MQL4 and MQL5 Programming Articles

Study the MQL5 language for programming trading strategies in numerous published articles mostly written by you - the community members. The articles are grouped into categories to help you quicker find answers to any questions related to programming: Integration, Tester, Trading Strategies, etc.

Follow our new publications and discuss them on the Forum!

Add a new article

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

MQL5 Wizard Techniques you should know (Part 10). The Unconventional RBM

Restrictive Boltzmann Machines are at the basic level, a two-layer neural network that is proficient at unsupervised classification through dimensionality reduction. We take its basic principles and examine if we were to re-design and train it unorthodoxly, we could get a useful signal filter.

Neural networks made easy (Part 70): Closed-Form Policy Improvement Operators (CFPI)

In this article, we will get acquainted with an algorithm that uses closed-form policy improvement operators to optimize Agent actions in offline mode.

Application of the Grey Model in Technical Analysis of Financial Time Series

This article explores the grey model, a promising tool that can expand trader's capabilities. We will look at some options for applying this model to technical analysis and building trading strategies.

Engineering Trading Discipline into Code (Part 6): Building a Unified Discipline Framework in MQL5

The article introduces a unified MQL5 discipline framework that consolidates the symbol whitelist, trading‑hours and news filters, and daily trade‑limit modules under CDisciplineEngine.mqh. It explains centralized trade validation and state synchronization shared by a chart dashboard and an enforcement Expert Advisor. Readers learn how to authorize orders through a single gate, monitor permissions in real time, and automatically enforce rules across the terminal.

Self Optimizing Expert Advisors in MQL5 (Part 14): Viewing Data Transformations as Tuning Parameters of Our Feedback Controller

Preprocessing is a powerful yet quickly overlooked tuning parameter. It lives in the shadows of its bigger brothers: optimizers and shiny model architectures. Small percentage improvements here can have disproportionately large, compounding effects on profitability and risk. Too often, this largely unexplored science is boiled down to a simple routine, seen only as a means to an end, when in reality it is where signal can be directly amplified, or just as easily destroyed.

The MQL5 Standard Library Explorer (Part 6): Optimizing a generated Expert Advisor

In this discussion, we follow up on the previously developed multi-signal Expert Advisor with the objective of exploring and applying available optimization methods. The aim is to determine whether the trading performance of the EA can be meaningfully improved through systematic optimization based on historical data.

Neural networks made easy (Part 77): Cross-Covariance Transformer (XCiT)

In our models, we often use various attention algorithms. And, probably, most often we use Transformers. Their main disadvantage is the resource requirement. In this article, we will consider a new algorithm that can help reduce computing costs without losing quality.

Introduction to MQL5 (Part 35): Mastering API and WebRequest Function in MQL5 (IX)

Discover how to detect user actions in MetaTrader 5, send requests to an AI API, extract responses, and implement scrolling text in your panel.

Market Microstructure in MQL5 (Part 1): Robust Foundation

This article builds the foundation layer of a twelve-part MQL5 market microstructure toolkit. It implements guarded math helpers (SafeDivide, SafeLog, SafeSqrt, SafeExp, SafeTanh), robust data validation (ValidateSymbolV2, SafeCopyClose), trimmed statistical estimators (robust mean var), a linear regression slope, shared structs, and an FFT. You compile a single include file that hardens indicators and expert advisors against silent numerical failures and standardizes data flow for later parts.

GoertzelBrain: Adaptive Spectral Cycle Detection with Neural Network Ensemble in MQL5

GoertzelBrain combines Goertzel spectral analysis with an online‑trained neural network ensemble to convert cycle features into a directional confirmation signal. The indicator builds a compact feature vector from the dominant period, amplitude, confidence and their dynamics, plus local volatility, and outputs +1, −1 or 0. The article provides the full MQL5 implementation, explains the architecture and feature engineering, and shows how to use it as a directional filter.

Overcoming The Limitation of Machine Learning (Part 8): Nonparametric Strategy Selection

This article shows how to configure a black-box model to automatically uncover strong trading strategies using a data-driven approach. By using Mutual Information to prioritize the most learnable signals, we can build smarter and more adaptive models that outperform conventional methods. Readers will also learn to avoid common pitfalls like overreliance on surface-level metrics, and instead develop strategies rooted in meaningful statistical insight.

Mastering Log Records (Part 9): Implementing the builder pattern and adding default configurations

This article shows how to drastically simplify the use of the Logify library with the Builder pattern and automatic default configurations. It explains the structure of the specialized builders, how to use them with smart auto-completion, and how to ensure a functional log even without manual configuration. It also covers tweaks for MetaTrader 5 build 5100.

