12-16 11:14:09 | afml.cache.unified_cache_system | DEBUG | Cache HIT: afml.production.model_development.generate_events_triple_barrier (key: 5a7b1eb0...) 2025-12-16 11:14:09 [info ] pipeline_step duration_seconds=0.14899849891662598 metrics={'events_generated': 75975, 'label_distribution': count proportion bin 1 49,791 0.65536 0 26,184 0.34464, 'average_uniqueness': 0.4667911271632548} status=completed step=label_generation ✓ Generated events: count proportion bin 1 49,791 0.65536 0 26,184 0.34464 Average Uniqueness: 0.4668 [Step 4/7] Computing sample weights... 2025-12-16 11:18:04 | afml.production.model_development | INFO | Best Weighting Scheme: Uniqueness Exp 0.05808 2025-12-16 11:18:07 | afml.cache.unified_cache_system | DEBUG | Cache MISS: afml.production.model_development.find_optimal_sample_weight (key: 9d10ce42...) (00:03:57) 2025-12-16 11:18:07 [info ] pipeline_step duration_seconds=237.31548690795898 metrics={'weighting_scheme': 'uniqueness_exp_0.05808361216819946', 'weight_cv_score': 0.7457131539000748} status=completed step=weight_computation ✓ Best weighting scheme: uniqueness_exp_0.05808361216819946 [Step 5/7] Computing rolling meta-label features... 2025-12-16 11:18:07 | afml.cache.unified_cache_system | DEBUG | Cache HIT: afml.production.model_development.calculate_rolling_metrics (key: ae8cdce2...) 2025-12-16 11:18:20 [info ] pipeline_step duration_seconds=13.350001573562622 metrics={'meta_features_added': 8, 'features_after_preprocessing': 72, 'features_removed': -4} status=completed step=meta_features_preprocessing ✓ Computed rolling meta-label features ✓ Preprocessed features: 72 features retained [Step 6/7] Training model with cross-validation... 2025-12-16 11:18:21 | afml.cache.unified_cache_system | DEBUG | Cache HIT: afml.cross_validation.hyper_fit.clf_hyper_fit_internal (key: 907bd2af...) 2025-12-16 11:18:21 [info ] pipeline_step duration_seconds=0.4719998836517334 metrics={'cv_score': 0.6915768921130778, 'best_params': {'clf__max_depth': 6, 'clf__max_features': 0.12075618253727419, 'clf__min_samples_leaf': 3, 'clf__min_samples_split': 13, 'clf__min_weight_fraction_leaf': 0.28140549728612524, 'clf__n_estimators': 369}, 'n_splits': 5} status=completed step=model_training ✓ Best CV score: 0.6916 ✓ Best params: {'clf__max_depth': 6, 'clf__max_features': 0.12075618253727419, 'clf__min_samples_leaf': 3, 'clf__min_samples_split': 13, 'clf__min_weight_fraction_leaf': 0.28140549728612524, 'clf__n_estimators': 369} [Step 7/7] Analyzing feature importance... 2025-12-16 11:18:21 [info ] pipeline_step duration_seconds=0.1509995460510254 metrics={'top_feature': 'rolling_accuracy_20'} status=completed step=feature_analysis Top 10 Features: feature importance rolling_accuracy_20 0.166330 rolling_f1_20 0.132372 rolling_accuracy_50 0.131260 rolling_f1_50 0.109463 spread 0.029035 d1_vol 0.025773 hour_cos_h2 0.022493 ret_1_lag_1 0.022391 parkinson_vol_10 0.019278 london_session_vol 0.018018 [Generating Reports] Creating analysis reports... 🔍 Running hyperparameter analysis... ================================================================================ HYPERPARAMETER ANALYSIS REPORT ================================================================================ 1. TOP PERFORMING MODELS (sorted by mean_test_score): -------------------------------------------------- params mean_test_score std_test_score mean_fit_time 4 {'clf__max_depth': 6, 'clf__max_features': 0.12075618253727419, 'clf__min_samples_leaf': 3, 'clf__min_samples_split': 13, 'clf__min_weight_fraction_leaf': 0.28140549728612524, 'clf__n_estimators': 369} 0.691577 0.011027 28.989994 2 {'clf__max_depth': 4, 'clf__max_features': 0.15077042112439024, 'clf__min_samples_leaf': 8, 'clf__min_samples_split': 13, 'clf__min_weight_fraction_leaf': 0.4723487190570876, 'clf__n_estimators': 435} 0.683852 0.011899 28.105996 6 {'clf__max_depth': 4, 'clf__max_features': 0.9539969835279999, 'clf__min_samples_leaf': 2, 'clf__min_samples_split': 10, 'clf__min_weight_fraction_leaf': 0.05718481349909639, 'clf__n_estimators': 435} 0.677322 0.006976 614.569299 17 {'clf__max_depth': 4, 'clf__max_features': 0.8984914683186939, 'clf__min_samples_leaf': 1, 'clf__min_samples_split': 4, 'clf__min_weight_fraction_leaf': 0.10381741067223577, 'clf__n_estimators': 180} 0.675696 0.006911 