Überwachung des Handels mit Push-Benachrichtigungen — Beispiel für einen MetaTrader 5 Dienst

Inhalt

- Einführung

- Projektstruktur

- Die Klasse Deal

- Historische Positionsklasse

- Klasse zum Suchen und Sortieren nach Eigenschaften von Deals und Positionen

- Klassensammlung von historischen Positionen

- Konto-Klasse

- Klassensammlung von Konten

- Service-App zur Erstellung von Handelsberichten und zum Versand von Benachrichtigungen

- Schlussfolgerung

Einführung

Eine wichtige Komponente beim Handel auf den Finanzmärkten ist die Verfügbarkeit von Informationen über die Ergebnisse von Geschäften, die in einem bestimmten Zeitraum in der Vergangenheit getätigt wurden.

Wahrscheinlich war jeder Händler schon einmal mit der Notwendigkeit konfrontiert, die Handelsergebnisse des vergangenen Tages, der vergangenen Woche, des vergangenen Monats usw. zu überwachen, um seine Strategie auf der Grundlage der Handelsergebnisse anzupassen. Das MetaTrader 5 Kundenterminal bietet Statistiken in Form von Berichten an, die es uns ermöglichen, die Handelsergebnisse in einer bequemen visuellen Form zu bewerten. Der Bericht kann uns helfen, unser Portfolio zu optimieren und zu verstehen, wie wir Risiken reduzieren und die Stabilität des Handels erhöhen können.

Um eine Strategie zu analysieren, klicken Sie auf Bericht im Kontextmenü des Handelsverlaufs oder auf Berichte im Menü Ansicht (oder drücken Sie einfach Alt+E):

|  |

Weitere Details finden Sie in dem Artikel „Neuer MetaTrader-Bericht: Die 5 wichtigsten Handelsmetriken“.

Wenn die vom Client-Terminal bereitgestellten Standardberichte aus irgendeinem Grund nicht ausreichen, bietet die MQL5-Sprache zahlreiche Möglichkeiten, eigene Programme zu erstellen, einschließlich solcher, die Berichte erzeugen und an das Smartphone des Händlers senden. Diese Möglichkeit wollen wir heute diskutieren.

Unser Programm sollte mit dem Start des Terminals beginnen, den Wechsel eines Handelskontos, den Beginn des Tages und die Zeit für die Erstellung und Versendung von Berichten verfolgen. Der Programmtyp Service ist für diese Zwecke geeignet.

Laut der MQL5-Referenz ist ein Service ein Programm, das im Gegensatz zu Indikatoren, EAs und Skripten keine Verbindung zu einem Chart benötigt, um zu funktionieren. Wie Skripte reagieren Dienste nicht auf Ereignisse außer auf Auslöser (trigger). Um einen Dienst zu starten, sollte sein Code die OnStart-Handler-Funktion enthalten. Dienste akzeptieren keine anderen Ereignisse außer Start, aber sie können mit EventChartCustom nutzerdefinierte Ereignisse an Charts senden. Dienste werden in <terminal_directory>\MQL5\Services gespeichert.

Jeder Dienst, der im Terminal läuft, arbeitet in seinem eigenen Fluss. Dies bedeutet, dass ein in einer Schleife laufender Dienst den Betrieb anderer Programme nicht beeinträchtigen kann. Unser Dienst soll in einer Endlosschleife arbeiten, soll in der angegebenen Zeit überwachen, soll die gesamte Handelshistorie lesen, die Listen von geschlossenen Positionen erstellen, diese Listen nach verschiedenen Kriterien sortieren und soll Berichte darüber im Journal und mittels Push-Benachrichtigungen an das Smartphone des Nutzers senden. Wenn der Dienst zum ersten Mal gestartet wird oder seine Einstellungen geändert werden, sollte er außerdem prüfen, ob Push-Benachrichtigungen vom Terminal aus gesendet werden können. Um dies zu erreichen, sollten wir eine Interaktion mit dem Nutzer über Nachrichtenfenster arrangieren und auf die Antwort und Reaktion des Nutzers warten. Außerdem gibt es beim Senden von Push-Benachrichtigungen Beschränkungen hinsichtlich der Häufigkeit der Benachrichtigungen pro Zeiteinheit. Daher ist es notwendig, Verzögerungen bei der Übermittlung von Benachrichtigungen festzulegen. All dies sollte den Betrieb anderer Anwendungen, die auf dem Client-Terminal laufen, in keiner Weise beeinträchtigen. Ausgehend von all dem oben Gesagten sind Dienste das geeignetste Instrument für die Erstellung eines solchen Projekts.

Nun muss man sich ein Bild von den Komponenten machen, die notwendig sind, um alles zusammenzusetzen.

Projektstruktur

Schauen wir uns das Programm und seine Bestandteile von Anfang bis Ende an:

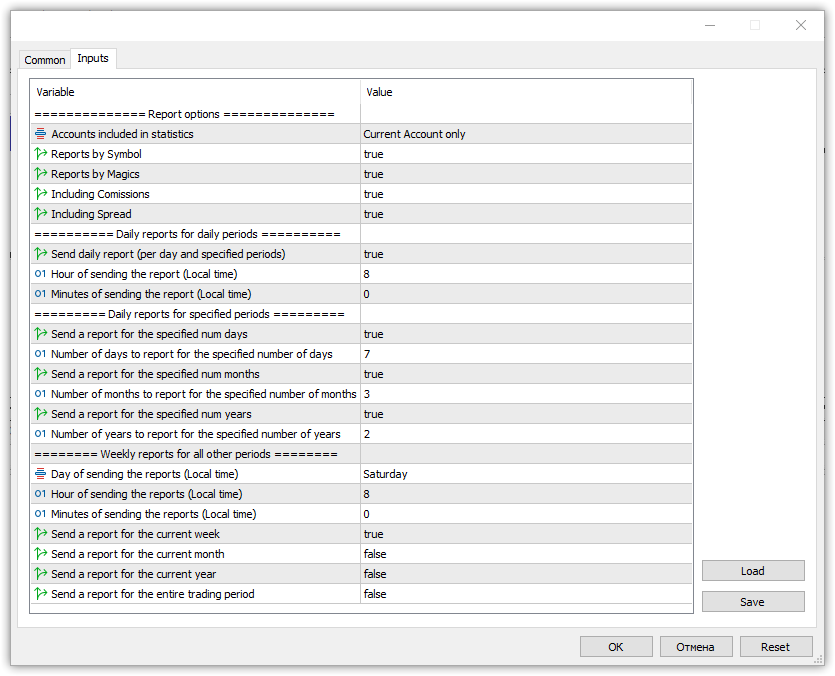

- Service-App. Die App hat Zugriff auf die Daten aller Konten, die während der gesamten Dauer des Betriebs des Dienstes aktiv waren. Aus den Kontendaten erhält die App Listen der geschlossenen Positionen und fasst sie zu einer Gesamtliste zusammen. Je nach den Einstellungen kann der Dienst Daten über geschlossene Positionen nur aus dem aktuellen aktiven Konto oder aus dem aktuellen und allen zuvor verwendeten Konten im Kundenterminal verwenden.

Die Handelsstatistik wird für die gewünschten Handelsperioden auf der Grundlage der Daten über geschlossene Positionen aus der Kontenliste erstellt. Anschließend wird sie als Push-Benachrichtigung an das Smartphone des Nutzers gesendet. Darüber hinaus werden die Handelsstatistiken in tabellarischer Form in den Terminalprotokollen der Experten angezeigt. - Einbeziehen der Konten. Die Sammlung enthält eine Liste der Konten, mit denen das Terminal während des laufenden Betriebs des Dienstes verbunden war. Die Kontenliste ermöglicht den Zugriff auf jedes Konto in der Liste und auf alle geschlossenen Positionen aller Konten. Die Listen stehen in der Service-App zur Verfügung, und der Dienst nimmt eine Auswahl vor und erstellt auf dieser Grundlage Statistiken.

- Objektklasse des Kontos. Speichert Daten für ein Konto mit einer Liste (Sammlung) aller geschlossenen Positionen, deren Deale auf diesem Konto während des laufenden Betriebs des Dienstes getätigt wurden. Ermöglicht den Zugriff auf die Kontoeigenschaften, das Erstellen und Aktualisieren der Liste der geschlossenen Positionen dieses Kontos und liefert Listen der geschlossenen Positionen nach verschiedenen Auswahlkriterien.

- Die Klassen für die Liste der historischen Positionen. Enthält eine Liste von Positionsobjekten und ermöglicht den Zugriff auf die Eigenschaften geschlossener Positionen sowie das Erstellen und Aktualisieren der Liste von Positionen. Gibt die Liste der geschlossenen Positionen zurück.

- Objektklasse Position. Speichert und ermöglicht den Zugriff auf die Eigenschaften einer geschlossenen Position. Enthält Funktionen zum Vergleich zweier Objekte anhand verschiedener Eigenschaften, die es ermöglichen, Positionslisten anhand verschiedener Auswahlkriterien zu erstellen. Enthält eine Liste der Angebote für diese Position und ermöglicht den Zugang zu ihnen.

- Objektklasse handeln. Speichert die Eigenschaften eines einzelnen Deals und ermöglicht den Zugriff darauf. Das Objekt enthält Funktionen für den Vergleich zweier Objekte anhand verschiedener Eigenschaften, wodurch es möglich ist, Listen von Deals anhand verschiedener Auswahlkriterien zu erstellen.

Das Konzept, eine geschlossene Position aus der Liste der historischen Deals wiederzufinden, haben wir im Artikel „Die Handelsgeschäfte direkt auf dem Chart beurteilen, statt in der Handelshistorie unterzugehen“ besprochen. Die Liste der Deals ermöglicht es, die Zugehörigkeit jedes Deals zu einer bestimmten Position anhand der in den Dealseigenschaften festgelegten Positions-ID (PositionID) zu bestimmen. Es wird ein Positionsobjekt erstellt, in dem die gefundenen Deals in die Liste aufgenommen werden. Hier werden wir genauso verfahren. Aber um die Konstruktion von Deal- und Positionsobjekten zu organisieren, werden wir ein völlig anderes, seit langem bewährtes Konzept verwenden, bei dem jedes Objekt identische Methoden des Zugriffs auf Eigenschaften hat, um sie zu setzen und zu erhalten. Dieses Konzept ermöglicht es uns, Objekte in einem einzigen gemeinsamen Schlüssel zu erstellen, sie in Listen zu speichern, nach einer beliebigen Objekteigenschaft zu filtern und zu sortieren und neue Listen im Zusammenhang mit der angegebenen Eigenschaft zu erhalten.

Lesen Sie die folgenden Artikel, um das Konzept des Erstellens von Klassen in diesem Projekt richtig zu verstehen:

- Struktur der Objekteigenschaften „(Teil I): Konzept, Datenmanagement und erste Ergebnisse“,

- Struktur von Objektlisten „(Teil II): Erhebung (Collection) historischer Aufträge und Deals“ und

- Methoden zum Filtern von Objekten in Listen nach Eigenschaften „(Teil III): Erhebung (Collection) von Marktorders und Positionen“

Im Wesentlichen beschreiben die drei Artikel die Möglichkeit, eine Datenbank für beliebige Objekte in MQL5 zu erstellen, sie in der Datenbank zu speichern und die erforderlichen Eigenschaften und Werte zu erhalten. Dies ist genau die Funktionalität, die in diesem Projekt benötigt wird, und aus diesem Grund wurde beschlossen, Objekte und ihre Sammlungen nach dem in den Artikeln beschriebenen Konzept aufzubauen. Nur wird es hier ein wenig einfacher gemacht - ohne abstrakte Objektklassen mit geschützten Konstruktoren zu erstellen und ohne nicht unterstützte Objekteigenschaften in den Klassen zu definieren. Alles wird einfacher - jedes Objekt hat seine eigene Liste von Eigenschaften, die in drei Arrays gespeichert sind und in die man schreiben und abrufen kann. Alle diese Objekte werden in den Listen gespeichert, aus denen dann neue Listen mit nur den gewünschten Objekten entsprechend den angegebenen Eigenschaften abgerufen werden können.

Kurz gesagt, jedes im Projekt erstellte Objekt hat einen Satz eigener Eigenschaften, so wie jedes Objekt oder jede Entität in MQL5. Nur in MQL5 gibt es Standardfunktionen für den Erhalt von Eigenschaften, und für Projektobjekte werden dies Methoden für den Erhalt von Integer-, Real- und String-Eigenschaften sein, die direkt in der Klasse jedes Objekts eingestellt werden. Im weiteren Verlauf werden alle diese Objekte in Listen gespeichert — dynamische Arrays von Zeigern auf die CObject-Objekte der Standardbibliothek. Die Klassen der Standardbibliothek ermöglichen es uns, komplexe Projekte mit minimalen Aufwand zu erstellen. In diesem Fall handelt es sich um eine Datenbank mit den geschlossenen Positionen aller Konten, auf denen Handel betrieben wurde, mit der Möglichkeit, Listen von Objekten zu erhalten, die nach jeder gewünschten Eigenschaft sortiert und ausgewählt werden können.

Jede Position besteht nur von dem Moment an, in dem sie eröffnet wird — einem „In-Deal“ bis zu dem Moment, in dem sie geschlossen wird — einem „Out/OutBuy-Deal“. Mit anderen Worten, es ist ein Objekt, das nur als Marktobjekt existiert. Jedes Handelsgeschäft bzw. „Deal“ ist im Gegenteil nur ein historischer Gegenstand, da ein Deal lediglich die Tatsache der Ausführung eines Auftrags (Handelsauftrags) ist. Daher gibt es im Kundenterminal keine Positionen in der historischen Liste - sie existieren nur in der Liste der aktuellen Marktpositionen.

Um eine bereits geschlossene Marktposition wiederherzustellen, ist es daher notwendig, eine bereits bestehende Position aus historischen Deals „zusammenzusetzen“. Glücklicherweise enthält jeder Deal die ID einer Position, an der der Deal beteiligt war. Wir müssen die Liste der historischen Deals durchgehen, den nächsten Deal aus der Liste holen, die Positions-ID überprüfen und das Positionsobjekt erstellen. Wir fügen das erstellte Deal-Objekt der neuen, historischen Position hinzu. Wir werden dies weiter umsetzen. In der Zwischenzeit erstellen wir die Klassen für die Objeke der DEals und Positionen, mit denen wir weiterarbeiten werden.

Die Klasse Deal

Im Terminalverzeichnis \MQL5\Services\ erstellen wir den neuen Ordner AccountReporter\ mit der neuen Datei Deal.mqh der Klasse CDeal.

Die Klasse sollte von der Basisklasse der Standardbibliothek CObject abgeleitet werden, während ihre Datei in die neu erstellte Klasse eingebunden werden sollte:

//+------------------------------------------------------------------+ //| Deal.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include <Object.mqh> //+------------------------------------------------------------------+ //| Deal class | //+------------------------------------------------------------------+ class CDeal : public CObject { }

Fügen wir nun die Enumeration von Integer-, Real- und String-Eigenschaften der Deals hinzu, während wir in den Abschnitten private, protected und public die Mitgliedsvariablen der Klasse und die Methoden zur Behandlung von Deal-Eigenschaften deklarieren:

//+------------------------------------------------------------------+ //| Deal.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include <Object.mqh> //--- Enumeration of integer deal properties enum ENUM_DEAL_PROPERTY_INT { DEAL_PROP_TICKET = 0, // Deal ticket DEAL_PROP_ORDER, // Deal order number DEAL_PROP_TIME, // Deal execution time DEAL_PROP_TIME_MSC, // Deal execution time in milliseconds DEAL_PROP_TYPE, // Deal type DEAL_PROP_ENTRY, // Deal direction DEAL_PROP_MAGIC, // Deal magic number DEAL_PROP_REASON, // Deal execution reason or source DEAL_PROP_POSITION_ID, // Position ID DEAL_PROP_SPREAD, // Spread when performing a deal }; //--- Enumeration of real deal properties enum ENUM_DEAL_PROPERTY_DBL { DEAL_PROP_VOLUME = DEAL_PROP_SPREAD+1,// Deal volume DEAL_PROP_PRICE, // Deal price DEAL_PROP_COMMISSION, // Commission DEAL_PROP_SWAP, // Accumulated swap when closing DEAL_PROP_PROFIT, // Deal financial result DEAL_PROP_FEE, // Deal fee DEAL_PROP_SL, // Stop Loss level DEAL_PROP_TP, // Take Profit level }; //--- Enumeration of string deal properties enum ENUM_DEAL_PROPERTY_STR { DEAL_PROP_SYMBOL = DEAL_PROP_TP+1, // Symbol the deal is executed for DEAL_PROP_COMMENT, // Deal comment DEAL_PROP_EXTERNAL_ID, // Deal ID in an external trading system }; //+------------------------------------------------------------------+ //| Deal class | //+------------------------------------------------------------------+ class CDeal : public CObject { private: MqlTick m_tick; // Deal tick structure long m_lprop[DEAL_PROP_SPREAD+1]; // Array for storing integer properties double m_dprop[DEAL_PROP_TP-DEAL_PROP_SPREAD]; // Array for storing real properties string m_sprop[DEAL_PROP_EXTERNAL_ID-DEAL_PROP_TP]; // Array for storing string properties //--- Return the index of the array the deal's (1) double and (2) string properties are located at int IndexProp(ENUM_DEAL_PROPERTY_DBL property) const { return(int)property-DEAL_PROP_SPREAD-1; } int IndexProp(ENUM_DEAL_PROPERTY_STR property) const { return(int)property-DEAL_PROP_TP-1; } //--- Get a (1) deal tick and (2) a spread of the deal minute bar bool GetDealTick(const int amount=20); int GetSpreadM1(void); //--- Return time with milliseconds string TimeMscToString(const long time_msc,int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const; protected: //--- Additional properties int m_digits; // Symbol Digits double m_point; // Symbol Point double m_bid; // Bid when performing a deal double m_ask; // Ask when performing a deal public: //--- Set the properties //--- Set deal's (1) integer, (2) real and (3) string properties void SetProperty(ENUM_DEAL_PROPERTY_INT property,long value){ this.m_lprop[property]=value; } void SetProperty(ENUM_DEAL_PROPERTY_DBL property,double value){ this.m_dprop[this.IndexProp(property)]=value; } void SetProperty(ENUM_DEAL_PROPERTY_STR property,string value){ this.m_sprop[this.IndexProp(property)]=value; } //--- Integer properties void SetTicket(const long ticket) { this.SetProperty(DEAL_PROP_TICKET, ticket); } // Ticket void SetOrder(const long order) { this.SetProperty(DEAL_PROP_ORDER, order); } // Order void SetTime(const datetime time) { this.SetProperty(DEAL_PROP_TIME, time); } // Time void SetTimeMsc(const long value) { this.SetProperty(DEAL_PROP_TIME_MSC, value); } // Time in milliseconds void SetTypeDeal(const ENUM_DEAL_TYPE type) { this.SetProperty(DEAL_PROP_TYPE, type); } // Type void SetEntry(const ENUM_DEAL_ENTRY entry) { this.SetProperty(DEAL_PROP_ENTRY, entry); } // Direction void SetMagic(const long magic) { this.SetProperty(DEAL_PROP_MAGIC, magic); } // Magic number void SetReason(const ENUM_DEAL_REASON reason) { this.SetProperty(DEAL_PROP_REASON, reason); } // Deal execution reason or source void SetPositionID(const long id) { this.SetProperty(DEAL_PROP_POSITION_ID, id); } // Position ID //--- Real properties void SetVolume(const double volume) { this.SetProperty(DEAL_PROP_VOLUME, volume); } // Volume void SetPrice(const double price) { this.SetProperty(DEAL_PROP_PRICE, price); } // Price void SetCommission(const double value) { this.SetProperty(DEAL_PROP_COMMISSION, value); } // Commission void SetSwap(const double value) { this.SetProperty(DEAL_PROP_SWAP, value); } // Accumulated swap when closing void SetProfit(const double value) { this.SetProperty(DEAL_PROP_PROFIT, value); } // Financial result void SetFee(const double value) { this.SetProperty(DEAL_PROP_FEE, value); } // Deal fee void SetSL(const double value) { this.SetProperty(DEAL_PROP_SL, value); } // Stop Loss level void SetTP(const double value) { this.SetProperty(DEAL_PROP_TP, value); } // Take Profit level //--- String properties void SetSymbol(const string symbol) { this.SetProperty(DEAL_PROP_SYMBOL,symbol); } // Symbol name void SetComment(const string comment) { this.SetProperty(DEAL_PROP_COMMENT,comment); } // Comment void SetExternalID(const string ext_id) { this.SetProperty(DEAL_PROP_EXTERNAL_ID,ext_id); } // Deal ID in an external trading system //--- Get the properties //--- Return deal’s (1) integer, (2) real and (3) string property from the properties array long GetProperty(ENUM_DEAL_PROPERTY_INT property) const { return this.m_lprop[property]; } double GetProperty(ENUM_DEAL_PROPERTY_DBL property) const { return this.m_dprop[this.IndexProp(property)]; } string GetProperty(ENUM_DEAL_PROPERTY_STR property) const { return this.m_sprop[this.IndexProp(property)]; } //--- Integer properties long Ticket(void) const { return this.GetProperty(DEAL_PROP_TICKET); } // Ticket long Order(void) const { return this.GetProperty(DEAL_PROP_ORDER); } // Order datetime Time(void) const { return (datetime)this.GetProperty(DEAL_PROP_TIME); } // Time long TimeMsc(void) const { return this.GetProperty(DEAL_PROP_TIME_MSC); } // Time in milliseconds ENUM_DEAL_TYPE TypeDeal(void) const { return (ENUM_DEAL_TYPE)this.GetProperty(DEAL_PROP_TYPE); } // Type ENUM_DEAL_ENTRY Entry(void) const { return (ENUM_DEAL_ENTRY)this.GetProperty(DEAL_PROP_ENTRY); } // Direction long Magic(void) const { return this.GetProperty(DEAL_PROP_MAGIC); } // Magic number ENUM_DEAL_REASON Reason(void) const { return (ENUM_DEAL_REASON)this.GetProperty(DEAL_PROP_REASON); } // Deal execution reason or source long PositionID(void) const { return this.GetProperty(DEAL_PROP_POSITION_ID); } // Position ID //--- Real properties double Volume(void) const { return this.GetProperty(DEAL_PROP_VOLUME); } // Volume double Price(void) const { return this.GetProperty(DEAL_PROP_PRICE); } // Price double Commission(void) const { return this.GetProperty(DEAL_PROP_COMMISSION); } // Commission double Swap(void) const { return this.GetProperty(DEAL_PROP_SWAP); } // Accumulated swap when closing double Profit(void) const { return this.GetProperty(DEAL_PROP_PROFIT); } // Financial result double Fee(void) const { return this.GetProperty(DEAL_PROP_FEE); } // Deal fee double SL(void) const { return this.GetProperty(DEAL_PROP_SL); } // Stop Loss level double TP(void) const { return this.GetProperty(DEAL_PROP_TP); } // Take Profit level //--- String properties string Symbol(void) const { return this.GetProperty(DEAL_PROP_SYMBOL); } // Symbol name string Comment(void) const { return this.GetProperty(DEAL_PROP_COMMENT); } // Comment string ExternalID(void) const { return this.GetProperty(DEAL_PROP_EXTERNAL_ID); } // Deal ID in an external trading system //--- Additional properties double Bid(void) const { return this.m_bid; } // Bid when performing a deal double Ask(void) const { return this.m_ask; } // Ask when performing a deal int Spread(void) const { return (int)this.GetProperty(DEAL_PROP_SPREAD); } // Spread when performing a deal //--- Return the description of a (1) deal type, (2) position change method and (3) deal reason string TypeDescription(void) const; string EntryDescription(void) const; string ReasonDescription(void) const; //--- Return deal description string Description(void); //--- Print deal properties in the journal void Print(void); //--- Compare two objects by the property specified in 'mode' virtual int Compare(const CObject *node, const int mode=0) const; //--- Constructors/destructor CDeal(void){} CDeal(const ulong ticket); ~CDeal(); };

Werfen wir einen Blick auf die Implementierung der Methoden der Klasse.

Im Klassenkonstruktor kann man davon ausgehen, dass das Deal bereits ausgewählt wurde und wir seine Eigenschaften abrufen können:

//+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CDeal::CDeal(const ulong ticket) { //--- Store the properties //--- Integer properties this.SetTicket((long)ticket); // Deal ticket this.SetOrder(::HistoryDealGetInteger(ticket, DEAL_ORDER)); // Order this.SetTime((datetime)::HistoryDealGetInteger(ticket, DEAL_TIME)); // Deal execution time this.SetTimeMsc(::HistoryDealGetInteger(ticket, DEAL_TIME_MSC)); // Deal execution time in milliseconds this.SetTypeDeal((ENUM_DEAL_TYPE)::HistoryDealGetInteger(ticket, DEAL_TYPE)); // Type this.SetEntry((ENUM_DEAL_ENTRY)::HistoryDealGetInteger(ticket, DEAL_ENTRY)); // Direction this.SetMagic(::HistoryDealGetInteger(ticket, DEAL_MAGIC)); // Magic number this.SetReason((ENUM_DEAL_REASON)::HistoryDealGetInteger(ticket, DEAL_REASON)); // Deal execution reason or source this.SetPositionID(::HistoryDealGetInteger(ticket, DEAL_POSITION_ID)); // Position ID //--- Real properties this.SetVolume(::HistoryDealGetDouble(ticket, DEAL_VOLUME)); // Volume this.SetPrice(::HistoryDealGetDouble(ticket, DEAL_PRICE)); // Price this.SetCommission(::HistoryDealGetDouble(ticket, DEAL_COMMISSION)); // Commission this.SetSwap(::HistoryDealGetDouble(ticket, DEAL_SWAP)); // Accumulated swap when closing this.SetProfit(::HistoryDealGetDouble(ticket, DEAL_PROFIT)); // Financial result this.SetFee(::HistoryDealGetDouble(ticket, DEAL_FEE)); // Deal fee this.SetSL(::HistoryDealGetDouble(ticket, DEAL_SL)); // Stop Loss level this.SetTP(::HistoryDealGetDouble(ticket, DEAL_TP)); // Take Profit level //--- String properties this.SetSymbol(::HistoryDealGetString(ticket, DEAL_SYMBOL)); // Symbol name this.SetComment(::HistoryDealGetString(ticket, DEAL_COMMENT)); // Comment this.SetExternalID(::HistoryDealGetString(ticket, DEAL_EXTERNAL_ID)); // Deal ID in an external trading system //--- Additional parameters this.m_digits = (int)::SymbolInfoInteger(this.Symbol(), SYMBOL_DIGITS); this.m_point = ::SymbolInfoDouble(this.Symbol(), SYMBOL_POINT); //--- Parameters for calculating spread this.m_bid = 0; this.m_ask = 0; this.SetProperty(DEAL_PROP_SPREAD, 0); //--- If the historical tick and the Point value of the symbol were obtained if(this.GetDealTick() && this.m_point!=0) { //--- set the Bid and Ask price values, calculate and save the spread value this.m_bid=this.m_tick.bid; this.m_ask=this.m_tick.ask; int spread=(int)::fabs((this.m_ask-this.m_bid)/this.m_point); this.SetProperty(DEAL_PROP_SPREAD, spread); } //--- If failed to obtain a historical tick, take the spread value of the minute bar the deal took place on else this.SetProperty(DEAL_PROP_SPREAD, this.GetSpreadM1()); }

Wir speichern die Eigenschaften des Deals sowie die Ziffern und den Punkt des Symbols, für das das Deal getätigt wurde, in den Arrays der Klasseneigenschaften, um Berechnungen durchzuführen und die Dealsinformationen anzuzeigen. Als Nächstes rufen wir den historischen Tick zum Zeitpunkt des Dealsabschlusses ab. Auf diese Weise erhalten wir Zugang zu den Geld- und Briefkursen (Ask & Bid) zum Zeitpunkt des Deals und damit die Möglichkeit, den Spread zu berechnen.

Die Methode, die zwei Objekte anhand einer bestimmten Eigenschaft vergleicht:

//+------------------------------------------------------------------+ //| Compare two objects by the specified property | //+------------------------------------------------------------------+ int CDeal::Compare(const CObject *node,const int mode=0) const { const CDeal * obj = node; switch(mode) { case DEAL_PROP_TICKET : return(this.Ticket() > obj.Ticket() ? 1 : this.Ticket() < obj.Ticket() ? -1 : 0); case DEAL_PROP_ORDER : return(this.Order() > obj.Order() ? 1 : this.Order() < obj.Order() ? -1 : 0); case DEAL_PROP_TIME : return(this.Time() > obj.Time() ? 1 : this.Time() < obj.Time() ? -1 : 0); case DEAL_PROP_TIME_MSC : return(this.TimeMsc() > obj.TimeMsc() ? 1 : this.TimeMsc() < obj.TimeMsc() ? -1 : 0); case DEAL_PROP_TYPE : return(this.TypeDeal() > obj.TypeDeal() ? 1 : this.TypeDeal() < obj.TypeDeal() ? -1 : 0); case DEAL_PROP_ENTRY : return(this.Entry() > obj.Entry() ? 1 : this.Entry() < obj.Entry() ? -1 : 0); case DEAL_PROP_MAGIC : return(this.Magic() > obj.Magic() ? 1 : this.Magic() < obj.Magic() ? -1 : 0); case DEAL_PROP_REASON : return(this.Reason() > obj.Reason() ? 1 : this.Reason() < obj.Reason() ? -1 : 0); case DEAL_PROP_POSITION_ID : return(this.PositionID() > obj.PositionID() ? 1 : this.PositionID() < obj.PositionID() ? -1 : 0); case DEAL_PROP_SPREAD : return(this.Spread() > obj.Spread() ? 1 : this.Spread() < obj.Spread() ? -1 : 0); case DEAL_PROP_VOLUME : return(this.Volume() > obj.Volume() ? 1 : this.Volume() < obj.Volume() ? -1 : 0); case DEAL_PROP_PRICE : return(this.Price() > obj.Price() ? 1 : this.Price() < obj.Price() ? -1 : 0); case DEAL_PROP_COMMISSION : return(this.Commission() > obj.Commission() ? 1 : this.Commission() < obj.Commission() ? -1 : 0); case DEAL_PROP_SWAP : return(this.Swap() > obj.Swap() ? 1 : this.Swap() < obj.Swap() ? -1 : 0); case DEAL_PROP_PROFIT : return(this.Profit() > obj.Profit() ? 1 : this.Profit() < obj.Profit() ? -1 : 0); case DEAL_PROP_FEE : return(this.Fee() > obj.Fee() ? 1 : this.Fee() < obj.Fee() ? -1 : 0); case DEAL_PROP_SL : return(this.SL() > obj.SL() ? 1 : this.SL() < obj.SL() ? -1 : 0); case DEAL_PROP_TP : return(this.TP() > obj.TP() ? 1 : this.TP() < obj.TP() ? -1 : 0); case DEAL_PROP_SYMBOL : return(this.Symbol() > obj.Symbol() ? 1 : this.Symbol() < obj.Symbol() ? -1 : 0); case DEAL_PROP_COMMENT : return(this.Comment() > obj.Comment() ? 1 : this.Comment() < obj.Comment() ? -1 : 0); case DEAL_PROP_EXTERNAL_ID : return(this.ExternalID() > obj.ExternalID() ? 1 : this.ExternalID() < obj.ExternalID() ? -1 : 0); default : return(-1); } }

Dies ist eine virtuelle Methode, die die gleichnamige Methode in der übergeordneten Klasse CObject außer Kraft setzt. Je nach Vergleichsmodus (eine der Eigenschaften des Deal-Objekts) werden diese Eigenschaften für das aktuelle Objekt und für das durch den Zeiger an die Methode übergebene Objekt verglichen. Die Methode gibt 1 zurück, wenn der Wert der aktuellen Objekteigenschaft größer ist als der des Vergleichsobjekts. Ist er kleiner, erhalten wir -1. Wenn die Werte gleich sind, erhalten wir 0.

Die Methode, die eine Beschreibung des Deal-Typs zurückgibt:

//+------------------------------------------------------------------+ //| Return the deal type description | //+------------------------------------------------------------------+ string CDeal::TypeDescription(void) const { switch(this.TypeDeal()) { case DEAL_TYPE_BUY : return "Buy"; case DEAL_TYPE_SELL : return "Sell"; case DEAL_TYPE_BALANCE : return "Balance"; case DEAL_TYPE_CREDIT : return "Credit"; case DEAL_TYPE_CHARGE : return "Additional charge"; case DEAL_TYPE_CORRECTION : return "Correction"; case DEAL_TYPE_BONUS : return "Bonus"; case DEAL_TYPE_COMMISSION : return "Additional commission"; case DEAL_TYPE_COMMISSION_DAILY : return "Daily commission"; case DEAL_TYPE_COMMISSION_MONTHLY : return "Monthly commission"; case DEAL_TYPE_COMMISSION_AGENT_DAILY : return "Daily agent commission"; case DEAL_TYPE_COMMISSION_AGENT_MONTHLY: return "Monthly agent commission"; case DEAL_TYPE_INTEREST : return "Interest rate"; case DEAL_TYPE_BUY_CANCELED : return "Canceled buy deal"; case DEAL_TYPE_SELL_CANCELED : return "Canceled sell deal"; case DEAL_DIVIDEND : return "Dividend operations"; case DEAL_DIVIDEND_FRANKED : return "Franked (non-taxable) dividend operations"; case DEAL_TAX : return "Tax charges"; default : return "Unknown: "+(string)this.TypeDeal(); } }

Je nach Art des Deals wird dessen Textbeschreibung zurückgegeben. Für dieses Projekt ist diese Methode überflüssig, da wir nicht alle Arten von Deals verwenden werden, sondern nur diejenigen, die sich auf die Position - Kauf oder Verkauf - beziehen.

Die Methode liefert eine Beschreibung der Positionsänderungsmethode:

//+------------------------------------------------------------------+ //| Return position change method | //+------------------------------------------------------------------+ string CDeal::EntryDescription(void) const { switch(this.Entry()) { case DEAL_ENTRY_IN : return "Entry In"; case DEAL_ENTRY_OUT : return "Entry Out"; case DEAL_ENTRY_INOUT : return "Reverse"; case DEAL_ENTRY_OUT_BY : return "Close a position by an opposite one"; default : return "Unknown: "+(string)this.Entry(); } }

Die Methode liefert eine Beschreibung des Handelsgeschäftsgrundes:

//+------------------------------------------------------------------+ //| Return a deal reason description | //+------------------------------------------------------------------+ string CDeal::ReasonDescription(void) const { switch(this.Reason()) { case DEAL_REASON_CLIENT : return "Terminal"; case DEAL_REASON_MOBILE : return "Mobile"; case DEAL_REASON_WEB : return "Web"; case DEAL_REASON_EXPERT : return "EA"; case DEAL_REASON_SL : return "SL"; case DEAL_REASON_TP : return "TP"; case DEAL_REASON_SO : return "SO"; case DEAL_REASON_ROLLOVER : return "Rollover"; case DEAL_REASON_VMARGIN : return "Var. Margin"; case DEAL_REASON_SPLIT : return "Split"; case DEAL_REASON_CORPORATE_ACTION: return "Corp. Action"; default : return "Unknown reason "+(string)this.Reason(); } }

Die Methode liefert eine Handelsgeschäftsbeschreibung:

//+------------------------------------------------------------------+ //| Return deal description | //+------------------------------------------------------------------+ string CDeal::Description(void) { return(::StringFormat("Deal: %-9s %.2f %-4s #%I64d at %s", this.EntryDescription(), this.Volume(), this.TypeDescription(), this.Ticket(), this.TimeMscToString(this.TimeMsc()))); }

Die Methode, die die Handelsgeschäftseigenschaften im Journal ausgibt:

//+------------------------------------------------------------------+ //| Print deal properties in the journal | //+------------------------------------------------------------------+ void CDeal::Print(void) { ::Print(this.Description()); }

Die Methode liefert Zeitwert mit Millisekunden:

//+------------------------------------------------------------------+ //| Return time with milliseconds | //+------------------------------------------------------------------+ string CDeal::TimeMscToString(const long time_msc, int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const { return(::TimeToString(time_msc/1000, flags) + "." + ::IntegerToString(time_msc %1000, 3, '0')); }

Alle Methoden, die Textbeschreibungen zurückgeben und protokollieren, dienen der Beschreibung des Deals. Bei diesem Projekt werden sie eigentlich nicht benötigt, aber man sollte immer an Erweiterungen und Verbesserungen denken. Aus diesem Grund werden solche Methoden hier vorgestellt.

Methode, die den Deal-Tick empfängt:

//+------------------------------------------------------------------+ //| Get the deal tick | //| https://www.mql5.com/ru/forum/42122/page47#comment_37205238 | //+------------------------------------------------------------------+ bool CDeal::GetDealTick(const int amount=20) { MqlTick ticks[]; // We will receive ticks here int attempts = amount; // Number of attempts to get ticks int offset = 500; // Initial time offset for an attempt int copied = 0; // Number of ticks copied //--- Until the tick is copied and the number of copy attempts is over //--- we try to get a tick, doubling the initial time offset at each iteration (expand the "from_msc" time range) while(!::IsStopped() && (copied<=0) && (attempts--)!=0) copied = ::CopyTicksRange(this.Symbol(), ticks, COPY_TICKS_INFO, this.TimeMsc()-(offset <<=1), this.TimeMsc()); //--- If the tick was successfully copied (it is the last one in the tick array), set it to the m_tick variable if(copied>0) this.m_tick=ticks[copied-1]; //--- Return the flag that the tick was copied return(copied>0); }

Die Logik der Methode wird in den Codekommentaren beschrieben. Nach dem Erhalt eines Ticks werden der Brief- und der Geldkurs (Ask & Bid) daraus entnommen und die Spread-Größe wird als (Ask - Bid) / Point berechnet.

Wenn es nicht gelingt, mit dieser Methode einen Tick zu erhalten, ermitteln wir den Durchschnittswert der Spanne mit der Methode zur Ermittlung der Spanne des Minutenbarrens des Deals:

//+------------------------------------------------------------------+ //| Gets the spread of the deal minute bar | //+------------------------------------------------------------------+ int CDeal::GetSpreadM1(void) { int array[1]={}; int bar=::iBarShift(this.Symbol(), PERIOD_M1, this.Time()); if(bar==WRONG_VALUE) return 0; return(::CopySpread(this.Symbol(), PERIOD_M1, bar, 1, array)==1 ? array[0] : 0); }

Die Klasse der Deals ist fertig. Die Objekte der Klasse werden in der Liste der Deals in der historischen Positionsklasse gespeichert, aus der es möglich sein wird, Zeiger auf die gewünschten Deals zu erhalten und deren Daten zu bearbeiten.

Historische Positionsklasse

Wir erstellen in \MQL5\Services\AccountReporter\ die neue Datei Position.mqh mit der Klasse CPosition.

Die Klasse sollte von der Basisobjektklasse CObject Standard Library abgeleitet werden:

//+------------------------------------------------------------------+ //| Position.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" //+------------------------------------------------------------------+ //| Position class | //+------------------------------------------------------------------+ class CPosition : public CObject { }

Da die Positionsklasse eine Liste für diese Position enthalten wird, ist es notwendig, in die erstellte Datei die Deal-Klassendatei und die Klassendatei des dynamischen Arrays von Zeigern auf CObject-Objekte aufzunehmen:

//+------------------------------------------------------------------+ //| Position.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include "Deal.mqh" #include <Arrays\ArrayObj.mqh> //+------------------------------------------------------------------+ //| Position class | //+------------------------------------------------------------------+ class CPosition : public CObject { }

Fügen wir nun die Enumeration der Integer-, Real- und String-Deal-Eigenschaften hinzu, während wir in den Abschnitten private, protected und public die Mitgliedsvariablen der Klasse und die Methoden zur Behandlung der Positionseigenschaften deklarieren:

//+------------------------------------------------------------------+ //| Position.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include "Deal.mqh" #include <Arrays\ArrayObj.mqh> //--- Enumeration of integer position properties enum ENUM_POSITION_PROPERTY_INT { POSITION_PROP_TICKET = 0, // Position ticket POSITION_PROP_TIME, // Position open time POSITION_PROP_TIME_MSC, // Position open time in milliseconds POSITION_PROP_TIME_UPDATE, // Position change time POSITION_PROP_TIME_UPDATE_MSC, // Position change time in milliseconds POSITION_PROP_TYPE, // Position type POSITION_PROP_MAGIC, // Position magic number POSITION_PROP_IDENTIFIER, // Position ID POSITION_PROP_REASON, // Position open reason POSITION_PROP_ACCOUNT_LOGIN, // Account number POSITION_PROP_TIME_CLOSE, // Position close time POSITION_PROP_TIME_CLOSE_MSC, // Position close time in milliseconds }; //--- Enumeration of real position properties enum ENUM_POSITION_PROPERTY_DBL { POSITION_PROP_VOLUME = POSITION_PROP_TIME_CLOSE_MSC+1,// Position volume POSITION_PROP_PRICE_OPEN, // Position price POSITION_PROP_SL, // Stop Loss for open position POSITION_PROP_TP, // Take Profit for open position POSITION_PROP_PRICE_CURRENT, // Symbol current price POSITION_PROP_SWAP, // Accumulated swap POSITION_PROP_PROFIT, // Current profit POSITION_PROP_CONTRACT_SIZE, // Symbol trade contract size POSITION_PROP_PRICE_CLOSE, // Position close price POSITION_PROP_COMMISSIONS, // Accumulated commission POSITION_PROP_FEE, // Accumulated payment for deals }; //--- Enumeration of string position properties enum ENUM_POSITION_PROPERTY_STR { POSITION_PROP_SYMBOL = POSITION_PROP_FEE+1,// A symbol the position is open for POSITION_PROP_COMMENT, // Comment to a position POSITION_PROP_EXTERNAL_ID, // Position ID in the external system POSITION_PROP_CURRENCY_PROFIT, // Position symbol profit currency POSITION_PROP_ACCOUNT_CURRENCY, // Account deposit currency POSITION_PROP_ACCOUNT_SERVER, // Server name }; //+------------------------------------------------------------------+ //| Position class | //+------------------------------------------------------------------+ class CPosition : public CObject { private: long m_lprop[POSITION_PROP_TIME_CLOSE_MSC+1]; // Array for storing integer properties double m_dprop[POSITION_PROP_FEE-POSITION_PROP_TIME_CLOSE_MSC]; // Array for storing real properties string m_sprop[POSITION_PROP_ACCOUNT_SERVER-POSITION_PROP_FEE]; // Array for storing string properties //--- Return the index of the array the order's (1) double and (2) string properties are located at int IndexProp(ENUM_POSITION_PROPERTY_DBL property) const { return(int)property-POSITION_PROP_TIME_CLOSE_MSC-1;} int IndexProp(ENUM_POSITION_PROPERTY_STR property) const { return(int)property-POSITION_PROP_FEE-1; } protected: CArrayObj m_list_deals; // List of position deals CDeal m_temp_deal; // Temporary deal object for searching by property in the list //--- Return time with milliseconds string TimeMscToString(const long time_msc,int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const; //--- Additional properties int m_profit_pt; // Profit in points int m_digits; // Symbol digits double m_point; // One symbol point value double m_tick_value; // Calculated tick value //--- Return the pointer to (1) open and (2) close deal CDeal *GetDealIn(void) const; CDeal *GetDealOut(void) const; public: //--- Return the list of deals CArrayObj *GetListDeals(void) { return(&this.m_list_deals); } //--- Set the properties //--- Set (1) integer, (2) real and (3) string properties void SetProperty(ENUM_POSITION_PROPERTY_INT property,long value) { this.m_lprop[property]=value; } void SetProperty(ENUM_POSITION_PROPERTY_DBL property,double value) { this.m_dprop[this.IndexProp(property)]=value; } void SetProperty(ENUM_POSITION_PROPERTY_STR property,string value) { this.m_sprop[this.IndexProp(property)]=value; } //--- Integer properties void SetTicket(const long ticket) { this.SetProperty(POSITION_PROP_TICKET, ticket); } // Position ticket void SetTime(const datetime time) { this.SetProperty(POSITION_PROP_TIME, time); } // Position open time void SetTimeMsc(const long value) { this.SetProperty(POSITION_PROP_TIME_MSC, value); } // Position open time in milliseconds since 01.01.1970 void SetTimeUpdate(const datetime time) { this.SetProperty(POSITION_PROP_TIME_UPDATE, time); } // Position update time void SetTimeUpdateMsc(const long value) { this.SetProperty(POSITION_PROP_TIME_UPDATE_MSC, value); } // Position update time in milliseconds since 01.01.1970 void SetTypePosition(const ENUM_POSITION_TYPE type) { this.SetProperty(POSITION_PROP_TYPE, type); } // Position type void SetMagic(const long magic) { this.SetProperty(POSITION_PROP_MAGIC, magic); } // Magic number for a position (see ORDER_MAGIC) void SetID(const long id) { this.SetProperty(POSITION_PROP_IDENTIFIER, id); } // Position ID void SetReason(const ENUM_POSITION_REASON reason) { this.SetProperty(POSITION_PROP_REASON, reason); } // Position open reason void SetTimeClose(const datetime time) { this.SetProperty(POSITION_PROP_TIME_CLOSE, time); } // Close time void SetTimeCloseMsc(const long value) { this.SetProperty(POSITION_PROP_TIME_CLOSE_MSC, value); } // Close time in milliseconds void SetAccountLogin(const long login) { this.SetProperty(POSITION_PROP_ACCOUNT_LOGIN, login); } // Acount number //--- Real properties void SetVolume(const double volume) { this.SetProperty(POSITION_PROP_VOLUME, volume); } // Position volume void SetPriceOpen(const double price) { this.SetProperty(POSITION_PROP_PRICE_OPEN, price); } // Position price void SetSL(const double value) { this.SetProperty(POSITION_PROP_SL, value); } // Stop Loss level for an open position void SetTP(const double value) { this.SetProperty(POSITION_PROP_TP, value); } // Take Profit level for an open position void SetPriceCurrent(const double price) { this.SetProperty(POSITION_PROP_PRICE_CURRENT, price); } // Current price by symbol void SetSwap(const double value) { this.SetProperty(POSITION_PROP_SWAP, value); } // Accumulated swap void SetProfit(const double value) { this.SetProperty(POSITION_PROP_PROFIT, value); } // Current profit void SetPriceClose(const double price) { this.SetProperty(POSITION_PROP_PRICE_CLOSE, price); } // Close price void SetContractSize(const double value) { this.SetProperty(POSITION_PROP_CONTRACT_SIZE, value); } // Symbol trading contract size void SetCommissions(void); // Total commission of all deals void SetFee(void); // Total deal fee //--- String properties void SetSymbol(const string symbol) { this.SetProperty(POSITION_PROP_SYMBOL, symbol); } // Symbol a position is opened for void SetComment(const string comment) { this.SetProperty(POSITION_PROP_COMMENT, comment); } // Position comment void SetExternalID(const string ext_id) { this.SetProperty(POSITION_PROP_EXTERNAL_ID, ext_id); } // Position ID in an external system (on the exchange) void SetAccountServer(const string server) { this.SetProperty(POSITION_PROP_ACCOUNT_SERVER, server); } // Server name void SetAccountCurrency(const string currency) { this.SetProperty(POSITION_PROP_ACCOUNT_CURRENCY, currency); } // Account deposit currency void SetCurrencyProfit(const string currency) { this.SetProperty(POSITION_PROP_CURRENCY_PROFIT, currency); } // Profit currency of the position symbol //--- Get the properties //--- Return (1) integer, (2) real and (3) string property from the properties array long GetProperty(ENUM_POSITION_PROPERTY_INT property) const { return this.m_lprop[property]; } double GetProperty(ENUM_POSITION_PROPERTY_DBL property) const { return this.m_dprop[this.IndexProp(property)]; } string GetProperty(ENUM_POSITION_PROPERTY_STR property) const { return this.m_sprop[this.IndexProp(property)]; } //--- Integer properties long Ticket(void) const { return this.GetProperty(POSITION_PROP_TICKET); } // Position ticket datetime Time(void) const { return (datetime)this.GetProperty(POSITION_PROP_TIME); } // Position open time long TimeMsc(void) const { return this.GetProperty(POSITION_PROP_TIME_MSC); } // Position open time in milliseconds since 01.01.1970 datetime TimeUpdate(void) const { return (datetime)this.GetProperty(POSITION_PROP_TIME_UPDATE);} // Position change time long TimeUpdateMsc(void) const { return this.GetProperty(POSITION_PROP_TIME_UPDATE_MSC); } // Position update time in milliseconds since 01.01.1970 ENUM_POSITION_TYPE TypePosition(void) const { return (ENUM_POSITION_TYPE)this.GetProperty(POSITION_PROP_TYPE);}// Position type long Magic(void) const { return this.GetProperty(POSITION_PROP_MAGIC); } // Magic number for a position (see ORDER_MAGIC) long ID(void) const { return this.GetProperty(POSITION_PROP_IDENTIFIER); } // Position ID ENUM_POSITION_REASON Reason(void) const { return (ENUM_POSITION_REASON)this.GetProperty(POSITION_PROP_REASON);}// Position opening reason datetime TimeClose(void) const { return (datetime)this.GetProperty(POSITION_PROP_TIME_CLOSE); } // Close time long TimeCloseMsc(void) const { return this.GetProperty(POSITION_PROP_TIME_CLOSE_MSC); } // Close time in milliseconds long AccountLogin(void) const { return this.GetProperty(POSITION_PROP_ACCOUNT_LOGIN); } // Login //--- Real properties double Volume(void) const { return this.GetProperty(POSITION_PROP_VOLUME); } // Position volume double PriceOpen(void) const { return this.GetProperty(POSITION_PROP_PRICE_OPEN); } // Position price double SL(void) const { return this.GetProperty(POSITION_PROP_SL); } // Stop Loss level for an open position double TP(void) const { return this.GetProperty(POSITION_PROP_TP); } // Take Profit level for an open position double PriceCurrent(void) const { return this.GetProperty(POSITION_PROP_PRICE_CURRENT); } // Current price by symbol double Swap(void) const { return this.GetProperty(POSITION_PROP_SWAP); } // Accumulated swap double Profit(void) const { return this.GetProperty(POSITION_PROP_PROFIT); } // Current profit double ContractSize(void) const { return this.GetProperty(POSITION_PROP_CONTRACT_SIZE); } // Symbol trading contract size double PriceClose(void) const { return this.GetProperty(POSITION_PROP_PRICE_CLOSE); } // Close price double Commissions(void) const { return this.GetProperty(POSITION_PROP_COMMISSIONS); } // Total commission of all deals double Fee(void) const { return this.GetProperty(POSITION_PROP_FEE); } // Total deal fee //--- String properties string Symbol(void) const { return this.GetProperty(POSITION_PROP_SYMBOL); } // A symbol position is opened on string Comment(void) const { return this.GetProperty(POSITION_PROP_COMMENT); } // Position comment string ExternalID(void) const { return this.GetProperty(POSITION_PROP_EXTERNAL_ID); } // Position ID in an external system (on the exchange) string AccountServer(void) const { return this.GetProperty(POSITION_PROP_ACCOUNT_SERVER); } // Server name string AccountCurrency(void) const { return this.GetProperty(POSITION_PROP_ACCOUNT_CURRENCY); } // Account deposit currency string CurrencyProfit(void) const { return this.GetProperty(POSITION_PROP_CURRENCY_PROFIT); } // Profit currency of the position symbol //--- Additional properties ulong DealIn(void) const; // Open deal ticket ulong DealOut(void) const; // Close deal ticket int ProfitInPoints(void) const; // Profit in points int SpreadIn(void) const; // Spread when opening int SpreadOut(void) const; // Spread when closing double SpreadOutCost(void) const; // Spread cost when closing double PriceOutAsk(void) const; // Ask price when closing double PriceOutBid(void) const; // Bid price when closing //--- Add a deal to the list of deals, return the pointer CDeal *DealAdd(const long ticket); //--- Return a position type description string TypeDescription(void) const; //--- Return position open time and price description string TimePriceCloseDescription(void); //--- Return position close time and price description string TimePriceOpenDescription(void); //--- Return position description string Description(void); //--- Print the properties of the position and its deals in the journal void Print(void); //--- Compare two objects by the property specified in 'mode' virtual int Compare(const CObject *node, const int mode=0) const; //--- Constructor/destructor CPosition(const long position_id, const string symbol); CPosition(void){} ~CPosition(); };

Werfen wir einen Blick auf die Implementierung der Methoden der Klasse.

Wir legen die Positions-ID und das Symbol aus den Parametern fest, die der Methode im Klassenkonstruktor übergeben wurden, und schreiben die Konto- und Symboldaten:

//+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CPosition::CPosition(const long position_id, const string symbol) { this.m_list_deals.Sort(DEAL_PROP_TIME_MSC); this.SetID(position_id); this.SetSymbol(symbol); this.SetAccountLogin(::AccountInfoInteger(ACCOUNT_LOGIN)); this.SetAccountServer(::AccountInfoString(ACCOUNT_SERVER)); this.SetAccountCurrency(::AccountInfoString(ACCOUNT_CURRENCY)); this.SetCurrencyProfit(::SymbolInfoString(this.Symbol(),SYMBOL_CURRENCY_PROFIT)); this.SetContractSize(::SymbolInfoDouble(this.Symbol(),SYMBOL_TRADE_CONTRACT_SIZE)); this.m_digits = (int)::SymbolInfoInteger(this.Symbol(),SYMBOL_DIGITS); this.m_point = ::SymbolInfoDouble(this.Symbol(),SYMBOL_POINT); this.m_tick_value = ::SymbolInfoDouble(this.Symbol(), SYMBOL_TRADE_TICK_VALUE); }

Wir löschen im Destruktor der Klasse die Liste der Deals der Positionen:

//+------------------------------------------------------------------+ //| Destructor | //+------------------------------------------------------------------+ CPosition::~CPosition() { this.m_list_deals.Clear(); }

Die Methode, die zwei Objekte anhand einer bestimmten Eigenschaft vergleicht:

//+------------------------------------------------------------------+ //| Compare two objects by the specified property | //+------------------------------------------------------------------+ int CPosition::Compare(const CObject *node,const int mode=0) const { const CPosition *obj=node; switch(mode) { case POSITION_PROP_TICKET : return(this.Ticket() > obj.Ticket() ? 1 : this.Ticket() < obj.Ticket() ? -1 : 0); case POSITION_PROP_TIME : return(this.Time() > obj.Time() ? 1 : this.Time() < obj.Time() ? -1 : 0); case POSITION_PROP_TIME_MSC : return(this.TimeMsc() > obj.TimeMsc() ? 1 : this.TimeMsc() < obj.TimeMsc() ? -1 : 0); case POSITION_PROP_TIME_UPDATE : return(this.TimeUpdate() > obj.TimeUpdate() ? 1 : this.TimeUpdate() < obj.TimeUpdate() ? -1 : 0); case POSITION_PROP_TIME_UPDATE_MSC : return(this.TimeUpdateMsc() > obj.TimeUpdateMsc() ? 1 : this.TimeUpdateMsc() < obj.TimeUpdateMsc() ? -1 : 0); case POSITION_PROP_TYPE : return(this.TypePosition() > obj.TypePosition() ? 1 : this.TypePosition() < obj.TypePosition() ? -1 : 0); case POSITION_PROP_MAGIC : return(this.Magic() > obj.Magic() ? 1 : this.Magic() < obj.Magic() ? -1 : 0); case POSITION_PROP_IDENTIFIER : return(this.ID() > obj.ID() ? 1 : this.ID() < obj.ID() ? -1 : 0); case POSITION_PROP_REASON : return(this.Reason() > obj.Reason() ? 1 : this.Reason() < obj.Reason() ? -1 : 0); case POSITION_PROP_ACCOUNT_LOGIN : return(this.AccountLogin() > obj.AccountLogin() ? 1 : this.AccountLogin() < obj.AccountLogin() ? -1 : 0); case POSITION_PROP_TIME_CLOSE : return(this.TimeClose() > obj.TimeClose() ? 1 : this.TimeClose() < obj.TimeClose() ? -1 : 0); case POSITION_PROP_TIME_CLOSE_MSC : return(this.TimeCloseMsc() > obj.TimeCloseMsc() ? 1 : this.TimeCloseMsc() < obj.TimeCloseMsc() ? -1 : 0); case POSITION_PROP_VOLUME : return(this.Volume() > obj.Volume() ? 1 : this.Volume() < obj.Volume() ? -1 : 0); case POSITION_PROP_PRICE_OPEN : return(this.PriceOpen() > obj.PriceOpen() ? 1 : this.PriceOpen() < obj.PriceOpen() ? -1 : 0); case POSITION_PROP_SL : return(this.SL() > obj.SL() ? 1 : this.SL() < obj.SL() ? -1 : 0); case POSITION_PROP_TP : return(this.TP() > obj.TP() ? 1 : this.TP() < obj.TP() ? -1 : 0); case POSITION_PROP_PRICE_CURRENT : return(this.PriceCurrent() > obj.PriceCurrent() ? 1 : this.PriceCurrent() < obj.PriceCurrent() ? -1 : 0); case POSITION_PROP_SWAP : return(this.Swap() > obj.Swap() ? 1 : this.Swap() < obj.Swap() ? -1 : 0); case POSITION_PROP_PROFIT : return(this.Profit() > obj.Profit() ? 1 : this.Profit() < obj.Profit() ? -1 : 0); case POSITION_PROP_CONTRACT_SIZE : return(this.ContractSize() > obj.ContractSize() ? 1 : this.ContractSize() < obj.ContractSize() ? -1 : 0); case POSITION_PROP_PRICE_CLOSE : return(this.PriceClose() > obj.PriceClose() ? 1 : this.PriceClose() < obj.PriceClose() ? -1 : 0); case POSITION_PROP_COMMISSIONS : return(this.Commissions() > obj.Commissions() ? 1 : this.Commissions() < obj.Commissions() ? -1 : 0); case POSITION_PROP_FEE : return(this.Fee() > obj.Fee() ? 1 : this.Fee() < obj.Fee() ? -1 : 0); case POSITION_PROP_SYMBOL : return(this.Symbol() > obj.Symbol() ? 1 : this.Symbol() < obj.Symbol() ? -1 : 0); case POSITION_PROP_COMMENT : return(this.Comment() > obj.Comment() ? 1 : this.Comment() < obj.Comment() ? -1 : 0); case POSITION_PROP_EXTERNAL_ID : return(this.ExternalID() > obj.ExternalID() ? 1 : this.ExternalID() < obj.ExternalID() ? -1 : 0); case POSITION_PROP_CURRENCY_PROFIT : return(this.CurrencyProfit() > obj.CurrencyProfit() ? 1 : this.CurrencyProfit() < obj.CurrencyProfit() ? -1 : 0); case POSITION_PROP_ACCOUNT_CURRENCY : return(this.AccountCurrency() > obj.AccountCurrency() ? 1 : this.AccountCurrency() < obj.AccountCurrency() ? -1 : 0); case POSITION_PROP_ACCOUNT_SERVER : return(this.AccountServer() > obj.AccountServer() ? 1 : this.AccountServer() < obj.AccountServer() ? -1 : 0); default : return -1; } }

Dies ist eine virtuelle Methode, die die gleichnamige Methode in der übergeordneten Klasse CObject außer Kraft setzt. Je nach Vergleichsmodus (eine der Eigenschaften des Positionsobjekts) werden diese Eigenschaften für das aktuelle Objekt und für das durch den Zeiger an die Methode übergebene Objekt verglichen. Die Methode gibt 1 zurück, wenn der Wert der aktuellen Objekteigenschaft größer ist als der des Vergleichsobjekts. Ist er kleiner, erhalten wir -1. Wenn die Werte gleich sind, erhalten wir 0.

Die Methode, die die Zeit in Millisekunden zurückgibt:

//+------------------------------------------------------------------+ //| Return time with milliseconds | //+------------------------------------------------------------------+ string CPosition::TimeMscToString(const long time_msc, int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const { return(::TimeToString(time_msc/1000, flags) + "." + ::IntegerToString(time_msc %1000, 3, '0')); }

Die Methode, die den Zeiger auf das offene Deal zurückgibt:

//+------------------------------------------------------------------+ //| Return the pointer to the opening deal | //+------------------------------------------------------------------+ CDeal *CPosition::GetDealIn(void) const { int total=this.m_list_deals.Total(); for(int i=0; i<total; i++) { CDeal *deal=this.m_list_deals.At(i); if(deal==NULL) continue; if(deal.Entry()==DEAL_ENTRY_IN) return deal; } return NULL; }

In der Schleife über die Liste der Positions-Deals suchen wir nach einem Deal mit der Positionsänderung DEAL_ENTRY_IN (Markteintritt) und geben den Zeiger auf das gefundene Deal zurück

Die Methode, die den Zeiger auf das Schließen des Handelsgeschäfts zurückgibt:

//+------------------------------------------------------------------+ //| Return the pointer to the close deal | //+------------------------------------------------------------------+ CDeal *CPosition::GetDealOut(void) const { for(int i=this.m_list_deals.Total()-1; i>=0; i--) { CDeal *deal=this.m_list_deals.At(i); if(deal==NULL) continue; if(deal.Entry()==DEAL_ENTRY_OUT || deal.Entry()==DEAL_ENTRY_OUT_BY) return deal; } return NULL; }

Wir suchen in der Schleife durch die Liste der Positions-Deals nach einem Deal mit der Positionsänderung DEAL_ENTRY_OUT (Marktaustritt) oder DEAL_ENTRY_OUT_BY (Close by) und geben den Zeiger auf den gefundenen Deal zurück.

Die Methode, die die Ticketnummer des Deals der Eröffnung zurückgibt:

//+------------------------------------------------------------------+ //| Return the open deal ticket | //+------------------------------------------------------------------+ ulong CPosition::DealIn(void) const { CDeal *deal=this.GetDealIn(); return(deal!=NULL ? deal.Ticket() : 0); }

Sie holt den Zeiger auf den Markteintritts-Deal und gibt dessen Ticket zurück.

Die Methode, die die Ticketnummer des Deals des Schließens zurückgibt:

//+------------------------------------------------------------------+ //| Return the close deal ticket | //+------------------------------------------------------------------+ ulong CPosition::DealOut(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Ticket() : 0); }

Sie holt sich den Zeiger auf den Marktaustritts-Deal und gibt dessen Ticket zurück.

Die Methode, die den Spread beim Öffnen zurückgibt:

//+------------------------------------------------------------------+ //| Return spread when opening | //+------------------------------------------------------------------+ int CPosition::SpreadIn(void) const { CDeal *deal=this.GetDealIn(); return(deal!=NULL ? deal.Spread() : 0); }

Sie ermittelt den Zeiger auf den Markteintritts-Deal und gibt den im Deal eingetragenen Spread zurück.

Die Methode, die den Spread beim Schließen zurückgibt:

//+------------------------------------------------------------------+ //| Return spread when closing | //+------------------------------------------------------------------+ int CPosition::SpreadOut(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Spread() : 0); }

Sie ermittelt den Zeiger auf den Marktaustritts-Deal und gibt die in diesem Deal festgelegten Spread zurück.

Die Methode liefert den Briefkurs (Ask) beim Schließen zurück:

//+------------------------------------------------------------------+ //| Return Ask price when closing | //+------------------------------------------------------------------+ double CPosition::PriceOutAsk(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Ask() : 0); }

Sie ermittelt den Zeiger auf den Marktaustritts-Deal und gibt den im Deal festgelegten Wert für den Briefkurs zurück.

Die Methode liefert den Geldkurs (Bid) beim Schließen:

//+------------------------------------------------------------------+ //| Return the Bid price when closing | //+------------------------------------------------------------------+ double CPosition::PriceOutBid(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Bid() : 0); }

Sie ermittelt den Zeiger auf den Marktaustritts-Deal und gibt den im Deal festgelegten Geldkurs zurück.

Die Methode liefert den Gewinn in Punkten:

//+------------------------------------------------------------------+ //| Return a profit in points | //+------------------------------------------------------------------+ int CPosition::ProfitInPoints(void) const { //--- If symbol Point has not been received previously, inform of that and return 0 if(this.m_point==0) { ::Print("The Point() value could not be retrieved."); return 0; } //--- Get position open and close prices double open =this.PriceOpen(); double close=this.PriceClose(); //--- If failed to get the prices, return 0 if(open==0 || close==0) return 0; //--- Depending on the position type, return the calculated value of the position profit in points return (int)::round(this.TypePosition()==POSITION_TYPE_BUY ? (close-open)/this.m_point : (open-close)/this.m_point); }

Die Methode, die die Spanne beim Schließen zurückgibt:

//+------------------------------------------------------------------+ //| Return the spread value when closing | //+------------------------------------------------------------------+ double CPosition::SpreadOutCost(void) const { //--- Get close deal CDeal *deal=this.GetDealOut(); if(deal==NULL) return 0; //--- Get position profit and position profit in points double profit=this.Profit(); int profit_pt=this.ProfitInPoints(); //--- If the profit is zero, return the spread value using the TickValue * Spread * Lots equation if(profit==0) return(this.m_tick_value * deal.Spread() * deal.Volume()); //--- Calculate and return the spread value (proportion) return(profit_pt>0 ? deal.Spread() * ::fabs(profit / profit_pt) : 0); }

Die Methode verwendet zwei Methoden zur Werteberechnung des Spreads:

- Wenn der Positionsgewinn ungleich Null ist, werden die Kosten des Spreads im Verhältnis berechnet: Spreadgröße in Punkten * Positionsgewinn in Geld / Positionsgewinn in Punkten.

- Wenn der Positionsgewinn gleich Null ist, wird der Spread-Wert nach folgender Gleichung berechnet: Berechneter Tick-Wert * Spread-Größe in Punkten * Dealsvolumen.

Die Methode, die die Gesamtprovision für alle Deals festlegt:

//+------------------------------------------------------------------+ //| Set the total commission for all deals | //+------------------------------------------------------------------+ void CPosition::SetCommissions(void) { double res=0; int total=this.m_list_deals.Total(); for(int i=0; i<total; i++) { CDeal *deal=this.m_list_deals.At(i); res+=(deal!=NULL ? deal.Commission() : 0); } this.SetProperty(POSITION_PROP_COMMISSIONS, res); }

Um die Provision für die gesamte Laufzeit der Position zu ermitteln, müssen wir die Provisionen aller Deals in der Position addieren. In der Schleife durch die Liste der Positionsgeschäfte addieren wir die Provision jedes Deals zu dem resultierenden Wert, der schließlich von der Methode zurückgegeben wird.

Die Methode zur Festlegung der gesamten Dealsgebühr:

//+------------------------------------------------------------------+ //| Sets the total deal fee | //+------------------------------------------------------------------+ void CPosition::SetFee(void) { double res=0; int total=this.m_list_deals.Total(); for(int i=0; i<total; i++) { CDeal *deal=this.m_list_deals.At(i); res+=(deal!=NULL ? deal.Fee() : 0); } this.SetProperty(POSITION_PROP_FEE, res); }

Hier ist alles genau gleich wie in der vorherigen Methode - wir geben die Gesamtsumme der Fee-Werte jedes Positionsgeschäfts zurück.

Diese beiden Methoden müssen aufgerufen werden, wenn alle Handelsgeschäfte der Position bereits aufgelistet sind, da das Ergebnis sonst unvollständig ist.

Die Methode, die ein Deal zur Liste der Positionsgeschäfte hinzufügt:

//+------------------------------------------------------------------+ //| Add a deal to the list of deals | //+------------------------------------------------------------------+ CDeal *CPosition::DealAdd(const long ticket) { //--- A temporary object gets a ticket of the desired deal and the flag of sorting the list of deals by ticket this.m_temp_deal.SetTicket(ticket); this.m_list_deals.Sort(DEAL_PROP_TICKET); //--- Set the result of checking if a deal with such a ticket is present in the list bool exist=(this.m_list_deals.Search(&this.m_temp_deal)!=WRONG_VALUE); //--- Return sorting by time in milliseconds for the list this.m_list_deals.Sort(DEAL_PROP_TIME_MSC); //--- If a deal with such a ticket is already in the list, return NULL if(exist) return NULL; //--- Create a new deal object CDeal *deal=new CDeal(ticket); if(deal==NULL) return NULL; //--- Add the created object to the list in sorting order by time in milliseconds //--- If failed to add the deal to the list, remove the the deal object and return NULL if(!this.m_list_deals.InsertSort(deal)) { delete deal; return NULL; } //--- If this is a position closing deal, set the profit from the deal properties to the position profit value if(deal.Entry()==DEAL_ENTRY_OUT || deal.Entry()==DEAL_ENTRY_OUT_BY) { this.SetProfit(deal.Profit()); this.SetSwap(deal.Swap()); } //--- Return the pointer to the created deal object return deal; }

Die Methodenlogik wird in den Codekommentaren beschrieben. Die Methode erhält das Ticket des aktuell ausgewählten Deals. Wenn es noch keine Deals mit einem solchen Ticket in der Liste gibt, wird ein neues Dealsobjekt erstellt und zur Liste der Positionsgeschäfte hinzugefügt.

Die Methoden, die Beschreibungen einiger Positionseigenschaften zurückgeben:

//+------------------------------------------------------------------+ //| Return a position type description | //+------------------------------------------------------------------+ string CPosition::TypeDescription(void) const { return(this.TypePosition()==POSITION_TYPE_BUY ? "Buy" : this.TypePosition()==POSITION_TYPE_SELL ? "Sell" : "Unknown::"+(string)this.TypePosition()); } //+------------------------------------------------------------------+ //| Return position open time and price description | //+------------------------------------------------------------------+ string CPosition::TimePriceOpenDescription(void) { return(::StringFormat("Opened %s [%.*f]", this.TimeMscToString(this.TimeMsc()),this.m_digits, this.PriceOpen())); } //+------------------------------------------------------------------+ //| Return position close time and price description | //+------------------------------------------------------------------+ string CPosition::TimePriceCloseDescription(void) { if(this.TimeCloseMsc()==0) return "Not closed yet"; return(::StringFormat("Closed %s [%.*f]", this.TimeMscToString(this.TimeCloseMsc()),this.m_digits, this.PriceClose())); } //+------------------------------------------------------------------+ //| Return a brief position description | //+------------------------------------------------------------------+ string CPosition::Description(void) { return(::StringFormat("%I64d (%s): %s %.2f %s #%I64d, Magic %I64d", this.AccountLogin(), this.AccountServer(), this.Symbol(), this.Volume(), this.TypeDescription(), this.ID(), this.Magic())); }

Diese Methoden werden z.B. verwendet, um eine Stellenbeschreibung im Journal anzuzeigen.

Mit der Methode „Print“ kann die Positionsbeschreibung im Journal angezeigt werden:

//+------------------------------------------------------------------+ //| Print the position properties and deals in the journal | //+------------------------------------------------------------------+ void CPosition::Print(void) { ::PrintFormat("%s\n-%s\n-%s", this.Description(), this.TimePriceOpenDescription(), this.TimePriceCloseDescription()); for(int i=0; i<this.m_list_deals.Total(); i++) { CDeal *deal=this.m_list_deals.At(i); if(deal==NULL) continue; deal.Print(); } }

Zunächst wird eine Kopfzeile mit einer Positionsbeschreibung gedruckt. Dann wird eine Beschreibung jedes Deals mit Hilfe der Print()-Methode in einer Schleife über alle Positionsgeschäfte gedruckt.

Die historische Positionsklasse ist fertig. Lassen Sie uns nun eine statische Klasse für die Auswahl, Suche und Sortierung von Deals und Positionen nach ihren Eigenschaften erstellen.

Klasse zum Suchen und Sortieren nach Eigenschaften von Deals und Positionen

Diese Klasse wurde besprochen in dem Artikel „Bibliothek für ein leichtes und schnelles Entwickeln vom Programmen für den MetaTrader (Teil III). Erhebung (Collection) von Marktorders und Positionen“ (Anordnen des Suchbereichs).

In \MQL5\Services\AccountReporter\ erstellen wir die neue Datei Select.mqh der Klasse CSelect:

//+------------------------------------------------------------------+ //| Select.mqh | //| Copyright 2024, MetaQuotes Software Corp. | //| https://mql5.com/de/users/artmedia70 | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Software Corp." #property link "https://mql5.com/de/users/artmedia70" #property version "1.00" //+------------------------------------------------------------------+ //| Class for sorting objects meeting the criterion | //+------------------------------------------------------------------+ class CSelect { }

Wir definieren die die Enumeration der Vergleichsmodi, binden die Dateien der Deal- und Positionsklassen ein und deklarieren die Speicherliste:

//+------------------------------------------------------------------+ //| Select.mqh | //| Copyright 2024, MetaQuotes Software Corp. | //| https://mql5.com/de/users/artmedia70 | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Software Corp." #property link "https://mql5.com/de/users/artmedia70" #property version "1.00" enum ENUM_COMPARER_TYPE { EQUAL, // Equal MORE, // More LESS, // Less NO_EQUAL, // Not equal EQUAL_OR_MORE, // Equal or more EQUAL_OR_LESS // Equal or less }; //+------------------------------------------------------------------+ //| Include files | //+------------------------------------------------------------------+ #include "Deal.mqh" #include "Position.mqh" //+------------------------------------------------------------------+ //| Storage list | //+------------------------------------------------------------------+ CArrayObj ListStorage; // Storage object for storing sorted collection lists //+------------------------------------------------------------------+ //| Class for sorting objects meeting the criterion | //+------------------------------------------------------------------+ class CSelect { }

Wir schreiben alle Methoden zur Auswahl von Objekten und zur Erstellung von Listen, die den Suchkriterien entsprechen: