Using association rules in Forex data analysis

Introduction to association rules concept

Modern algorithmic trading requires new approaches to analysis. The market is constantly changing, and classical methods of technical analysis are no longer able to cope with identifying complex market relationships.

I have been working with data for a long time and have noticed that many successful ideas come from related areas. Today I want to share my experience of using association rules in trading. This method has proven itself in retail analytics, allowing us to find connections between purchases, transactions, price movements and future supply and demand. What if we apply it to the foreign exchange market?

The basic idea is simple - we are looking for stable patterns of price behavior, indicators and their combinations. For example, how often does a rise in EURUSD follow a fall in USDJPY? Or what conditions most often precede strong moves?

In this article, I will show the complete process of creating a trading system based on this idea. We will:

- Collect historical data in MQL5

- Analyze them in Python

- Find significant patterns

- Turn them into trading signals

Why this particular stack? MQL5 is great for working with stock exchange data and trading automation. In turn, Python provides powerful tools for analysis. From my experience, I can say that such a combination is very effective for developing trading systems.

There will be a lot of interesting things in the code, namely in the area of applying association rules to Forex.

Collection and preparation of historical Forex data

It is extremely important for us to collect and prepare all the data we need. Let's take H1 data of the main currency pairs for the last two years (since 2022) as a basis.

Now we will make an MQL5 script, which will collect and export the data we need in CSV format:

//+------------------------------------------------------------------+ //| Dataset.mq5 | //| Copyright 2024, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" //+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ //+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart() { string pairs[] = {"EURUSD", "GBPUSD", "USDJPY", "USDCHF"}; datetime startTime = D'2022.01.01 00:00'; datetime endTime = D'2024.01.01 00:00'; for(int i=0; i<ArraySize(pairs); i++) { string filename = pairs[i] + "_H1.csv"; int fileHandle = FileOpen(filename, FILE_WRITE|FILE_CSV); if(fileHandle != INVALID_HANDLE) { // Set headers FileWrite(fileHandle, "DateTime", "Open", "High", "Low", "Close", "Volume"); MqlRates rates[]; ArraySetAsSeries(rates, true); int copied = CopyRates(pairs[i], PERIOD_H1, startTime, endTime, rates); for(int j=copied-1; j>=0; j--) { FileWrite(fileHandle, TimeToString(rates[j].time), DoubleToString(rates[j].open, 5), DoubleToString(rates[j].high, 5), DoubleToString(rates[j].low, 5), DoubleToString(rates[j].close, 5), IntegerToString(rates[j].tick_volume) ); } FileClose(fileHandle); } } } //+------------------------------------------------------------------+

Data processing in Python

After forming a dataset, it is important to handle the data correctly.

For this purpose, I created the special ForexDataProcessor class, which takes care of all the dirty work. Let's have a look at its main components.

We will start from loading the data. Our function works with hourly data for the main currency pairs - EURUSD, GBPUSD, USDJPY and USDCHF. The data should be in CSV format with the main price characteristics.

import pandas as pd

import numpy as np

from datetime import datetime

import os

import warnings

warnings.filterwarnings('ignore')

class ForexDataProcessor:

def __init__(self):

self.pairs = ["EURUSD", "GBPUSD", "USDJPY", "USDCHF"]

self.data = {}

self.processed_data = {}

def load_data(self):

"""Load data for all currency pairs"""

success = True

for pair in self.pairs:

filename = f"{pair}_H1.csv"

try:

df = pd.read_csv(filename,

encoding='utf-16',

sep='\t',

names=['DateTime', 'Open', 'High', 'Low', 'Close', 'Volume'])

# Remove lines with duplicate headers

df = df[df['DateTime'] != 'DateTime']

# Convert data types

df['DateTime'] = pd.to_datetime(df['DateTime'], format='%Y.%m.%d %H:%M')

for col in ['Open', 'High', 'Low', 'Close']:

df[col] = pd.to_numeric(df[col], errors='coerce')

df['Volume'] = pd.to_numeric(df['Volume'], errors='coerce')

# Remove NaN strings

df = df.dropna()

df.set_index('DateTime', inplace=True)

self.data[pair] = df

print(f"Loaded {pair} data successfully. Shape: {df.shape}")

except Exception as e:

print(f"Error loading {pair} data: {str(e)}")

success = False

return success

def safe_qcut(self, series, q, labels):

"""Safe quantization with error handling"""

try:

if series.nunique() <= q:

# If there are fewer unique values than quantiles, use regular categorization

return pd.qcut(series, q=q, labels=labels, duplicates='drop')

return pd.qcut(series, q=q, labels=labels)

except Exception as e:

print(f"Warning: Error in qcut - {str(e)}. Using manual categorization.")

# Manual categorization as a backup option

percentiles = np.percentile(series, [20, 40, 60, 80])

return pd.cut(series,

bins=[-np.inf] + list(percentiles) + [np.inf],

labels=labels)

def calculate_indicators(self, df):

"""Calculate technical indicators for a single dataframe"""

result = df.copy()

# Basic calculations

result['Returns'] = result['Close'].pct_change()

result['Log_Returns'] = np.log(result['Close']/result['Close'].shift(1))

result['Range'] = result['High'] - result['Low']

result['Range_Pct'] = result['Range'] / result['Open'] * 100

# SMA calculations

for period in [5, 10, 20, 50, 200]:

result[f'SMA_{period}'] = result['Close'].rolling(window=period).mean()

# EMA calculations

for period in [5, 10, 20, 50]:

result[f'EMA_{period}'] = result['Close'].ewm(span=period, adjust=False).mean()

# Volatility

result['Volatility'] = result['Returns'].rolling(window=20).std() * np.sqrt(20)

# RSI

delta = result['Close'].diff()

gain = (delta.where(delta > 0, 0)).rolling(window=14).mean()

loss = (-delta.where(delta < 0, 0)).rolling(window=14).mean()

rs = gain / loss

result['RSI'] = 100 - (100 / (1 + rs))

# MACD

exp1 = result['Close'].ewm(span=12, adjust=False).mean()

exp2 = result['Close'].ewm(span=26, adjust=False).mean()

result['MACD'] = exp1 - exp2

result['MACD_Signal'] = result['MACD'].ewm(span=9, adjust=False).mean()

result['MACD_Hist'] = result['MACD'] - result['MACD_Signal']

# Bollinger Bands

result['BB_Middle'] = result['Close'].rolling(window=20).mean()

result['BB_Upper'] = result['BB_Middle'] + (result['Close'].rolling(window=20).std() * 2)

result['BB_Lower'] = result['BB_Middle'] - (result['Close'].rolling(window=20).std() * 2)

result['BB_Width'] = (result['BB_Upper'] - result['BB_Lower']) / result['BB_Middle']

# Discretization for association rules

# SMA-based trend

result['Trend'] = 'Sideways'

result.loc[result['Close'] > result['SMA_50'], 'Trend'] = 'Uptrend'

result.loc[result['Close'] < result['SMA_50'], 'Trend'] = 'Downtrend'

# RSI zones

result['RSI_Zone'] = pd.cut(result['RSI'].fillna(50),

bins=[-np.inf, 30, 45, 55, 70, np.inf],

labels=['Oversold', 'Weak', 'Neutral', 'Strong', 'Overbought'])

# Secure quantization for other parameters

labels = ['Very_Low', 'Low', 'Medium', 'High', 'Very_High']

result['Volatility_Zone'] = self.safe_qcut(

result['Volatility'].fillna(result['Volatility'].mean()),

5, labels)

result['Price_Zone'] = self.safe_qcut(

result['Close'],

5, labels)

result['Volume_Zone'] = self.safe_qcut(

result['Volume'],

5, labels)

# Candle patterns

result['Body'] = result['Close'] - result['Open']

result['Upper_Shadow'] = result['High'] - result[['Open', 'Close']].max(axis=1)

result['Lower_Shadow'] = result[['Open', 'Close']].min(axis=1) - result['Low']

result['Body_Pct'] = result['Body'] / result['Open'] * 100

body_mean = abs(result['Body_Pct']).mean()

result['Candle_Pattern'] = 'Normal'

result.loc[abs(result['Body_Pct']) < body_mean * 0.1, 'Candle_Pattern'] = 'Doji'

result.loc[result['Body_Pct'] > body_mean * 2, 'Candle_Pattern'] = 'Long_Bullish'

result.loc[result['Body_Pct'] < -body_mean * 2, 'Candle_Pattern'] = 'Long_Bearish'

return result

def process_all_pairs(self):

"""Process all currency pairs and create combined dataset"""

if not self.load_data():

return None

# Handling each pair

for pair in self.pairs:

if not self.data[pair].empty:

print(f"Processing {pair}...")

self.processed_data[pair] = self.calculate_indicators(self.data[pair])

# Add a pair prefix to the column names

self.processed_data[pair].columns = [f"{pair}_{col}" for col in self.processed_data[pair].columns]

else:

print(f"Skipping {pair} - no data")