175.406800 1 {'clf__max_depth': 5, 'clf__max_features': 0.5133240027692805, 'clf__min_samples_leaf': 5, 'clf__min_samples_split': 5, 'clf__min_weight_fraction_leaf': 0.11429006806487335, 'clf__n_estimators': 180} 0.670490 0.007110 95.500397 5 {'clf__max_depth': 3, 'clf__max_features': 0.14180537144799796, 'clf__min_samples_leaf': 3, 'clf__min_samples_split': 8, 'clf__min_weight_fraction_leaf': 0.1267358556592812, 'clf__n_estimators': 216} 0.669676 0.009235 33.474998 10 {'clf__max_depth': 4, 'clf__max_features': 0.905344615384884, 'clf__min_samples_leaf': 8, 'clf__min_samples_split': 15, 'clf__min_weight_fraction_leaf': 0.13819228808861533, 'clf__n_estimators': 239} 0.669449 0.008087 196.870216 16 {'clf__max_depth': 4, 'clf__max_features': 0.1858691048413702, 'clf__min_samples_leaf': 7, 'clf__min_samples_split': 6, 'clf__min_weight_fraction_leaf': 0.37832278025212884, 'clf__n_estimators': 409} 0.667428 0.007923 36.593196 13 {'clf__max_depth': 5, 'clf__max_features': 0.4810613326357327, 'clf__min_samples_leaf': 1, 'clf__min_samples_split': 13, 'clf__min_weight_fraction_leaf': 0.18206967862311718, 'clf__n_estimators': 112} 0.664284 0.002792 40.329997 12 {'clf__max_depth': 3, 'clf__max_features': 0.3528410587186427, 'clf__min_samples_leaf': 9, 'clf__min_samples_split': 16, 'clf__min_weight_fraction_leaf': 0.12437012257835113, 'clf__n_estimators': 394} 0.664078 0.007689 133.290791 2. PERFORMANCE SUMMARY: -------------------------------------------------- Average mean_test_score: 0.6656 ± 0.0106 Best mean_test_score: 0.6916 Worst mean_test_score: 0.6482 Performance Range: 0.0434 3. STABILITY ANALYSIS: -------------------------------------------------- Models with stable performance (std ≤ 0.03): 20 Best stable model: 0.6916 ± 0.0110 4. TIME-EFFICIENCY ANALYSIS: -------------------------------------------------- 5. HYPERPARAMETER TRENDS: -------------------------------------------------- Parameter: clf__max_depth Optimal value: 4 (score: 0.6716) Performance by value: score_mean score_std count fold_std_mean time_mean param_clf__max_depth 4 0.6716 0.0098 6 0.0088 184.0137 6 0.6659 0.0177 4 0.0104 99.7223 3 0.6638 0.0048 4 0.0088 108.2067 5 0.6607 0.0073 6 0.0076 60.1069 Parameter: clf__max_features Optimal value: 0.12075618253727419 (score: 0.6916) Performance by value: score_mean score_std count fold_std_mean time_mean param_clf__max_features 0.120756 0.6916 NaN 1 0.0110 28.9900 0.150770 0.6839 NaN 1 0.0119 28.1060 0.953997 0.6773 NaN 1 0.0070 614.5693 0.898491 0.6757 NaN 1 0.0069 175.4068 0.513324 0.6705 NaN 1 0.0071 95.5004 0.141805 0.6697 NaN 1 0.0092 33.4750 0.905345 0.6694 NaN 1 0.0081 196.8702 0.185869 0.6674 NaN 1 0.0079 36.5932 0.481061 0.6643 NaN 1 0.0028 40.3300 0.352841 0.6641 NaN 1 0.0077 133.2908 0.749557 0.6636 NaN 1 0.0093 166.1914 0.316923 0.6623 NaN 1 0.0069 119.1400 0.484787 0.6620 NaN 1 0.0052 37.7866 0.816889 0.6600 NaN 1 0.0078 117.2920 0.278958 0.6595 NaN 1 0.0110 46.2450 0.860080 0.6581 NaN 1 0.0081 132.6173 0.933671 0.6579 NaN 1 0.0089 99.8698 0.568061 0.6556 NaN 1 0.0112 52.5364 0.992990 0.6515 NaN 1 0.0156 118.1418 0.918388 0.6482 NaN 1 0.0115 23.4877 Parameter: clf__min_samples_leaf Optimal value: 3 (score: 0.6744) Performance by value: score_mean score_std count fold_std_mean time_mean param_clf__min_samples_leaf 3 0.6744 0.0153 3 0.0085 33.4172 5 0.6705 NaN 1 0.0071 95.5004 8 0.6682 0.0114 4 0.0097 97.1283 2 0.6677 0.0136 2 0.0076 373.5933 7 0.6644 0.0027 3 0.0081 107.3082 1 0.6638 0.0121 3 0.0084 111.2929 9 0.6610 0.0044 2 0.0083 116.5803 4 0.6519 0.0052 2 0.0113 38.0120 Parameter: clf__min_samples_split Optimal value: 10 (score: 0.6773) Performance by value: score_mean score_std count fold_std_mean time_mean param_clf__min_samples_split 10 0.6773 NaN 1 0.0070 614.5693 13 0.6707 0.0165 5 0.0097 66.9416 5 0.6705 NaN 1 0.0071 95.5004 4 0.6676 0.0115 2 0.0090 110.8259 6 0.6674 NaN 1 0.0079 36.5932 15 0.6665 0.0041 2 0.0087 181.5308 8 0.6624 0.0051 4 0.0078 72.1058 16 0.6611 0.0042 2 0.0079 132.9540 19 0.6519 0.0052 2 0.0113 38.0120 Parameter: clf__min_weight_fraction_leaf Optimal value: 0.28140549728612524 (score: 0.6916) Performance by value: score_mean score_std count fold_std_mean time_mean param_clf__min_weight_fraction_leaf 0.281405 0.6916 NaN 1 0.0110 28.9900 0.472349 0.6839 NaN 1 0.0119 