Developing a Replay System (Part 57): Understanding a Test Service

One point to note: although the service code is not included in this article and will only be provided in the next one, I'll explain it since we'll be using that same code as a springboard for what we're actually developing. So, be attentive and patient. Wait for the next article, because every day everything becomes more interesting.

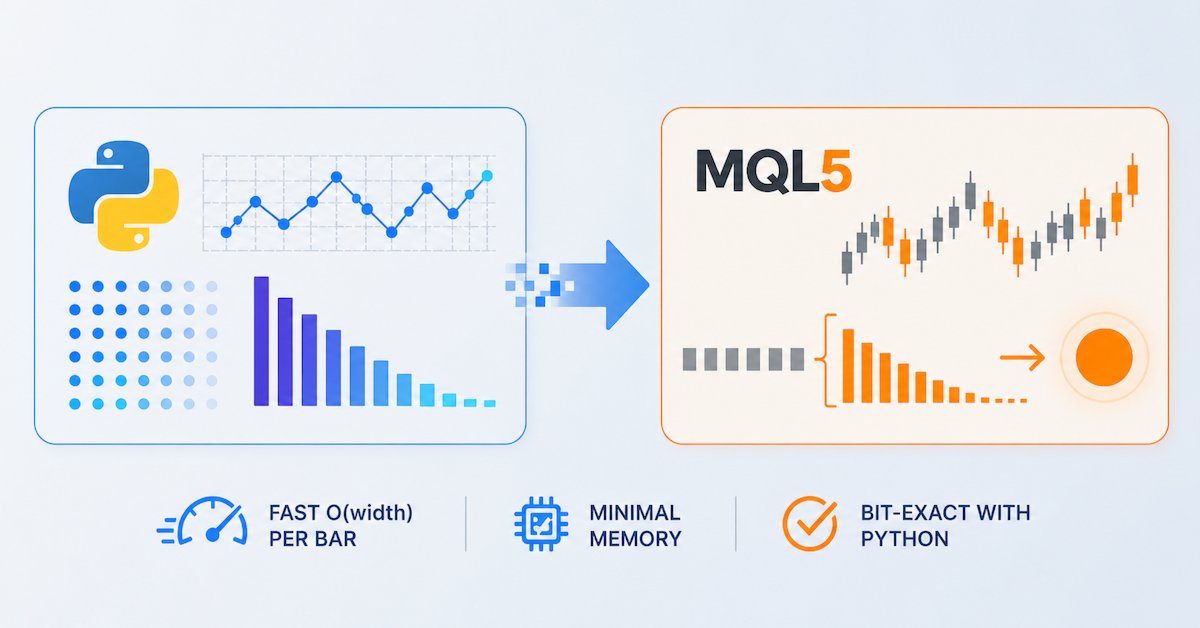

Feature Engineering for ML (Part 2): Implementing Fixed-Width Fractional Differentiation in MQL5

This article delivers a production-grade MQL5 implementation of fixed-width fractional differentiation for live MetaTrader 5 feeds. We introduce a header-only CFFDEngine that precomputes weights without a fixed cap, performs O(width) per-bar updates, and avoids per-tick allocations. The FFD.mq5 indicator supports all ENUM_APPLIED_PRICE types and prev_calculated optimization. Validation scripts confirm numerical equivalence with the standard Python frac diff_ffd pipeline.

Neural Networks in Trading: Hyperbolic Latent Diffusion Model (HypDiff)

The article considers methods of encoding initial data in hyperbolic latent space through anisotropic diffusion processes. This helps to more accurately preserve the topological characteristics of the current market situation and improves the quality of its analysis.

From Basic to Intermediate: Struct (VI)

In this article, we will explore how to approach the implementation of a common structural code base. The goal is to reduce the programming workload and leverage the full potential of the programming language itself—in this case, MQL5.

Mastering Log Records (Part 10): Avoiding Log Replay by Implementing a Suppression

We created a log suppression system in the Logify library. It details how the CLogifySuppression class reduces console noise by applying configurable rules to avoid repetitive or irrelevant messages. We also cover the external configuration framework, validation mechanisms, and comprehensive testing to ensure robustness and flexibility in log capture during bot or indicator development.

Feature Engineering for ML (Part 2): Implementing Fixed-Width Fractional Differentiation in MQL5

This article delivers a production-grade MQL5 implementation of fixed-width fractional differentiation for live MetaTrader 5 feeds. We introduce a header-only CFFDEngine that precomputes weights without a fixed cap, performs O(width) per-bar updates, and avoids per-tick allocations. The FFD.mq5 indicator supports all ENUM_APPLIED_PRICE types and prev_calculated optimization. Validation scripts confirm numerical equivalence with the standard Python frac diff_ffd pipeline.

Atmosphere Clouds Model Optimization (ACMO): Theory

The article is devoted to the metaheuristic Atmosphere Clouds Model Optimization (ACMO) algorithm, which simulates the behavior of clouds to solve optimization problems. The algorithm uses the principles of cloud generation, movement and propagation, adapting to the "weather conditions" in the solution space. The article reveals how the algorithm's meteorological simulation finds optimal solutions in a complex possibility space and describes in detail the stages of ACMO operation, including "sky" preparation, cloud birth, cloud movement, and rain concentration.

From Basic to Intermediate: Struct (IV)

In this article, we will explore how to create so-called structural code, where the entire context and methods for manipulating variables and information are placed within a structure to create a suitable context for implementing any code. Therefore, we will examine the necessity of using a private section of the code to separate what is public from what is not, thereby adhering to the rule of encapsulation and preserving the context for which the data structure was created.

Introduction to MQL5 (Part 41): Beginner Guide to File Handling in MQL5 (III)

Learn how to read a CSV file in MQL5 and organize its trading data into dynamic arrays. This article shows step by step how to count file elements, store all data in a single array, and separate each column into dedicated arrays, laying the foundation for advanced analysis and trading performance visualization.

Feature Engineering for ML (Part 4): Implementing Time Features in MQL5

Applying Python session boundaries to MQL5 broker timestamps misclassifies session membership by two to three hours on any non-UTC broker, corrupting session flags across the full backtest history. We implement CTimeFeatures.mqh, containing CRingBuffer and CTimeFeatures, with three EA-facing methods: Initialize (UTC offset capture and frequency gate configuration), Update (log return push to session-conditional ring buffers), and Calculate (cyclical encoding, session flags, and session volatility). The output is a flat double array drop-compatible with Python's get_time_features for sub-hourly, hourly, and daily timeframes.

Developing a Replay System (Part 60): Playing the Service (I)

We have been working on just the indicators for a long time now, but now it's time to get the service working again and see how the chart is built based on the data provided. However, since the whole thing is not that simple, we will have to be attentive to understand what awaits us ahead.

MQL5 Trading Toolkit (Part 6): Expanding the History Management EX5 Library with the Last Filled Pending Order Functions

Learn how to create an EX5 module of exportable functions that seamlessly query and save data for the most recently filled pending order. In this comprehensive step-by-step guide, we will enhance the History Management EX5 library by developing dedicated and compartmentalized functions to retrieve essential properties of the last filled pending order. These properties include the order type, setup time, execution time, filling type, and other critical details necessary for effective pending orders trade history management and analysis.

Reimagining Classic Strategies in MQL5 (Part II): FTSE100 and UK Gilts

In this series of articles, we explore popular trading strategies and try to improve them using AI. In today's article, we revisit the classical trading strategy built on the relationship between the stock market and the bond market.

Feature Engineering for ML (Part 4): Implementing Time Features in MQL5

Applying Python session boundaries to MQL5 broker timestamps misclassifies session membership by two to three hours on any non-UTC broker, corrupting session flags across the full backtest history. We implement CTimeFeatures.mqh, containing CRingBuffer and CTimeFeatures, with three EA-facing methods: Initialize (UTC offset capture and frequency gate configuration), Update (log return push to session-conditional ring buffers), and Calculate (cyclical encoding, session flags, and session volatility). The output is a flat double array drop-compatible with Python's get_time_features for sub-hourly, hourly, and daily timeframes.

A Generic Object Pool in MQL5: Eliminating Heap Fragmentation in High-Frequency Indicators

High-frequency MQL5 indicators that instantiate objects on every tick accumulate allocation overhead and timing jitter in OnCalculate(). This article constructs a generic templated object pool using a free-list index array, delivering O(1) Acquire() and Release() operations. The design includes double-release protection, strict separation of payload state from pool metadata in Reset(), and a fixed-capacity free list with no heap fallback. A dual-path custom indicator benchmark measures per-tick overhead difference using GetMicrosecondCount().

Step-by-Step Implementation of a Local Stop Loss System in MQL5

This article shows how to build a local stop-loss system in an MQL5 Expert Advisor that keeps stop levels on the terminal side. It walks through the execution logic, event handlers, inputs, and an OOP design using CTrade, CPositionInfo, CHashMap/CHashSet, and chart objects. You will implement multi-position tracking, draggable stops, visual spacers and labels, plus cleanup and disconnection behavior to create a practical risk-control utility.

Neural networks made easy (Part 69): Density-based support constraint for the behavioral policy (SPOT)

In offline learning, we use a fixed dataset, which limits the coverage of environmental diversity. During the learning process, our Agent can generate actions beyond this dataset. If there is no feedback from the environment, how can we be sure that the assessments of such actions are correct? Maintaining the Agent's policy within the training dataset becomes an important aspect to ensure the reliability of training. This is what we will talk about in this article.

MQL5 Wizard Techniques you should know (Part 88): Using Blooms Filter with a Custom Trailing Class

Our next focus in these series on ideas that can be rapidly prototyped with the MQL5 Wizard, is a Custom Trailing class that uses the Blooming Filter. Trailing Stop systems are an optional but very resourceful part to any trading system that we want to explore more in these series besides the traditional Entry Signals.

A feature selection algorithm using energy based learning in pure MQL5

In this article we present the implementation of a feature selection algorithm described in an academic paper titled,"FREL: A stable feature selection algorithm", called Feature weighting as regularized energy based learning.

Analyzing Price Time Gaps in MQL5 (Part II): Creating a Heat Map of Liquidity Distribution Over Time

A detailed guide on how to create a heat map indicator for MetaTrader 5 that visualizes the price distribution over time. The article reveals the mathematical basis of time density analysis, where each price level is colored from red (minimum stay time) to blue (maximum stay time).

Step-by-Step Implementation of a Local Stop Loss System in MQL5

This article shows how to build a local stop-loss system in an MQL5 Expert Advisor that keeps stop levels on the terminal side. It walks through the execution logic, event handlers, inputs, and an OOP design using CTrade, CPositionInfo, CHashMap/CHashSet, and chart objects. You will implement multi-position tracking, draggable stops, visual spacers and labels, plus cleanup and disconnection behavior to create a practical risk-control utility.

The MQL5 Standard Library Explorer (Part 12): Multi-Timeframe Composite-Score Dashboard

The article implements CMultiTimeframeMatrix, a reusable dashboard that maps symbols vs. timeframes and displays a numeric, colour‑coded score. The score combines trend, momentum, and volatility, updates by timer, and respects performance constraints. You will learn how to build the UI with CAppDialog/CLabel, compute metrics via CMatrixDouble, and embed the component into a thin EA for a consistent, real-time overview.

The MQL5 Standard Library Explorer (Part 12): Multi-Timeframe Composite-Score Dashboard

The article implements CMultiTimeframeMatrix, a reusable dashboard that maps symbols vs. timeframes and displays a numeric, colour‑coded score. The score combines trend, momentum, and volatility, updates by timer, and respects performance constraints. You will learn how to build the UI with CAppDialog/CLabel, compute metrics via CMatrixDouble, and embed the component into a thin EA for a consistent, real-time overview.

Atmosphere Clouds Model Optimization (ACMO): Practice

In this article, we will continue diving into the implementation of the ACMO (Atmospheric Cloud Model Optimization) algorithm. In particular, we will discuss two key aspects: the movement of clouds into low-pressure regions and the rain simulation, including the initialization of droplets and their distribution among clouds. We will also look at other methods that play an important role in managing the state of clouds and ensuring their interaction with the environment.

Population optimization algorithms: Bacterial Foraging Optimization - Genetic Algorithm (BFO-GA)

The article presents a new approach to solving optimization problems by combining ideas from bacterial foraging optimization (BFO) algorithms and techniques used in the genetic algorithm (GA) into a hybrid BFO-GA algorithm. It uses bacterial swarming to globally search for an optimal solution and genetic operators to refine local optima. Unlike the original BFO, bacteria can now mutate and inherit genes.

Developing a Replay System (Part 45): Chart Trade Project (IV)

The main purpose of this article is to introduce and explain the C_ChartFloatingRAD class. We have a Chart Trade indicator that works in a rather interesting way. As you may have noticed, we still have a fairly small number of objects on the chart, and yet we get the expected functionality. The values present in the indicator can be edited. The question is, how is this possible? This article will start to make things clearer.

MQL5 Trading Tools (Part 25): Expanding to Multiple Distributions with Interactive Switching

In this article, we expand the MQL5 graphing tool to support seventeen statistical distributions with interactive cycling via a header switch icon. We add type-specific data loading, discrete and continuous histogram computation, and theoretical density functions for each model, with dynamic titles, axis labels, and parameter panels that adapt automatically. The result lets you overlay distribution models on the same sample and compare fit across families without reloading the tool.

Adaptive Social Behavior Optimization (ASBO): Two-phase evolution

We continue dwelling on the topic of social behavior of living organisms and its impact on the development of a new mathematical model - ASBO (Adaptive Social Behavior Optimization). We will dive into the two-phase evolution, test the algorithm and draw conclusions. Just as in nature a group of living organisms join their efforts to survive, ASBO uses principles of collective behavior to solve complex optimization problems.