Monitoreo de transacciones usando notificaciones push: ejemplo de un servicio en MetaTrader 5

Contenido

- Introducción

- Estructura del proyecto

- Clase de transacción

- Clase de posición histórica

- Clase para la búsqueda y el filtrado según las propiedades de las transacciones y posiciones

- Clase de colección de posiciones históricas

- Clase de cuenta

- Clase de colección de cuentas

- Programa de servicio para crear informes comerciales y enviar notificaciones

- Conclusión

Introducción

Al negociar en los mercados financieros, un componente importante es la disponibilidad de información sobre los resultados de las transacciones realizadas durante un determinado periodo de tiempo.

Probablemente, cada tráder al menos una vez se ha enfrentado a la necesidad de monitorear los resultados comerciales del último día, semana, mes, etc., con el fin de ajustar su estrategia según los resultados de la negociación. El terminal de cliente MetaTrader 5 ofrece buenas estadísticas en forma de informes, permitiéndole evaluar los resultados de sus transacciones en un formato visual cómodo. Los informes pueden ayudarle a optimizar su portafolio, comprender cómo reducir los riesgos y aumentar la estabilidad de su negociación.

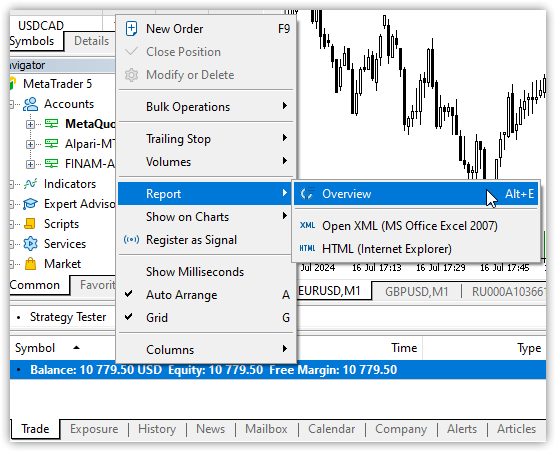

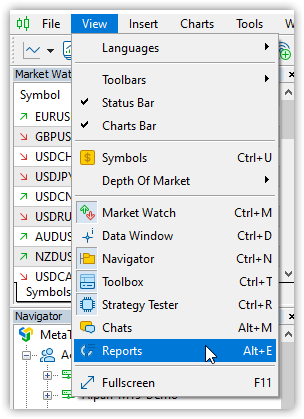

Para analizar su estrategia, deberá clicar en “Informe \ Revisar” en el menú contextual de la sección de historial comercial o en “Informes” en el menú “Ver” (o simplemente presionando Alt+E):

|  |

Podrá leer más información sobre los informes en el terminal MetaTrader 5, en el artículo "Nuevo informe en MetaTrader: los 5 indicadores comerciales más importantes" .

Si por alguna razón los informes estándar ofrecidos por el terminal de cliente no resultan suficientes, el lenguaje MQL5 ofrece amplias oportunidades para crear sus propios programas, incluso para generar informes y enviarlos al smartphone del tráder. Esta es la posibilidad que discutiremos hoy.

Nuestro programa deberá ponerse en marcha al iniciar el terminal, y monitorear el cambio de cuenta o cuenta comercial, el inicio del día y la hora de creación y el envío de informes. Para dichos fines nos conviene el tipo de programa “Servicio”.

Como se desprende de la ayuda, un Servicio es un programa que, a diferencia de los indicadores, asesores y scripts, no requiere una conexión a un gráfico para funcionar. Al igual que los scripts, los servicios no procesan ningún evento que no sea el evento de inicio. Para iniciar un servicio, su código deberá contener la función del manejador OnStart. Los servicios no aceptan ningún otro evento que no sea Start, pero pueden enviar eventos personalizados a los gráficos usando EventChartCustom. Los servicios se almacenan en el directorio <directorio_terminal>\MQL5\Services .

Cada servicio que se ejecuta en el terminal se ejecutará en su propio hilo. Esto significa que un servicio en bucle no puede influir en el funcionamiento de otros programas. Nuestro servicio deberá funcionar en un ciclo infinito, verificar el tiempo especificado, leer la historia comercial completa, crear listas de posiciones cerradas, filtrar estas listas según diferentes criterios y mostrar informes sobre ellas en el diario de registro y en Notificaciones push en el smartphone del usuario. Además, al iniciar el servicio por primera vez o modificar su configuración, el servicio deberá comprobar la posibilidad de enviar notificaciones Push desde el terminal. Y para ello deberemos organizar la correlación interactiva con el usuario mediante ventanas de mensajes con la expectativa de una respuesta y reacción por parte del usuario. Además, al enviar notificaciones Push, existen limitaciones en la frecuencia de las notificaciones por unidad de tiempo, por lo que será necesario organizar retrasos en el envío de notificaciones. Y todo esto no deberá influir de ninguna manera en el funcionamiento de otras aplicaciones que se ejecuten en el terminal del cliente. En base a lo dicho, los Servicios serán la herramienta más cómoda para crear un proyecto de este tipo.

Ya hemos decidido el tipo de programa. Ahora deberemos formarnos una idea sobre los componentes necesarios para ensamblar todo lo planeado.

Estructura del proyecto

Vamos a analizar el programa y sus componentes "de principio a fin":

- Programa de servicio. Tiene acceso a los datos de todas las cuentas que han estado activas durante todo el periodo de funcionamiento continuo del servicio. Partiendo de los datos de todas las cuentas, el programa obtiene las listas de las posiciones cerradas y las combina en una lista general. Dependiendo de la configuración, el servicio puede usar datos sobre posiciones cerradas solo de la cuenta activa actual, o de la cuenta actual y de cada una de las cuentas utilizadas anteriormente en el trading en el terminal del cliente.

A partir de los datos sobre las posiciones cerradas obtenidos de la lista de cuentas, se crean estadísticas comerciales para los periodos comerciales requeridos y se envían en notificaciones push al smartphone del usuario. Además, las estadísticas comerciales se muestran en forma de tabla en el diario del terminal "Expertos". - Colección de cuentas. Incluye una lista de cuentas a las que el terminal ha estado conectado durante el funcionamiento continuo del servicio. La colección de cuentas ofrece acceso a cualquier cuenta de la lista y a todas las posiciones cerradas de todas las cuentas. Las listas están disponibles en el programa de servicio y, usando estas como base, el servicio realiza selecciones y crea estadísticas.

- Clase de objeto de cuenta. Almacena datos de una cuenta con una lista (colección) de todas las posiciones cerradas, cuyas transacciones se han realizado en esta cuenta durante el funcionamiento continuo del servicio. Ofrece acceso a las propiedades de la cuenta, para crear y actualizar una lista de posiciones cerradas de esta cuenta y retorna las listas de las posiciones cerradas según varios criterios de selección.

- Colección de clase de posiciones históricas. Contiene una lista de objetos de posiciones, ofrece acceso a las propiedades de las posiciones cerradas, para crear y actualizar la lista de posiciones. Retorna una lista de posiciones cerradas.

- Clase de objeto de posición. Almacena y ofrecese acceso a las propiedades de una posición cerrada. El objeto contiene la funcionalidad necesaria para comparar dos objetos según diferentes propiedades, lo que permite crear listas de posiciones según diferentes criterios de selección. Contiene una lista de transacciones para esta posición y ofrece acceso a ellas.

- Clase de objeto de transacción. Almacena y ofrece acceso a las propiedades de una sola transacción. El objeto tiene la funcionalidad necesaria para comparar dos objetos según diferentes propiedades, lo que permite crear listas de transacciones según diferentes criterios de selección.

Ya discutimos el concepto de recreación de una posición cerrada a partir de una lista de transacciones históricas en el artículo "Cómo ver las transacciones directamente en el gráfico sin tener que perderse en el historial de transacciones". Usando como base la lista de transacciones, cada transacción se identifica como perteneciente a una posición particular utilizando el identificador de posición (PositionID) registrado en las propiedades de la transacción. Así, se crea un objeto de posición en el que las transacciones encontradas se colocan en la lista de transacciones. Aquí lo haremos de la misma manera. Pero para organizar la construcción de objetos de transacción y posición, usaremos un concepto completamente diferente y probado durante mucho tiempo, donde cada objeto tiene métodos idénticos de acceso a las propiedades para configurarlas y obtenerlas. Este concepto permite crear objetos en una única clave común, y almacenarlos en listas, así como filtrar y realizar la clasificación según cualquiera de las propiedades de los objetos y obtener nuevas listas en el contexto de la propiedad especificada.

Para comprender adecuadamente el concepto de construcción de clases en este proyecto, resulta muy recomendable la lectura de tres artículos que lo describen con gran detalle:

- La estructura de las propiedades de los objetos "(Parte I): Concepto, organización de datos y primeros resultados" ,

- La estructura de las listas de los objetos "(Parte II): Colección de órdenes y transacciones históricas" y

- Los métodos para filtrar los objetos en las listas según las propiedades "(Parte III): Colección de órdenes y posiciones de mercado, búsqueda y filtrado"

Tras leer los artículos enumerados, quedará claro el concepto completo de la construcción de objetos, su almacenamiento en listas y la obtención de varias listas filtradas según las propiedades requeridas. En esencia, los tres artículos describen la posibilidad de crear bases de datos para cualquier objeto en MQL5, almacenarlos en la base de datos y obtener las propiedades y valores requeridos. Esta es precisamente la funcionalidad que se necesita en este proyecto, y por ello hemos decidido construir los objetos y sus colecciones según el concepto descrito en los artículos, solo que aquí lo haremos de forma un poco más simple: sin crear clases de objetos abstractos con constructores protegidos y sin definir propiedades de objetos no compatibles en las clases. Todo será más sencillo: cada objeto tendrá su propia lista de propiedades almacenadas en tres arrays con la capacidad de escribir y recuperar estas propiedades. Y todos estos objetos se almacenarán en listas, donde será posible obtener nuevas listas solo de los objetos requeridos según las propiedades especificadas.

En resumen, cada objeto creado en el proyecto tendrá un conjunto de propiedades propias, como, de hecho, cualquier objeto o entidad en MQL5. Solo en MQL5 existen funciones estándar para obtener propiedades; los objetos de proyecto, entre tanto, tendrán métodos para obtener las propiedades enteras, reales y string escritas directamente en la clase de cada objeto. Luego todos estos objetos se almacenarán en listas : los arrays dinámicos de punteros a objetos CObject de la biblioteca estándar. Y son las clases de la Biblioteca Estándar las que nos permitirán crear proyectos complejos con el mínimo esfuerzo. En este caso, una base de datos de las posiciones cerradas de todas las cuentas donde se han realizado transacciones, con la posibilidad de obtener listas de objetos clasificados y seleccionados según cualquier propiedad requerida.

Cualquier posición existe solo desde el momento en que se abre (ejecución de una transacción In) hasta el momento en que se cierra (ejecución de una transacción Out/OutBuy). Es decir, es un objeto que existe únicamente como objeto de mercado. Cualquier transacción, por el contrario, es solo un objeto histórico, ya que una transacción supone simplemente el hecho de la ejecución de una orden (orden comercial). Por ello, en el terminal del cliente no hay posiciones en la lista histórica; solo existen en la lista de posiciones actuales del mercado.

Por consiguiente, para recrear una posición de mercado ya cerrada, es necesario “reunir” una posición previamente existente partiendo de transacciones históricas. Afortunadamente, para este propósito, cada transacción tiene un identificador de posición en cuya vida ha participado la transacción. Para hacer esto, se debe iterar la lista de transacciones históricas, obtener la siguiente transacción de la lista, crear un nuevo objeto de transacción, verificar el ID de la posición y crear un objeto de posición. El objeto de transacción creado se añade a la nueva posición histórica. Y seguiremos haciendo esto en lo sucesivo. Entretanto, crearemos las clases para el objeto de transacción y el objeto de posición, con los que continuaremos trabajando.

Clase de transacción

En el directorio del terminal \MQL5\Services\ crearemos una nueva carpeta AccountReporter\, y en ella un nuevo archivo Deal.mqh de la clase CDeal.

La clase debe heredarse de la clase básica CObject de la biblioteca estándar, y su archivo debe estar incluido en la clase recién creada :

//+------------------------------------------------------------------+ //| Deal.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include <Object.mqh> //+------------------------------------------------------------------+ //| Deal class | //+------------------------------------------------------------------+ class CDeal : public CObject { }

Ahora introduciremos las enumeraciones de propiedades enteras, reales y string de la transacción, y en las secciones privada, protegida y pública declararemos las variables de miembro de clase y los métodos para trabajar con las propiedades de la transacción:

//+------------------------------------------------------------------+ //| Deal.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include <Object.mqh> //--- Enumeration of integer deal properties enum ENUM_DEAL_PROPERTY_INT { DEAL_PROP_TICKET = 0, // Deal ticket DEAL_PROP_ORDER, // Deal order number DEAL_PROP_TIME, // Deal execution time DEAL_PROP_TIME_MSC, // Deal execution time in milliseconds DEAL_PROP_TYPE, // Deal type DEAL_PROP_ENTRY, // Deal direction DEAL_PROP_MAGIC, // Deal magic number DEAL_PROP_REASON, // Deal execution reason or source DEAL_PROP_POSITION_ID, // Position ID DEAL_PROP_SPREAD, // Spread when performing a deal }; //--- Enumeration of real deal properties enum ENUM_DEAL_PROPERTY_DBL { DEAL_PROP_VOLUME = DEAL_PROP_SPREAD+1,// Deal volume DEAL_PROP_PRICE, // Deal price DEAL_PROP_COMMISSION, // Commission DEAL_PROP_SWAP, // Accumulated swap when closing DEAL_PROP_PROFIT, // Deal financial result DEAL_PROP_FEE, // Deal fee DEAL_PROP_SL, // Stop Loss level DEAL_PROP_TP, // Take Profit level }; //--- Enumeration of string deal properties enum ENUM_DEAL_PROPERTY_STR { DEAL_PROP_SYMBOL = DEAL_PROP_TP+1, // Symbol the deal is executed for DEAL_PROP_COMMENT, // Deal comment DEAL_PROP_EXTERNAL_ID, // Deal ID in an external trading system }; //+------------------------------------------------------------------+ //| Deal class | //+------------------------------------------------------------------+ class CDeal : public CObject { private: MqlTick m_tick; // Deal tick structure long m_lprop[DEAL_PROP_SPREAD+1]; // Array for storing integer properties double m_dprop[DEAL_PROP_TP-DEAL_PROP_SPREAD]; // Array for storing real properties string m_sprop[DEAL_PROP_EXTERNAL_ID-DEAL_PROP_TP]; // Array for storing string properties //--- Return the index of the array the deal's (1) double and (2) string properties are located at int IndexProp(ENUM_DEAL_PROPERTY_DBL property) const { return(int)property-DEAL_PROP_SPREAD-1; } int IndexProp(ENUM_DEAL_PROPERTY_STR property) const { return(int)property-DEAL_PROP_TP-1; } //--- Get a (1) deal tick and (2) a spread of the deal minute bar bool GetDealTick(const int amount=20); int GetSpreadM1(void); //--- Return time with milliseconds string TimeMscToString(const long time_msc,int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const; protected: //--- Additional properties int m_digits; // Symbol Digits double m_point; // Symbol Point double m_bid; // Bid when performing a deal double m_ask; // Ask when performing a deal public: //--- Set the properties //--- Set deal's (1) integer, (2) real and (3) string properties void SetProperty(ENUM_DEAL_PROPERTY_INT property,long value){ this.m_lprop[property]=value; } void SetProperty(ENUM_DEAL_PROPERTY_DBL property,double value){ this.m_dprop[this.IndexProp(property)]=value; } void SetProperty(ENUM_DEAL_PROPERTY_STR property,string value){ this.m_sprop[this.IndexProp(property)]=value; } //--- Integer properties void SetTicket(const long ticket) { this.SetProperty(DEAL_PROP_TICKET, ticket); } // Ticket void SetOrder(const long order) { this.SetProperty(DEAL_PROP_ORDER, order); } // Order void SetTime(const datetime time) { this.SetProperty(DEAL_PROP_TIME, time); } // Time void SetTimeMsc(const long value) { this.SetProperty(DEAL_PROP_TIME_MSC, value); } // Time in milliseconds void SetTypeDeal(const ENUM_DEAL_TYPE type) { this.SetProperty(DEAL_PROP_TYPE, type); } // Type void SetEntry(const ENUM_DEAL_ENTRY entry) { this.SetProperty(DEAL_PROP_ENTRY, entry); } // Direction void SetMagic(const long magic) { this.SetProperty(DEAL_PROP_MAGIC, magic); } // Magic number void SetReason(const ENUM_DEAL_REASON reason) { this.SetProperty(DEAL_PROP_REASON, reason); } // Deal execution reason or source void SetPositionID(const long id) { this.SetProperty(DEAL_PROP_POSITION_ID, id); } // Position ID //--- Real properties void SetVolume(const double volume) { this.SetProperty(DEAL_PROP_VOLUME, volume); } // Volume void SetPrice(const double price) { this.SetProperty(DEAL_PROP_PRICE, price); } // Price void SetCommission(const double value) { this.SetProperty(DEAL_PROP_COMMISSION, value); } // Commission void SetSwap(const double value) { this.SetProperty(DEAL_PROP_SWAP, value); } // Accumulated swap when closing void SetProfit(const double value) { this.SetProperty(DEAL_PROP_PROFIT, value); } // Financial result void SetFee(const double value) { this.SetProperty(DEAL_PROP_FEE, value); } // Deal fee void SetSL(const double value) { this.SetProperty(DEAL_PROP_SL, value); } // Stop Loss level void SetTP(const double value) { this.SetProperty(DEAL_PROP_TP, value); } // Take Profit level //--- String properties void SetSymbol(const string symbol) { this.SetProperty(DEAL_PROP_SYMBOL,symbol); } // Symbol name void SetComment(const string comment) { this.SetProperty(DEAL_PROP_COMMENT,comment); } // Comment void SetExternalID(const string ext_id) { this.SetProperty(DEAL_PROP_EXTERNAL_ID,ext_id); } // Deal ID in an external trading system //--- Get the properties //--- Return deal’s (1) integer, (2) real and (3) string property from the properties array long GetProperty(ENUM_DEAL_PROPERTY_INT property) const { return this.m_lprop[property]; } double GetProperty(ENUM_DEAL_PROPERTY_DBL property) const { return this.m_dprop[this.IndexProp(property)]; } string GetProperty(ENUM_DEAL_PROPERTY_STR property) const { return this.m_sprop[this.IndexProp(property)]; } //--- Integer properties long Ticket(void) const { return this.GetProperty(DEAL_PROP_TICKET); } // Ticket long Order(void) const { return this.GetProperty(DEAL_PROP_ORDER); } // Order datetime Time(void) const { return (datetime)this.GetProperty(DEAL_PROP_TIME); } // Time long TimeMsc(void) const { return this.GetProperty(DEAL_PROP_TIME_MSC); } // Time in milliseconds ENUM_DEAL_TYPE TypeDeal(void) const { return (ENUM_DEAL_TYPE)this.GetProperty(DEAL_PROP_TYPE); } // Type ENUM_DEAL_ENTRY Entry(void) const { return (ENUM_DEAL_ENTRY)this.GetProperty(DEAL_PROP_ENTRY); } // Direction long Magic(void) const { return this.GetProperty(DEAL_PROP_MAGIC); } // Magic number ENUM_DEAL_REASON Reason(void) const { return (ENUM_DEAL_REASON)this.GetProperty(DEAL_PROP_REASON); } // Deal execution reason or source long PositionID(void) const { return this.GetProperty(DEAL_PROP_POSITION_ID); } // Position ID //--- Real properties double Volume(void) const { return this.GetProperty(DEAL_PROP_VOLUME); } // Volume double Price(void) const { return this.GetProperty(DEAL_PROP_PRICE); } // Price double Commission(void) const { return this.GetProperty(DEAL_PROP_COMMISSION); } // Commission double Swap(void) const { return this.GetProperty(DEAL_PROP_SWAP); } // Accumulated swap when closing double Profit(void) const { return this.GetProperty(DEAL_PROP_PROFIT); } // Financial result double Fee(void) const { return this.GetProperty(DEAL_PROP_FEE); } // Deal fee double SL(void) const { return this.GetProperty(DEAL_PROP_SL); } // Stop Loss level double TP(void) const { return this.GetProperty(DEAL_PROP_TP); } // Take Profit level //--- String properties string Symbol(void) const { return this.GetProperty(DEAL_PROP_SYMBOL); } // Symbol name string Comment(void) const { return this.GetProperty(DEAL_PROP_COMMENT); } // Comment string ExternalID(void) const { return this.GetProperty(DEAL_PROP_EXTERNAL_ID); } // Deal ID in an external trading system //--- Additional properties double Bid(void) const { return this.m_bid; } // Bid when performing a deal double Ask(void) const { return this.m_ask; } // Ask when performing a deal int Spread(void) const { return (int)this.GetProperty(DEAL_PROP_SPREAD); } // Spread when performing a deal //--- Return the description of a (1) deal type, (2) position change method and (3) deal reason string TypeDescription(void) const; string EntryDescription(void) const; string ReasonDescription(void) const; //--- Return deal description string Description(void); //--- Print deal properties in the journal void Print(void); //--- Compare two objects by the property specified in 'mode' virtual int Compare(const CObject *node, const int mode=0) const; //--- Constructors/destructor CDeal(void){} CDeal(const ulong ticket); ~CDeal(); };