28.1060 0.057185 0.6773 NaN 1 0.0070 614.5693 0.103817 0.6757 NaN 1 0.0069 175.4068 0.114290 0.6705 NaN 1 0.0071 95.5004 0.126736 0.6697 NaN 1 0.0092 33.4750 0.138192 0.6694 NaN 1 0.0081 196.8702 0.378323 0.6674 NaN 1 0.0079 36.5932 0.182070 0.6643 NaN 1 0.0028 40.3300 0.124370 0.6641 NaN 1 0.0077 133.2908 0.272208 0.6636 NaN 1 0.0093 166.1914 0.272830 0.6623 NaN 1 0.0069 119.1400 0.263917 0.6620 NaN 1 0.0052 37.7866 0.250625 0.6600 NaN 1 0.0078 117.2920 0.405579 0.6595 NaN 1 0.0110 46.2450 0.422932 0.6581 NaN 1 0.0081 132.6173 0.432517 0.6579 NaN 1 0.0089 99.8698 0.398810 0.6556 NaN 1 0.0112 52.5364 0.325244 0.6515 NaN 1 0.0156 118.1418 0.348135 0.6482 NaN 1 0.0115 23.4877 6. CROSS-VALIDATION CONSISTENCY: -------------------------------------------------- Fold performance consistency: Fold 0: 0.6758 ± 0.0113 Fold 1: 0.6734 ± 0.0104 Fold 2: 0.6607 ± 0.0091 Fold 3: 0.6612 ± 0.0127 Fold 4: 0.6570 ± 0.0149 7. MODEL SELECTION RECOMMENDATION: -------------------------------------------------- ✅ RECOMMENDATION: Choose stable model Score: 0.6916 (vs best: 0.6916) Stability: 0.0110 (vs best: 0.0110) Performance difference: 0.0000 (insignificant) 🎯 RECOMMENDED HYPERPARAMETERS: clf__max_depth: 6 clf__max_features: 0.12075618253727419 clf__min_samples_leaf: 3 clf__min_samples_split: 13 clf__min_weight_fraction_leaf: 0.28140549728612524 clf__n_estimators: 369 8. GENERATING VISUALIZATIONS... 9. PRACTICAL INTERPRETATION FOR TRADING: -------------------------------------------------- Expected Strategy Performance: • Best mean_test_score: 0.6916 • Cross-validation Consistency: Good ✅ LOW RISK: Excellent consistency across CV folds Strategy likely to perform similarly in live trading ================================================================================ ANALYSIS COMPLETE ================================================================================ SPECIFIC INSIGHTS FROM YOUR RESULTS: ================================================================================ 1. KEY OBSERVATIONS: -------------------------------------------------- max_depth: 6 min_samples_leaf: 3 min_samples_split: 13 n_estimators: 369 Best Model mean_test_score: 0.6916 Standard Deviation: 0.0110 Training Time: 28.99s Best Simple Model (param_clf__max_depth ≤ 4): param_clf__max_depth=4 mean_test_score: 0.6839 (vs best: 0.6916) 2. PERFORMANCE SATURATION: -------------------------------------------------- Maximum performance by max_depth: depth=3: 0.6697 depth=4: 0.6839 depth=5: 0.6705 depth=6: 0.6916 3. ACTIONABLE RECOMMENDATIONS: -------------------------------------------------- ✅ Excellent performance achieved! Consider testing with additional features or ensemble methods 4. PRODUCTION CONSIDERATIONS: -------------------------------------------------- Expected Inference Speed: ~199.1ms per prediction Training Time Range: 23.49s to 614.57s Average Model Size: ~303 trees ✅ Markdown report generated: Models\Bollinger_w10_std1_5\EURUSD\FUNDEDNEXT_STLR2_6K\time\M1\20220101_20231231\bdad004f\reports\hyperparameter_analysis_report.md 2025-12-16 11:18:24 | afml.production.model_development | INFO | Generated hyperparameter report: Models\Bollinger_w10_std1_5\EURUSD\FUNDEDNEXT_STLR2_6K\time\M1\20220101_20231231\bdad004f\reports\hyperparameter_analysis_report.md 2025-12-16 11:18:25 | afml.production.model_development | INFO | Generated feature importance plot: Models\Bollinger_w10_std1_5\EURUSD\FUNDEDNEXT_STLR2_6K\time\M1\20220101_20231231\bdad004f\plots\feature_importance.png 2025-12-16 11:18:25 | afml.production.model_development | WARNING | HTML summary generation failed: 'numpy.ndarray' object is not callable ✓ Reports generated in 4.15s [Saving] Writing artifacts to disk... 2025-12-16 11:18:29 | afml.production.model_development | INFO | Saved all artifacts to Models\Bollinger_w10_std1_5\EURUSD\FUNDEDNEXT_STLR2_6K\time\M1\20220101_20231231\bdad004f ✓ Saved to Models\Bollinger_w10_std1_5\EURUSD\FUNDEDNEXT_STLR2_6K\time\M1\20220101_20231231\bdad004f 2025-12-16 11:18:29 [info ] pipeline_step duration_seconds=260.72733187675476 metrics={'total_duration': 260.72733187675476, 'model_trained': True, 'reports_generated': True} status=completed step=pipeline_complete ✓ Pipeline completed in 00:04:21 ======================================================================

Stage 5: Model Export and Validation

The final stage exports the model to ONNX format with comprehensive validation:

[Saving] Writing artifacts to disk... ONNX EXPORT PIPELINE

======================================================================

ONNX EXPORT PIPELINE

======================================================================

[Step 1/5] Preparing metadata...

✓ Model type: RandomForestClassifier

✓ Features: 74

✓ Version: 1.0

[Step 2/5] Converting to ONNX format...

✓ Conversion successful

✓ ONNX opset: 12 (MQL5 compatible)

[Step 3/5] Saving ONNX model...

✓ Saved to: C:\Users\JoeN\Documents\GitHub\Machine-Learning-Blueprint\models\bollinger_meta_model_eurusd_tick_m1.onxx

✓ File size: 0.16 MB

[Step 4/5] Validating ONNX model...

✓ ONNX model structure valid

[Step 5/5] Comparing Python vs ONNX predictions...

Generating test data...

Computing Python predictions...

Computing ONNX predictions...

✓ ONNX returned 2 output(s)

Output 0: shape=(1000,), dtype=int64

Sample values: 1

Output 1: shape=(1000, 2), dtype=float32

Sample values: [0.48720157 0.5127984 ]

✓ Using output 1 (probabilities)

✓ Extracted positive class probabilities from shape (1000, 2)

Prediction Comparison (1000 samples):

• Max difference: 1.52e-07

• Mean difference: 4.91e-08

• Std difference: 3.30e-08

✅ VALIDATION PASSED - Predictions match within tolerance (1.00e-05)

Sample Predictions (first 5):

Index Python ONNX Diff

--------------------------------------------------

0 0.512798 0.512798 8.19e-08

1 0.459688 0.459688 5.50e-08

2 0.451748 0.451748 7.06e-08

3 0.478857 0.478857 6.04e-08

4 0.460223 0.460223 6.36e-08

======================================================================

✅ EXPORT SUCCESSFUL - Model ready for MQL5 deployment

======================================================================

This validation step is crucial. The system generates random test data and verifies that the ONNX model produces bit-for-bit identical predictions to the Python model. If there's any discrepancy, the export fails immediately rather than silently producing wrong predictions in production.

Understanding the Outputs

After the pipeline completes, you have a complete audit trail. Every file is timestamped, versioned, and linked. You can navigate your research history like a well-organized library.

| File Types (Color as Key) | Function |

|---|---|

| Configuration Files | Complete settings needed to reproduce this experiment. Config hash ensures uniqueness. |

| Model Files | Trained model in multiple formats: Python (joblib) for research, ONNX for MQL5 deployment. |

| Data Artifacts | Processed features, labels and weights. Allows model analysis without recomputing. |

| Reports & Logs | Comprehensive documentation: execution logs, performance charts, analysis reports. |

What This Organization Gives You

- Easy Navigation: Find any experiment by strategy, symbol, date range

- Perfect Reproducibility: Config hash guarantees uniqueness and traceability

- Compare Experiments: Side-by-side comparison of different configurations

- Quick Deployment: ONNX file ready to drop into MQL5 EA

- Complete Audit Trail: Everything documented automatically

To find trained models that fit a certain criteria, you can use the code below:

from ..production.utils import ModelFileManager file_manager = ModelFileManager() base_dir = "Models" # base_dir is path to where trained models are saved search_criteria = {"bar_size": "M1", "bar_type": "time"} file_manager.find_models(search_criteria, base_dir)

The Power of Caching

Let's talk about what makes this system fast. The core of this efficiency lies in its intelligent cache invalidation logic, which ensures that only the necessary components of the pipeline are recomputed when changes are made. By treating the machine learning workflow as a dependency graph, the system can distinguish between heavy modifications, like changing data symbols which require a full recompute of all stages, and lighter modifications, such as tuning model hyper-parameters. In the latter scenario, the system reuses cached data for the bars, features, labels, and weights, only performing the final model training step. This granular control prevents redundant calculations, allowing researchers to iterate on specific parts of the strategy—like feature engineering or labeling—without wasting time reprocessing the entire dataset.

For a deeper dive into my caching system, read the last article in my series.

After the first run, subsequent experiments are dramatically faster.

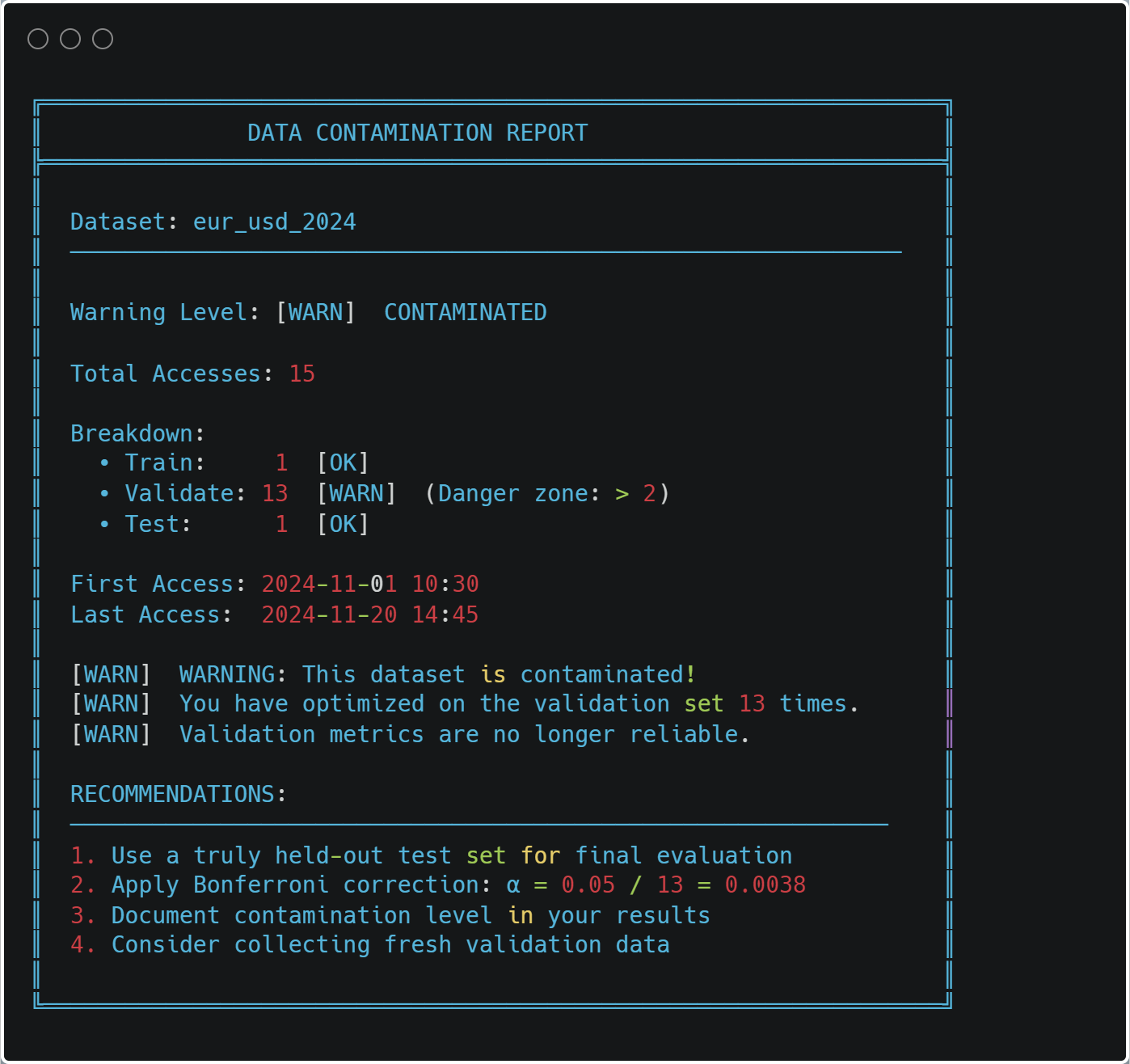

Cache Safety and Data Contamination

The most important feature of the caching system is contamination prevention. Every data access is logged:

@cacheable(time_aware=True) def load_and_prepare_training_data(...): # ... load data ... log_data_access( dataset_name=f"{symbol}_{bar_type}_{bar_size}".lower(), start_date=data.index[0], end_date=data.index[-1], purpose="train", data_shape=data.shape) return data

At any time, you can check for contamination:

from ..cache import print_contamination_report print_contamination_report()

Practical Usage Patterns

Let me show you some common research workflows:

1. Strategy Comparison

strategies = [ BollingerBandStrategy(window=20, num_std=2.0), BollingerBandStrategy(window=20, num_std=2.5), BollingerBandStrategy(window=30, num_std=2.0), ] results = [] for strategy in strategies: pipeline = ModelDevelopmentPipeline( symbol="EURUSD", train_start="2023-01-01", train_end="2023-12-31", strategy=strategy, # ... config ... ) model, features, metrics, config = pipeline.run(verbose=False) results.append({ "strategy": strategy.get_strategy_name(), "cv_score": metrics["cv_results"]["best_score"], "features": len(features), "model": model }) comparison = pd.DataFrame(results).sort_values("cv_score", ascending=False) print(comparison)

Because of caching, comparing strategies is fast—only the model training changes.

2. Feature Engineering Experiments

feature_configs = [

{"func": calculate_basic_features, "params": {}},

{"func": calculate_advanced_features, "params": {"lookback": 20}},

{"func": calculate_advanced_features, "params": {"lookback": 50}},

]

for i, feat_config in enumerate(feature_configs):

pipeline = ModelDevelopmentPipeline(

# ... same data config ... feature_config=feat_config,

# ... rest of config ...

)

model, features, metrics, _ = pipeline.run()

print(f"Feature set {i+1}: {metrics['cv_results']['best_score']:.4f}") 3. Walk-Forward Analysis

train_periods = [ ("2022-01-01", "2022-12-31"), ("2022-07-01", "2023-06-30"), ("2023-01-01", "2023-12-31"), ] models = [] for train_start, train_end in train_periods: pipeline = ModelDevelopmentPipeline( symbol="EURUSD", train_start=train_start, train_end=train_end, # ... config ... ) model, _, metrics, _ = pipeline.run() models.append({ "period": f"{train_start} to {train_end}", "score": metrics["cv_results"]["best_score"], "model_path": pipeline.file_paths["model"] })

The organized directory structure makes it easy to compare models across time periods.

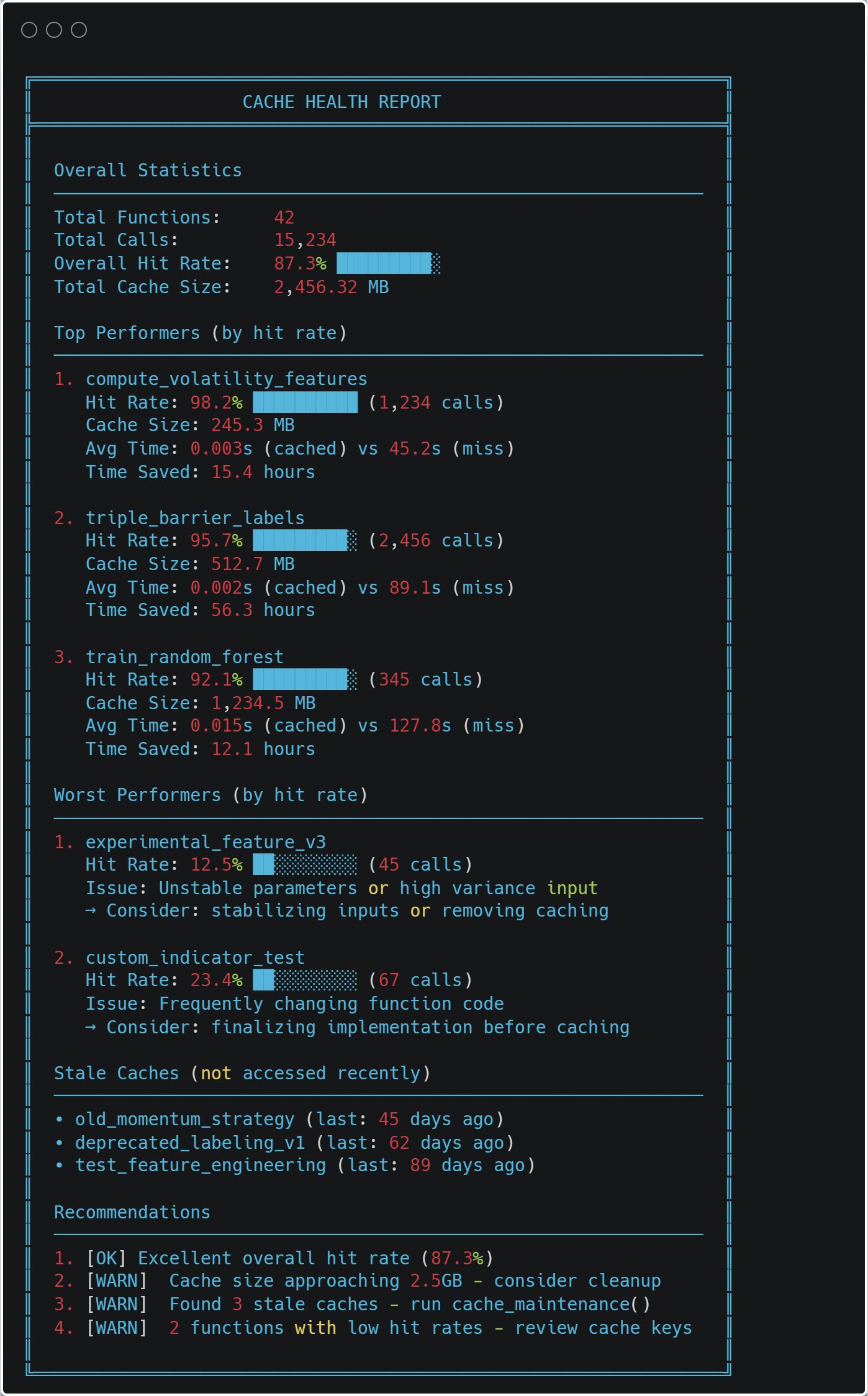

Performance Monitoring

The system tracks its own performance:

from ..cache import print_health_report print_health_report()

Integration with MQL5

The ONNX export makes deployment straightforward. Here's a minimal MQL5 EA skeleton:

//+------------------------------------------------------------------+ //| BollingerBandStrategy_EA.mq5 | //+------------------------------------------------------------------+ #property version "1.00" #property strict //--- Include Resources #include <Trade\Trade.mqh> //--- Load the ONNX model from resources #resource "\\Models\\BollingerBandStrategy\\EURUSD\\model.onnx" as uchar model_data[] //--- Input Parameters input double InpLotSize = 0.01; // Trade Lot Size input double InpThresholdBuy = 0.55; // Probability to Buy input double InpThresholdExit = 0.45; // Probability to Exit/Sell //--- Global Variables long model_handle = INVALID_HANDLE; CTrade trade; //+------------------------------------------------------------------+ //| Expert initialization function | //+------------------------------------------------------------------+ int OnInit() { // Load ONNX model from the resource buffer model_handle = OnnxCreateFromBuffer(model_data, ONNX_DEFAULT); if(model_handle == INVALID_HANDLE) { Print("Error: Failed to load ONNX model. Code: ", GetLastError()); return(INIT_FAILED); } // Set output shape if necessary (depends on your model export) // OnnxSetOutputShape(model_handle, 0, [1, 1]); Print("Model loaded successfully. Handle: ", model_handle); return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Expert deinitialization function | //+------------------------------------------------------------------+ void OnDeinit(const int reason) { if(model_handle != INVALID_HANDLE) { OnnxRelease(model_handle); model_handle = INVALID_HANDLE; } } //+------------------------------------------------------------------+ //| Expert tick function | //+------------------------------------------------------------------+ void OnTick() { // 1. Prepare Features double features[47]; if(!CalculateFeatures(features)) return; // 2. Prepare ONNX Vectors vector v_features; v_features.Assign(features); vector v_output; // 3. Run Inference if(!OnnxRun(model_handle, ONNX_NO_CONVERSION, v_features, v_output)) { Print("Inference failed. Error: ", GetLastError()); return; } // 4. Trade Logic double probability = v_output[0]; CheckTradeLogic(probability); } //+------------------------------------------------------------------+ //| Logic for Entry and Exit | //+------------------------------------------------------------------+ void CheckTradeLogic(double prob) { bool hasPosition = (PositionsTotal() > 0); // Buy Logic if(prob > InpThresholdBuy && !hasPosition) { trade.Buy(InpLotSize, _Symbol, SymbolInfoDouble(_Symbol, SYMBOL_ASK), 0, 0, "ONNX Signal"); } // Exit Logic else if(prob < InpThresholdExit && hasPosition) { trade.PositionClose(_Symbol); } } //+------------------------------------------------------------------+ //| Feature Calculation - MUST MATCH PYTHON PRE-PROCESSING | //+------------------------------------------------------------------+ bool CalculateFeatures(double &features[]) { ArrayInitialize(features, 0.0); // Example: Getting Bollinger Bands data for the current bar double bb_upper = iBands(_Symbol, PERIOD_CURRENT, 20, 2.0, 0, PRICE_CLOSE, MODE_UPPER, 0); double bb_lower = iBands(_Symbol, PERIOD_CURRENT, 20, 2.0, 0, PRICE_CLOSE, MODE_LOWER, 0); double close = iClose(_Symbol, PERIOD_CURRENT, 0); // Fill your 47 features here exactly as your model expects // features[0] = (close - bb_lower) / (bb_upper - bb_lower); // Normalized example // ... return true; }

The key is ensuring your MQL5 features exactly match your Python features. The training summary's feature list helps with this.

Debugging and Troubleshooting

When something goes wrong, the system provides detailed diagnostics:

Example: Model Performance Drops

# Get all experiments for a symbol file_manager = ModelFileManager("Models") models = file_manager.find_models({ "symbol": "EURUSD", "strategy": "BollingerBandStrategy" }) # Compare performance over time for model_info in models: metrics = json.load(open(model_info["file_path"].replace(".joblib", "_metrics.json"))) print(f"{model_info['date_range']}: {metrics['cv_results']['best_score']:.4f}")

You can quickly identify when performance changed and load the corresponding configuration to see what was different.

Example: Cache Issues

If you suspect cache corruption:

from cache import clear_cache # Clear specific function cache clear_cache("load_and_prepare_training_data") # Or clear everything clear_cache()

The system will rebuild from scratch, ensuring correctness.

Best Practices

After using this system for months, here are my recommendations:

1. Always Use Descriptive Strategy Names

# Good strategy name BollingerBandStrategy(window=20, num_std=2.0) strategy.get_strategy_name() # "BollingerBand_w20_std2.0" # Better - includes your hypothesis strategy BollingerBandStrategy(window=20, num_std=2.0, name="BB_MeanReversion_v1")

Your future self will thank you when browsing 50 experiments.

2. Start with Small Parameter Grids

# First iteration - quick feedback param_grid = { "n_estimators": [100, 200], "max_depth": [3, 5, 7] } # After you understand the landscape param_grid = { "n_estimators": [100, 200, 300, 500], "max_depth": [3, 5, 7, 10, 15], "min_samples_split": [2, 5, 10, 20] }

Iterate quickly first, then refine.

3. Save Everything

Storage is cheap, reproducibility is priceless:

pipeline.run( generate_reports=True, # Always save=True, # Always export_onnx=True, # If deploying verbose=True # Until you're confident )

4. Review Reports Before Deployment

Don't deploy based on CV score alone. Check:

- Fold consistency (high variance = unreliable)

- Feature importance (sensible features?)

- Label distribution (balanced?)

- ONNX validation (passed?)

The reports make this easy.

5. Version Your Feature Functions

def calculate_features_v1(data, **params): """Initial feature set - baseline.""" # ... features ... def calculate_features_v2(data, **params): """Added momentum indicators.""" # ... features ... feature_config = { "func": calculate_features_v2, # Track version in function name "params": {} }

When you improve features, create a new function. The cache will automatically handle versioning.

Conclusion

Building a production-grade research system requires upfront investment, but the payoff is enormous:

- Speed: 10x more experiments in the same time

- Reliability: Reproducible results you can trust

- Insight: Automatic analysis reveals patterns you'd miss

- Deployment: One-button export to MQL5

- Maintenance: Easy to debug, easy to extend

The code we've explored exhibits some of the most critical aspects of a financial ML research methodology. It enforces best practices: proper cross-validation, sample weighting, feature analysis (albeit very limited), and validation. It makes the right way the easy way.

Most importantly, it lets you focus on what matters: developing better trading strategies. The plumbing just works.

Next Steps

To implement this system:

- Start Small: Begin with a single strategy and symbol

- Verify Caching: Run the pipeline twice, confirm speedup

- Check Reports: Review all generated reports

- Validate ONNX: Ensure predictions match perfectly

- Deploy Carefully: Start with paper trading

- Iterate: Use the system to run systematic experiments

The full code is available in the accompanying files. Start with model_development.py in the folder "production", and work through the example notebook.

Remember: trading is hard enough without fighting your research tools. Build systems that help you win.

File Reference Guide

| File | Primary Purpose | Key Classes/Functions | Dependencies | When to Use |

|---|---|---|---|---|

| __init__.py | Module exports | complete_export_workflow() export_model_to_onnx() extract_onnx_metadata() validate_onnx_predictions() | model_export.py | Exposes the ONNX export functionality at the package level |

| dual_model_development.py | Bid/Ask-aware separate long/short models | BidAskLongShortPipeline train_bidask_longshort_models() | model_development.py, strategy classes | When you need separate models for long and short positions using realistic execution prices (long → ask, short → bid) |

| model_development.py | Core production pipeline | ModelDevelopmentPipeline TickDataLoader load_and_prepare_training_data() generate_events_triple_barrier() train_model_with_cv() | feature_engine, sklearn, numba, cache system | The main pipeline for training and evaluating any single model with full reproducibility |

| model_export.py | ONNX conversion and validation | export_model_to_onnx() validate_onnx_predictions() complete_export_workflow() | skl2onnx, onnxruntime | Final step before MQL5 deployment - ensures production model matches Python exactly |

| utils.py | File management and organization | ConfigPathGenerator ModelFileManager find_models() load_artifacts() | hashlib, json, pickle, pathlib | Managing the model directory structure, saving/loading artifacts, and finding past experiments |

File Relationships:

- __init__.py → model_export.py (exposes export functions)

- dual_model_development.py → model_development.py (extends the base pipeline)

- model_development.py → utils.py (uses file management)

- model_export.py → Standalone (can work independently)

- All files → Cache system (for performance)

Key Integration Points:

- dual_model_development.py creates two ModelDevelopmentPipeline instances (long/short)

- ModelFileManager in utils.py is used by ModelDevelopmentPipeline for organized storage

- export_model_to_onnx() is called from ModelDevelopmentPipeline when export_onnx=True

Warning: All rights to these materials are reserved by MetaQuotes Ltd. Copying or reprinting of these materials in whole or in part is prohibited.

This article was written by a user of the site and reflects their personal views. MetaQuotes Ltd is not responsible for the accuracy of the information presented, nor for any consequences resulting from the use of the solutions, strategies or recommendations described.

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use