# Find the common time range for non-empty data

common_dates = None

for pair in self.pairs:

if pair in self.processed_data and not self.processed_data[pair].empty:

if common_dates is None:

common_dates = set(self.processed_data[pair].index)

else:

common_dates &= set(self.processed_data[pair].index)

if not common_dates:

print("No common dates found")

return None

# Align all pairs by common dates

aligned_data = {}

for pair in self.pairs:

if pair in self.processed_data and not self.processed_data[pair].empty:

aligned_data[pair] = self.processed_data[pair].loc[sorted(common_dates)]

# Combine all pairs

combined_df = pd.concat([aligned_data[pair] for pair in aligned_data], axis=1)

return combined_df

def save_data(self, data, suffix='combined'):

"""Save processed data to CSV"""

timestamp = datetime.now().strftime('%Y%m%d_%H%M%S')

filename = f"forex_data_{suffix}_{timestamp}.csv"

try:

data.to_csv(filename, sep='\t', encoding='utf-16')

print(f"Saved processed data to: {filename}")

return True

except Exception as e:

print(f"Error saving data: {str(e)}")

return False

if __name__ == "__main__":

processor = ForexDataProcessor()

# Handling all pairs

combined_data = processor.process_all_pairs()

if combined_data is not None:

# Save the combined dataset

processor.save_data(combined_data)

# Display dataset info

print("\nCombined dataset shape:", combined_data.shape)

print("\nFeatures for association rules analysis:")

for col in combined_data.columns:

if any(x in col for x in ['_Zone', '_Pattern', 'Trend']):

print(f"- {col}")

# Save individual pairs

for pair in processor.pairs:

if pair in processor.processed_data and not processor.processed_data[pair].empty:

processor.save_data(processor.processed_data[pair], pair)

After successful loading, the most interesting part begins - calculation of technical indicators. Here I rely on a whole arsenal of time-tested tools. Moving averages help identify trends of varying duration. SMA(50) often acts as dynamic support or resistance. The RSI oscillator with a classic period of 14 is good for determining overbought and oversold market zones. MACD is indispensable for identifying momentum and reversal points. Bollinger Bands give a clear picture of the current market volatility.

# Volatility and RSI calculation example result['Volatility'] = result['Returns'].rolling(window=20).std() * np.sqrt(20) delta = result['Close'].diff() gain = (delta.where(delta > 0, 0)).rolling(window=14).mean() loss = (-delta.where(delta < 0, 0)).rolling(window=14).mean() rs = gain / loss result['RSI'] = 100 - (100 / (1 + rs))

Data discretization deserves special attention. All continuous values need to be broken down into clear categories. In this matter, it is important to find a golden mean - too steep a division will complicate the search for patterns, and too close a division will lead to the loss of important market nuances. For example, to determine the trend, a simpler division works better - by the position of the price relative to the average:

# Defining a trend result['Trend'] = 'Sideways' result.loc[result['Close'] > result['SMA_50'], 'Trend'] = 'Uptrend' result.loc[result['Close'] < result['SMA_50'], 'Trend'] = 'Downtrend'

Candle patterns also require a special approach. Based on statistical analysis, I distinguish Doji at the minimum candle body size, Long_Bullish and Long_Bearish at extreme price movements. This classification allows us to clearly identify moments of market indecision and strong impulse movements.

At the end of the processing, all currency pairs are combined into a single data array with a common time scale. This step is of fundamental importance - it opens up the possibility of searching for complex relationships between different instruments. Now we can see how the trend of one pair affects the volatility of another, or how candlestick patterns relate to trading volumes across the entire market.

Implementation the Apriori algorithm in Python

After preparing the data, we move on to the key stage - implementing the Apriori algorithm to find association rules in our financial data. We adapt the Apriori algorithm, originally developed for analyzing market baskets, to work with time series of currency pairs.

In the context of the foreign exchange market, a "transaction" is a set of states of various indicators and currency pairs at a certain point in time. For example:- EURUSD_Trend = Uptrend

- GBPUSD_RSI_Zone = Overbought

- USDJPY_Volatility_Zone = High

The algorithm searches for frequently occurring combinations of such states, on the basis of which trading rules are then formed.

import pandas as pd import numpy as np from collections import defaultdict from itertools import combinations import time import logging # Setting up logging logging.basicConfig( level=logging.INFO, format='%(asctime)s - %(levelname)s - %(message)s', handlers=[ logging.FileHandler('apriori_forex_advanced.log'), logging.StreamHandler() ] ) class AdvancedForexApriori: def __init__(self, min_support=0.01, min_confidence=0.7, max_length=3): self.min_support = min_support self.min_confidence = min_confidence self.max_length = max_length def find_patterns(self, df): start_time = time.time() logging.info("Starting advanced pattern search...") # Group columns by type for more meaningful analysis column_groups = { 'trend': [col for col in df.columns if 'Trend' in col], 'rsi': [col for col in df.columns if 'RSI_Zone' in col], 'volume': [col for col in df.columns if 'Volume_Zone' in col], 'price': [col for col in df.columns if 'Price_Zone' in col], 'pattern': [col for col in df.columns if 'Pattern' in col] } # Create a list of all columns for analysis pattern_cols = [] for cols in column_groups.values(): pattern_cols.extend(cols) logging.info(f"Found {len(pattern_cols)} pattern columns in {len(column_groups)} groups") # Prepare data pattern_df = df[pattern_cols] n_rows = len(pattern_df) # Find single patterns logging.info("Finding single patterns...") single_patterns = {} for col in pattern_cols: value_counts = pattern_df[col].value_counts() value_counts = value_counts[value_counts/n_rows >= self.min_support] for value, count in value_counts.items(): pattern = f"{col}={value}" single_patterns[pattern] = count/n_rows # Find pair and triple patterns logging.info("Finding complex patterns...") complex_rules = [] # Generate column combinations for analysis column_combinations = [] for i in range(2, self.max_length + 1): column_combinations.extend(combinations(pattern_cols, i)) total_combinations = len(column_combinations) for idx, cols in enumerate(column_combinations, 1): if idx % 10 == 0: logging.info(f"Processing combination {idx}/{total_combinations}") # Create a cross-table for the selected columns grouped = pattern_df.groupby([*cols]).size().reset_index(name='count') grouped['support'] = grouped['count'] / n_rows # Sort by minimum support grouped = grouped[grouped['support'] >= self.min_support] for _, row in grouped.iterrows(): # Form all possible combinations of antecedents and consequents items = [f"{col}={row[col]}" for col in cols] for i in range(1, len(items)): for antecedent in combinations(items, i): consequent = tuple(set(items) - set(antecedent)) # Calculate the support of the antecedent ant_support = self._calculate_support(pattern_df, antecedent) if ant_support > 0: # Avoid division by zero confidence = row['support'] / ant_support if confidence >= self.min_confidence: # Count the lift cons_support = self._calculate_support(pattern_df, consequent) lift = confidence / cons_support if cons_support > 0 else 0 # Adding additional metrics to evaluate rules leverage = row['support'] - (ant_support * cons_support) conviction = (1 - cons_support) / (1 - confidence) if confidence < 1 else float('inf') rule = { 'antecedent': antecedent, 'consequent': consequent, 'support': row['support'], 'confidence': confidence, 'lift': lift, 'leverage': leverage, 'conviction': conviction } # Sort the rules by additional criteria if self._is_meaningful_rule(rule): complex_rules.append(rule) # Sort the rules by complex metric complex_rules.sort(key=self._rule_score, reverse=True) end_time = time.time() logging.info(f"Pattern search completed in {end_time - start_time:.2f} seconds") logging.info(f"Found {len(complex_rules)} meaningful rules") return complex_rules def _calculate_support(self, df, items): """Calculate support for a set of elements""" mask = pd.Series(True, index=df.index) for item in items: col, val = item.split('=') mask &= (df[col] == val) return mask.mean() def _is_meaningful_rule(self, rule): """Check the rule for its relevance to trading""" # The rule should have the high lift and 'leverage' if rule['lift'] < 1.5 or rule['leverage'] < 0.01: return False # At least one element should be related to a trend or RSI has_trend_or_rsi = any('Trend' in item or 'RSI' in item for item in rule['antecedent'] + rule['consequent']) if not has_trend_or_rsi: return False return True def _rule_score(self, rule): """Calculate the rule complex evaluation""" return (rule['lift'] * 0.4 + rule['confidence'] * 0.3 + rule['support'] * 0.2 + rule['leverage'] * 0.1) # Load data logging.info("Loading data...") data = pd.read_csv('forex_data_combined_20241116_074242.csv', sep='\t', encoding='utf-16', index_col='DateTime') logging.info(f"Data loaded, shape: {data.shape}") # Apply the algorithm apriori = AdvancedForexApriori(min_support=0.01, min_confidence=0.7, max_length=3) rules = apriori.find_patterns(data) # Display results logging.info("\nTop 10 trading rules:") for i, rule in enumerate(rules[:10], 1): logging.info(f"\nRule {i}:") logging.info(f"IF {' AND '.join(rule['antecedent'])}") logging.info(f"THEN {' AND '.join(rule['consequent'])}") logging.info(f"Support: {rule['support']:.3f}") logging.info(f"Confidence: {rule['confidence']:.3f}") logging.info(f"Lift: {rule['lift']:.3f}") logging.info(f"Leverage: {rule['leverage']:.3f}") logging.info(f"Conviction: {rule['conviction']:.3f}") # Save results results_df = pd.DataFrame(rules) results_df.to_csv('forex_rules_advanced.csv', index=False, sep='\t', encoding='utf-16') logging.info("Results saved to forex_rules_advanced.csv")

Adaptation of association rules for currency pair analysis

In the course of my work on adapting the Apriori algorithm for the foreign exchange market, I encountered interesting challenges. Although this method was originally created to analyze in-store purchases, its potential for Forex seemed promising to me.

The main difficulty was that the Forex market is radically different from regular shopping in a store. Over the years of working in the financial markets, I have become accustomed to dealing with constantly changing prices and indicators. But how do you apply an algorithm that usually just looks for connections between bananas and milk on supermarket receipts?

As a result of my experiments, a system of five metrics was born. I tested each of them thoroughly.

'Support' turned out to be a very tricky metric. I once almost included a rule with excellent performance in a trading system, but the support was only 0.02. Fortunately, I noticed it in time – in practice, such a rule would only activate once every hundred years!

'Confidence' turned out to be simpler. When you work in the market, you quickly learn that even a 70% probability is an excellent indicator. The main thing is to manage risks wisely with the remaining 30%. We should always keep risk management in mind. Without it, you will face a drawdown or even a drain even if you have a Grail in your hands.

'Lift' has become my favorite indicator. After hundreds of hours of testing, I noticed a pattern - rules with the lift above 1.5 actually work in the real market. This discovery had a profound impact on my approach to signal sorting.

Dealing with 'Leverage' turned out to be funny. At first I wanted to exclude it from the system altogether, considering it useless. But during one particularly volatile period in the market, it helped sort out most of the false signals.

'Conviction' was added last after researching the forums. It helped me understand how important this indicator is for assessing the real significance of the patterns found.

The most surprising thing for me was how the algorithm finds unexpected connections between different currency pairs. For example, who would have thought that certain patterns in EURUSD could predict USDJPY movements with such accuracy? In 9 years of working in the market, I did not notice many of the relationships that the algorithm discovered. Although pair trading, basket trading and arbitrage were once my domain, I still remember the times when cmillion was just starting to develop its robots based on the mutual movements of pairs.

Now I continue my research, testing new combinations of indicators and time periods. The market is constantly changing and every day brings new discoveries. Next week I plan to publish the results of testing the system on annual data, as well as the first live results of the algorithm on live demo trading. There are several very interesting findings there.

To be honest, I did not even expect this project to go this far. It all started as a simple experiment with data mining and attempts to rigidly classify all market movements for the needs of classification algorithms, and eventually turned into a full-fledged trading system. I think I am just beginning to understand the true potential of this approach.

Features of implementation for Forex

Let's go back a little to the code itself. Our code has several important adaptations of the algorithm for handling financial data:

column_groups = {

'trend': [col for col in df.columns if 'Trend' in col],

'rsi': [col for col in df.columns if 'RSI_Zone' in col],

'volume': [col for col in df.columns if 'Volume_Zone' in col],

'price': [col for col in df.columns if 'Price_Zone' in col],

'pattern': [col for col in df.columns if 'Pattern' in col]

}

This grouping helps to find more meaningful combinations of indicators and reduces computational complexity.

def _is_meaningful_rule(self, rule): if rule['lift'] < 1.5 or rule['leverage'] < 0.01: return False has_trend_or_rsi = any('Trend' in item or 'RSI' in item for item in rule['antecedent'] + rule['consequent']) if not has_trend_or_rsi: return False return True

We select only rules with strong statistical significance (lift > 1.5) and mandatory inclusion of trend indicators or RSI.

def _rule_score(self, rule): return (rule['lift'] * 0.4 + rule['confidence'] * 0.3 + rule['support'] * 0.2 + rule['leverage'] * 0.1)

The weighted score helps rank rules based on their potential usefulness for trading.

Visualization of found associations

After finding the association rules, we should visualize and analyze them correctly. For this purpose, I have developed the special ForexRulesVisualizer class, which provides several ways of visual analysis of the found patterns.

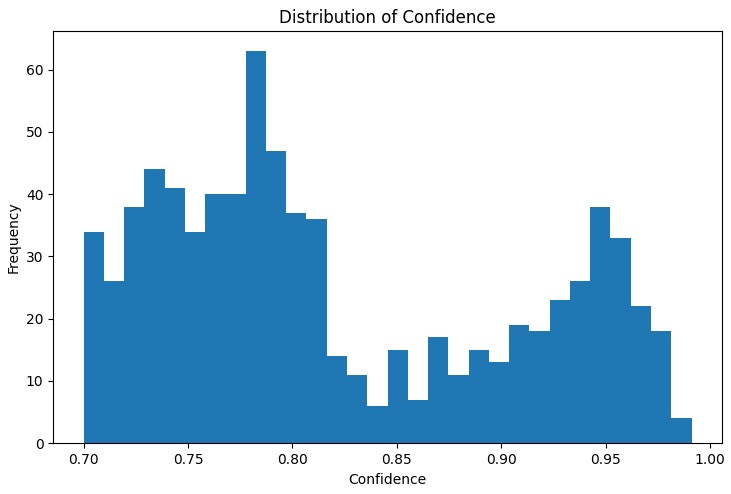

Distribution of rule metrics

The first step in the analysis is to understand the distribution of the main metrics of the rules found. The distribution graph of 'support', 'confidence', 'lift' and 'leverage' helps to evaluate the quality of the found rules and, if necessary, adjust the algorithm parameters.

A particularly useful tool was the interactive network graph, which clearly shows the connections between different market conditions. In this graph, the nodes are the indicator states (e.g. "EURUSD_Trend=Uptrend" or "USDJPY_RSI_Zone=Overbought"), and the edges represent the rules found, where the edge thickness is proportional to the 'lift' value.

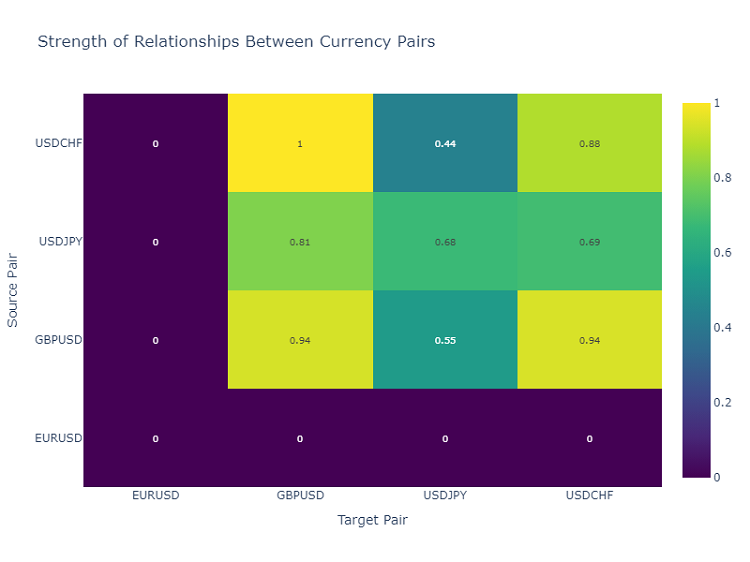

Heat map of currency pair interactions

To analyze the relationships between currency pairs, I use a heat map, which shows the strength of the relationships between different instruments. This helps identify pairs that most often influence each other, which is critical for building a diversified trading portfolio.

Creating trading signals

Once we have found and visualized the association rules, the next important step is to transform them into trading signals. For this purpose, I developed the ForexSignalGenerator class, which analyzes the current state of the market and generates trading signals based on the rules found.

import pandas as pd import numpy as np from datetime import datetime import logging class ForexSignalGenerator: def __init__(self, rules_df, min_rule_strength=0.5): """ Signal generator initialization Parameters: rules_df: DataFrame with association rules min_rule_strength: minimum rule strength to generate a signal """ self.rules_df = rules_df self.min_rule_strength = min_rule_strength self.active_signals = {} def calculate_rule_strength(self, rule): """ Comprehensive assessment of the rule strength Takes into account all metrics with different weights """ strength = ( rule['lift'] * 0.4 + # Main weight on 'lift' rule['confidence'] * 0.3 + # Rule confidence rule['support'] * 0.2 + # Occurrence frequency rule['leverage'] * 0.1 # Improvement over randomness ) # Additional bonus for having trend indicators if any('Trend' in item for item in rule['antecedent']): strength *= 1.2 return strength def analyze_market_state(self, current_data): """ Current market state analysis Parameters: current_data: DataFrame with current indicator values """ signals = [] state = self._create_market_state(current_data) # Find all the matching rules matching_rules = self._find_matching_rules(state) # Grouping rules by currency pairs for pair in ['EURUSD', 'GBPUSD', 'USDJPY', 'USDCHF']: pair_rules = [r for r in matching_rules if any(pair in c for c in r['consequent'])] if pair_rules: signal = self._generate_pair_signal(pair, pair_rules) signals.append(signal) return signals def _create_market_state(self, data): """Forming the current market state""" state = [] for col in data.columns: if any(x in col for x in ['_Zone', '_Pattern', 'Trend']): state.append(f"{col}={data[col].iloc[-1]}") return set(state) def _find_matching_rules(self, state): """Searching for rules that match the current state""" matching_rules = [] for _, rule in self.rules_df.iterrows(): # Check if all the rule conditions are met if all(cond in state for cond in rule['antecedent']): strength = self.calculate_rule_strength(rule) if strength >= self.min_rule_strength: rule['calculated_strength'] = strength matching_rules.append(rule) return matching_rules def _generate_pair_signal(self, pair, rules): """Generating a signal for a specific currency pair""" # Divide the rules by signal type trend_signals = defaultdict(float) for rule in rules: # Looking for trend-related consequents trend_cons = [c for c in rule['consequent'] if pair in c and 'Trend' in c] if trend_cons: for cons in trend_cons: trend = cons.split('=')[1] trend_signals[trend] += rule['calculated_strength'] # Determine the final signal if trend_signals: strongest_trend = max(trend_signals.items(), key=lambda x: x[1]) return { 'pair': pair, 'signal': strongest_trend[0], 'strength': strongest_trend[1], 'timestamp': datetime.now() } return None # Usage example def run_trading_system(data, rules_df): """ Trading system launch Parameters: data: DataFrame with historical data rules_df: DataFrame with association rules """ signal_generator = ForexSignalGenerator(rules_df) # Simulate a pass along historical data signals_history = [] for i in range(len(data) - 1): current_slice = data.iloc[i:i+1] signals = signal_generator.analyze_market_state(current_slice) for signal in signals: if signal: signals_history.append({ 'datetime': current_slice.index[0], 'pair': signal['pair'], 'signal': signal['signal'], 'strength': signal['strength'] }) return pd.DataFrame(signals_history) # Loading historical data and rules data = pd.read_csv('forex_data_combined_20241116_090857.csv', sep='\t', encoding='utf-16', index_col='DateTime', parse_dates=True) rules_df = pd.read_csv('forex_rules_advanced.csv', sep='\t', encoding='utf-16') rules_df['antecedent'] = rules_df['antecedent'].apply(eval) rules_df['consequent'] = rules_df['consequent'].apply(eval) # Launch the test signals_df = run_trading_system(data, rules_df) # Analyze the results print("Generated signals statistics:") print(signals_df.groupby('pair')['signal'].value_counts())

Assessing the strength of rules

After long experiments with visualizing the rules, it is time for the most difficult part - creating real trading signals. I admit, this task made me sweat quite a bit. It is one thing to find beautiful patterns on charts, and quite another to turn them into a working trading system.

I decided to create a separate module ForexSignalGenerator. At first, I just wanted to generate signals according to the strongest rules, but I quickly realized that everything is much more complicated. The market is constantly changing, and a rule that worked well yesterday may fail today.

I had to take a serious approach to assessing the strength of the rules. After several unsuccessful experiments, I developed a scale system. I had the most trouble choosing the ratios - I probably tried dozens of combinations. In the end, I settled on 'lift' giving 40% of the final assessment (this is a really key indicator), 'confidence' - 30%, 'support' - 20%, and 'leverage' - 10%.

Interestingly enough, often the strongest signals were obtained when the rule contained a trend component. I even added a special 20% bonus to the strength of such rules, and practice has shown that this is justified.

I also had to work hard when handling the current market state analysis. At first, I simply compared the current values of the indicators with the conditions of the rules. But then I realized that I needed to take into account the broader context. For example, I added verification of the general trend over the last few periods, the state of volatility, even the time of day.

Currently, the system analyzes about 20 different parameters for each currency pair. Some of the patterns I found really surprised me.

Of course, the system is still far from perfect. Sometimes, I catch myself thinking that I need to add fundamental factors. However, I have left this for later. First, I want to finish the current version.

Signal sorting and aggregation

During the system development, I quickly realized that simply finding rules is not enough - we need strict control of the quality of signals. After a few unsuccessful trades, it became clear that sorting is perhaps even more important than finding patterns themselves.

I started with a simple threshold of the minimum rule strength. At first I set it to 0.5, but I kept getting false positives. After two weeks of testing, I raised it to 0.7, and the situation improved noticeably. Еhe number of signals has decreased by about a third, but their quality has increased significantly.

The second level of sorting appeared after one particularly offensive incident. There was a rule with excellent performance, I opened a position according to it, but the market went strictly in the opposite direction. When I started to look into it, it turned out that other rules at that moment were giving opposite signals. Since then, I have been checking for consistency opening only if several rules point in the same direction.

Dealing with volatility turned out to be interesting. I noticed that during calm periods the system works like clockwork, but as soon as the market becomes more lively, problems begin. So, I added a dynamic filter by ATR. If volatility is above the 75 th percentile over the last 20 days, we increase the requirements for the strength of the rules by 20%.

The most difficult part was checking the conflicting signals. It happens that some rules say to buy, others say to sell, and all rules have good parameters. I tried different approaches, but eventually settled on a simple solution: if there are significant contradictions in the signals, we skip this situation. By doing that, we lose some opportunities, but we significantly reduce risks.

Next month, I am going to add sorting by time. I noticed that at certain hours the rules work noticeably worse. This is especially true during periods of low liquidity and the release of important news. I think, this should further increase the percentage of successful trades.

Test results

After several months of developing the system, I faced a key question - how to correctly evaluate the strength of each rule found? It all looked simple on paper, but the real market quickly exposed all the weaknesses of the initial approach.

As a result of long experiments, I came to a system of weights for different factors. I made 'Lift' the main component (40% influence) - practice has shown that this is a truly critically important indicator. 'Confidence' gives 30% - after all, the confidence of the rule also means a lot. 'Support' and 'leverage' have been given smaller weights - they act more like filters.

Signal sorting turned out to be a separate story. At first, I tried to trade by all the rules in a row, but I quickly realized my mistake. So, I had to introduce a multi-level sorting system. First, we sort out weak rules based on the minimum strength threshold. Then we check whether the signal is confirmed by several rules - single ones are usually less reliable.

Taking volatility into account proved to be particularly important. During calm periods, the system worked perfectly, but as soon as volatility jumped, the number of false signals increased sharply. I had to add dynamic filters that become more stringent as volatility increases.

Testing the system took almost three months. I ran it on a two-year history for four major pairs. The results were quite unexpected. For example, USDJPY showed the best performance - 65% of profitable trades with RR 1.6. But GBPUSD was disappointing - only 58% with RR 1.4.

Interestingly, rules with 'lift' above 2.0 and 'confidence' above 0.8 consistently showed the best results for all pairs. Apparently, these levels really are some kind of natural significance thresholds in the Forex market.

Further improvements

Currently, I see several directions for improving the system. First, the parameters of the rules need to be made more dynamic - the market is changing, and the system needs to adapt. Secondly, there is a clear lack of consideration of macroeconomics and the news background. Yes, it will complicate the system, but the potential gains are worth it.

Applying adaptive filters seems particularly interesting. Different market phases clearly require different system settings. It is crudely implemented at the moment, but I can already see several ways to improve it.

Next week I plan to start testing a new version with dynamic optimization of position sizes. Preliminary results on historical data look promising, but the real market, as always, will make its own adjustments.

Conclusion

The use of association rules in algo trading opens up interesting opportunities for finding non-obvious market patterns. The key to success here is proper data preparation, careful selection of rules and a well-thought-out signal generation system.

It is important to remember that any trading system requires constant monitoring and adaptation to changing market conditions. Associative rules are a powerful analysis tool, but they need to be used in conjunction with other technical and fundamental analysis methods.

Translated from Russian by MetaQuotes Ltd.

Original article: https://www.mql5.com/ru/articles/16061

Warning: All rights to these materials are reserved by MetaQuotes Ltd. Copying or reprinting of these materials in whole or in part is prohibited.

This article was written by a user of the site and reflects their personal views. MetaQuotes Ltd is not responsible for the accuracy of the information presented, nor for any consequences resulting from the use of the solutions, strategies or recommendations described.

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

Apparently, it is assumed that the reader must already have some knowledge of such a method, and if not?

I don't understand the metrics that are mentioned, in particular:

Lift has become my favourite indicator. After hundreds of hours of testing, I noticed a pattern - rules with lift above 1.5 really work in the real market. This discovery seriously influenced my approach to signal filtering.

If I understood the method correctly, correlating signals are searched for in quantum segments. But I didn't understand the next step. What is the target one? I assume that the resulting rules are checked against the target and evaluated against the metrics.

If so, it echoes my method, and it's interesting to evaluate performance and efficiency.