プッシュ通知による取引の監視:MetaTrader 5サービスの例

内容

- はじめに

- プロジェクトの構造

- 取引クラス

- 履歴ポジションクラス

- 取引とポジションのプロパティで検索および並べ替えをおこなうクラス

- 履歴ポジションコレクションクラス

- 口座クラス

- 口座コレクションクラス

- 取引レポートの作成と通知の送信のためのサービスアプリ

- 結論

はじめに

金融市場で取引をおこなう場合、過去の一定期間におこなわれた取引の結果に関する情報が利用可能かどうかが重要な要素となります。

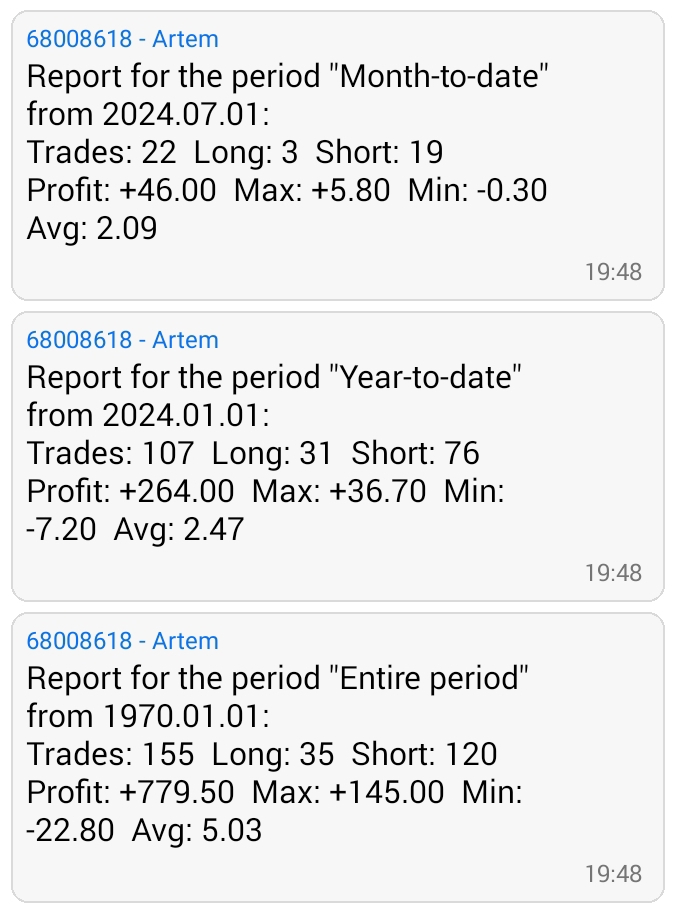

おそらく、すべてのトレーダーは、取引結果に基づいて戦略を調整するために、過去1日、1週間、1か月などの取引結果を監視する必要に少なくとも一度は直面したことがあるでしょう。MetaTrader5クライアント端末は、レポートの形で優れた統計情報を提供するため、取引結果を便利な視覚形式で評価できるようになります。このレポートは、ポートフォリオを最適化するだけでなく、リスクを軽減して取引の安定性を高める方法を理解するのに役立ちます。

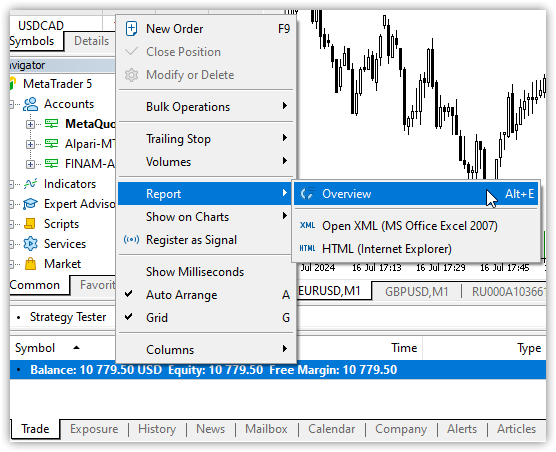

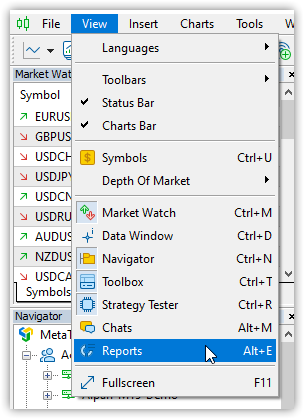

戦略を分析するには、取引履歴のコンテキストメニューで[レポート]をクリックするか、[表示]メニューで[レポート]をクリックします(または、Alt+Eを押します)。

|  |

詳細は「新しいMetaTraderレポート:5つの主要取引指標」で参照してください。

何らかの理由でクライアント端末から提供される標準レポートが十分でない場合、MQL5言語では、レポートを生成してトレーダーのスマートフォンに送信するプログラムなど、独自のプログラムを作成する十分な機会が提供されます。これが今日議論する可能性です。

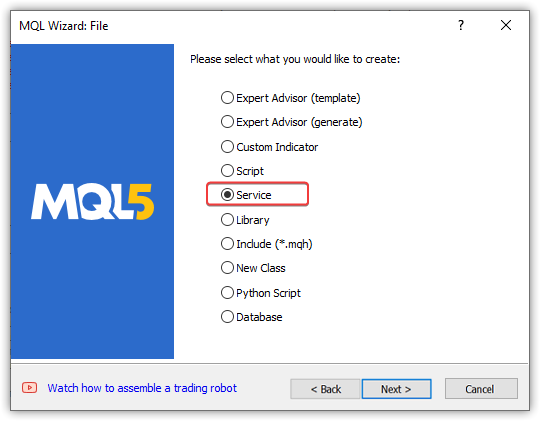

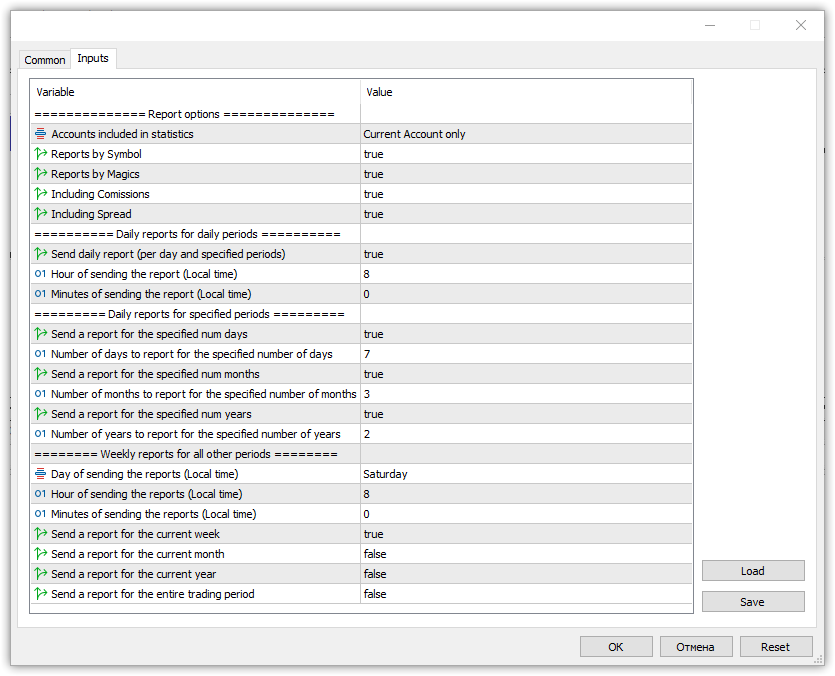

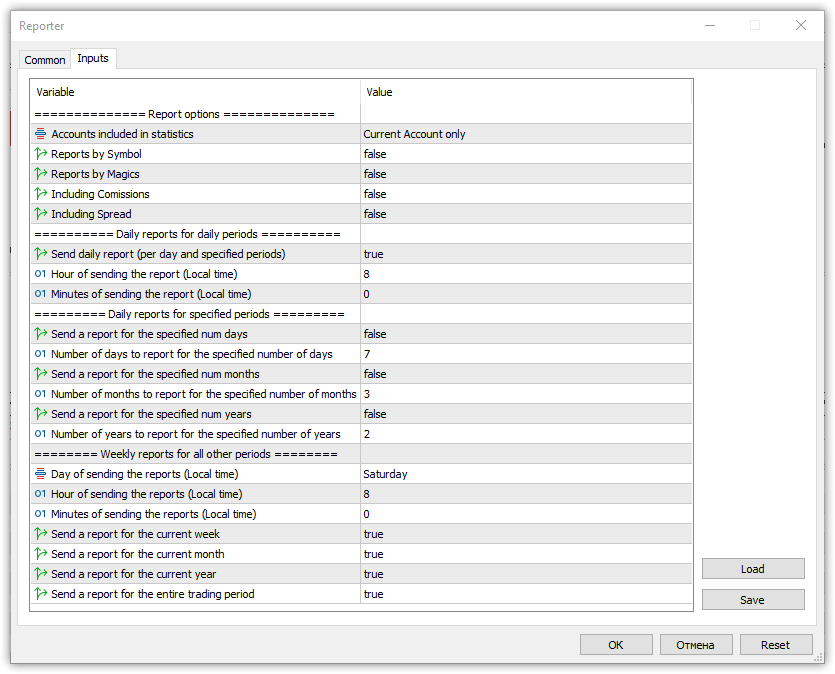

私たちのプログラムは、端末の起動時に開始し、取引口座の変更、日中の開始、レポートの作成と送信の時間を追跡する必要があります。このような目的には、サービスプログラムタイプが適しています。

MQL5リファレンスによれば、サービスはインジケーター、EA、スクリプトとは異なり、動作するためにチャートに接続する必要がないプログラムです。スクリプトと同様、サービスはトリガー以外のイベントを処理しません。サービスを起動するには、そのコードにOnStartハンドラ関数を含める必要があります。サービスはStart以外のイベントを受け入れませんが、EventChartCustomを使用してカスタムイベントをチャートへ送信できます。サービスは<端末ディレクトリ>\MQL5\Servicesに保存されます。

端末で実行されている各サービスは、独自のフローで動作します。つまり、ループされたサービスは他のプログラムの動作に影響を与えることはできません。私たちのサービスは、無限ループで動作し、指定された時間をチェックし、取引履歴全体を読み取り、クローズ済みポジションのリストを作成し、これらのリストをさまざまな基準で並べ替え、操作ログとプッシュ通知にレポートを表示し、ユーザーのスマートフォンに通知をプッシュします。また、サービスを初めて起動したときや設定を変更したときは、端末からプッシュ通知を送信できるかどうかをサービスで確認する必要があります。これを実現するには、ユーザーの応答と反応を待つメッセージウィンドウを介してユーザーとの対話を設定する必要があります。また、プッシュ通知を送信する場合、単位時間あたりの通知頻度に制限があるため、通知の送信に遅延を設定する必要があります。これらはすべて、クライアント端末で実行されている他のアプリケーションの動作に決して影響を与えません。上記のすべてに基づくと、サービスはこのようなプロジェクトを作成するための最も便利なツールです。

ここで、すべてを組み立てるために必要なコンポーネントのアイデアを形成する必要があります。

プロジェクトの構造

プログラムとそのコンポーネントを最初から最後まで見てみましょう。

- サービスアプリ:サービスの継続的な運用期間全体にわたってアクティブであったすべての口座のデータにアクセスできます。口座データからクローズ済みポジションのリストを受け取り、それらを1つの一般的なリストに結合します。設定に応じて、サービスは現在アクティブな口座からのみクローズ済みポジションのデータを使用するか、クライアント端末の現在の口座と以前に使用された各口座からクローズ済みポジションのデータを使用することができます。

取引統計は、口座リストから取得したクローズドポジションのデータに基づいて、必要な取引期間に対して作成されます。その後、プッシュ通知としてユーザーのスマートフォンに送信されます。さらに、取引統計はエキスパート端末ログに表形式で表示されます。 - 口座コレクション:コレクションには、サービスの継続的な運用中に端末が接続されていた口座のリストが含まれます。口座コレクションを使用すると、リスト内の任意の口座と、すべての口座のすべてのクローズ済みポジションにアクセスできます。リストはサービスアプリで利用でき、サービスは選択をおこない、それに基づいて統計を作成します。

- 口座オブジェクトクラス:サービスの継続的な運用中にこの口座で取引が実行されたすべてのクローズ済みポジションのリスト(コレクション)を含む、1つの口座のデータを保存します。口座のプロパティへのアクセス、この口座のクローズ済みポジションのリストの作成と更新を提供し、さまざまな選択基準によってクローズ済みポジションのリストを返します。

- 履歴ポジションコレクションクラス:ポジションオブジェクトのリストが含まれており、クローズ済みポジションのプロパティへのアクセス、ポジションのリストの作成と更新を提供します。クローズ済みポジションのリストを返します。

- ポジションオブジェクトクラス:クローズ済みポジションのプロパティを保存し、アクセスを提供します。さまざまなプロパティで2つのオブジェクトを比較する機能が含まれており、さまざまな選択基準によるポジションのリストを作成できます。このポジションの取引のリストが含まれており、それらにアクセスできます。

- 取引オブジェクトクラス:単一の取引のプロパティを保存し、アクセスを提供します。このオブジェクトには、さまざまなプロパティで2つのオブジェクトを比較する機能が含まれており、さまざまな選択基準で取引のリストを作成できます。

「取引履歴を気にせずにチャート上で直接取引を表示する方法」稿では、過去の取引リストからクローズ済みポジションを回復するという概念について説明しました。取引リストでは、取引プロパティで設定されたポジションID(PositionID)によって、各取引が特定のポジションに所属しているかどうかを判断できます。ポジションオブジェクトが作成され、見つかった取引がリストに配置されます。ここでも同じ方法を実行します。しかし、取引オブジェクトとポジションオブジェクトの構築を調整するために、各オブジェクトがプロパティを設定および取得するための同一のアクセス方法を持つ、完全に異なる、長年テストされた概念を使用します。この概念により、単一の共通キーでオブジェクトを作成し、リストに保存し、任意のオブジェクトプロパティでフィルタリングおよび並べ替え、指定されたプロパティのコンテキストで新しいリストを取得できるようになります。

このプロジェクトでクラスを構築する概念を正しく理解するには、次の記事をご覧ください。

- オブジェクトプロパティの構造「(第1回):概念、データ管理および最初の結果」

- オブジェクトリストの構造「(第2回):過去の注文と取引のコレクション」

- リスト内のオブジェクトをプロパティでフィルタリングする方法「(第3回):市場注文とポジションの収集、検索、並べ替え」

本質的には、この3つの記事では、MQL5内の任意のオブジェクトのデータベースを作成し、それらをデータベースに保存して、必要なプロパティと値を取得する可能性について説明しています。これはまさにこのプロジェクトに必要な機能であり、このため、記事で説明されている概念に従ってオブジェクトとそのコレクションを構築することが決定されました。ここでのみ、protectedコンストラクタを持つ抽象オブジェクトクラスを作成せず、クラスでサポートされていないオブジェクトプロパティを定義せずに、少し簡単に実行されます。すべてがよりシンプルになります。各オブジェクトには独自のプロパティリストがあり、3つの配列に格納されて、書き込みと取得が可能になります。これらのオブジェクトはすべてリストに保存され、指定されたプロパティに従って必要なオブジェクトのみの新しいリストを取得できるようになります。

つまり、プロジェクトで作成された各オブジェクトには、MQL5のあらゆるオブジェクトやエンティティと同様に、独自のプロパティセットが存在します。MQL5にのみ、プロパティを取得するための標準関数があり、プロジェクトオブジェクトの場合、これらは各オブジェクトのクラスに直接設定された整数、実数、文字列のプロパティを取得するためのメソッドになります。さらに、これらすべてのオブジェクトは、リストに格納されます。このリストは、標準ライブラリのCObjectオブジェクトへのポインタの動的配列です。標準ライブラリクラスを使用すると、最小限のコストで複雑なプロジェクトを作成できます。この場合、これは、取引がおこなわれたすべての口座のクローズ済みポジションのデータベースを意味し、必要なプロパティによって並べ替えられ選択されたオブジェクトのリストを取得する機能を備えています。

ポジションは、建てた瞬間(In dealを実行)からクローズした瞬間(Out/OutBuy dealを実行)までのみ存在します。つまり、市場オブジェクトとしてのみ存在するオブジェクトです。対照的に、取引は単に注文(取引注文)を実行した事実であるため、あらゆる取引は単なる履歴オブジェクトにすぎません。したがって、クライアント端末では、履歴リストにポジションはなく、現在の市場ポジションのリストにのみ存在します。

したがって、すでに閉じられた市場ポジションを再現するには、過去の取引から以前に存在していたポジションを「組み立てる」必要があります。幸いなことに、各取引には、その取引が関与したポジションIDが含まれています。過去の取引のリストを調べ、リストから次の取引を取得し、ポジションIDをチェックして、ポジションオブジェクトを作成する必要があります。作成された取引オブジェクトを新しい履歴ポジションに追加します。これをさらに実行していきます。その間、引き続き作業する取引とポジションオブジェクトのクラスを作成しましょう。

取引クラス

<端末ディレクトリ>\MQL5\Services\に、新しいAccountReporter\フォルダを作成して、CDealクラスのDeal.mqhという新しいファイルを配置します。

クラスは標準ライブラリのCObject基底クラスから派生する必要があり、そのファイルは新しく作成されたクラスに含まれる必要があります。

//+------------------------------------------------------------------+ //| Deal.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include <Object.mqh> //+------------------------------------------------------------------+ //| Deal class | //+------------------------------------------------------------------+ class CDeal : public CObject { }

次に、整数、実数、文字列の取引プロパティの列挙を追加し、private、protected、publicのセクションで、クラスメンバー変数と取引プロパティを処理するためのメソッドを宣言します。

//+------------------------------------------------------------------+ //| Deal.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include <Object.mqh> //--- Enumeration of integer deal properties enum ENUM_DEAL_PROPERTY_INT { DEAL_PROP_TICKET = 0, // Deal ticket DEAL_PROP_ORDER, // Deal order number DEAL_PROP_TIME, // Deal execution time DEAL_PROP_TIME_MSC, // Deal execution time in milliseconds DEAL_PROP_TYPE, // Deal type DEAL_PROP_ENTRY, // Deal direction DEAL_PROP_MAGIC, // Deal magic number DEAL_PROP_REASON, // Deal execution reason or source DEAL_PROP_POSITION_ID, // Position ID DEAL_PROP_SPREAD, // Spread when performing a deal }; //--- Enumeration of real deal properties enum ENUM_DEAL_PROPERTY_DBL { DEAL_PROP_VOLUME = DEAL_PROP_SPREAD+1,// Deal volume DEAL_PROP_PRICE, // Deal price DEAL_PROP_COMMISSION, // Commission DEAL_PROP_SWAP, // Accumulated swap when closing DEAL_PROP_PROFIT, // Deal financial result DEAL_PROP_FEE, // Deal fee DEAL_PROP_SL, // Stop Loss level DEAL_PROP_TP, // Take Profit level }; //--- Enumeration of string deal properties enum ENUM_DEAL_PROPERTY_STR { DEAL_PROP_SYMBOL = DEAL_PROP_TP+1, // Symbol the deal is executed for DEAL_PROP_COMMENT, // Deal comment DEAL_PROP_EXTERNAL_ID, // Deal ID in an external trading system }; //+------------------------------------------------------------------+ //| Deal class | //+------------------------------------------------------------------+ class CDeal : public CObject { private: MqlTick m_tick; // Deal tick structure long m_lprop[DEAL_PROP_SPREAD+1]; // Array for storing integer properties double m_dprop[DEAL_PROP_TP-DEAL_PROP_SPREAD]; // Array for storing real properties string m_sprop[DEAL_PROP_EXTERNAL_ID-DEAL_PROP_TP]; // Array for storing string properties //--- Return the index of the array the deal's (1) double and (2) string properties are located at int IndexProp(ENUM_DEAL_PROPERTY_DBL property) const { return(int)property-DEAL_PROP_SPREAD-1; } int IndexProp(ENUM_DEAL_PROPERTY_STR property) const { return(int)property-DEAL_PROP_TP-1; } //--- Get a (1) deal tick and (2) a spread of the deal minute bar bool GetDealTick(const int amount=20); int GetSpreadM1(void); //--- Return time with milliseconds string TimeMscToString(const long time_msc,int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const; protected: //--- Additional properties int m_digits; // Symbol Digits double m_point; // Symbol Point double m_bid; // Bid when performing a deal double m_ask; // Ask when performing a deal public: //--- Set the properties //--- Set deal's (1) integer, (2) real and (3) string properties void SetProperty(ENUM_DEAL_PROPERTY_INT property,long value){ this.m_lprop[property]=value; } void SetProperty(ENUM_DEAL_PROPERTY_DBL property,double value){ this.m_dprop[this.IndexProp(property)]=value; } void SetProperty(ENUM_DEAL_PROPERTY_STR property,string value){ this.m_sprop[this.IndexProp(property)]=value; } //--- Integer properties void SetTicket(const long ticket) { this.SetProperty(DEAL_PROP_TICKET, ticket); } // Ticket void SetOrder(const long order) { this.SetProperty(DEAL_PROP_ORDER, order); } // Order void SetTime(const datetime time) { this.SetProperty(DEAL_PROP_TIME, time); } // Time void SetTimeMsc(const long value) { this.SetProperty(DEAL_PROP_TIME_MSC, value); } // Time in milliseconds void SetTypeDeal(const ENUM_DEAL_TYPE type) { this.SetProperty(DEAL_PROP_TYPE, type); } // Type void SetEntry(const ENUM_DEAL_ENTRY entry) { this.SetProperty(DEAL_PROP_ENTRY, entry); } // Direction void SetMagic(const long magic) { this.SetProperty(DEAL_PROP_MAGIC, magic); } // Magic number void SetReason(const ENUM_DEAL_REASON reason) { this.SetProperty(DEAL_PROP_REASON, reason); } // Deal execution reason or source void SetPositionID(const long id) { this.SetProperty(DEAL_PROP_POSITION_ID, id); } // Position ID //--- Real properties void SetVolume(const double volume) { this.SetProperty(DEAL_PROP_VOLUME, volume); } // Volume void SetPrice(const double price) { this.SetProperty(DEAL_PROP_PRICE, price); } // Price void SetCommission(const double value) { this.SetProperty(DEAL_PROP_COMMISSION, value); } // Commission void SetSwap(const double value) { this.SetProperty(DEAL_PROP_SWAP, value); } // Accumulated swap when closing void SetProfit(const double value) { this.SetProperty(DEAL_PROP_PROFIT, value); } // Financial result void SetFee(const double value) { this.SetProperty(DEAL_PROP_FEE, value); } // Deal fee void SetSL(const double value) { this.SetProperty(DEAL_PROP_SL, value); } // Stop Loss level void SetTP(const double value) { this.SetProperty(DEAL_PROP_TP, value); } // Take Profit level //--- String properties void SetSymbol(const string symbol) { this.SetProperty(DEAL_PROP_SYMBOL,symbol); } // Symbol name void SetComment(const string comment) { this.SetProperty(DEAL_PROP_COMMENT,comment); } // Comment void SetExternalID(const string ext_id) { this.SetProperty(DEAL_PROP_EXTERNAL_ID,ext_id); } // Deal ID in an external trading system //--- Get the properties //--- Return deal’s (1) integer, (2) real and (3) string property from the properties array long GetProperty(ENUM_DEAL_PROPERTY_INT property) const { return this.m_lprop[property]; } double GetProperty(ENUM_DEAL_PROPERTY_DBL property) const { return this.m_dprop[this.IndexProp(property)]; } string GetProperty(ENUM_DEAL_PROPERTY_STR property) const { return this.m_sprop[this.IndexProp(property)]; } //--- Integer properties long Ticket(void) const { return this.GetProperty(DEAL_PROP_TICKET); } // Ticket long Order(void) const { return this.GetProperty(DEAL_PROP_ORDER); } // Order datetime Time(void) const { return (datetime)this.GetProperty(DEAL_PROP_TIME); } // Time long TimeMsc(void) const { return this.GetProperty(DEAL_PROP_TIME_MSC); } // Time in milliseconds ENUM_DEAL_TYPE TypeDeal(void) const { return (ENUM_DEAL_TYPE)this.GetProperty(DEAL_PROP_TYPE); } // Type ENUM_DEAL_ENTRY Entry(void) const { return (ENUM_DEAL_ENTRY)this.GetProperty(DEAL_PROP_ENTRY); } // Direction long Magic(void) const { return this.GetProperty(DEAL_PROP_MAGIC); } // Magic number ENUM_DEAL_REASON Reason(void) const { return (ENUM_DEAL_REASON)this.GetProperty(DEAL_PROP_REASON); } // Deal execution reason or source long PositionID(void) const { return this.GetProperty(DEAL_PROP_POSITION_ID); } // Position ID //--- Real properties double Volume(void) const { return this.GetProperty(DEAL_PROP_VOLUME); } // Volume double Price(void) const { return this.GetProperty(DEAL_PROP_PRICE); } // Price double Commission(void) const { return this.GetProperty(DEAL_PROP_COMMISSION); } // Commission double Swap(void) const { return this.GetProperty(DEAL_PROP_SWAP); } // Accumulated swap when closing double Profit(void) const { return this.GetProperty(DEAL_PROP_PROFIT); } // Financial result double Fee(void) const { return this.GetProperty(DEAL_PROP_FEE); } // Deal fee double SL(void) const { return this.GetProperty(DEAL_PROP_SL); } // Stop Loss level double TP(void) const { return this.GetProperty(DEAL_PROP_TP); } // Take Profit level //--- String properties string Symbol(void) const { return this.GetProperty(DEAL_PROP_SYMBOL); } // Symbol name string Comment(void) const { return this.GetProperty(DEAL_PROP_COMMENT); } // Comment string ExternalID(void) const { return this.GetProperty(DEAL_PROP_EXTERNAL_ID); } // Deal ID in an external trading system //--- Additional properties double Bid(void) const { return this.m_bid; } // Bid when performing a deal double Ask(void) const { return this.m_ask; } // Ask when performing a deal int Spread(void) const { return (int)this.GetProperty(DEAL_PROP_SPREAD); } // Spread when performing a deal //--- Return the description of a (1) deal type, (2) position change method and (3) deal reason string TypeDescription(void) const; string EntryDescription(void) const; string ReasonDescription(void) const; //--- Return deal description string Description(void); //--- Print deal properties in the journal void Print(void); //--- Compare two objects by the property specified in 'mode' virtual int Compare(const CObject *node, const int mode=0) const; //--- Constructors/destructor CDeal(void){} CDeal(const ulong ticket); ~CDeal(); };

クラスメソッドの実装を見てみましょう。

クラスコンストラクタでは、取引がすでに選択されており、そのプロパティを取得できることを考慮に入れます。

//+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CDeal::CDeal(const ulong ticket) { //--- Store the properties //--- Integer properties this.SetTicket((long)ticket); // Deal ticket this.SetOrder(::HistoryDealGetInteger(ticket, DEAL_ORDER)); // Order this.SetTime((datetime)::HistoryDealGetInteger(ticket, DEAL_TIME)); // Deal execution time this.SetTimeMsc(::HistoryDealGetInteger(ticket, DEAL_TIME_MSC)); // Deal execution time in milliseconds this.SetTypeDeal((ENUM_DEAL_TYPE)::HistoryDealGetInteger(ticket, DEAL_TYPE)); // Type this.SetEntry((ENUM_DEAL_ENTRY)::HistoryDealGetInteger(ticket, DEAL_ENTRY)); // Direction this.SetMagic(::HistoryDealGetInteger(ticket, DEAL_MAGIC)); // Magic number this.SetReason((ENUM_DEAL_REASON)::HistoryDealGetInteger(ticket, DEAL_REASON)); // Deal execution reason or source this.SetPositionID(::HistoryDealGetInteger(ticket, DEAL_POSITION_ID)); // Position ID //--- Real properties this.SetVolume(::HistoryDealGetDouble(ticket, DEAL_VOLUME)); // Volume this.SetPrice(::HistoryDealGetDouble(ticket, DEAL_PRICE)); // Price this.SetCommission(::HistoryDealGetDouble(ticket, DEAL_COMMISSION)); // Commission this.SetSwap(::HistoryDealGetDouble(ticket, DEAL_SWAP)); // Accumulated swap when closing this.SetProfit(::HistoryDealGetDouble(ticket, DEAL_PROFIT)); // Financial result this.SetFee(::HistoryDealGetDouble(ticket, DEAL_FEE)); // Deal fee this.SetSL(::HistoryDealGetDouble(ticket, DEAL_SL)); // Stop Loss level this.SetTP(::HistoryDealGetDouble(ticket, DEAL_TP)); // Take Profit level //--- String properties this.SetSymbol(::HistoryDealGetString(ticket, DEAL_SYMBOL)); // Symbol name this.SetComment(::HistoryDealGetString(ticket, DEAL_COMMENT)); // Comment this.SetExternalID(::HistoryDealGetString(ticket, DEAL_EXTERNAL_ID)); // Deal ID in an external trading system //--- Additional parameters this.m_digits = (int)::SymbolInfoInteger(this.Symbol(), SYMBOL_DIGITS); this.m_point = ::SymbolInfoDouble(this.Symbol(), SYMBOL_POINT); //--- Parameters for calculating spread this.m_bid = 0; this.m_ask = 0; this.SetProperty(DEAL_PROP_SPREAD, 0); //--- If the historical tick and the Point value of the symbol were obtained if(this.GetDealTick() && this.m_point!=0) { //--- set the Bid and Ask price values, calculate and save the spread value this.m_bid=this.m_tick.bid; this.m_ask=this.m_tick.ask; int spread=(int)::fabs((this.m_ask-this.m_bid)/this.m_point); this.SetProperty(DEAL_PROP_SPREAD, spread); } //--- If failed to obtain a historical tick, take the spread value of the minute bar the deal took place on else this.SetProperty(DEAL_PROP_SPREAD, this.GetSpreadM1()); }

計算を実行して取引情報を表示するには、取引プロパティ、および取引が実行された銘柄の数字とポイントをクラスプロパティ配列に保存します。次に、取引時の履歴ティックを取得します。この方法により、取引時のBid価格とAsk価格にアクセスでき、スプレッドを計算できるようになります。

以下は、指定されたプロパティで2つのオブジェクトを比較するメソッドです。

//+------------------------------------------------------------------+ //| Compare two objects by the specified property | //+------------------------------------------------------------------+ int CDeal::Compare(const CObject *node,const int mode=0) const { const CDeal * obj = node; switch(mode) { case DEAL_PROP_TICKET : return(this.Ticket() > obj.Ticket() ? 1 : this.Ticket() < obj.Ticket() ? -1 : 0); case DEAL_PROP_ORDER : return(this.Order() > obj.Order() ? 1 : this.Order() < obj.Order() ? -1 : 0); case DEAL_PROP_TIME : return(this.Time() > obj.Time() ? 1 : this.Time() < obj.Time() ? -1 : 0); case DEAL_PROP_TIME_MSC : return(this.TimeMsc() > obj.TimeMsc() ? 1 : this.TimeMsc() < obj.TimeMsc() ? -1 : 0); case DEAL_PROP_TYPE : return(this.TypeDeal() > obj.TypeDeal() ? 1 : this.TypeDeal() < obj.TypeDeal() ? -1 : 0); case DEAL_PROP_ENTRY : return(this.Entry() > obj.Entry() ? 1 : this.Entry() < obj.Entry() ? -1 : 0); case DEAL_PROP_MAGIC : return(this.Magic() > obj.Magic() ? 1 : this.Magic() < obj.Magic() ? -1 : 0); case DEAL_PROP_REASON : return(this.Reason() > obj.Reason() ? 1 : this.Reason() < obj.Reason() ? -1 : 0); case DEAL_PROP_POSITION_ID : return(this.PositionID() > obj.PositionID() ? 1 : this.PositionID() < obj.PositionID() ? -1 : 0); case DEAL_PROP_SPREAD : return(this.Spread() > obj.Spread() ? 1 : this.Spread() < obj.Spread() ? -1 : 0); case DEAL_PROP_VOLUME : return(this.Volume() > obj.Volume() ? 1 : this.Volume() < obj.Volume() ? -1 : 0); case DEAL_PROP_PRICE : return(this.Price() > obj.Price() ? 1 : this.Price() < obj.Price() ? -1 : 0); case DEAL_PROP_COMMISSION : return(this.Commission() > obj.Commission() ? 1 : this.Commission() < obj.Commission() ? -1 : 0); case DEAL_PROP_SWAP : return(this.Swap() > obj.Swap() ? 1 : this.Swap() < obj.Swap() ? -1 : 0); case DEAL_PROP_PROFIT : return(this.Profit() > obj.Profit() ? 1 : this.Profit() < obj.Profit() ? -1 : 0); case DEAL_PROP_FEE : return(this.Fee() > obj.Fee() ? 1 : this.Fee() < obj.Fee() ? -1 : 0); case DEAL_PROP_SL : return(this.SL() > obj.SL() ? 1 : this.SL() < obj.SL() ? -1 : 0); case DEAL_PROP_TP : return(this.TP() > obj.TP() ? 1 : this.TP() < obj.TP() ? -1 : 0); case DEAL_PROP_SYMBOL : return(this.Symbol() > obj.Symbol() ? 1 : this.Symbol() < obj.Symbol() ? -1 : 0); case DEAL_PROP_COMMENT : return(this.Comment() > obj.Comment() ? 1 : this.Comment() < obj.Comment() ? -1 : 0); case DEAL_PROP_EXTERNAL_ID : return(this.ExternalID() > obj.ExternalID() ? 1 : this.ExternalID() < obj.ExternalID() ? -1 : 0); default : return(-1); } }

これは、CObject親クラス内の同じ名前のメソッドをオーバーライドする仮想メソッドです。比較モード(取引オブジェクトのプロパティの1つ)に応じて、これらのプロパティは現在のオブジェクトと、ポインタによってメソッドに渡されたオブジェクトに対して比較されます。現在のオブジェクトプロパティの値が比較対象オブジェクトの値を超える場合、このメソッドは1を返します。少ない場合は-1になります。値が等しい場合は0となります。

以下は、取引の種類の説明を返すメソッドです。

//+------------------------------------------------------------------+ //| Return the deal type description | //+------------------------------------------------------------------+ string CDeal::TypeDescription(void) const { switch(this.TypeDeal()) { case DEAL_TYPE_BUY : return "Buy"; case DEAL_TYPE_SELL : return "Sell"; case DEAL_TYPE_BALANCE : return "Balance"; case DEAL_TYPE_CREDIT : return "Credit"; case DEAL_TYPE_CHARGE : return "Additional charge"; case DEAL_TYPE_CORRECTION : return "Correction"; case DEAL_TYPE_BONUS : return "Bonus"; case DEAL_TYPE_COMMISSION : return "Additional commission"; case DEAL_TYPE_COMMISSION_DAILY : return "Daily commission"; case DEAL_TYPE_COMMISSION_MONTHLY : return "Monthly commission"; case DEAL_TYPE_COMMISSION_AGENT_DAILY : return "Daily agent commission"; case DEAL_TYPE_COMMISSION_AGENT_MONTHLY: return "Monthly agent commission"; case DEAL_TYPE_INTEREST : return "Interest rate"; case DEAL_TYPE_BUY_CANCELED : return "Canceled buy deal"; case DEAL_TYPE_SELL_CANCELED : return "Canceled sell deal"; case DEAL_DIVIDEND : return "Dividend operations"; case DEAL_DIVIDEND_FRANKED : return "Franked (non-taxable) dividend operations"; case DEAL_TAX : return "Tax charges"; default : return "Unknown: "+(string)this.TypeDeal(); } }

取引の種類に応じて、そのテキストの説明が返されます。このプロジェクトでは、すべてのタイプの取引を使用するのではなく、ポジション(買いまたは売り)に関連する取引のみを使用するため、このメソッドは冗長です。

以下は、ポジション変更メソッドの説明を返すメソッドです。

//+------------------------------------------------------------------+ //| Return position change method | //+------------------------------------------------------------------+ string CDeal::EntryDescription(void) const { switch(this.Entry()) { case DEAL_ENTRY_IN : return "Entry In"; case DEAL_ENTRY_OUT : return "Entry Out"; case DEAL_ENTRY_INOUT : return "Reverse"; case DEAL_ENTRY_OUT_BY : return "Close a position by an opposite one"; default : return "Unknown: "+(string)this.Entry(); } }

以下は、取引理由の説明を返すメソッドです。

//+------------------------------------------------------------------+ //| Return a deal reason description | //+------------------------------------------------------------------+ string CDeal::ReasonDescription(void) const { switch(this.Reason()) { case DEAL_REASON_CLIENT : return "Terminal"; case DEAL_REASON_MOBILE : return "Mobile"; case DEAL_REASON_WEB : return "Web"; case DEAL_REASON_EXPERT : return "EA"; case DEAL_REASON_SL : return "SL"; case DEAL_REASON_TP : return "TP"; case DEAL_REASON_SO : return "SO"; case DEAL_REASON_ROLLOVER : return "Rollover"; case DEAL_REASON_VMARGIN : return "Var. Margin"; case DEAL_REASON_SPLIT : return "Split"; case DEAL_REASON_CORPORATE_ACTION: return "Corp. Action"; default : return "Unknown reason "+(string)this.Reason(); } }

以下は、取引の説明を返すメソッドです。

//+------------------------------------------------------------------+ //| Return deal description | //+------------------------------------------------------------------+ string CDeal::Description(void) { return(::StringFormat("Deal: %-9s %.2f %-4s #%I64d at %s", this.EntryDescription(), this.Volume(), this.TypeDescription(), this.Ticket(), this.TimeMscToString(this.TimeMsc()))); }

以下は、操作ログに取引プロパティを出力するメソッドです。

//+------------------------------------------------------------------+ //| Print deal properties in the journal | //+------------------------------------------------------------------+ void CDeal::Print(void) { ::Print(this.Description()); }

以下は、ミリ秒単位で時間を返すメソッドです。

//+------------------------------------------------------------------+ //| Return time with milliseconds | //+------------------------------------------------------------------+ string CDeal::TimeMscToString(const long time_msc, int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const { return(::TimeToString(time_msc/1000, flags) + "." + ::IntegerToString(time_msc %1000, 3, '0')); }

テキストの説明を返してログに記録するすべてのメソッドは、取引を説明することを目的としています。このプロジェクトでは実際には必要ありませんが、拡張と改善については常に覚えておく必要があります。このようなメソッドがここに存在するのはそのためです。

以下は、取引ティックを受け取るメソッドです。

//+------------------------------------------------------------------+ //| Get the deal tick | //| https://www.mql5.com/ru/forum/42122/page47#comment_37205238 | //+------------------------------------------------------------------+ bool CDeal::GetDealTick(const int amount=20) { MqlTick ticks[]; // We will receive ticks here int attempts = amount; // Number of attempts to get ticks int offset = 500; // Initial time offset for an attempt int copied = 0; // Number of ticks copied //--- Until the tick is copied and the number of copy attempts is over //--- we try to get a tick, doubling the initial time offset at each iteration (expand the "from_msc" time range) while(!::IsStopped() && (copied<=0) && (attempts--)!=0) copied = ::CopyTicksRange(this.Symbol(), ticks, COPY_TICKS_INFO, this.TimeMsc()-(offset <<=1), this.TimeMsc()); //--- If the tick was successfully copied (it is the last one in the tick array), set it to the m_tick variable if(copied>0) this.m_tick=ticks[copied-1]; //--- Return the flag that the tick was copied return(copied>0); }

メソッドのロジックは、コードのコメントで説明されています。ティックを受け取った後、そこからAskおよびBid価格が取得され、スプレッドサイズは(Ask-Bid)/ポイントとして計算されます。

このメソッドを使用してティックを取得できなかった場合は、取引分足のスプレッドを取得するメソッドを使用してスプレッドの平均値を取得します。

//+------------------------------------------------------------------+ //| Gets the spread of the deal minute bar | //+------------------------------------------------------------------+ int CDeal::GetSpreadM1(void) { int array[1]={}; int bar=::iBarShift(this.Symbol(), PERIOD_M1, this.Time()); if(bar==WRONG_VALUE) return 0; return(::CopySpread(this.Symbol(), PERIOD_M1, bar, 1, array)==1 ? array[0] : 0); }

取引クラスの準備ができました。クラスオブジェクトは、履歴ポジションクラスの取引リストに保存され、そこから必要な取引へのポインタを取得してそのデータを処理できるようになります。

履歴ポジションクラス

\MQL5\Services\AccountReporter\で、CPositionクラスの新しいファイルPosition.mqhを作成します。

クラスは標準ライブラリのCObject基本オブジェクトクラスから継承する必要があります。

//+------------------------------------------------------------------+ //| Position.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" //+------------------------------------------------------------------+ //| Position class | //+------------------------------------------------------------------+ class CPosition : public CObject { }

ポジションクラスにはこのポジションのリストが含まれるため、作成されたファイルに取引クラスファイルとCObjectオブジェクトへのポインタの動的配列のクラスファイルを含める必要があります。

//+------------------------------------------------------------------+ //| Position.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include "Deal.mqh" #include <Arrays\ArrayObj.mqh> //+------------------------------------------------------------------+ //| Position class | //+------------------------------------------------------------------+ class CPosition : public CObject { }

ここで、整数、実数、文字列の取引プロパティの列挙を追加し、private、protected、publicのセクションで、クラスメンバー変数とポジションプロパティを処理するためのメソッドを宣言します。

//+------------------------------------------------------------------+ //| Position.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include "Deal.mqh" #include <Arrays\ArrayObj.mqh> //--- Enumeration of integer position properties enum ENUM_POSITION_PROPERTY_INT { POSITION_PROP_TICKET = 0, // Position ticket POSITION_PROP_TIME, // Position open time POSITION_PROP_TIME_MSC, // Position open time in milliseconds POSITION_PROP_TIME_UPDATE, // Position change time POSITION_PROP_TIME_UPDATE_MSC, // Position change time in milliseconds POSITION_PROP_TYPE, // Position type POSITION_PROP_MAGIC, // Position magic number POSITION_PROP_IDENTIFIER, // Position ID POSITION_PROP_REASON, // Position open reason POSITION_PROP_ACCOUNT_LOGIN, // Account number POSITION_PROP_TIME_CLOSE, // Position close time POSITION_PROP_TIME_CLOSE_MSC, // Position close time in milliseconds }; //--- Enumeration of real position properties enum ENUM_POSITION_PROPERTY_DBL { POSITION_PROP_VOLUME = POSITION_PROP_TIME_CLOSE_MSC+1,// Position volume POSITION_PROP_PRICE_OPEN, // Position price POSITION_PROP_SL, // Stop Loss for open position POSITION_PROP_TP, // Take Profit for open position POSITION_PROP_PRICE_CURRENT, // Symbol current price POSITION_PROP_SWAP, // Accumulated swap POSITION_PROP_PROFIT, // Current profit POSITION_PROP_CONTRACT_SIZE, // Symbol trade contract size POSITION_PROP_PRICE_CLOSE, // Position close price POSITION_PROP_COMMISSIONS, // Accumulated commission POSITION_PROP_FEE, // Accumulated payment for deals }; //--- Enumeration of string position properties enum ENUM_POSITION_PROPERTY_STR { POSITION_PROP_SYMBOL = POSITION_PROP_FEE+1,// A symbol the position is open for POSITION_PROP_COMMENT, // Comment to a position POSITION_PROP_EXTERNAL_ID, // Position ID in the external system POSITION_PROP_CURRENCY_PROFIT, // Position symbol profit currency POSITION_PROP_ACCOUNT_CURRENCY, // Account deposit currency POSITION_PROP_ACCOUNT_SERVER, // Server name }; //+------------------------------------------------------------------+ //| Position class | //+------------------------------------------------------------------+ class CPosition : public CObject { private: long m_lprop[POSITION_PROP_TIME_CLOSE_MSC+1]; // Array for storing integer properties double m_dprop[POSITION_PROP_FEE-POSITION_PROP_TIME_CLOSE_MSC]; // Array for storing real properties string m_sprop[POSITION_PROP_ACCOUNT_SERVER-POSITION_PROP_FEE]; // Array for storing string properties //--- Return the index of the array the order's (1) double and (2) string properties are located at int IndexProp(ENUM_POSITION_PROPERTY_DBL property) const { return(int)property-POSITION_PROP_TIME_CLOSE_MSC-1;} int IndexProp(ENUM_POSITION_PROPERTY_STR property) const { return(int)property-POSITION_PROP_FEE-1; } protected: CArrayObj m_list_deals; // List of position deals CDeal m_temp_deal; // Temporary deal object for searching by property in the list //--- Return time with milliseconds string TimeMscToString(const long time_msc,int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const; //--- Additional properties int m_profit_pt; // Profit in points int m_digits; // Symbol digits double m_point; // One symbol point value double m_tick_value; // Calculated tick value //--- Return the pointer to (1) open and (2) close deal CDeal *GetDealIn(void) const; CDeal *GetDealOut(void) const; public: //--- Return the list of deals CArrayObj *GetListDeals(void) { return(&this.m_list_deals); } //--- Set the properties //--- Set (1) integer, (2) real and (3) string properties void SetProperty(ENUM_POSITION_PROPERTY_INT property,long value) { this.m_lprop[property]=value; } void SetProperty(ENUM_POSITION_PROPERTY_DBL property,double value) { this.m_dprop[this.IndexProp(property)]=value; } void SetProperty(ENUM_POSITION_PROPERTY_STR property,string value) { this.m_sprop[this.IndexProp(property)]=value; } //--- Integer properties void SetTicket(const long ticket) { this.SetProperty(POSITION_PROP_TICKET, ticket); } // Position ticket void SetTime(const datetime time) { this.SetProperty(POSITION_PROP_TIME, time); } // Position open time void SetTimeMsc(const long value) { this.SetProperty(POSITION_PROP_TIME_MSC, value); } // Position open time in milliseconds since 01.01.1970 void SetTimeUpdate(const datetime time) { this.SetProperty(POSITION_PROP_TIME_UPDATE, time); } // Position update time void SetTimeUpdateMsc(const long value) { this.SetProperty(POSITION_PROP_TIME_UPDATE_MSC, value); } // Position update time in milliseconds since 01.01.1970 void SetTypePosition(const ENUM_POSITION_TYPE type) { this.SetProperty(POSITION_PROP_TYPE, type); } // Position type void SetMagic(const long magic) { this.SetProperty(POSITION_PROP_MAGIC, magic); } // Magic number for a position (see ORDER_MAGIC) void SetID(const long id) { this.SetProperty(POSITION_PROP_IDENTIFIER, id); } // Position ID void SetReason(const ENUM_POSITION_REASON reason) { this.SetProperty(POSITION_PROP_REASON, reason); } // Position open reason void SetTimeClose(const datetime time) { this.SetProperty(POSITION_PROP_TIME_CLOSE, time); } // Close time void SetTimeCloseMsc(const long value) { this.SetProperty(POSITION_PROP_TIME_CLOSE_MSC, value); } // Close time in milliseconds void SetAccountLogin(const long login) { this.SetProperty(POSITION_PROP_ACCOUNT_LOGIN, login); } // Acount number //--- Real properties void SetVolume(const double volume) { this.SetProperty(POSITION_PROP_VOLUME, volume); } // Position volume void SetPriceOpen(const double price) { this.SetProperty(POSITION_PROP_PRICE_OPEN, price); } // Position price void SetSL(const double value) { this.SetProperty(POSITION_PROP_SL, value); } // Stop Loss level for an open position void SetTP(const double value) { this.SetProperty(POSITION_PROP_TP, value); } // Take Profit level for an open position void SetPriceCurrent(const double price) { this.SetProperty(POSITION_PROP_PRICE_CURRENT, price); } // Current price by symbol void SetSwap(const double value) { this.SetProperty(POSITION_PROP_SWAP, value); } // Accumulated swap void SetProfit(const double value) { this.SetProperty(POSITION_PROP_PROFIT, value); } // Current profit void SetPriceClose(const double price) { this.SetProperty(POSITION_PROP_PRICE_CLOSE, price); } // Close price void SetContractSize(const double value) { this.SetProperty(POSITION_PROP_CONTRACT_SIZE, value); } // Symbol trading contract size void SetCommissions(void); // Total commission of all deals void SetFee(void); // Total deal fee //--- String properties void SetSymbol(const string symbol) { this.SetProperty(POSITION_PROP_SYMBOL, symbol); } // Symbol a position is opened for void SetComment(const string comment) { this.SetProperty(POSITION_PROP_COMMENT, comment); } // Position comment void SetExternalID(const string ext_id) { this.SetProperty(POSITION_PROP_EXTERNAL_ID, ext_id); } // Position ID in an external system (on the exchange) void SetAccountServer(const string server) { this.SetProperty(POSITION_PROP_ACCOUNT_SERVER, server); } // Server name void SetAccountCurrency(const string currency) { this.SetProperty(POSITION_PROP_ACCOUNT_CURRENCY, currency); } // Account deposit currency void SetCurrencyProfit(const string currency) { this.SetProperty(POSITION_PROP_CURRENCY_PROFIT, currency); } // Profit currency of the position symbol //--- Get the properties //--- Return (1) integer, (2) real and (3) string property from the properties array long GetProperty(ENUM_POSITION_PROPERTY_INT property) const { return this.m_lprop[property]; } double GetProperty(ENUM_POSITION_PROPERTY_DBL property) const { return this.m_dprop[this.IndexProp(property)]; } string GetProperty(ENUM_POSITION_PROPERTY_STR property) const { return this.m_sprop[this.IndexProp(property)]; } //--- Integer properties long Ticket(void) const { return this.GetProperty(POSITION_PROP_TICKET); } // Position ticket datetime Time(void) const { return (datetime)this.GetProperty(POSITION_PROP_TIME); } // Position open time long TimeMsc(void) const { return this.GetProperty(POSITION_PROP_TIME_MSC); } // Position open time in milliseconds since 01.01.1970 datetime TimeUpdate(void) const { return (datetime)this.GetProperty(POSITION_PROP_TIME_UPDATE);} // Position change time long TimeUpdateMsc(void) const { return this.GetProperty(POSITION_PROP_TIME_UPDATE_MSC); } // Position update time in milliseconds since 01.01.1970 ENUM_POSITION_TYPE TypePosition(void) const { return (ENUM_POSITION_TYPE)this.GetProperty(POSITION_PROP_TYPE);}// Position type long Magic(void) const { return this.GetProperty(POSITION_PROP_MAGIC); } // Magic number for a position (see ORDER_MAGIC) long ID(void) const { return this.GetProperty(POSITION_PROP_IDENTIFIER); } // Position ID ENUM_POSITION_REASON Reason(void) const { return (ENUM_POSITION_REASON)this.GetProperty(POSITION_PROP_REASON);}// Position opening reason datetime TimeClose(void) const { return (datetime)this.GetProperty(POSITION_PROP_TIME_CLOSE); } // Close time long TimeCloseMsc(void) const { return this.GetProperty(POSITION_PROP_TIME_CLOSE_MSC); } // Close time in milliseconds long AccountLogin(void) const { return this.GetProperty(POSITION_PROP_ACCOUNT_LOGIN); } // Login //--- Real properties double Volume(void) const { return this.GetProperty(POSITION_PROP_VOLUME); } // Position volume double PriceOpen(void) const { return this.GetProperty(POSITION_PROP_PRICE_OPEN); } // Position price double SL(void) const { return this.GetProperty(POSITION_PROP_SL); } // Stop Loss level for an open position double TP(void) const { return this.GetProperty(POSITION_PROP_TP); } // Take Profit level for an open position double PriceCurrent(void) const { return this.GetProperty(POSITION_PROP_PRICE_CURRENT); } // Current price by symbol double Swap(void) const { return this.GetProperty(POSITION_PROP_SWAP); } // Accumulated swap double Profit(void) const { return this.GetProperty(POSITION_PROP_PROFIT); } // Current profit double ContractSize(void) const { return this.GetProperty(POSITION_PROP_CONTRACT_SIZE); } // Symbol trading contract size double PriceClose(void) const { return this.GetProperty(POSITION_PROP_PRICE_CLOSE); } // Close price double Commissions(void) const { return this.GetProperty(POSITION_PROP_COMMISSIONS); } // Total commission of all deals double Fee(void) const { return this.GetProperty(POSITION_PROP_FEE); } // Total deal fee //--- String properties string Symbol(void) const { return this.GetProperty(POSITION_PROP_SYMBOL); } // A symbol position is opened on string Comment(void) const { return this.GetProperty(POSITION_PROP_COMMENT); } // Position comment string ExternalID(void) const { return this.GetProperty(POSITION_PROP_EXTERNAL_ID); } // Position ID in an external system (on the exchange) string AccountServer(void) const { return this.GetProperty(POSITION_PROP_ACCOUNT_SERVER); } // Server name string AccountCurrency(void) const { return this.GetProperty(POSITION_PROP_ACCOUNT_CURRENCY); } // Account deposit currency string CurrencyProfit(void) const { return this.GetProperty(POSITION_PROP_CURRENCY_PROFIT); } // Profit currency of the position symbol //--- Additional properties ulong DealIn(void) const; // Open deal ticket ulong DealOut(void) const; // Close deal ticket int ProfitInPoints(void) const; // Profit in points int SpreadIn(void) const; // Spread when opening int SpreadOut(void) const; // Spread when closing double SpreadOutCost(void) const; // Spread cost when closing double PriceOutAsk(void) const; // Ask price when closing double PriceOutBid(void) const; // Bid price when closing //--- Add a deal to the list of deals, return the pointer CDeal *DealAdd(const long ticket); //--- Return a position type description string TypeDescription(void) const; //--- Return position open time and price description string TimePriceCloseDescription(void); //--- Return position close time and price description string TimePriceOpenDescription(void); //--- Return position description string Description(void); //--- Print the properties of the position and its deals in the journal void Print(void); //--- Compare two objects by the property specified in 'mode' virtual int Compare(const CObject *node, const int mode=0) const; //--- Constructor/destructor CPosition(const long position_id, const string symbol); CPosition(void){} ~CPosition(); };

クラスメソッドの実装を見てみましょう。

クラスコンストラクタのメソッドに渡されるパラメータからポジションIDと銘柄を設定し、口座と銘柄のデータを書き込みます。

//+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CPosition::CPosition(const long position_id, const string symbol) { this.m_list_deals.Sort(DEAL_PROP_TIME_MSC); this.SetID(position_id); this.SetSymbol(symbol); this.SetAccountLogin(::AccountInfoInteger(ACCOUNT_LOGIN)); this.SetAccountServer(::AccountInfoString(ACCOUNT_SERVER)); this.SetAccountCurrency(::AccountInfoString(ACCOUNT_CURRENCY)); this.SetCurrencyProfit(::SymbolInfoString(this.Symbol(),SYMBOL_CURRENCY_PROFIT)); this.SetContractSize(::SymbolInfoDouble(this.Symbol(),SYMBOL_TRADE_CONTRACT_SIZE)); this.m_digits = (int)::SymbolInfoInteger(this.Symbol(),SYMBOL_DIGITS); this.m_point = ::SymbolInfoDouble(this.Symbol(),SYMBOL_POINT); this.m_tick_value = ::SymbolInfoDouble(this.Symbol(), SYMBOL_TRADE_TICK_VALUE); }

クラスのデストラクタで、ポジション取引のリストをクリアします。

//+------------------------------------------------------------------+ //| Destructor | //+------------------------------------------------------------------+ CPosition::~CPosition() { this.m_list_deals.Clear(); }

以下は、指定されたプロパティで2つのオブジェクトを比較するメソッドです。

//+------------------------------------------------------------------+ //| Compare two objects by the specified property | //+------------------------------------------------------------------+ int CPosition::Compare(const CObject *node,const int mode=0) const { const CPosition *obj=node; switch(mode) { case POSITION_PROP_TICKET : return(this.Ticket() > obj.Ticket() ? 1 : this.Ticket() < obj.Ticket() ? -1 : 0); case POSITION_PROP_TIME : return(this.Time() > obj.Time() ? 1 : this.Time() < obj.Time() ? -1 : 0); case POSITION_PROP_TIME_MSC : return(this.TimeMsc() > obj.TimeMsc() ? 1 : this.TimeMsc() < obj.TimeMsc() ? -1 : 0); case POSITION_PROP_TIME_UPDATE : return(this.TimeUpdate() > obj.TimeUpdate() ? 1 : this.TimeUpdate() < obj.TimeUpdate() ? -1 : 0); case POSITION_PROP_TIME_UPDATE_MSC : return(this.TimeUpdateMsc() > obj.TimeUpdateMsc() ? 1 : this.TimeUpdateMsc() < obj.TimeUpdateMsc() ? -1 : 0); case POSITION_PROP_TYPE : return(this.TypePosition() > obj.TypePosition() ? 1 : this.TypePosition() < obj.TypePosition() ? -1 : 0); case POSITION_PROP_MAGIC : return(this.Magic() > obj.Magic() ? 1 : this.Magic() < obj.Magic() ? -1 : 0); case POSITION_PROP_IDENTIFIER : return(this.ID() > obj.ID() ? 1 : this.ID() < obj.ID() ? -1 : 0); case POSITION_PROP_REASON : return(this.Reason() > obj.Reason() ? 1 : this.Reason() < obj.Reason() ? -1 : 0); case POSITION_PROP_ACCOUNT_LOGIN : return(this.AccountLogin() > obj.AccountLogin() ? 1 : this.AccountLogin() < obj.AccountLogin() ? -1 : 0); case POSITION_PROP_TIME_CLOSE : return(this.TimeClose() > obj.TimeClose() ? 1 : this.TimeClose() < obj.TimeClose() ? -1 : 0); case POSITION_PROP_TIME_CLOSE_MSC : return(this.TimeCloseMsc() > obj.TimeCloseMsc() ? 1 : this.TimeCloseMsc() < obj.TimeCloseMsc() ? -1 : 0); case POSITION_PROP_VOLUME : return(this.Volume() > obj.Volume() ? 1 : this.Volume() < obj.Volume() ? -1 : 0); case POSITION_PROP_PRICE_OPEN : return(this.PriceOpen() > obj.PriceOpen() ? 1 : this.PriceOpen() < obj.PriceOpen() ? -1 : 0); case POSITION_PROP_SL : return(this.SL() > obj.SL() ? 1 : this.SL() < obj.SL() ? -1 : 0); case POSITION_PROP_TP : return(this.TP() > obj.TP() ? 1 : this.TP() < obj.TP() ? -1 : 0); case POSITION_PROP_PRICE_CURRENT : return(this.PriceCurrent() > obj.PriceCurrent() ? 1 : this.PriceCurrent() < obj.PriceCurrent() ? -1 : 0); case POSITION_PROP_SWAP : return(this.Swap() > obj.Swap() ? 1 : this.Swap() < obj.Swap() ? -1 : 0); case POSITION_PROP_PROFIT : return(this.Profit() > obj.Profit() ? 1 : this.Profit() < obj.Profit() ? -1 : 0); case POSITION_PROP_CONTRACT_SIZE : return(this.ContractSize() > obj.ContractSize() ? 1 : this.ContractSize() < obj.ContractSize() ? -1 : 0); case POSITION_PROP_PRICE_CLOSE : return(this.PriceClose() > obj.PriceClose() ? 1 : this.PriceClose() < obj.PriceClose() ? -1 : 0); case POSITION_PROP_COMMISSIONS : return(this.Commissions() > obj.Commissions() ? 1 : this.Commissions() < obj.Commissions() ? -1 : 0); case POSITION_PROP_FEE : return(this.Fee() > obj.Fee() ? 1 : this.Fee() < obj.Fee() ? -1 : 0); case POSITION_PROP_SYMBOL : return(this.Symbol() > obj.Symbol() ? 1 : this.Symbol() < obj.Symbol() ? -1 : 0); case POSITION_PROP_COMMENT : return(this.Comment() > obj.Comment() ? 1 : this.Comment() < obj.Comment() ? -1 : 0); case POSITION_PROP_EXTERNAL_ID : return(this.ExternalID() > obj.ExternalID() ? 1 : this.ExternalID() < obj.ExternalID() ? -1 : 0); case POSITION_PROP_CURRENCY_PROFIT : return(this.CurrencyProfit() > obj.CurrencyProfit() ? 1 : this.CurrencyProfit() < obj.CurrencyProfit() ? -1 : 0); case POSITION_PROP_ACCOUNT_CURRENCY : return(this.AccountCurrency() > obj.AccountCurrency() ? 1 : this.AccountCurrency() < obj.AccountCurrency() ? -1 : 0); case POSITION_PROP_ACCOUNT_SERVER : return(this.AccountServer() > obj.AccountServer() ? 1 : this.AccountServer() < obj.AccountServer() ? -1 : 0); default : return -1; } }

これは、CObject親クラス内の同じ名前のメソッドをオーバーライドする仮想メソッドです。比較モード(ポジションオブジェクトのプロパティの1つ)に応じて、これらのプロパティは現在のオブジェクトと、ポインタによってメソッドに渡されたオブジェクトに対して比較されます。現在のオブジェクトプロパティの値が比較対象オブジェクトの値を超える場合、このメソッドは1を返します。少ない場合は-1になります。値が等しい場合は0となります。

以下は、ミリ秒単位で時間を返すメソッドです。

//+------------------------------------------------------------------+ //| Return time with milliseconds | //+------------------------------------------------------------------+ string CPosition::TimeMscToString(const long time_msc, int flags=TIME_DATE|TIME_MINUTES|TIME_SECONDS) const { return(::TimeToString(time_msc/1000, flags) + "." + ::IntegerToString(time_msc %1000, 3, '0')); }

以下は、市場エントリー取引へのポインタを返すメソッドです。

//+------------------------------------------------------------------+ //| Return the pointer to the opening deal | //+------------------------------------------------------------------+ CDeal *CPosition::GetDealIn(void) const { int total=this.m_list_deals.Total(); for(int i=0; i<total; i++) { CDeal *deal=this.m_list_deals.At(i); if(deal==NULL) continue; if(deal.Entry()==DEAL_ENTRY_IN) return deal; } return NULL; }

ポジション取引のリストを介したループで、DEAL_ENTRY_IN(市場参入)ポジション変更メソッドを使用して取引を探し、見つかった取引へのポインタを返します。

以下は、市場決済取引へのポインタを返すメソッドです。

//+------------------------------------------------------------------+ //| Return the pointer to the close deal | //+------------------------------------------------------------------+ CDeal *CPosition::GetDealOut(void) const { for(int i=this.m_list_deals.Total()-1; i>=0; i--) { CDeal *deal=this.m_list_deals.At(i); if(deal==NULL) continue; if(deal.Entry()==DEAL_ENTRY_OUT || deal.Entry()==DEAL_ENTRY_OUT_BY) return deal; } return NULL; }

ポジション取引のリストを介したループでは、DEAL_ENTRY_OUT(市場終了)またはDEAL_ENTRY_OUT_BY(クローズバイ)ポジション変更メソッドを使用して取引を探し、見つかった取引へのポインタを返します。

以下は、市場エントリー取引のチケットを返すメソッドです。

//+------------------------------------------------------------------+ //| Return the open deal ticket | //+------------------------------------------------------------------+ ulong CPosition::DealIn(void) const { CDeal *deal=this.GetDealIn(); return(deal!=NULL ? deal.Ticket() : 0); }

市場エントリー取引へのポインタを取得し、そのチケットを返します。

以下は、市場決済取引のチケットを返すメソッドです。

//+------------------------------------------------------------------+ //| Return the close deal ticket | //+------------------------------------------------------------------+ ulong CPosition::DealOut(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Ticket() : 0); }

市場決済取引へのポインタを取得し、そのチケットを返します。

以下は、エントリー時にスプレッドを返すメソッドです。

//+------------------------------------------------------------------+ //| Return spread when opening | //+------------------------------------------------------------------+ int CPosition::SpreadIn(void) const { CDeal *deal=this.GetDealIn(); return(deal!=NULL ? deal.Spread() : 0); }

市場エントリー取引へのポインタを取得し、取引に設定されたスプレッドを返します。

以下は、クローズ時にスプレッドを返すメソッドです。

//+------------------------------------------------------------------+ //| Return spread when closing | //+------------------------------------------------------------------+ int CPosition::SpreadOut(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Spread() : 0); }

市場決済取引へのポインタを取得し、取引で設定されたスプレッドを返します。

以下は、クローズ時にAsk価格を返すメソッドです。

//+------------------------------------------------------------------+ //| Return Ask price when closing | //+------------------------------------------------------------------+ double CPosition::PriceOutAsk(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Ask() : 0); }

市場決済取引へのポインタを取得し、取引で設定された売り価格の値を返します。

以下は、クローズ時にBid価格を返すメソッドです。

//+------------------------------------------------------------------+ //| Return the Bid price when closing | //+------------------------------------------------------------------+ double CPosition::PriceOutBid(void) const { CDeal *deal=this.GetDealOut(); return(deal!=NULL ? deal.Bid() : 0); }

市場決済取引へのポインタを取得し、取引に設定された入札価格の値を返します。

以下は、ポイント単位の利益を返すメソッドです。

//+------------------------------------------------------------------+ //| Return a profit in points | //+------------------------------------------------------------------+ int CPosition::ProfitInPoints(void) const { //--- If symbol Point has not been received previously, inform of that and return 0 if(this.m_point==0) { ::Print("The Point() value could not be retrieved."); return 0; } //--- Get position open and close prices double open =this.PriceOpen(); double close=this.PriceClose(); //--- If failed to get the prices, return 0 if(open==0 || close==0) return 0; //--- Depending on the position type, return the calculated value of the position profit in points return (int)::round(this.TypePosition()==POSITION_TYPE_BUY ? (close-open)/this.m_point : (open-close)/this.m_point); }

以下は、クローズ時にスプレッドを返すメソッドです。

//+------------------------------------------------------------------+ //| Return the spread value when closing | //+------------------------------------------------------------------+ double CPosition::SpreadOutCost(void) const { //--- Get close deal CDeal *deal=this.GetDealOut(); if(deal==NULL) return 0; //--- Get position profit and position profit in points double profit=this.Profit(); int profit_pt=this.ProfitInPoints(); //--- If the profit is zero, return the spread value using the TickValue * Spread * Lots equation if(profit==0) return(this.m_tick_value * deal.Spread() * deal.Volume()); //--- Calculate and return the spread value (proportion) return(profit_pt>0 ? deal.Spread() * ::fabs(profit / profit_pt) : 0); }

このメソッドでは、スプレッド値を計算するために2つの方法が使用されます。

- ポジション利益がゼロでない場合、スプレッドのコストは、スプレッドサイズ(ポイント)×ポジション利益(金額)/ポジション利益(ポイント)の割合で計算されます。

- ポジション利益がゼロの場合、スプレッド値は「計算されたティック値*ポイントでのスプレッドサイズ*取引量」を使用して計算されます。

以下は、すべての取引の合計手数料を設定するメソッドです。

//+------------------------------------------------------------------+ //| Set the total commission for all deals | //+------------------------------------------------------------------+ void CPosition::SetCommissions(void) { double res=0; int total=this.m_list_deals.Total(); for(int i=0; i<total; i++) { CDeal *deal=this.m_list_deals.At(i); res+=(deal!=NULL ? deal.Commission() : 0); } this.SetProperty(POSITION_PROP_COMMISSIONS, res); }

ポジションの全期間にかかる手数料を決定するには、ポジション内のすべての取引の手数料を合計する必要があります。ポジション取引のリストをループして、各取引の手数料を結果の値に追加します。この値は最終的にメソッドから返されます。

以下は、総取引手数料を設定するメソッドです。

//+------------------------------------------------------------------+ //| Sets the total deal fee | //+------------------------------------------------------------------+ void CPosition::SetFee(void) { double res=0; int total=this.m_list_deals.Total(); for(int i=0; i<total; i++) { CDeal *deal=this.m_list_deals.At(i); res+=(deal!=NULL ? deal.Fee() : 0); } this.SetProperty(POSITION_PROP_FEE, res); }

ここではすべてが前の方法とまったく同じで、各ポジション取引の手数料の合計を返します。

これらのメソッドは両方とも、ポジションの取引がすべてリストされているときに呼び出す必要があります。そうしないと、結果が不完全になります。

以下は、ポジション取引のリストに取引を追加するメソッドです。

//+------------------------------------------------------------------+ //| Add a deal to the list of deals | //+------------------------------------------------------------------+ CDeal *CPosition::DealAdd(const long ticket) { //--- A temporary object gets a ticket of the desired deal and the flag of sorting the list of deals by ticket this.m_temp_deal.SetTicket(ticket); this.m_list_deals.Sort(DEAL_PROP_TICKET); //--- Set the result of checking if a deal with such a ticket is present in the list bool exist=(this.m_list_deals.Search(&this.m_temp_deal)!=WRONG_VALUE); //--- Return sorting by time in milliseconds for the list this.m_list_deals.Sort(DEAL_PROP_TIME_MSC); //--- If a deal with such a ticket is already in the list, return NULL if(exist) return NULL; //--- Create a new deal object CDeal *deal=new CDeal(ticket); if(deal==NULL) return NULL; //--- Add the created object to the list in sorting order by time in milliseconds //--- If failed to add the deal to the list, remove the the deal object and return NULL if(!this.m_list_deals.InsertSort(deal)) { delete deal; return NULL; } //--- If this is a position closing deal, set the profit from the deal properties to the position profit value if(deal.Entry()==DEAL_ENTRY_OUT || deal.Entry()==DEAL_ENTRY_OUT_BY) { this.SetProfit(deal.Profit()); this.SetSwap(deal.Swap()); } //--- Return the pointer to the created deal object return deal; }

メソッドのロジックはコードのコメントで完全に説明されています。このメソッドは、現在選択されている取引のチケットを受け取ります。リスト内にそのようなチケットを含む取引がまだない場合は、新しい取引オブジェクトが作成され、ポジション取引のリストに追加されます。

以下は、いくつかのポジションプロパティの説明を返すメソッドです。

//+------------------------------------------------------------------+ //| Return a position type description | //+------------------------------------------------------------------+ string CPosition::TypeDescription(void) const { return(this.TypePosition()==POSITION_TYPE_BUY ? "Buy" : this.TypePosition()==POSITION_TYPE_SELL ? "Sell" : "Unknown::"+(string)this.TypePosition()); } //+------------------------------------------------------------------+ //| Return position open time and price description | //+------------------------------------------------------------------+ string CPosition::TimePriceOpenDescription(void) { return(::StringFormat("Opened %s [%.*f]", this.TimeMscToString(this.TimeMsc()),this.m_digits, this.PriceOpen())); } //+------------------------------------------------------------------+ //| Return position close time and price description | //+------------------------------------------------------------------+ string CPosition::TimePriceCloseDescription(void) { if(this.TimeCloseMsc()==0) return "Not closed yet"; return(::StringFormat("Closed %s [%.*f]", this.TimeMscToString(this.TimeCloseMsc()),this.m_digits, this.PriceClose())); } //+------------------------------------------------------------------+ //| Return a brief position description | //+------------------------------------------------------------------+ string CPosition::Description(void) { return(::StringFormat("%I64d (%s): %s %.2f %s #%I64d, Magic %I64d", this.AccountLogin(), this.AccountServer(), this.Symbol(), this.Volume(), this.TypeDescription(), this.ID(), this.Magic())); }

これらのメソッドは、たとえば、操作ログに役職の説明を表示するために使用されます。

Printメソッドを使用すると、操作ログにポジションの説明を表示できます。

//+------------------------------------------------------------------+ //| Print the position properties and deals in the journal | //+------------------------------------------------------------------+ void CPosition::Print(void) { ::PrintFormat("%s\n-%s\n-%s", this.Description(), this.TimePriceOpenDescription(), this.TimePriceCloseDescription()); for(int i=0; i<this.m_list_deals.Total(); i++) { CDeal *deal=this.m_list_deals.At(i); if(deal==NULL) continue; deal.Print(); } }

まず、ポジションの説明を含むヘッダーが印刷されます。次に、すべてのポジション取引をループし、Print()メソッドを使用して各取引の説明が印刷されます。

履歴ポジションクラスの準備が完了しました。次に、取引とポジションをプロパティ別に選択、検索、並べ替えるための静的クラスを作成しましょう。

取引とポジションのプロパティで検索および並べ替えをおこなうクラス

このクラスは「MetaTraderプログラムを簡単かつ迅速に開発するためのライブラリ(第3部):成行注文と取引のコレクション、検索と並び替え」稿で徹底的に検討されました(検索配置セクション)。

\MQL5\Services\AccountReporter\で、CSelectクラスの新しいファイルSelect.mqhを作成します。

//+------------------------------------------------------------------+ //| Select.mqh | //| Copyright 2024, MetaQuotes Software Corp. | //| https://mql5.com/ja/users/artmedia70 | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Software Corp." #property link "https://mql5.com/ja/users/artmedia70" #property version "1.00" //+------------------------------------------------------------------+ //| Class for sorting objects meeting the criterion | //+------------------------------------------------------------------+ class CSelect { }

比較モードの列挙を設定し、取引クラスとポジションクラスのファイルをインクルードし、ストレージリストを宣言します。

//+------------------------------------------------------------------+ //| Select.mqh | //| Copyright 2024, MetaQuotes Software Corp. | //| https://mql5.com/ja/users/artmedia70 | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Software Corp." #property link "https://mql5.com/ja/users/artmedia70" #property version "1.00" enum ENUM_COMPARER_TYPE { EQUAL, // Equal MORE, // More LESS, // Less NO_EQUAL, // Not equal EQUAL_OR_MORE, // Equal or more EQUAL_OR_LESS // Equal or less }; //+------------------------------------------------------------------+ //| Include files | //+------------------------------------------------------------------+ #include "Deal.mqh" #include "Position.mqh" //+------------------------------------------------------------------+ //| Storage list | //+------------------------------------------------------------------+ CArrayObj ListStorage; // Storage object for storing sorted collection lists //+------------------------------------------------------------------+ //| Class for sorting objects meeting the criterion | //+------------------------------------------------------------------+ class CSelect { }

オブジェクトを選択し、検索条件を満たすリストを作成するためのすべてのメソッドを記述します。

//+------------------------------------------------------------------+ //| Select.mqh | //| Copyright 2024, MetaQuotes Software Corp. | //| https://mql5.com/ja/users/artmedia70 | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Software Corp." #property link "https://mql5.com/ja/users/artmedia70" #property version "1.00" enum ENUM_COMPARER_TYPE // Comparison modes { EQUAL, // Equal MORE, // More LESS, // Less NO_EQUAL, // Not equal EQUAL_OR_MORE, // Equal or more EQUAL_OR_LESS // Equal or less }; //+------------------------------------------------------------------+ //| Include files | //+------------------------------------------------------------------+ #include "Deal.mqh" #include "Position.mqh" //+------------------------------------------------------------------+ //| Storage list | //+------------------------------------------------------------------+ CArrayObj ListStorage; // Storage object for storing sorted collection lists //+------------------------------------------------------------------+ //| Class for sorting objects meeting the criterion | //+------------------------------------------------------------------+ class CSelect { private: //--- Method for comparing two values template<typename T> static bool CompareValues(T value1,T value2,ENUM_COMPARER_TYPE mode); public: //+------------------------------------------------------------------+ //| Deal handling methods | //+------------------------------------------------------------------+ //--- Return the list of deals with one out of (1) integer, (2) real and (3) string properties meeting a specified criterion static CArrayObj *ByDealProperty(CArrayObj *list_source,ENUM_DEAL_PROPERTY_INT property,long value,ENUM_COMPARER_TYPE mode); static CArrayObj *ByDealProperty(CArrayObj *list_source,ENUM_DEAL_PROPERTY_DBL property,double value,ENUM_COMPARER_TYPE mode); static CArrayObj *ByDealProperty(CArrayObj *list_source,ENUM_DEAL_PROPERTY_STR property,string value,ENUM_COMPARER_TYPE mode); //--- Return the deal index with the maximum value of the (1) integer, (2) real and (3) string properties static int FindDealMax(CArrayObj *list_source,ENUM_DEAL_PROPERTY_INT property); static int FindDealMax(CArrayObj *list_source,ENUM_DEAL_PROPERTY_DBL property); static int FindDealMax(CArrayObj *list_source,ENUM_DEAL_PROPERTY_STR property); //--- Return the deal index with the minimum value of the (1) integer, (2) real and (3) string properties static int FindDealMin(CArrayObj *list_source,ENUM_DEAL_PROPERTY_INT property); static int FindDealMin(CArrayObj *list_source,ENUM_DEAL_PROPERTY_DBL property); static int FindDealMin(CArrayObj *list_source,ENUM_DEAL_PROPERTY_STR property); //+------------------------------------------------------------------+ //| Position handling methods | //+------------------------------------------------------------------+ //--- Return the list of positions with one out of (1) integer, (2) real and (3) string properties meeting a specified criterion static CArrayObj *ByPositionProperty(CArrayObj *list_source,ENUM_POSITION_PROPERTY_INT property,long value,ENUM_COMPARER_TYPE mode); static CArrayObj *ByPositionProperty(CArrayObj *list_source,ENUM_POSITION_PROPERTY_DBL property,double value,ENUM_COMPARER_TYPE mode); static CArrayObj *ByPositionProperty(CArrayObj *list_source,ENUM_POSITION_PROPERTY_STR property,string value,ENUM_COMPARER_TYPE mode); //--- Return the position index with the maximum value of the (1) integer, (2) real and (3) string properties static int FindPositionMax(CArrayObj *list_source,ENUM_POSITION_PROPERTY_INT property); static int FindPositionMax(CArrayObj *list_source,ENUM_POSITION_PROPERTY_DBL property); static int FindPositionMax(CArrayObj *list_source,ENUM_POSITION_PROPERTY_STR property); //--- Return the position index with the minimum value of the (1) integer, (2) real and (3) string properties static int FindPositionMin(CArrayObj *list_source,ENUM_POSITION_PROPERTY_INT property); static int FindPositionMin(CArrayObj *list_source,ENUM_POSITION_PROPERTY_DBL property); static int FindPositionMin(CArrayObj *list_source,ENUM_POSITION_PROPERTY_STR property); }; //+------------------------------------------------------------------+ //| Method for comparing two values | //+------------------------------------------------------------------+ template<typename T> bool CSelect::CompareValues(T value1,T value2,ENUM_COMPARER_TYPE mode) { switch(mode) { case EQUAL : return(value1==value2 ? true : false); case NO_EQUAL : return(value1!=value2 ? true : false); case MORE : return(value1>value2 ? true : false); case LESS : return(value1<value2 ? true : false); case EQUAL_OR_MORE : return(value1>=value2 ? true : false); case EQUAL_OR_LESS : return(value1<=value2 ? true : false); default : return false; } } //+------------------------------------------------------------------+ //| Deal list handling methods | //+------------------------------------------------------------------+ //+------------------------------------------------------------------+ //| Return the list of deals with one integer | //| property meeting the specified criterion | //+------------------------------------------------------------------+ CArrayObj *CSelect::ByDealProperty(CArrayObj *list_source,ENUM_DEAL_PROPERTY_INT property,long value,ENUM_COMPARER_TYPE mode) { if(list_source==NULL) return NULL; CArrayObj *list=new CArrayObj(); if(list==NULL) return NULL; list.FreeMode(false); if(!ListStorage.Add(list)) { delete list; return NULL; } int total=list_source.Total(); for(int i=0; i<total; i++) { CDeal *obj=list_source.At(i); long obj_prop=obj.GetProperty(property); if(CompareValues(obj_prop, value, mode)) list.Add(obj); } return list; } //+------------------------------------------------------------------+ //| Return the list of deals with one real | //| property meeting the specified criterion | //+------------------------------------------------------------------+ CArrayObj *CSelect::ByDealProperty(CArrayObj *list_source,ENUM_DEAL_PROPERTY_DBL property,double value,ENUM_COMPARER_TYPE mode) { if(list_source==NULL) return NULL; CArrayObj *list=new CArrayObj(); if(list==NULL) return NULL; list.FreeMode(false); if(!ListStorage.Add(list)) { delete list; return NULL; } for(int i=0; i<list_source.Total(); i++) { CDeal *obj=list_source.At(i); double obj_prop=obj.GetProperty(property); if(CompareValues(obj_prop,value,mode)) list.Add(obj); } return list; } //+------------------------------------------------------------------+ //| Return the list of deals with one string | //| property meeting the specified criterion | //+------------------------------------------------------------------+ CArrayObj *CSelect::ByDealProperty(CArrayObj *list_source,ENUM_DEAL_PROPERTY_STR property,string value,ENUM_COMPARER_TYPE mode) { if(list_source==NULL) return NULL; CArrayObj *list=new CArrayObj(); if(list==NULL) return NULL; list.FreeMode(false); if(!ListStorage.Add(list)) { delete list; return NULL; } for(int i=0; i<list_source.Total(); i++) { CDeal *obj=list_source.At(i); string obj_prop=obj.GetProperty(property); if(CompareValues(obj_prop,value,mode)) list.Add(obj); } return list; } //+------------------------------------------------------------------+ //| Return the deal index in the list | //| with the maximum integer property value | //+------------------------------------------------------------------+ int CSelect::FindDealMax(CArrayObj *list_source,ENUM_DEAL_PROPERTY_INT property) { if(list_source==NULL) return WRONG_VALUE; int index=0; CDeal *max_obj=NULL; int total=list_source.Total(); if(total==0) return WRONG_VALUE; for(int i=1; i<total; i++) { CDeal *obj=list_source.At(i); long obj1_prop=obj.GetProperty(property); max_obj=list_source.At(index); long obj2_prop=max_obj.GetProperty(property); if(CompareValues(obj1_prop,obj2_prop,MORE)) index=i; } return index; } //+------------------------------------------------------------------+ //| Return the deal index in the list | //| with the maximum real property value | //+------------------------------------------------------------------+ int CSelect::FindDealMax(CArrayObj *list_source,ENUM_DEAL_PROPERTY_DBL property) { if(list_source==NULL) return WRONG_VALUE; int index=0; CDeal *max_obj=NULL; int total=list_source.Total(); if(total==0) return WRONG_VALUE; for(int i=1; i<total; i++) { CDeal *obj=list_source.At(i); double obj1_prop=obj.GetProperty(property); max_obj=list_source.At(index); double obj2_prop=max_obj.GetProperty(property); if(CompareValues(obj1_prop,obj2_prop,MORE)) index=i; } return index; } //+------------------------------------------------------------------+ //| Return the deal index in the list | //| with the maximum string property value | //+------------------------------------------------------------------+ int CSelect::FindDealMax(CArrayObj *list_source,ENUM_DEAL_PROPERTY_STR property) { if(list_source==NULL) return WRONG_VALUE; int index=0; CDeal *max_obj=NULL; int total=list_source.Total(); if(total==0) return WRONG_VALUE; for(int i=1; i<total; i++) { CDeal *obj=list_source.At(i); string obj1_prop=obj.GetProperty(property); max_obj=list_source.At(index); string obj2_prop=max_obj.GetProperty(property); if(CompareValues(obj1_prop,obj2_prop,MORE)) index=i; } return index; } //+------------------------------------------------------------------+ //| Return the deal index in the list | //| with the minimum integer property value | //+------------------------------------------------------------------+ int CSelect::FindDealMin(CArrayObj* list_source,ENUM_DEAL_PROPERTY_INT property) { int index=0; CDeal *min_obj=NULL; int total=list_source.Total(); if(total==0) return WRONG_VALUE; for(int i=1; i<total; i++) { CDeal *obj=list_source.At(i); long obj1_prop=obj.GetProperty(property); min_obj=list_source.At(index); long obj2_prop=min_obj.GetProperty(property); if(CompareValues(obj1_prop,obj2_prop,LESS)) index=i; } return index; } //+------------------------------------------------------------------+ //| Return the deal index in the list | //| with the minimum real property value | //+------------------------------------------------------------------+ int CSelect::FindDealMin(CArrayObj* list_source,ENUM_DEAL_PROPERTY_DBL property) { int index=0; CDeal *min_obj=NULL; int total=list_source.Total(); if(total==0) return WRONG_VALUE; for(int i=1; i<total; i++) { CDeal *obj=list_source.At(i); double obj1_prop=obj.GetProperty(property); min_obj=list_source.At(index); double obj2_prop=min_obj.GetProperty(property); if(CompareValues(obj1_prop,obj2_prop,LESS)) index=i; } return index; } //+------------------------------------------------------------------+ //| Return the deal index in the list | //| with the minimum string property value | //+------------------------------------------------------------------+ int CSelect::FindDealMin(CArrayObj* list_source,ENUM_DEAL_PROPERTY_STR property) { int index=0; CDeal *min_obj=NULL; int total=list_source.Total(); if(total==0) return WRONG_VALUE; for(int i=1; i<total; i++) { CDeal *obj=list_source.At(i); string obj1_prop=obj.GetProperty(property); min_obj=list_source.At(index); string obj2_prop=min_obj.GetProperty(property); if(CompareValues(obj1_prop,obj2_prop,LESS)) index=i; } return index; } //+------------------------------------------------------------------+ //| Position list handling method | //+------------------------------------------------------------------+ //+------------------------------------------------------------------+ //| Return the list of positions with one integer | //| property meeting the specified criterion | //+------------------------------------------------------------------+ CArrayObj *CSelect::ByPositionProperty(CArrayObj *list_source,ENUM_POSITION_PROPERTY_INT property,long value,ENUM_COMPARER_TYPE mode) { if(list_source==NULL) return NULL; CArrayObj *list=new CArrayObj(); if(list==NULL) return NULL; list.FreeMode(false); if(!ListStorage.Add(list)) { delete list; return NULL; } int total=list_source.Total(); for(int i=0; i<total; i++) { CPosition *obj=list_source.At(i); long obj_prop=obj.GetProperty(property); if(CompareValues(obj_prop, value, mode)) list.Add(obj); } return list; } //+------------------------------------------------------------------+ //| Return the list of positions with one real | //| property meeting the specified criterion | //+------------------------------------------------------------------+ CArrayObj *CSelect::ByPositionProperty(CArrayObj *list_source,ENUM_POSITION_PROPERTY_DBL property,double value,ENUM_COMPARER_TYPE mode) { if(list_source==NULL) return NULL; CArrayObj *list=new CArrayObj(); if(list==NULL) return NULL; list.FreeMode(false); if(!ListStorage.Add(list)) { delete list; return NULL; } for(int i=0; i<list_source.Total(); i++) { CPosition *obj=list_source.At(i); double obj_prop=obj.GetProperty(property); if(CompareValues(obj_prop,value,mode)) list.Add(obj); } return list; } //+------------------------------------------------------------------+ //| Return the list of positions with one string | //| property meeting the specified criterion | //+------------------------------------------------------------------+ CArrayObj *CSelect::ByPositionProperty(CArrayObj *list_source,ENUM_POSITION_PROPERTY_STR property,string value,ENUM_COMPARER_TYPE mode) { if(list_source==NULL) return NULL; CArrayObj *list=new CArrayObj(); if(list==NULL) return NULL; list.FreeMode(false); if(!ListStorage.Add(list)) { delete list; return NULL; } for(int i=0; i<list_source.Total(); i++) { CPosition *obj=list_source.At(i); string obj_prop=obj.GetProperty(property); if(CompareValues(obj_prop,value,mode)) list.Add(obj); } return list; } //+------------------------------------------------------------------+ //| Return the position index in the list | //| with the maximum integer property value | //+------------------------------------------------------------------+ int CSelect::FindPositionMax(CArrayObj *list_source,ENUM_POSITION_PROPERTY_INT property) { if(list_source==NULL) return WRONG_VALUE; int index=0; CPosition *max_obj=NULL; int total=list_source.Total(); if(total==0) return WRONG_VALUE; for(int i=1; i<total; i++) { CPosition *obj=list_source.At(i); long obj1_prop=obj.GetProperty(property); max_obj=list_source.At(index); long obj2_prop=max_obj.GetProperty(property); if(CompareValues(obj1_prop,obj2_prop,MORE)) index=i; } return index; } //+------------------------------------------------------------------+ //| Return the position index in the list | //| with the maximum real property value | //+------------------------------------------------------------------+ int CSelect::FindPositionMax(CArrayObj *list_source,ENUM_POSITION_PROPERTY_DBL property) { if(list_source==NULL) return WRONG_VALUE; int index=0; CPosition *max_obj=NULL; int total=list_source.Total(); if(total==0) return WRONG_VALUE; for(int i=1; i<total; i++) { CPosition *obj=list_source.At(i); double obj1_prop=obj.GetProperty(property); max_obj=list_source.At(index); double obj2_prop=max_obj.GetProperty(property); if(CompareValues(obj1_prop,obj2_prop,MORE)) index=i; } return index; } //+------------------------------------------------------------------+ //| Return the position index in the list | //| with the maximum string property value | //+------------------------------------------------------------------+ int CSelect::FindPositionMax(CArrayObj *list_source,ENUM_POSITION_PROPERTY_STR property) { if(list_source==NULL) return WRONG_VALUE; int index=0; CPosition *max_obj=NULL; int total=list_source.Total(); if(total==0) return WRONG_VALUE; for(int i=1; i<total; i++) { CPosition *obj=list_source.At(i); string obj1_prop=obj.GetProperty(property); max_obj=list_source.At(index); string obj2_prop=max_obj.GetProperty(property); if(CompareValues(obj1_prop,obj2_prop,MORE)) index=i; } return index; } //+------------------------------------------------------------------+ //| Return the position index in the list | //| with the minimum integer property value | //+------------------------------------------------------------------+ int CSelect::FindPositionMin(CArrayObj* list_source,ENUM_POSITION_PROPERTY_INT property) { int index=0; CPosition *min_obj=NULL; int total=list_source.Total(); if(total==0) return WRONG_VALUE; for(int i=1; i<total; i++) { CPosition *obj=list_source.At(i); long obj1_prop=obj.GetProperty(property); min_obj=list_source.At(index); long obj2_prop=min_obj.GetProperty(property); if(CompareValues(obj1_prop,obj2_prop,LESS)) index=i; } return index; } //+------------------------------------------------------------------+ //| Return the position index in the list | //| with the minimum real property value | //+------------------------------------------------------------------+ int CSelect::FindPositionMin(CArrayObj* list_source,ENUM_POSITION_PROPERTY_DBL property) { int index=0; CPosition *min_obj=NULL; int total=list_source.Total(); if(total==0) return WRONG_VALUE; for(int i=1; i<total; i++) { CPosition *obj=list_source.At(i); double obj1_prop=obj.GetProperty(property); min_obj=list_source.At(index); double obj2_prop=min_obj.GetProperty(property); if(CompareValues(obj1_prop,obj2_prop,LESS)) index=i; } return index; } //+------------------------------------------------------------------+ //| Return the position index in the list | //| with the minimum string property value | //+------------------------------------------------------------------+ int CSelect::FindPositionMin(CArrayObj* list_source,ENUM_POSITION_PROPERTY_STR property) { int index=0; CPosition *min_obj=NULL; int total=list_source.Total(); if(total==0) return WRONG_VALUE; for(int i=1; i<total; i++) { CPosition *obj=list_source.At(i); string obj1_prop=obj.GetProperty(property); min_obj=list_source.At(index); string obj2_prop=min_obj.GetProperty(property); if(CompareValues(obj1_prop,obj2_prop,LESS)) index=i; } return index; }

上記記事の「検索の整理」セクションを参照してください。

これで、履歴ポジションのリストを処理するクラスを作成する準備が整いました。

履歴ポジションコレクションクラス

\MQL5\Services\AccountReporter\端末フォルダに、CPositionsControlクラスの新しいファイルPositionsControl.mqhを作成します。

クラスは標準ライブラリのCObject基底オブジェクトから継承する必要があり、履歴ポジションクラスと検索およびフィルタクラスファイルは作成されるファイルに含まれる必要があります。

//+------------------------------------------------------------------+ //| PositionsControl.mqh | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include "Position.mqh" #include "Select.mqh" //+------------------------------------------------------------------+ //| Collection class of historical positions | //+------------------------------------------------------------------+ class CPositionsControl : public CObject { }

private、protected、publicのクラスメソッドを宣言しましょう。

//+------------------------------------------------------------------+ //| Collection class of historical positions | //+------------------------------------------------------------------+ class CPositionsControl : public CObject { private: //--- Return (1) position type and (2) reason for opening by deal type ENUM_POSITION_TYPE PositionTypeByDeal(const CDeal *deal); ENUM_POSITION_REASON PositionReasonByDeal(const CDeal *deal); protected: CPosition m_temp_pos; // Temporary position object for searching CArrayObj m_list_pos; // List of positions //--- Return the position object from the list by ID CPosition *GetPositionObjByID(const long id); //--- Return the flag of the market position bool IsMarketPosition(const long id); public: //--- Create and update the list of positions. It can be redefined in the inherited classes virtual bool Refresh(void); //--- Return (1) the list, (2) number of positions in the list CArrayObj *GetPositionsList(void) { return &this.m_list_pos; } int PositionsTotal(void) const { return this.m_list_pos.Total(); } //--- Print the properties of all positions and their deals in the journal void Print(void); //--- Constructor/destructor CPositionsControl(void); ~CPositionsControl(); };

宣言されたメソッドの実装を考えてみましょう。

クラスコンストラクタで、履歴ポジションのリストのクローズ時間(ミリ秒単位)による並び替えフラグを設定します。

//+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CPositionsControl::CPositionsControl(void) { this.m_list_pos.Sort(POSITION_PROP_TIME_CLOSE_MSC); }

クラスデストラクタで、履歴ポジションのリストを破棄します。

//+------------------------------------------------------------------+ //| Destructor | //+------------------------------------------------------------------+ CPositionsControl::~CPositionsControl() { this.m_list_pos.Shutdown(); }

以下は、IDによるリストからポジションオブジェクトへのポインタを返すメソッドです。

//+------------------------------------------------------------------+ //| Return the position object from the list by ID | //+------------------------------------------------------------------+ CPosition *CPositionsControl::GetPositionObjByID(const long id) { //--- Set the position ID for the temporary object and set the flag of sorting by position ID for the list this.m_temp_pos.SetID(id); this.m_list_pos.Sort(POSITION_PROP_IDENTIFIER); //--- Get the index of the position object with the specified ID (or -1 if it is absent) from the list //--- Use the obtained index to get the pointer to the positino object from the list (or NULL if the index value is -1) int index=this.m_list_pos.Search(&this.m_temp_pos); CPosition *pos=this.m_list_pos.At(index); //--- Return the flag of sorting by position close time in milliseconds for the list and //--- return the pointer to the position object (or NULL if it is absent) this.m_list_pos.Sort(POSITION_PROP_TIME_CLOSE_MSC); return pos; }

以下は、市場ポジションフラグを返すメソッドです。