Vamos a analizar la implementación de los métodos de clase.

En el constructor de la clase, debemos asumir que la transacción ya ha sido seleccionada y podemos obtener sus propiedades:

//+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CDeal::CDeal(const ulong ticket) { //--- Store the properties //--- Integer properties this.SetTicket((long)ticket); // Deal ticket this.SetOrder(::HistoryDealGetInteger(ticket, DEAL_ORDER)); // Order this.SetTime((datetime)::HistoryDealGetInteger(ticket, DEAL_TIME)); // Deal execution time this.SetTimeMsc(::HistoryDealGetInteger(ticket, DEAL_TIME_MSC)); // Deal execution time in milliseconds this.SetTypeDeal((ENUM_DEAL_TYPE)::HistoryDealGetInteger(ticket, DEAL_TYPE)); // Type this.SetEntry((ENUM_DEAL_ENTRY)::HistoryDealGetInteger(ticket, DEAL_ENTRY)); // Direction this.SetMagic(::HistoryDealGetInteger(ticket, DEAL_MAGIC)); // Magic number this.SetReason((ENUM_DEAL_REASON)::HistoryDealGetInteger(ticket, DEAL_REASON)); // Deal execution reason or source this.SetPositionID(::HistoryDealGetInteger(ticket, DEAL_POSITION_ID)); // Position ID //--- Real properties this.SetVolume(::HistoryDealGetDouble(ticket, DEAL_VOLUME)); // Volume this.SetPrice(::HistoryDealGetDouble(ticket, DEAL_PRICE)); // Price this.SetCommission(::HistoryDealGetDouble(ticket, DEAL_COMMISSION)); // Commission this.SetSwap(::HistoryDealGetDouble(ticket, DEAL_SWAP)); // Accumulated swap when closing this.SetProfit(::HistoryDealGetDouble(ticket, DEAL_PROFIT)); // Financial result this.SetFee(::HistoryDealGetDouble(ticket, DEAL_FEE)); // Deal fee this.SetSL(::HistoryDealGetDouble(ticket, DEAL_SL)); // Stop Loss level this.SetTP(::HistoryDealGetDouble(ticket, DEAL_TP)); // Take Profit level //--- String properties this.SetSymbol(::HistoryDealGetString(ticket, DEAL_SYMBOL)); // Symbol name this.SetComment(::HistoryDealGetString(ticket, DEAL_COMMENT)); // Comment this.SetExternalID(::HistoryDealGetString(ticket, DEAL_EXTERNAL_ID)); // Deal ID in an external trading system //--- Additional parameters this.m_digits = (int)::SymbolInfoInteger(this.Symbol(), SYMBOL_DIGITS); this.m_point = ::SymbolInfoDouble(this.Symbol(), SYMBOL_POINT); //--- Parameters for calculating spread this.m_bid = 0; this.m_ask = 0; this.SetProperty(DEAL_PROP_SPREAD, 0); //--- If the historical tick and the Point value of the symbol were obtained if(this.GetDealTick() && this.m_point!=0) { //--- set the Bid and Ask price values, calculate and save the spread value this.m_bid=this.m_tick.bid; this.m_ask=this.m_tick.ask; int spread=(int)::fabs((this.m_ask-this.m_bid)/this.m_point); this.SetProperty(DEAL_PROP_SPREAD, spread); } //--- If failed to obtain a historical tick, take the spread value of the minute bar the deal took place on else this.SetProperty(DEAL_PROP_SPREAD, this.GetSpreadM1()); }

Guardamos las propiedades de la transacción, Digits y Point del símbolo para el cual se ha realizado la transacción en los arrays de propiedades de clase para realizar los cálculos y mostrar la información sobre la transacción. A continuación obtenemos el tick histórico en el momento de la transacción. De esta manera ofreceremos acceso a los precios Bid y Ask en el momento de la transacción y, por lo tanto, la capacidad de calcular el spread.

Método que compara dos objetos según una propiedad específica:

//+------------------------------------------------------------------+ //| Compare two objects by the specified property | //+------------------------------------------------------------------+ int CDeal::Compare(const CObject *node,const int mode=0) const { const CDeal * obj = node; switch(mode) { case DEAL_PROP_TICKET : return(this.Ticket() > obj.Ticket() ? 1 : this.Ticket() < obj.Ticket() ? -1 : 0); case DEAL_PROP_ORDER : return(this.Order() > obj.Order() ? 1 : this.Order() < obj.Order() ? -1 : 0); case DEAL_PROP_TIME : return(this.Time() > obj.Time() ? 1 : this.Time() < obj.Time() ? -1 : 0); case DEAL_PROP_TIME_MSC : return(this.TimeMsc() > obj.TimeMsc() ? 1 : this.TimeMsc() < obj.TimeMsc() ? -1 : 0); case DEAL_PROP_TYPE : return(this.TypeDeal() > obj.TypeDeal() ? 1 : this.TypeDeal() < obj.TypeDeal() ? -1 : 0); case DEAL_PROP_ENTRY : return(this.Entry() > obj.Entry() ? 1 : this.Entry() < obj.Entry() ? -1 : 0); case DEAL_PROP_MAGIC : return(this.Magic() > obj.Magic() ? 1 : this.Magic() < obj.Magic() ? -1 : 0); case DEAL_PROP_REASON : return(this.Reason() > obj.Reason() ? 1 : this.Reason() < obj.Reason() ? -1 : 0); case DEAL_PROP_POSITION_ID : return(this.PositionID() > obj.PositionID() ? 1 : this.PositionID() < obj.PositionID() ? -1 : 0); case DEAL_PROP_SPREAD : return(this.Spread() > obj.Spread() ? 1 : this.Spread() < obj.Spread() ? -1 : 0); case DEAL_PROP_VOLUME : return(this.Volume() > obj.Volume() ? 1 : this.Volume() < obj.Volume() ? -1 : 0); case DEAL_PROP_PRICE : return(this.Price() > obj.Price() ? 1 : this.Price() < obj.Price() ? -1 : 0); case DEAL_PROP_COMMISSION : return(this.Commission() > obj.Commission() ? 1 : this.Commission() < obj.Commission() ? -1 : 0); case DEAL_PROP_SWAP : return(this.Swap() > obj.Swap() ? 1 : this.Swap() < obj.Swap() ? -1 : 0); case DEAL_PROP_PROFIT : return(this.Profit() > obj.Profit() ? 1 : this.Profit() < obj.Profit() ? -1 : 0); case DEAL_PROP_FEE : return(this.Fee() > obj.Fee() ? 1 : this.Fee() < obj.Fee() ? -1 : 0); case DEAL_PROP_SL : return(this.SL() > obj.SL() ? 1 : this.SL() < obj.SL() ? -1 : 0); case DEAL_PROP_TP : return(this.TP() > obj.TP() ? 1 : this.TP() < obj.TP() ? -1 : 0); case DEAL_PROP_SYMBOL : return(this.Symbol() > obj.Symbol() ? 1 : this.Symbol() < obj.Symbol() ? -1 : 0); case DEAL_PROP_COMMENT : return(this.Comment() > obj.Comment() ? 1 : this.Comment() < obj.Comment() ? -1 : 0); case DEAL_PROP_EXTERNAL_ID : return(this.ExternalID() > obj.ExternalID() ? 1 : this.ExternalID() < obj.ExternalID() ? -1 : 0); default : return(-1); } }

Este es un método virtual que redefine el método homónimo en la clase principal CObject. Dependiendo del modo de comparación (una de las propiedades del objeto de transacción), estas propiedades se compararán para el objeto actual y para el transmitido por puntero al método. El método retornará 1 si el valor de la propiedad del objeto actual es mayor que el valor de esta propiedad del objeto comparado. Si es menor, se retornará -1; si los valores son iguales, se retornará 0.

Método que retorna la descripción del tipo de transacción:

//+------------------------------------------------------------------+ //| Return the deal type description | //+------------------------------------------------------------------+ string CDeal::TypeDescription(void) const { switch(this.TypeDeal()) { case DEAL_TYPE_BUY : return "Buy"; case DEAL_TYPE_SELL : return "Sell"; case DEAL_TYPE_BALANCE : return "Balance"; case DEAL_TYPE_CREDIT : return "Credit"; case DEAL_TYPE_CHARGE : return "Additional charge"; case DEAL_TYPE_CORRECTION : return "Correction"; case DEAL_TYPE_BONUS : return "Bonus"; case DEAL_TYPE_COMMISSION : return "Additional commission"; case DEAL_TYPE_COMMISSION_DAILY : return "Daily commission"; case DEAL_TYPE_COMMISSION_MONTHLY : return "Monthly commission"; case DEAL_TYPE_COMMISSION_AGENT_DAILY : return "Daily agent commission"; case DEAL_TYPE_COMMISSION_AGENT_MONTHLY: return "Monthly agent commission"; case DEAL_TYPE_INTEREST : return "Interest rate"; case DEAL_TYPE_BUY_CANCELED : return "Canceled buy deal"; case DEAL_TYPE_SELL_CANCELED : return "Canceled sell deal"; case DEAL_DIVIDEND : return "Dividend operations"; case DEAL_DIVIDEND_FRANKED : return "Franked (non-taxable) dividend operations"; case DEAL_TAX : return "Tax charges"; default : return "Unknown: "+(string)this.TypeDeal(); } }

Dependiendo del tipo de transacción, se retornará su descripción de texto. Para nuestro proyecto, este método resulta redundante, ya que no utilizaremos todos los tipos de transacciones, sino solo aquellas relacionadas con la posición: compra o venta.

Método que retorna la descripción del método para cambiar la posición:

//+------------------------------------------------------------------+ //| Return position change method | //+------------------------------------------------------------------+ string CDeal::EntryDescription(void) const { switch(this.Entry()) { case DEAL_ENTRY_IN : return "Entry In"; case DEAL_ENTRY_OUT : return "Entry Out"; case DEAL_ENTRY_INOUT : return "Reverse"; case DEAL_ENTRY_OUT_BY : return "Close a position by an opposite one"; default : return "Unknown: "+(string)this.Entry(); } }

Método que retorna la descripción del motivo de la transacción:

//+------------------------------------------------------------------+ //| Return a deal reason description | //+------------------------------------------------------------------+ string CDeal::ReasonDescription(void) const { switch(this.Reason()) { case DEAL_REASON_CLIENT : return "Terminal"; case DEAL_REASON_MOBILE : return "Mobile"; case DEAL_REASON_WEB : return "Web"; case DEAL_REASON_EXPERT : return "EA"; case DEAL_REASON_SL : return "SL"; case DEAL_REASON_TP : return "TP"; case DEAL_REASON_SO : return "SO"; case DEAL_REASON_ROLLOVER : return "Rollover"; case DEAL_REASON_VMARGIN : return "Var. Margin"; case DEAL_REASON_SPLIT : return "Split"; case DEAL_REASON_CORPORATE_ACTION: return "Corp. Action"; default : return "Unknown reason "+(string)this.Reason(); } }

Método que retorna la descripción de una transacción:

//+------------------------------------------------------------------+ //| Return deal description | //+------------------------------------------------------------------+ string CDeal::Description(void) { return(::StringFormat("Deal: %-9s %.2f %-4s #%I64d at %s", this.EntryDescription(), this.Volume(), this.TypeDescription(), this.Ticket(), this.TimeMscToString(this.TimeMsc()))); }

Método que imprime las propiedades de la transacción en el registro:

//+------------------------------------------------------------------+ //| Print deal properties in the journal | //+------------------------------------------------------------------+ void CDeal::Print(void) { ::Print(this.Description()); }

Método que retorna el tiempo en milisegundos:

//+------------------------------------------------------------------+ //| Return time with milliseconds | //+------------------------------------------------------------------+ string CDeal::TimeMscToString(const long time_msc, int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const { return(::TimeToString(time_msc/1000, flags) + "." + ::IntegerToString(time_msc %1000, 3, '0')); }

Todos los métodos que retornan y registran descripciones de texto tienen como objetivo describir la transacción. En este proyecto en realidad no son necesarios, pero siempre debemos recordar las ampliaciones y mejoras, y por eso estos métodos estarán presentes aquí.

Método que obtiene el tick de la transacción:

//+------------------------------------------------------------------+ //| Get the deal tick | //| https://www.mql5.com/ru/forum/42122/page47#comment_37205238 | //+------------------------------------------------------------------+ bool CDeal::GetDealTick(const int amount=20) { MqlTick ticks[]; // We will receive ticks here int attempts = amount; // Number of attempts to get ticks int offset = 500; // Initial time offset for an attempt int copied = 0; // Number of ticks copied //--- Until the tick is copied and the number of copy attempts is over //--- we try to get a tick, doubling the initial time offset at each iteration (expand the "from_msc" time range) while(!::IsStopped() && (copied<=0) && (attempts--)!=0) copied = ::CopyTicksRange(this.Symbol(), ticks, COPY_TICKS_INFO, this.TimeMsc()-(offset <<=1), this.TimeMsc()); //--- If the tick was successfully copied (it is the last one in the tick array), set it to the m_tick variable if(copied>0) this.m_tick=ticks[copied-1]; //--- Return the flag that the tick was copied return(copied>0); }

La lógica del método se explica con detalle en los comentarios al código. Tras recibir un tick, se toman los precios Bid y Ask y el tamaño del spread se calcula como (Ask - Bid) / Point.

Si como resultado no ha sido posible obtener un tick utilizando este método, entonces obtendremos el valor promedio del spread usando el método para obtener el spread de la barra de minutos de la transacción:

//+------------------------------------------------------------------+ //| Gets the spread of the deal minute bar | //+------------------------------------------------------------------+ int CDeal::GetSpreadM1(void) { int array[1]={}; int bar=::iBarShift(this.Symbol(), PERIOD_M1, this.Time()); if(bar==WRONG_VALUE) return 0; return(::CopySpread(this.Symbol(), PERIOD_M1, bar, 1, array)==1 ? array[0] : 0); }

La clase de transacción está lista. Los objetos de esta clase se almacenarán en la lista de transacciones en la clase de posición histórica, desde donde podremos obtener los punteros a las transacciones requeridas y procesar sus datos.

Clase de posición histórica

En la carpeta del terminal \MQL5\Services\AccountReporter\ crearemos un nuevo archivo Position.mqh de la clase CPosition.

La clase deberá heredar de la clase de objeto básico de la biblioteca estándar CObject:

//+------------------------------------------------------------------+ //| Position.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" //+------------------------------------------------------------------+ //| Position class | //+------------------------------------------------------------------+ class CPosition : public CObject { }

Como la clase de posición contendrá una lista de transacciones para esta posición, deberemos conectar el archivo de clase de transacción y el archivo de clase del array dinámico de punteros a objetos CObject al archivo creado:

//+------------------------------------------------------------------+ //| Position.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include "Deal.mqh" #include <Arrays\ArrayObj.mqh> //+------------------------------------------------------------------+ //| Position class | //+------------------------------------------------------------------+ class CPosition : public CObject { }

Ahora introduciremos las enumeraciones de propiedades enteras, reales y string de la transacción, y en las secciones privada, protegida y pública declararemos las variables de miembro de clase y los métodos para trabajar con las propiedades de la posición:

//+------------------------------------------------------------------+ //| Position.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include "Deal.mqh" #include <Arrays\ArrayObj.mqh> //--- Enumeration of integer position properties enum ENUM_POSITION_PROPERTY_INT { POSITION_PROP_TICKET = 0, // Position ticket POSITION_PROP_TIME, // Position open time POSITION_PROP_TIME_MSC, // Position open time in milliseconds POSITION_PROP_TIME_UPDATE, // Position change time POSITION_PROP_TIME_UPDATE_MSC, // Position change time in milliseconds POSITION_PROP_TYPE, // Position type POSITION_PROP_MAGIC, // Position magic number POSITION_PROP_IDENTIFIER, // Position ID POSITION_PROP_REASON, // Position open reason POSITION_PROP_ACCOUNT_LOGIN, // Account number POSITION_PROP_TIME_CLOSE, // Position close time POSITION_PROP_TIME_CLOSE_MSC, // Position close time in milliseconds }; //--- Enumeration of real position properties enum ENUM_POSITION_PROPERTY_DBL { POSITION_PROP_VOLUME = POSITION_PROP_TIME_CLOSE_MSC+1,// Position volume POSITION_PROP_PRICE_OPEN, // Position price POSITION_PROP_SL, // Stop Loss for open position POSITION_PROP_TP, // Take Profit for open position POSITION_PROP_PRICE_CURRENT, // Symbol current price POSITION_PROP_SWAP, // Accumulated swap POSITION_PROP_PROFIT, // Current profit POSITION_PROP_CONTRACT_SIZE, // Symbol trade contract size POSITION_PROP_PRICE_CLOSE, // Position close price POSITION_PROP_COMMISSIONS, // Accumulated commission POSITION_PROP_FEE, // Accumulated payment for deals }; //--- Enumeration of string position properties enum ENUM_POSITION_PROPERTY_STR { POSITION_PROP_SYMBOL = POSITION_PROP_FEE+1,// A symbol the position is open for POSITION_PROP_COMMENT, // Comment to a position POSITION_PROP_EXTERNAL_ID, // Position ID in the external system POSITION_PROP_CURRENCY_PROFIT, // Position symbol profit currency POSITION_PROP_ACCOUNT_CURRENCY, // Account deposit currency POSITION_PROP_ACCOUNT_SERVER, // Server name }; //+------------------------------------------------------------------+ //| Position class | //+------------------------------------------------------------------+ class CPosition : public CObject { private: long m_lprop[POSITION_PROP_TIME_CLOSE_MSC+1]; // Array for storing integer properties double m_dprop[POSITION_PROP_FEE-POSITION_PROP_TIME_CLOSE_MSC]; // Array for storing real properties string m_sprop[POSITION_PROP_ACCOUNT_SERVER-POSITION_PROP_FEE]; // Array for storing string properties //--- Return the index of the array the order's (1) double and (2) string properties are located at int IndexProp(ENUM_POSITION_PROPERTY_DBL property) const { return(int)property-POSITION_PROP_TIME_CLOSE_MSC-1;} int IndexProp(ENUM_POSITION_PROPERTY_STR property) const { return(int)property-POSITION_PROP_FEE-1; } protected: CArrayObj m_list_deals; // List of position deals CDeal m_temp_deal; // Temporary deal object for searching by property in the list //--- Return time with milliseconds string TimeMscToString(const long time_msc,int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const; //--- Additional properties int m_profit_pt; // Profit in points int m_digits; // Symbol digits double m_point; // One symbol point value double m_tick_value; // Calculated tick value //--- Return the pointer to (1) open and (2) close deal CDeal *GetDealIn(void) const; CDeal *GetDealOut(void) const; public: //--- Return the list of deals CArrayObj *GetListDeals(void) { return(&this.m_list_deals); } //--- Set the properties //--- Set (1) integer, (2) real and (3) string properties void SetProperty(ENUM_POSITION_PROPERTY_INT property,long value) { this.m_lprop[property]=value; } void SetProperty(ENUM_POSITION_PROPERTY_DBL property,double value) { this.m_dprop[this.IndexProp(property)]=value; } void SetProperty(ENUM_POSITION_PROPERTY_STR property,string value) { this.m_sprop[this.IndexProp(property)]=value; } //--- Integer properties void SetTicket(const long ticket) { this.SetProperty(POSITION_PROP_TICKET, ticket); } // Position ticket void SetTime(const datetime time) { this.SetProperty(POSITION_PROP_TIME, time); } // Position open time void SetTimeMsc(const long value) { this.SetProperty(POSITION_PROP_TIME_MSC, value); } // Position open time in milliseconds since 01.01.1970 void SetTimeUpdate(const datetime time) { this.SetProperty(POSITION_PROP_TIME_UPDATE, time); } // Position update time void SetTimeUpdateMsc(const long value) { this.SetProperty(POSITION_PROP_TIME_UPDATE_MSC, value); } // Position update time in milliseconds since 01.01.1970 void SetTypePosition(const ENUM_POSITION_TYPE type) { this.SetProperty(POSITION_PROP_TYPE, type); } // Position type void SetMagic(const long magic) { this.SetProperty(POSITION_PROP_MAGIC, magic); } // Magic number for a position (see ORDER_MAGIC) void SetID(const long id) { this.SetProperty(POSITION_PROP_IDENTIFIER, id); } // Position ID void SetReason(const ENUM_POSITION_REASON reason) { this.SetProperty(POSITION_PROP_REASON, reason); } // Position open reason void SetTimeClose(const datetime time) { this.SetProperty(POSITION_PROP_TIME_CLOSE, time); } // Close time void SetTimeCloseMsc(const long value) { this.SetProperty(POSITION_PROP_TIME_CLOSE_MSC, value); } // Close time in milliseconds void SetAccountLogin(const long login) { this.SetProperty(POSITION_PROP_ACCOUNT_LOGIN, login); } // Acount number //--- Real properties void SetVolume(const double volume) { this.SetProperty(POSITION_PROP_VOLUME, volume); } // Position volume void SetPriceOpen(const double price) { this.SetProperty(POSITION_PROP_PRICE_OPEN, price); } // Position price void SetSL(const double value) { this.SetProperty(POSITION_PROP_SL, value); } // Stop Loss level for an open position void SetTP(const double value) { this.SetProperty(POSITION_PROP_TP, value); } // Take Profit level for an open position void SetPriceCurrent(const double price) { this.SetProperty(POSITION_PROP_PRICE_CURRENT, price); } // Current price by symbol void SetSwap(const double value) { this.SetProperty(POSITION_PROP_SWAP, value); } // Accumulated swap void SetProfit(const double value) { this.SetProperty(POSITION_PROP_PROFIT, value); } // Current profit void SetPriceClose(const double price) { this.SetProperty(POSITION_PROP_PRICE_CLOSE, price); } // Close price void SetContractSize(const double value) { this.SetProperty(POSITION_PROP_CONTRACT_SIZE, value); } // Symbol trading contract size void SetCommissions(void); // Total commission of all deals void SetFee(void); // Total deal fee //--- String properties void SetSymbol(const string symbol) { this.SetProperty(POSITION_PROP_SYMBOL, symbol); } // Symbol a position is opened for void SetComment(const string comment) { this.SetProperty(POSITION_PROP_COMMENT, comment); } // Position comment void SetExternalID(const string ext_id) { this.SetProperty(POSITION_PROP_EXTERNAL_ID, ext_id); } // Position ID in an external system (on the exchange) void SetAccountServer(const string server) { this.SetProperty(POSITION_PROP_ACCOUNT_SERVER, server); } // Server name void SetAccountCurrency(const string currency) { this.SetProperty(POSITION_PROP_ACCOUNT_CURRENCY, currency); } // Account deposit currency void SetCurrencyProfit(const string currency) { this.SetProperty(POSITION_PROP_CURRENCY_PROFIT, currency); } // Profit currency of the position symbol //--- Get the properties //--- Return (1) integer, (2) real and (3) string property from the properties array long GetProperty(ENUM_POSITION_PROPERTY_INT property) const { return this.m_lprop[property]; } double GetProperty(ENUM_POSITION_PROPERTY_DBL property) const { return this.m_dprop[this.IndexProp(property)]; } string GetProperty(ENUM_POSITION_PROPERTY_STR property) const { return this.m_sprop[this.IndexProp(property)]; } //--- Integer properties long Ticket(void) const { return this.GetProperty(POSITION_PROP_TICKET); } // Position ticket datetime Time(void) const { return (datetime)this.GetProperty(POSITION_PROP_TIME); } // Position open time long TimeMsc(void) const { return this.GetProperty(POSITION_PROP_TIME_MSC); } // Position open time in milliseconds since 01.01.1970 datetime TimeUpdate(void) const { return (datetime)this.GetProperty(POSITION_PROP_TIME_UPDATE);} // Position change time long TimeUpdateMsc(void) const { return this.GetProperty(POSITION_PROP_TIME_UPDATE_MSC); } // Position update time in milliseconds since 01.01.1970 ENUM_POSITION_TYPE TypePosition(void) const { return (ENUM_POSITION_TYPE)this.GetProperty(POSITION_PROP_TYPE);}// Position type long Magic(void) const { return this.GetProperty(POSITION_PROP_MAGIC); } // Magic number for a position (see ORDER_MAGIC) long ID(void) const { return this.GetProperty(POSITION_PROP_IDENTIFIER); } // Position ID ENUM_POSITION_REASON Reason(void) const { return (ENUM_POSITION_REASON)this.GetProperty(POSITION_PROP_REASON);}// Position opening reason datetime TimeClose(void) const { return (datetime)this.GetProperty(POSITION_PROP_TIME_CLOSE); } // Close time long TimeCloseMsc(void) const { return this.GetProperty(POSITION_PROP_TIME_CLOSE_MSC); } // Close time in milliseconds long AccountLogin(void) const { return this.GetProperty(POSITION_PROP_ACCOUNT_LOGIN); } // Login //--- Real properties double Volume(void) const { return this.GetProperty(POSITION_PROP_VOLUME); } // Position volume double PriceOpen(void) const { return this.GetProperty(POSITION_PROP_PRICE_OPEN); } // Position price double SL(void) const { return this.GetProperty(POSITION_PROP_SL); } // Stop Loss level for an open position double TP(void) const { return this.GetProperty(POSITION_PROP_TP); } // Take Profit level for an open position double PriceCurrent(void) const { return this.GetProperty(POSITION_PROP_PRICE_CURRENT); } // Current price by symbol double Swap(void) const { return this.GetProperty(POSITION_PROP_SWAP); } // Accumulated swap double Profit(void) const { return this.GetProperty(POSITION_PROP_PROFIT); } // Current profit double ContractSize(void) const { return this.GetProperty(POSITION_PROP_CONTRACT_SIZE); } // Symbol trading contract size double PriceClose(void) const { return this.GetProperty(POSITION_PROP_PRICE_CLOSE); } // Close price double Commissions(void) const { return this.GetProperty(POSITION_PROP_COMMISSIONS); } // Total commission of all deals double Fee(void) const { return this.GetProperty(POSITION_PROP_FEE); } // Total deal fee //--- String properties string Symbol(void) const { return this.GetProperty(POSITION_PROP_SYMBOL); } // A symbol position is opened on string Comment(void) const { return this.GetProperty(POSITION_PROP_COMMENT); } // Position comment string ExternalID(void) const { return this.GetProperty(POSITION_PROP_EXTERNAL_ID); } // Position ID in an external system (on the exchange) string AccountServer(void) const { return this.GetProperty(POSITION_PROP_ACCOUNT_SERVER); } // Server name string AccountCurrency(void) const { return this.GetProperty(POSITION_PROP_ACCOUNT_CURRENCY); } // Account deposit currency string CurrencyProfit(void) const { return this.GetProperty(POSITION_PROP_CURRENCY_PROFIT); } // Profit currency of the position symbol //--- Additional properties ulong DealIn(void) const; // Open deal ticket ulong DealOut(void) const; // Close deal ticket int ProfitInPoints(void) const; // Profit in points int SpreadIn(void) const; // Spread when opening int SpreadOut(void) const; // Spread when closing double SpreadOutCost(void) const; // Spread cost when closing double PriceOutAsk(void) const; // Ask price when closing double PriceOutBid(void) const; // Bid price when closing //--- Add a deal to the list of deals, return the pointer CDeal *DealAdd(const long ticket); //--- Return a position type description string TypeDescription(void) const; //--- Return position open time and price description string TimePriceCloseDescription(void); //--- Return position close time and price description string TimePriceOpenDescription(void); //--- Return position description string Description(void); //--- Print the properties of the position and its deals in the journal void Print(void); //--- Compare two objects by the property specified in 'mode' virtual int Compare(const CObject *node, const int mode=0) const; //--- Constructor/destructor CPosition(const long position_id, const string symbol); CPosition(void){} ~CPosition(); };

Vamos a analizar la implementación de los métodos de clase.

En el constructor de la clase, establecemos el identificador de posición y el símbolo a partir de los parámetros transmitidos al método, y escribimos los datos de la cuenta y el símbolo:

//+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CPosition::CPosition(const long position_id, const string symbol) { this.m_list_deals.Sort(DEAL_PROP_TIME_MSC); this.SetID(position_id); this.SetSymbol(symbol); this.SetAccountLogin(::AccountInfoInteger(ACCOUNT_LOGIN)); this.SetAccountServer(::AccountInfoString(ACCOUNT_SERVER)); this.SetAccountCurrency(::AccountInfoString(ACCOUNT_CURRENCY)); this.SetCurrencyProfit(::SymbolInfoString(this.Symbol(),SYMBOL_CURRENCY_PROFIT)); this.SetContractSize(::SymbolInfoDouble(this.Symbol(),SYMBOL_TRADE_CONTRACT_SIZE)); this.m_digits = (int)::SymbolInfoInteger(this.Symbol(),SYMBOL_DIGITS); this.m_point = ::SymbolInfoDouble(this.Symbol(),SYMBOL_POINT); this.m_tick_value = ::SymbolInfoDouble(this.Symbol(), SYMBOL_TRADE_TICK_VALUE); }

En el destructor de clase, limpiamos la lista de transacciones de la posición:

//+------------------------------------------------------------------+ //| Destructor | //+------------------------------------------------------------------+ CPosition::~CPosition() { this.m_list_deals.Clear(); }

Método que compara dos objetos según una propiedad específica:

//+------------------------------------------------------------------+ //| Compare two objects by the specified property | //+------------------------------------------------------------------+ int CPosition::Compare(const CObject *node,const int mode=0) const { const CPosition *obj=node; switch(mode) { case POSITION_PROP_TICKET : return(this.Ticket() > obj.Ticket() ? 1 : this.Ticket() < obj.Ticket() ? -1 : 0); case POSITION_PROP_TIME : return(this.Time() > obj.Time() ? 1 : this.Time() < obj.Time() ? -1 : 0); case POSITION_PROP_TIME_MSC : return(this.TimeMsc() > obj.TimeMsc() ? 1 : this.TimeMsc() < obj.TimeMsc() ? -1 : 0); case POSITION_PROP_TIME_UPDATE : return(this.TimeUpdate() > obj.TimeUpdate() ? 1 : this.TimeUpdate() < obj.TimeUpdate() ? -1 : 0); case POSITION_PROP_TIME_UPDATE_MSC : return(this.TimeUpdateMsc() > obj.TimeUpdateMsc() ? 1 : this.TimeUpdateMsc() < obj.TimeUpdateMsc() ? -1 : 0); case POSITION_PROP_TYPE : return(this.TypePosition() > obj.TypePosition() ? 1 : this.TypePosition() < obj.TypePosition() ? -1 : 0); case POSITION_PROP_MAGIC : return(this.Magic() > obj.Magic() ? 1 : this.Magic() < obj.Magic() ? -1 : 0); case POSITION_PROP_IDENTIFIER : return(this.ID() > obj.ID() ? 1 : this.ID() < obj.ID() ? -1 : 0); case POSITION_PROP_REASON : return(this.Reason() > obj.Reason() ? 1 : this.Reason() < obj.Reason() ? -1 : 0); case POSITION_PROP_ACCOUNT_LOGIN : return(this.AccountLogin() > obj.AccountLogin() ? 1 : this.AccountLogin() < obj.AccountLogin() ? -1 : 0); case POSITION_PROP_TIME_CLOSE : return(this.TimeClose() > obj.TimeClose() ? 1 : this.TimeClose() < obj.TimeClose() ? -1 : 0); case POSITION_PROP_TIME_CLOSE_MSC : return(this.TimeCloseMsc() > obj.TimeCloseMsc() ? 1 : this.TimeCloseMsc() < obj.TimeCloseMsc() ? -1 : 0); case POSITION_PROP_VOLUME : return(this.Volume() > obj.Volume() ? 1 : this.Volume() < obj.Volume() ? -1 : 0); case POSITION_PROP_PRICE_OPEN : return(this.PriceOpen() > obj.PriceOpen() ? 1 : this.PriceOpen() < obj.PriceOpen() ? -1 : 0); case POSITION_PROP_SL : return(this.SL() > obj.SL() ? 1 : this.SL() < obj.SL() ? -1 : 0); case POSITION_PROP_TP : return(this.TP() > obj.TP() ? 1 : this.TP() < obj.TP() ? -1 : 0); case POSITION_PROP_PRICE_CURRENT : return(this.PriceCurrent() > obj.PriceCurrent() ? 1 : this.PriceCurrent() < obj.PriceCurrent() ? -1 : 0); case POSITION_PROP_SWAP : return(this.Swap() > obj.Swap() ? 1 : this.Swap() < obj.Swap() ? -1 : 0); case POSITION_PROP_PROFIT : return(this.Profit() > obj.Profit() ? 1 : this.Profit() < obj.Profit() ? -1 : 0); case POSITION_PROP_CONTRACT_SIZE : return(this.ContractSize() > obj.ContractSize() ? 1 : this.ContractSize() < obj.ContractSize() ? -1 : 0); case POSITION_PROP_PRICE_CLOSE : return(this.PriceClose() > obj.PriceClose() ? 1 : this.PriceClose() < obj.PriceClose() ? -1 : 0); case POSITION_PROP_COMMISSIONS : return(this.Commissions() > obj.Commissions() ? 1 : this.Commissions() < obj.Commissions() ? -1 : 0); case POSITION_PROP_FEE : return(this.Fee() > obj.Fee() ? 1 : this.Fee() < obj.Fee() ? -1 : 0); case POSITION_PROP_SYMBOL : return(this.Symbol() > obj.Symbol() ? 1 : this.Symbol() < obj.Symbol() ? -1 : 0); case POSITION_PROP_COMMENT : return(this.Comment() > obj.Comment() ? 1 : this.Comment() < obj.Comment() ? -1 : 0); case POSITION_PROP_EXTERNAL_ID : return(this.ExternalID() > obj.ExternalID() ? 1 : this.ExternalID() < obj.ExternalID() ? -1 : 0); case POSITION_PROP_CURRENCY_PROFIT : return(this.CurrencyProfit() > obj.CurrencyProfit() ? 1 : this.CurrencyProfit() < obj.CurrencyProfit() ? -1 : 0); case POSITION_PROP_ACCOUNT_CURRENCY : return(this.AccountCurrency() > obj.AccountCurrency() ? 1 : this.AccountCurrency() < obj.AccountCurrency() ? -1 : 0); case POSITION_PROP_ACCOUNT_SERVER : return(this.AccountServer() > obj.AccountServer() ? 1 : this.AccountServer() < obj.AccountServer() ? -1 : 0); default : return -1; } }

Este es un método virtual que redefine el método homónimo en la clase principal CObject. Dependiendo del modo de comparación (una de las propiedades del objeto de posición), estas propiedades se comparan para el objeto actual y para el transmitido por puntero al método. El método retornará 1 si el valor de la propiedad del objeto actual es mayor que el valor de esta propiedad del objeto comparado. Si es menor, se retornará -1; si los valores son iguales, se retornará 0.

Método que retorna el tiempo en milisegundos:

//+------------------------------------------------------------------+ //| Return time with milliseconds | //+------------------------------------------------------------------+ string CPosition::TimeMscToString(const long time_msc, int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const { return(::TimeToString(time_msc/1000, flags) + "." + ::IntegerToString(time_msc %1000, 3, '0')); }

Método que retorna el puntero a una transacción de apertura:

//+------------------------------------------------------------------+ //| Return the pointer to the opening deal | //+------------------------------------------------------------------+ CDeal *CPosition::GetDealIn(void) const { int total=this.m_list_deals.Total(); for(int i=0; i<total; i++) { CDeal *deal=this.m_list_deals.At(i); if(deal==NULL) continue; if(deal.Entry()==DEAL_ENTRY_IN) return deal; } return NULL; }

En el ciclo que itera la lista de transacciones de la posición, buscamos una transacción con el método de cambio de posición DEAL_ENTRY_IN (entrada al mercado) y retornamos el puntero a la transacción encontrada.

Método que retorna el puntero a la transacción de cierre:

//+------------------------------------------------------------------+ //| Return the pointer to the close deal | //+------------------------------------------------------------------+ CDeal *CPosition::GetDealOut(void) const { for(int i=this.m_list_deals.Total()-1; i>=0; i--) { CDeal *deal=this.m_list_deals.At(i); if(deal==NULL) continue; if(deal.Entry()==DEAL_ENTRY_OUT || deal.Entry()==DEAL_ENTRY_OUT_BY) return deal; } return NULL; }

En el ciclo a través de la lista de transacciones de posición, buscamos una transacción con el método de cambio de posición DEAL_ENTRY_OUT (salida del mercado) o DEAL_ENTRY_OUT_BY (cierre mediante una posición opuesta) y retornamos el puntero a la transacción encontrada.

Método que retorna el ticket de la transacción de apertura:

//+------------------------------------------------------------------+ //| Return the open deal ticket | //+------------------------------------------------------------------+ ulong CPosition::DealIn(void) const { CDeal *deal=this.GetDealIn(); return(deal!=NULL ? deal.Ticket() : 0); }

Obtenemos el puntero a la transacción de entrada al mercado y retornamos su ticket.

Método que retorna el ticket de la transacción cerrada:

//+------------------------------------------------------------------+ //| Return the close deal ticket | //+------------------------------------------------------------------+ ulong CPosition::DealOut(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Ticket() : 0); }

Obtenemos el puntero a la transacción de salida del mercado y retornamos su ticket.

Método que retorna el spread en la apertura:

//+------------------------------------------------------------------+ //| Return spread when opening | //+------------------------------------------------------------------+ int CPosition::SpreadIn(void) const { CDeal *deal=this.GetDealIn(); return(deal!=NULL ? deal.Spread() : 0); }

Obtenemos el puntero a la transacción de entrada al mercado y retornamos el valor del spread registrado en la transacción.

Método que retorna el spread al cierre:

//+------------------------------------------------------------------+ //| Return spread when closing | //+------------------------------------------------------------------+ int CPosition::SpreadOut(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Spread() : 0); }

Obtenemos el puntero a la transacción de salida del mercado y retornamos el valor del spread registrado en la transacción.

Método que retorna el precio Ask al cierre:

//+------------------------------------------------------------------+ //| Return Ask price when closing | //+------------------------------------------------------------------+ double CPosition::PriceOutAsk(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Ask() : 0); }

Obtenemos el puntero a la transacción de salida del mercado y retornamos el valor del precio Ask registrado en la transacción.

Método que retorna el precio de oferta al cierre:

//+------------------------------------------------------------------+ //| Return the Bid price when closing | //+------------------------------------------------------------------+ double CPosition::PriceOutBid(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Bid() : 0); }

Obtenemos el puntero a la transacción de salida del mercado y retornamos el valor del precio Bid registrado en la transacción.

Método que retorna el beneficio en puntos:

//+------------------------------------------------------------------+ //| Return a profit in points | //+------------------------------------------------------------------+ int CPosition::ProfitInPoints(void) const { //--- If symbol Point has not been received previously, inform of that and return 0 if(this.m_point==0) { ::Print("The Point() value could not be retrieved."); return 0; } //--- Get position open and close prices double open =this.PriceOpen(); double close=this.PriceClose(); //--- If failed to get the prices, return 0 if(open==0 || close==0) return 0; //--- Depending on the position type, return the calculated value of the position profit in points return (int)::round(this.TypePosition()==POSITION_TYPE_BUY ? (close-open)/this.m_point : (open-close)/this.m_point); }

Método que retorna el valor del spread al cierre:

//+------------------------------------------------------------------+ //| Return the spread value when closing | //+------------------------------------------------------------------+ double CPosition::SpreadOutCost(void) const { //--- Get close deal CDeal *deal=this.GetDealOut(); if(deal==NULL) return 0; //--- Get position profit and position profit in points double profit=this.Profit(); int profit_pt=this.ProfitInPoints(); //--- If the profit is zero, return the spread value using the TickValue * Spread * Lots equation if(profit==0) return(this.m_tick_value * deal.Spread() * deal.Volume()); //--- Calculate and return the spread value (proportion) return(profit_pt>0 ? deal.Spread() * ::fabs(profit / profit_pt) : 0); }

El método usa dos métodos para calcular el valor del spread:

- Si el beneficio de la posición no es igual a cero, entonces el coste del spread se calculará en proporción: tamaño del spread en puntos * beneficio de la posición en dinero / beneficio de la posición en puntos.

- Si el beneficio de la posición es cero, entonces el coste del spread se calculará utilizando la fórmula: coste del tick calculado * tamaño del spread en puntos * volumen de la transacción.

Método que establece la comisión total para todas las transacciones:

//+------------------------------------------------------------------+ //| Set the total commission for all deals | //+------------------------------------------------------------------+ void CPosition::SetCommissions(void) { double res=0; int total=this.m_list_deals.Total(); for(int i=0; i<total; i++) { CDeal *deal=this.m_list_deals.At(i); res+=(deal!=NULL ? deal.Commission() : 0); } this.SetProperty(POSITION_PROP_COMMISSIONS, res); }

Para determinar la comisión tomada durante toda la vida de una posición, deberemos sumar las comisiones de todas las transacciones en la posición. En un ciclo a través de la lista de las transacciones de la posición, añadimos la comisión de cada transacción al valor resultante, que finalmente será retornado por el método.

Método para establecer el pago total por la realización de transacciones:

//+------------------------------------------------------------------+ //| Sets the total deal fee | //+------------------------------------------------------------------+ void CPosition::SetFee(void) { double res=0; int total=this.m_list_deals.Total(); for(int i=0; i<total; i++) { CDeal *deal=this.m_list_deals.At(i); res+=(deal!=NULL ? deal.Fee() : 0); } this.SetProperty(POSITION_PROP_FEE, res); }

Aquí todo resulta exactamente igual que en el método anterior: retornamos la suma total de los valores Fee de cada transacción de la posición.

Ambos métodos deberán llamarse cuando ya se hayan enumerado todas las transacciones de la posición; de lo contrario, el resultado será incompleto.

Método que añade una transacción a la lista de transacciones en una posición:

//+------------------------------------------------------------------+ //| Add a deal to the list of deals | //+------------------------------------------------------------------+ CDeal *CPosition::DealAdd(const long ticket) { //--- A temporary object gets a ticket of the desired deal and the flag of sorting the list of deals by ticket this.m_temp_deal.SetTicket(ticket); this.m_list_deals.Sort(DEAL_PROP_TICKET); //--- Set the result of checking if a deal with such a ticket is present in the list bool exist=(this.m_list_deals.Search(&this.m_temp_deal)!=WRONG_VALUE); //--- Return sorting by time in milliseconds for the list this.m_list_deals.Sort(DEAL_PROP_TIME_MSC); //--- If a deal with such a ticket is already in the list, return NULL if(exist) return NULL; //--- Create a new deal object CDeal *deal=new CDeal(ticket); if(deal==NULL) return NULL; //--- Add the created object to the list in sorting order by time in milliseconds //--- If failed to add the deal to the list, remove the the deal object and return NULL if(!this.m_list_deals.InsertSort(deal)) { delete deal; return NULL; } //--- If this is a position closing deal, set the profit from the deal properties to the position profit value if(deal.Entry()==DEAL_ENTRY_OUT || deal.Entry()==DEAL_ENTRY_OUT_BY) { this.SetProfit(deal.Profit()); this.SetSwap(deal.Swap()); } //--- Return the pointer to the created deal object return deal; }

La lógica del método se detalla en los comentarios al código. El ticket de la transacción actualmente seleccionada se transmite al método. Si aún no hay transacciones con dicho ticket en la lista, se creará un nuevo objeto de transacción y se añadirá a la lista de transacciones de la posición.

Métodos que retornan las descripciones de algunas propiedades de una posición:

//+------------------------------------------------------------------+ //| Return a position type description | //+------------------------------------------------------------------+ string CPosition::TypeDescription(void) const { return(this.TypePosition()==POSITION_TYPE_BUY ? "Buy" : this.TypePosition()==POSITION_TYPE_SELL ? "Sell" : "Unknown::"+(string)this.TypePosition()); } //+------------------------------------------------------------------+ //| Return position open time and price description | //+------------------------------------------------------------------+ string CPosition::TimePriceOpenDescription(void) { return(::StringFormat("Opened %s [%.*f]", this.TimeMscToString(this.TimeMsc()),this.m_digits, this.PriceOpen())); } //+------------------------------------------------------------------+ //| Return position close time and price description | //+------------------------------------------------------------------+ string CPosition::TimePriceCloseDescription(void) { if(this.TimeCloseMsc()==0) return "Not closed yet"; return(::StringFormat("Closed %s [%.*f]", this.TimeMscToString(this.TimeCloseMsc()),this.m_digits, this.PriceClose())); } //+------------------------------------------------------------------+ //| Return a brief position description | //+------------------------------------------------------------------+ string CPosition::Description(void) { return(::StringFormat("%I64d (%s): %s %.2f %s #%I64d, Magic %I64d", this.AccountLogin(), this.AccountServer(), this.Symbol(), this.Volume(), this.TypeDescription(), this.ID(), this.Magic())); }

Estos métodos se usan, por ejemplo, para mostrar la descripción de una posición en el diario de registro.

Podemos imprimir la descripción de una posición en el diario de registro utilizando el método Print :

//+------------------------------------------------------------------+ //| Print the position properties and deals in the journal | //+------------------------------------------------------------------+ void CPosition::Print(void) { ::PrintFormat("%s\n-%s\n-%s", this.Description(), this.TimePriceOpenDescription(), this.TimePriceCloseDescription()); for(int i=0; i<this.m_list_deals.Total(); i++) { CDeal *deal=this.m_list_deals.At(i); if(deal==NULL) continue; deal.Print(); } }

Primero, se imprime un encabezado con una descripción de la posición y luego, en un ciclo a través de todas las transacciones en la posición, se imprime una descripción de cada transacción utilizando su método Print().

La clase de posición histórica está lista. Ahora crearemos una clase estática para seleccionar, buscar y filtrar transacciones y posiciones según sus propiedades.

Clase para la búsqueda y el filtrado según las propiedades de las transacciones y posiciones

Ya analizamos esta clase con detalle en el artículo "Biblioteca para el desarrollo rápido y sencillo de programas para MetaTrader (Parte III): Colección de órdenes y posiciones de mercado, búsqueda y filtrado" en el apartado Organización de la búsqueda.

En la carpeta \MQL5\Services\AccountReporter\, crearemos un nuevo archivo Select.mqh de la clase CSelect:

//+------------------------------------------------------------------+ //| Select.mqh | //| Copyright 2024, MetaQuotes Software Corp. | //| https://mql5.com/en/users/artmedia70 | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Software Corp." #property link "https://mql5.com/en/users/artmedia70" #property version "1.00" //+------------------------------------------------------------------+ //| Class for sorting objects meeting the criterion | //+------------------------------------------------------------------+ class CSelect { }

Luego escribiremos una enumeración de los modos de comparación, conectaremos los archivos de las clases de transacción y posición y declararemos una lista de almacenamiento :

//+------------------------------------------------------------------+ //| Select.mqh | //| Copyright 2024, MetaQuotes Software Corp. | //| https://mql5.com/en/users/artmedia70 | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Software Corp." #property link "https://mql5.com/en/users/artmedia70" #property version "1.00" enum ENUM_COMPARER_TYPE { EQUAL, // Equal MORE, // More LESS, // Less NO_EQUAL, // Not equal EQUAL_OR_MORE, // Equal or more EQUAL_OR_LESS // Equal or less }; //+------------------------------------------------------------------+ //| Include files | //+------------------------------------------------------------------+ #include "Deal.mqh" #include "Position.mqh" //+------------------------------------------------------------------+ //| Storage list | //+------------------------------------------------------------------+ CArrayObj ListStorage; // Storage object for storing sorted collection lists //+------------------------------------------------------------------+ //| Class for sorting objects meeting the criterion | //+------------------------------------------------------------------+ class CSelect { }

Vamos a escribir todos los métodos para seleccionar los objetos y crear listas que satisfagan los criterios de búsqueda: