Library for easy and quick development of MetaTrader programs (part XXV): Handling errors returned by the trade server

Contents

Concept

We have already implemented the verification of the valid parameters

of the terminal, account and trading symbol, as well as the auto correction of invalid

trading order parameters. Now it only remains to implement the handling of server responses to sent trading orders.

After we send a trading order to the server, we need to check the response. The server returns the absence of errors or the error codes we need to

handle.

We are going to perform the handling in exactly the same way as we process invalid trading order parameters:

- No error — an order has been successfully queued for execution,

- Disable trading for the EA — for example, a complete ban on trading operations from the server side,

- Exit the trading method — for example, it is impossible to successfully send an order to the server, a position is already

closed or a pending order is removed,

- Correct trading request parameters and repeat — there are some invalid values in trading order parameters. Most

likely, the data has been changed when preparing a server request, and now the appropriate adjustment is required,

- Update data and repeat — server data has changed, however there is no need to adjust trading request values,

- Wait and repeat — waiting is required, for example, if the price is close to one of position stop levels, the FreezeLevel

parameter disables modification since the stop order may have already been activated. Waiting allows you to wait either for a stop

order activation and canceling a trading request, or the price leaving the freeze area, so that the order is successfully sent to the

server,

- Create a pending request — to be discussed in the next article.

The return codes are more numerous compared to the ones implemented for fixing possible errors in a trading order. Besides, not every code can

be corrected to repeat a request. To exclude errors that can be fixed, we will try to handle and send them back to a trading order.

In the methods of sending trading requests, arrange the loop for resending a trading order to the server in the methods of sending trading

requests. In other words, if we receive an error after the first request to the server, we will send the trading order as many times as there are

defined trading attempts for the trading class — either till the order is successfully sent to the server or before all attempts are made.

If all attempts of sending the order to the server are unsuccessful, return false from the

trading method. In this case, we are able to see the last error code in the calling program. The code is returned by the trade server, so that you

are able to decide on handling the error.

Now it is time for implementation.

Implementation

In the section of the simplified access to the account object properties of the CAccount account class in the Account.mqh file, add the method returning the flag of working on the hedge type account:

//+------------------------------------------------------------------+ //| Methods of a simplified access to the account object properties | //+------------------------------------------------------------------+ //--- Return the account's integer properties ENUM_ACCOUNT_TRADE_MODE TradeMode(void) const { return (ENUM_ACCOUNT_TRADE_MODE)this.GetProperty(ACCOUNT_PROP_TRADE_MODE); } ENUM_ACCOUNT_STOPOUT_MODE MarginSOMode(void) const { return (ENUM_ACCOUNT_STOPOUT_MODE)this.GetProperty(ACCOUNT_PROP_MARGIN_SO_MODE); } ENUM_ACCOUNT_MARGIN_MODE MarginMode(void) const { return (ENUM_ACCOUNT_MARGIN_MODE)this.GetProperty(ACCOUNT_PROP_MARGIN_MODE); } long Login(void) const { return this.GetProperty(ACCOUNT_PROP_LOGIN); } long Leverage(void) const { return this.GetProperty(ACCOUNT_PROP_LEVERAGE); } long LimitOrders(void) const { return this.GetProperty(ACCOUNT_PROP_LIMIT_ORDERS); } long TradeAllowed(void) const { return this.GetProperty(ACCOUNT_PROP_TRADE_ALLOWED); } long TradeExpert(void) const { return this.GetProperty(ACCOUNT_PROP_TRADE_EXPERT); } long CurrencyDigits(void) const { return this.GetProperty(ACCOUNT_PROP_CURRENCY_DIGITS); } long ServerType(void) const { return this.GetProperty(ACCOUNT_PROP_SERVER_TYPE); } long FIFOClose(void) const { return this.GetProperty(ACCOUNT_PROP_FIFO_CLOSE); } bool IsHedge(void) const { return this.MarginMode()==ACCOUNT_MARGIN_MODE_RETAIL_HEDGING; } //--- Return the account's real properties

In the Defines.mqh file, add the macro substitution to specify the

default number of trading attempts for a trading class.

In this article, we are going to prepare for creation of pending

requests, so we need the timer for the trading class.

Therefore, let's write

the trading class timer parameters right away:

//+------------------------------------------------------------------+ //| Macro substitutions | //+------------------------------------------------------------------+ //--- Describe the function with the error line number #define DFUN_ERR_LINE (__FUNCTION__+(TerminalInfoString(TERMINAL_LANGUAGE)=="Russian" ? ", Page " : ", Line ")+(string)__LINE__+": ") #define DFUN (__FUNCTION__+": ") // "Function description" #define COUNTRY_LANG ("Russian") // Country language #define END_TIME (D'31.12.3000 23:59:59') // End date for account history data requests #define TIMER_FREQUENCY (16) // Minimal frequency of the library timer in milliseconds #define TOTAL_TRY (5) // Default number of trading attempts //--- Standard sounds #define SND_ALERT "alert.wav" #define SND_ALERT2 "alert2.wav" #define SND_CONNECT "connect.wav" #define SND_DISCONNECT "disconnect.wav" #define SND_EMAIL "email.wav" #define SND_EXPERT "expert.wav" #define SND_NEWS "news.wav" #define SND_OK "ok.wav" #define SND_REQUEST "request.wav" #define SND_STOPS "stops.wav" #define SND_TICK "tick.wav" #define SND_TIMEOUT "timeout.wav" #define SND_WAIT "wait.wav" //--- Parameters of the orders and deals collection timer #define COLLECTION_ORD_PAUSE (250) // Orders and deals collection timer pause in milliseconds #define COLLECTION_ORD_COUNTER_STEP (16) // Increment of the orders and deals collection timer counter #define COLLECTION_ORD_COUNTER_ID (1) // Orders and deals collection timer counter ID //--- Parameters of the account collection timer #define COLLECTION_ACC_PAUSE (1000) // Account collection timer pause in milliseconds #define COLLECTION_ACC_COUNTER_STEP (16) // Account timer counter increment #define COLLECTION_ACC_COUNTER_ID (2) // Account timer counter ID //--- Symbol collection timer 1 parameters #define COLLECTION_SYM_PAUSE1 (100) // Pause of the symbol collection timer 1 in milliseconds (for scanning market watch symbols) #define COLLECTION_SYM_COUNTER_STEP1 (16) // Increment of the symbol timer 1 counter #define COLLECTION_SYM_COUNTER_ID1 (3) // Symbol timer 1 counter ID //--- Symbol collection timer 2 parameters #define COLLECTION_SYM_PAUSE2 (300) // Pause of the symbol collection timer 2 in milliseconds (for events of the market watch symbol list) #define COLLECTION_SYM_COUNTER_STEP2 (16) // Increment of the symbol timer 2 counter #define COLLECTION_SYM_COUNTER_ID2 (4) // Symbol timer 2 counter ID //--- Trading class timer parameters #define COLLECTION_REQ_PAUSE (300) // Trading class timer pause in milliseconds #define COLLECTION_REQ_COUNTER_STEP (16) // Trading class timer counter increment #define COLLECTION_REQ_COUNTER_ID (5) // Trading class timer counter ID //--- Collection list IDs #define COLLECTION_HISTORY_ID (0x7779) // Historical collection list ID #define COLLECTION_MARKET_ID (0x777A) // Market collection list ID #define COLLECTION_EVENTS_ID (0x777B) // Event collection list ID #define COLLECTION_ACCOUNT_ID (0x777C) // Account collection list ID #define COLLECTION_SYMBOLS_ID (0x777D) // Symbol collection list ID //--- Data parameters for file operations #define DIRECTORY ("DoEasy\\") // Library directory for storing object folders #define RESOURCE_DIR ("DoEasy\\Resource\\") // Library directory for storing resource folders //--- Symbol parameters #define CLR_DEFAULT (0xFF000000) // Default color #define SYMBOLS_COMMON_TOTAL (1000) // Total number of working symbols //+------------------------------------------------------------------+

Add two flags to the list of flags of the trade server error handling methods — the

flag of the pending order price error and the flag of the stop limit order

price error. Also, add the method of correcting trading order

parameters to the methods for handling errors and trade server return codes:

//+------------------------------------------------------------------+ //| Flags indicating the trading request error handling methods | //+------------------------------------------------------------------+ enum ENUM_TRADE_REQUEST_ERR_FLAGS { TRADE_REQUEST_ERR_FLAG_NO_ERROR = 0, // No error TRADE_REQUEST_ERR_FLAG_FATAL_ERROR = 1, // Disable trading for an EA (critical error) - exit TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR = 2, // Library internal error - exit TRADE_REQUEST_ERR_FLAG_ERROR_IN_LIST = 4, // Error in the list - handle (ENUM_ERROR_CODE_PROCESSING_METHOD) TRADE_REQUEST_ERR_FLAG_PRICE_ERROR = 8, // Placement price error TRADE_REQUEST_ERR_FLAG_LIMIT_ERROR = 16, // Limit order price error }; //+------------------------------------------------------------------+ //| The methods of handling errors and server return codes | //+------------------------------------------------------------------+ enum ENUM_ERROR_CODE_PROCESSING_METHOD { ERROR_CODE_PROCESSING_METHOD_OK, // No errors ERROR_CODE_PROCESSING_METHOD_DISABLE, // Disable trading for the EA ERROR_CODE_PROCESSING_METHOD_EXIT, // Exit the trading method ERROR_CODE_PROCESSING_METHOD_CORRECT, // Correct trading request parameters and repeat ERROR_CODE_PROCESSING_METHOD_REFRESH, // Update data and repeat ERROR_CODE_PROCESSING_METHOD_PENDING, // Create a pending request ERROR_CODE_PROCESSING_METHOD_WAIT, // Wait and repeat }; //+------------------------------------------------------------------+

Write the new message indices in the Datas.mqh file:

//--- CTrading MSG_LIB_TEXT_TERMINAL_NOT_TRADE_ENABLED, // Trade operations are not allowed in the terminal (the AutoTrading button is disabled) MSG_LIB_TEXT_EA_NOT_TRADE_ENABLED, // EA is not allowed to trade (F7 --> Common --> Allow Automated Trading) MSG_LIB_TEXT_ACCOUNT_NOT_TRADE_ENABLED, // Trading is disabled for the current account MSG_LIB_TEXT_ACCOUNT_EA_NOT_TRADE_ENABLED, // Trading on the trading server side is disabled for EAs on the current account MSG_LIB_TEXT_REQUEST_REJECTED_DUE, // Request was rejected before sending to the server due to: MSG_LIB_TEXT_INVALID_REQUEST, // Invalid request: MSG_LIB_TEXT_NOT_ENOUTH_MONEY_FOR, // Insufficient funds for performing a trade MSG_LIB_TEXT_MAX_VOLUME_LIMIT_EXCEEDED, // Exceeded maximum allowed aggregate volume of orders and positions in one direction MSG_LIB_TEXT_REQ_VOL_LESS_MIN_VOLUME, // Request volume is less than the minimum acceptable one MSG_LIB_TEXT_REQ_VOL_MORE_MAX_VOLUME, // Request volume exceeds the maximum acceptable one MSG_LIB_TEXT_CLOSE_BY_ORDERS_DISABLED, // Close by is disabled MSG_LIB_TEXT_INVALID_VOLUME_STEP, // Request volume is not a multiple of the minimum lot change step gradation MSG_LIB_TEXT_CLOSE_BY_SYMBOLS_UNEQUAL, // Symbols of opposite positions are not equal MSG_LIB_TEXT_SL_LESS_STOP_LEVEL, // StopLoss violates requirements for symbol's StopLevel MSG_LIB_TEXT_TP_LESS_STOP_LEVEL, // TakeProfit violates requirements for symbol's StopLevel MSG_LIB_TEXT_PRICE_LESS_STOP_LEVEL, // Order distance in points is less than a value allowed by symbol's StopLevel parameter MSG_LIB_TEXT_LIMIT_LESS_STOP_LEVEL, // Limit order distance in points relative to a stop order is less than a value allowed by symbol's StopLevel parameter MSG_LIB_TEXT_SL_LESS_FREEZE_LEVEL, // The distance from the price to StopLoss is less than a value allowed by symbol's FreezeLevel parameter MSG_LIB_TEXT_TP_LESS_FREEZE_LEVEL, // The distance from the price to TakeProfit is less than a value allowed by symbol's FreezeLevel parameter MSG_LIB_TEXT_PR_LESS_FREEZE_LEVEL, // The distance from the price to an order activation level is less than a value allowed by symbol's FreezeLevel parameter MSG_LIB_TEXT_UNSUPPORTED_SL_TYPE, // Unsupported StopLoss parameter type (should be 'int' or 'double') MSG_LIB_TEXT_UNSUPPORTED_TP_TYPE, // Unsupported TakeProfit parameter type (should be 'int' or 'double') MSG_LIB_TEXT_UNSUPPORTED_PR_TYPE, // Unsupported price parameter type (should be 'int' or 'double') MSG_LIB_TEXT_UNSUPPORTED_PL_TYPE, // Unsupported limit order price parameter type (should be 'int' or 'double') MSG_LIB_TEXT_UNSUPPORTED_PRICE_TYPE_IN_REQ, // Unsupported price parameter type in a request MSG_LIB_TEXT_TRADING_DISABLE, // Trading disabled for the EA until the reason is eliminated MSG_LIB_TEXT_TRADING_OPERATION_ABORTED, // Trading operation is interrupted MSG_LIB_TEXT_CORRECTED_TRADE_REQUEST, // Correcting trading request parameters MSG_LIB_TEXT_CREATE_PENDING_REQUEST, // Creating a pending request MSG_LIB_TEXT_NOT_POSSIBILITY_CORRECT_LOT, // Unable to correct a lot MSG_LIB_TEXT_FAILING_CREATE_PENDING_REQ, // Failed to create a pending request MSG_LIB_TEXT_TRY_N, // Trading attempt # };

and message texts:

{"Дистанция установки ордера в пунктах меньше разрешённой параметром StopLevel символа","Distance to place order in points less than allowed by symbol's StopLevel"},

{"Дистанция установки лимит-ордера относительно стоп-ордера меньше разрешённой параметром StopLevel символа","Distance to place limit order relative to stop order less than allowed by symbol's StopLevel"},

{"Дистанция от цены до StopLoss меньше разрешённой параметром FreezeLevel символа","Distance from price to StopLoss less than allowed by symbol's FreezeLevel"},

{"Дистанция от цены до TakeProfit меньше разрешённой параметром FreezeLevel символа","Distance from price to TakeProfit less than allowed by symbol's FreezeLevel"},

{"Дистанция от цены до цены срабатывания ордера меньше разрешённой параметром FreezeLevel символа","Distance from price to order triggering price less than allowed by symbol's FreezeLevel"},

{"Неподдерживаемый тип параметра StopLoss (необходимо int или double)","Unsupported StopLoss parameter type (int or double required)"},

{"Неподдерживаемый тип параметра TakeProfit (необходимо int или double)","Unsupported TakeProfit parameter type (int or double required)"},

{"Неподдерживаемый тип параметра цены (необходимо int или double)","Unsupported price parameter type (int or double required)"},

{"Неподдерживаемый тип параметра цены limit-ордера (необходимо int или double)","Unsupported type of price parameter for limit order (int or double required)"},

{"Неподдерживаемый тип параметра цены в запросе","Unsupported price parameter type in request"},

{"Торговля отключена для эксперта до устранения причины запрета","Trading for expert disabled till this ban eliminated"},

{"Торговая операция прервана","Trading operation aborted"},

{"Корректировка параметров торгового запроса ...","Correction of trade request parameters ..."},

{"Создание отложенного запроса","Create pending request"},

{"Нет возможности скорректировать лот","Unable to correct lot"},

{"Не удалось создать отложенный запрос","Failed to create pending request"},

{"Торговая попытка #","Trading attempt #"},

};

The TradeObj.mqh base trading object file has undergone minor changes.

The method for placing a pending order

features the order type parameter defining the execution (the

default one was used before that):

//--- Place an order bool SetOrder(const ENUM_ORDER_TYPE type, const double volume, const double price, const double sl=0, const double tp=0, const double price_stoplimit=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE);

Now if the passed value exceeds -1, the value passed to the method is used. Otherwise, the default parameter value is applied:

//+------------------------------------------------------------------+ //| Set an order | //+------------------------------------------------------------------+ bool CTradeObj::SetOrder(const ENUM_ORDER_TYPE type, const double volume, const double price, const double sl=0, const double tp=0, const double price_stoplimit=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { ::ResetLastError(); //--- If an invalid order type has been passed, write the error code and description, send the message to the journal and return 'false' if(type==ORDER_TYPE_BUY || type==ORDER_TYPE_SELL || type==ORDER_TYPE_CLOSE_BY #ifdef __MQL4__ || type==ORDER_TYPE_BUY_STOP_LIMIT || type==ORDER_TYPE_SELL_STOP_LIMIT #endif ) { this.m_result.retcode=MSG_LIB_SYS_INVALID_ORDER_TYPE; this.m_result.comment=CMessage::Text(this.m_result.retcode); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_INVALID_ORDER_TYPE),OrderTypeDescription(type)); return false; } //--- Clear the structures ::ZeroMemory(this.m_request); ::ZeroMemory(this.m_result); //--- Fill in the request structure this.m_request.action = TRADE_ACTION_PENDING; this.m_request.symbol = this.m_symbol; this.m_request.magic = (magic==ULONG_MAX ? this.m_magic : magic); this.m_request.volume = volume; this.m_request.type = type; this.m_request.stoplimit = price_stoplimit; this.m_request.price = price; this.m_request.sl = sl; this.m_request.tp = tp; this.m_request.expiration = expiration; this.m_request.type_time = (type_time>WRONG_VALUE ? type_time : this.m_type_time); this.m_request.type_filling= (type_filling>WRONG_VALUE ? type_filling : this.m_type_filling); this.m_request.comment = (comment==NULL ? this.m_comment : comment); //--- Return the result of sending a request to the server #ifdef __MQL5__ return(!this.m_async_mode ? ::OrderSend(this.m_request,this.m_result) : ::OrderSendAsync(this.m_request,this.m_result)); #else ::ResetLastError(); int ticket=::OrderSend(m_request.symbol,m_request.type,m_request.volume,m_request.price,(int)m_request.deviation,m_request.sl,m_request.tp,m_request.comment,(int)m_request.magic,m_request.expiration,clrNONE); ::SymbolInfoTick(this.m_symbol,this.m_tick); if(ticket!=WRONG_VALUE) { this.m_result.retcode=::GetLastError(); this.m_result.ask=this.m_tick.ask; this.m_result.bid=this.m_tick.bid; this.m_result.order=ticket; this.m_result.price=(::OrderSelect(ticket,SELECT_BY_TICKET) ? ::OrderOpenPrice() : this.m_request.price); this.m_result.volume=(::OrderSelect(ticket,SELECT_BY_TICKET) ? ::OrderLots() : this.m_request.volume); this.m_result.comment=CMessage::Text(this.m_result.retcode); return true; } else { this.m_result.retcode=::GetLastError(); this.m_result.ask=this.m_tick.ask; this.m_result.bid=this.m_tick.bid; this.m_result.comment=CMessage::Text(this.m_result.retcode); return false; } #endif } //+------------------------------------------------------------------+

The prices in trading orders have also been corrected. Previously, if the chart was based on Last prices, the price in the trading order was set

as Ask and Last. Now it is always Ask and Bid, regardless of prices used to construct a chart.

You can find other minor changes in the files attached below. There is no point in dwelling on them here.

In the Trading.mqh file, in the private section of the CTrading trading class, add the

list of pending requests and the variable for storing the number of

trading attempts:

//+------------------------------------------------------------------+ //| Trading class | //+------------------------------------------------------------------+ class CTrading { private: CAccount *m_account; // Pointer to the current account object CSymbolsCollection *m_symbols; // Pointer to the symbol collection list CMarketCollection *m_market; // Pointer to the list of the collection of market orders and positions CHistoryCollection *m_history; // Pointer to the list of the collection of historical orders and deals CArrayObj m_list_request; // List of pending requests CArrayInt m_list_errors; // Error list bool m_is_trade_disable; // Flag disabling trading bool m_use_sound; // The flag of using sounds of the object trading events uchar m_total_try; // Number of trading attempts ENUM_LOG_LEVEL m_log_level; // Logging level MqlTradeRequest m_request; // Trading request prices ENUM_TRADE_REQUEST_ERR_FLAGS m_error_reason_flags; // Flags of error source in a trading method ENUM_ERROR_HANDLING_BEHAVIOR m_err_handling_behavior; // Behavior when handling error

In the future, we will use the list of trading requests to store the objects of the pending request class, while the m_total_try variable is to contain the number of trading attempts set by default for a trading class in its constructor:

//+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ CTrading::CTrading() { this.m_list_errors.Clear(); this.m_list_errors.Sort(); this.m_list_request.Clear(); this.m_list_request.Sort(); this.m_total_try=TOTAL_TRY; this.m_log_level=LOG_LEVEL_ALL_MSG; this.m_is_trade_disable=false; this.m_err_handling_behavior=ERROR_HANDLING_BEHAVIOR_CORRECT; ::ZeroMemory(this.m_request); } //+------------------------------------------------------------------+

Here, clear the list of pending requests and set the sorted list flag for it.

Add the price of placing a limit order for a StopLimit type order to the

parameters of the method for checking the price relative to StopLevel:

bool CheckPriceByStopLevel(const ENUM_ORDER_TYPE order_type,const double price,const CSymbol *symbol_obj,const double limit=0);

Add the check to the method itself:

//+------------------------------------------------------------------+ //| Return the flag checking the validity of the distance | //| from the price to the placement level by StopLevel | //+------------------------------------------------------------------+ bool CTrading::CheckPriceByStopLevel(const ENUM_ORDER_TYPE order_type,const double price,const CSymbol *symbol_obj,const double limit=0) { double lv=symbol_obj.TradeStopLevel()*symbol_obj.Point(); double pr=(this.DirectionByActionType((ENUM_ACTION_TYPE)order_type)==ORDER_TYPE_BUY ? symbol_obj.Ask() : symbol_obj.Bid()); return (limit==0 ? //--- Order placement prices relative to the price ( order_type==ORDER_TYPE_SELL_STOP || order_type==ORDER_TYPE_SELL_STOP_LIMIT || order_type==ORDER_TYPE_BUY_LIMIT ? price<(pr-lv) : order_type==ORDER_TYPE_BUY_STOP || order_type==ORDER_TYPE_BUY_STOP_LIMIT || order_type==ORDER_TYPE_SELL_LIMIT ? price>(pr+lv) : true ) : //--- Limit order placement prices relative to the stop order price ( order_type==ORDER_TYPE_BUY_STOP_LIMIT ? limit<(price-lv) : order_type==ORDER_TYPE_SELL_STOP_LIMIT ? limit>(price+lv) : true ) ); } //+------------------------------------------------------------------+

Here, if the limit order price is equal to zero, check the prices of stop and limit orders, otherwise check stop limit order prices (the limit order price relative to the stop order price a stop limit order is activated at).

Pass the error code to the method returning the way of handling errors and add the pointer to the trading object in the error correction method:

//--- Return the error handling method ENUM_ERROR_CODE_PROCESSING_METHOD ResultProccessingMethod(const uint result_code); //--- Correct errors ENUM_ERROR_CODE_PROCESSING_METHOD RequestErrorsCorrecting(MqlTradeRequest &request,const ENUM_ORDER_TYPE order_type,const uint spread_multiplier,CSymbol *symbol_obj,CTradeObj *trade_obj);

Since we have multiple methods of opening positions and placing orders, all of them turned out to be almost the same. The difference is only in the

types of opened positions and placed orders.

To avoid writing the same code for each method, declare and implement two private

methods — for opening a position and placing

pending orders:

//--- (1) Open a position, (2) place a pending order template<typename SL,typename TP> bool OpenPosition(const ENUM_POSITION_TYPE type, const double volume, const string symbol, const ulong magic=ULONG_MAX, const SL sl=0, const TP tp=0, const string comment=NULL, const ulong deviation=ULONG_MAX); template<typename PS,typename PL,typename SL,typename TP> bool PlaceOrder( const ENUM_ORDER_TYPE order_type, const double volume, const string symbol, const PS price_stop, const PL price_limit=0, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); public: //--- Constructor

In the public section of the class, declare the timer we

will need to work with the class of pending requests, the method returning the list

of pending requests and the method setting the number of trading attempts:

public: //--- Constructor CTrading(); //--- Timer void OnTimer(void); //--- Get the pointers to the lists (make sure to call the method in program's OnInit() since the symbol collection list is created there) void OnInit(CAccount *account,CSymbolsCollection *symbols,CMarketCollection *market,CHistoryCollection *history) { this.m_account=account; this.m_symbols=symbols; this.m_market=market; this.m_history=history; } //--- Return the list of (1) errors and (2) pending requests CArrayInt *GetListErrors(void) { return &this.m_list_errors; } CArrayObj *GetListRequests(void) { return &this.m_list_request;} //--- Set the number of trading attempts void SetTotalTry(const uchar number) { this.m_total_try=number; } //--- Check limitations and errors

Let's improve the specification of the method for closing positions by a closed volume. The default is WRONG_VALUE — full position closure, otherwise — partial closure by a specified volume:

bool ClosePosition(const ulong ticket,const double volume=WRONG_VALUE,const string comment=NULL,const ulong deviation=ULONG_MAX);

In the specifications of pending order placement methods, add the

types of executing orders by excess. Previously, the default value set for the class was used. Now, the order execution type

value is selected based on the value passed to the method. In case of WRONG_VALUE, the

specified value is set by default, otherwise the one passed to the method is applied:

//--- Set (1) BuyStop, (2) BuyLimit, (3) BuyStopLimit pending order template<typename PS,typename SL,typename TP> bool PlaceBuyStop(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); template<typename PS,typename SL,typename TP> bool PlaceBuyLimit(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); template<typename PS,typename PL,typename SL,typename TP> bool PlaceBuyStopLimit(const double volume, const string symbol, const PS price_stop, const PL price_limit, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); //--- Set (1) SellStop, (2) SellLimit, (3) SellStopLimit pending order template<typename PS,typename SL,typename TP> bool PlaceSellStop(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); template<typename PS,typename SL,typename TP> bool PlaceSellLimit(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); template<typename PS,typename PL,typename SL,typename TP> bool PlaceSellStopLimit(const double volume, const string symbol, const PS price_stop, const PL price_limit, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE); //--- Modify a pending order template<typename PS,typename PL,typename SL,typename TP> bool ModifyOrder(const ulong ticket, const PS price=WRONG_VALUE, const SL sl=WRONG_VALUE, const TP tp=WRONG_VALUE, const PL limit=WRONG_VALUE, datetime expiration=WRONG_VALUE, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE);

Let's implement the timer. So far, we will prepare a workpiece of handling the list of pending requests:

//+------------------------------------------------------------------+ //| Timer | //+------------------------------------------------------------------+ void CTrading::OnTimer(void) { int total=this.m_list_request.Total(); for(int i=total-1;i>WRONG_VALUE;i--) { } } //+------------------------------------------------------------------+

Implementing the method returning the ways to handle trade server return codes:

//+------------------------------------------------------------------+ //| Return the error handling method | //+------------------------------------------------------------------+ ENUM_ERROR_CODE_PROCESSING_METHOD CTrading::ResultProccessingMethod(const uint result_code) { switch(result_code) { #ifdef __MQL4__ //--- Malfunctional trade operation case 9 : //--- Account disabled case 64 : //--- Invalid account number case 65 : return ERROR_CODE_PROCESSING_METHOD_DISABLE; //--- No error but result is unknown case 1 : //--- General error case 2 : //--- Old client terminal version case 5 : //--- Not enough rights case 7 : //--- Market closed case 132 : //--- Trading disabled case 133 : //--- Order is locked and being processed case 139 : //--- Buy only case 140 : //--- The number of open and pending orders has reached the limit set by the broker case 148 : //--- Attempt to open an opposite order if hedging is disabled case 149 : //--- Attempt to close a position on a symbol contradicts the FIFO rule case 150 : return ERROR_CODE_PROCESSING_METHOD_EXIT; //--- Invalid trading request parameters case 3 : //--- Invalid price case 129 : //--- Invalid stop levels case 130 : //--- Invalid volume case 131 : //--- Not enough money to perform the operation case 134 : //--- Expirations are denied by broker case 147 : return ERROR_CODE_PROCESSING_METHOD_CORRECT; //--- Trade server is busy case 4 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- No connection to the trade server case 6 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Too frequent requests case 8 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)10000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- No price case 136 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Broker is busy case 137 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Too many requests case 141 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)10000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Modification denied because the order is too close to market case 145 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Trade context is busy case 146 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)1000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- Trade timeout case 128 : //--- Price has changed case 135 : //--- New prices case 138 : return ERROR_CODE_PROCESSING_METHOD_REFRESH; //--- MQL5 #else //--- Auto trading disabled by the server case 10026 : return ERROR_CODE_PROCESSING_METHOD_DISABLE; //--- Request canceled by a trader case 10007 : //--- Request expired case 10012 : //--- Trading disabled case 10017 : //--- Market closed case 10018 : //--- Order status changed case 10023 : //--- Request unchanged case 10025 : //--- Request blocked for handling case 10028 : //--- Transaction is allowed for live accounts only case 10032 : //--- The maximum number of pending orders is reached case 10033 : //--- Reached the maximum order and position volume for this symbol case 10034 : //--- Invalid or prohibited order type case 10035 : //--- Position with the specified ID already closed case 10036 : //--- A close order is already present for a specified position case 10039 : //--- The maximum number of open positions is reached case 10040 : //--- Request to activate a pending order is rejected, the order is canceled case 10041 : //--- Request is rejected, because the rule "Only long positions are allowed" is set for the symbol case 10042 : //--- Request is rejected, because the rule "Only short positions are allowed" is set for the symbol case 10043 : //--- Request is rejected, because the rule "Only closing of existing positions is allowed" is set for the symbol case 10044 : //--- Request is rejected, because the rule "Only closing of existing positions by FIFO rule is allowed" is set for the symbol case 10045 : return ERROR_CODE_PROCESSING_METHOD_EXIT; //--- Requote case 10004 : //--- Request rejected case 10006 : //--- Prices changed case 10020 : return ERROR_CODE_PROCESSING_METHOD_REFRESH; //--- Invalid request case 10013 : //--- Invalid request volume case 10014 : //--- Invalid request price case 10015 : //--- Invalid request stop levels case 10016 : //--- Insufficient funds for request execution case 10019 : //--- Invalid order expiration in a request case 10022 : //--- The specified type of order execution by balance is not supported case 10030 : //--- Closed volume exceeds the current position volume case 10038 : return ERROR_CODE_PROCESSING_METHOD_CORRECT; //--- No quotes to process the request case 10021 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT; //--- Too frequent requests case 10024 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)10000; // ERROR_CODE_PROCESSING_METHOD_WAIT //--- An order or a position is frozen case 10029 : return (ENUM_ERROR_CODE_PROCESSING_METHOD)10000; // ERROR_CODE_PROCESSING_METHOD_WAIT; //--- Request handling error case 10011 : return ERROR_CODE_PROCESSING_METHOD_PENDING; //--- Auto trading disabled by the client terminal case 10027 : return ERROR_CODE_PROCESSING_METHOD_PENDING; //--- No connection to the trade server case 10031 : return ERROR_CODE_PROCESSING_METHOD_PENDING; //--- Order placed case 10008 : //--- Request executed case 10009 : //--- Request executed partially case 10010 : #endif //--- "OK" default: break; } return ERROR_CODE_PROCESSING_METHOD_OK; } //+------------------------------------------------------------------+

Here all is simple: the method receives the code obtained from the server after

sending a trading request to it. Then the codes indicating an error can be fixed are handled by the error fixing method, the codes

requiring data update and re-sending a request are handled appropriately, etc.

Since MQL5 and MQL4 servers return different error

codes, the method features the conditional compilation for MQL4 and MQL5.

All codes requiring the same type of handling are grouped in a single case of the switch

operator and return the unified method of handling the trade server return code.

Implementing the method of handling trade server errors:

//+------------------------------------------------------------------+ //| Correct errors | //+------------------------------------------------------------------+ ENUM_ERROR_CODE_PROCESSING_METHOD CTrading::RequestErrorsCorrecting(MqlTradeRequest &request, const ENUM_ORDER_TYPE order_type, const uint spread_multiplier, CSymbol *symbol_obj, CTradeObj *trade_obj) { //--- The empty error list means no errors are detected, return success int total=this.m_list_errors.Total(); if(total==0) return ERROR_CODE_PROCESSING_METHOD_OK; //--- Trading is disabled for the current account //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_ACCOUNT_NOT_TRADE_ENABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_ACCOUNT_NOT_TRADE_ENABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Trading on the trading server side is disabled for EAs on the current account //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_ACCOUNT_EA_NOT_TRADE_ENABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_ACCOUNT_EA_NOT_TRADE_ENABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Trading operations are disabled in the terminal //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_TERMINAL_NOT_TRADE_ENABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_TERMINAL_NOT_TRADE_ENABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Trading operations are disabled for the EA //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_EA_NOT_TRADE_ENABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_EA_NOT_TRADE_ENABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Disable trading on a symbol //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_TRADE_MODE_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_TRADE_MODE_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Close only //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_TRADE_MODE_CLOSEONLY)) { trade_obj.SetResultRetcode(MSG_SYM_TRADE_MODE_CLOSEONLY); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Market orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_MARKET_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_MARKET_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Limit orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_LIMIT_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_LIMIT_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Stop orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_STOP_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_STOP_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- StopLimit orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_STOP_LIMIT_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_STOP_LIMIT_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Sell only //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_TRADE_MODE_SHORTONLY)) { trade_obj.SetResultRetcode(MSG_SYM_TRADE_MODE_SHORTONLY); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Buy only //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_TRADE_MODE_LONGONLY)) { trade_obj.SetResultRetcode(MSG_SYM_TRADE_MODE_LONGONLY); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- CloseBy orders are disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_SYM_CLOSE_BY_ORDER_DISABLED)) { trade_obj.SetResultRetcode(MSG_SYM_CLOSE_BY_ORDER_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Exceeded maximum allowed aggregate volume of orders and positions in one direction //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_MAX_VOLUME_LIMIT_EXCEEDED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_MAX_VOLUME_LIMIT_EXCEEDED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Close by is disabled //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_CLOSE_BY_ORDERS_DISABLED)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_CLOSE_BY_ORDERS_DISABLED); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Symbols of opposite positions are not equal //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_CLOSE_BY_SYMBOLS_UNEQUAL)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_CLOSE_BY_SYMBOLS_UNEQUAL); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Unsupported price parameter type in a request //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_UNSUPPORTED_PRICE_TYPE_IN_REQ)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_UNSUPPORTED_PRICE_TYPE_IN_REQ); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Trading disabled for the EA until the reason is eliminated //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(MSG_LIB_TEXT_TRADING_DISABLE)) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_TRADING_DISABLE); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- The maximum number of pending orders is reached //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(10033)) { trade_obj.SetResultRetcode(10033); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Reached the maximum order and position volume for this symbol //--- write the error code to the base trading class object and return "exit from the trading method" if(this.IsPresentErorCode(10034)) { trade_obj.SetResultRetcode(10034); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; } //--- Correcting trading request parameters //--- Price, according to which stop orders are placed double price_set=(this.IsPresentErrorFlag(TRADE_REQUEST_ERR_FLAG_PRICE_ERROR) ? request.price : request.stoplimit); //--- First, adjust stop orders relative to the order/position level if(this.IsPresentErorCode(MSG_LIB_TEXT_SL_LESS_STOP_LEVEL)) request.sl=this.CorrectStopLoss(order_type,price_set,request.sl,symbol_obj,spread_multiplier); if(this.IsPresentErorCode(MSG_LIB_TEXT_TP_LESS_STOP_LEVEL)) request.tp=this.CorrectTakeProfit(order_type,price_set,request.tp,symbol_obj,spread_multiplier); //--- Pending orders price double shift=0; if(this.IsPresentErrorFlag(TRADE_REQUEST_ERR_FLAG_PRICE_ERROR)) { price_set=request.price; request.price=this.CorrectPricePending(order_type,price_set,0,symbol_obj,spread_multiplier); shift=request.price-price_set; //--- If this is not a stop limit order, move stop orders by the calculated correcting order level shift if(request.stoplimit==0) { if(request.sl>0) request.sl=this.CorrectStopLoss(order_type,request.price,request.sl+shift,symbol_obj,spread_multiplier); if(request.tp>0) request.tp=this.CorrectTakeProfit(order_type,request.price,request.tp+shift,symbol_obj,spread_multiplier); } } //--- The specified type of order execution by balance is not supported if(this.IsPresentErorCode(10030)) request.type_filling=symbol_obj.GetCorrectTypeFilling(); //--- Invalid order expiration in a request - if(this.IsPresentErorCode(10022)) { //--- if the expiration type is not supported as set by the expiration date and the expiration data is defined, reset the expiration date if(!symbol_obj.IsExpirationModeSpecified() && request.expiration>0) request.expiration=0; } //--- View the list of remaining errors and correct trading request parameters for(int i=0;i<total;i++) { int err=this.m_list_errors.At(i); if(err==NULL) continue; switch(err) { //--- Correct an invalid volume and disabling stop levels in a trading request case MSG_LIB_TEXT_REQ_VOL_LESS_MIN_VOLUME : case MSG_LIB_TEXT_REQ_VOL_MORE_MAX_VOLUME : case MSG_LIB_TEXT_INVALID_VOLUME_STEP : request.volume=symbol_obj.NormalizedLot(request.volume); break; case MSG_SYM_SL_ORDER_DISABLED : request.sl=0; break; case MSG_SYM_TP_ORDER_DISABLED : request.tp=0; break; //--- If unable to select the position lot, return "abort trading attempt" since the funds are insufficient even for the minimum lot case MSG_LIB_TEXT_NOT_ENOUTH_MONEY_FOR : request.volume=this.CorrectVolume(request.price,order_type,symbol_obj,DFUN); if(request.volume==0) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_NOT_POSSIBILITY_CORRECT_LOT); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_EXIT; break; } //--- No quotes to process the request case 10021 : trade_obj.SetResultRetcode(10021); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT - wait 5 seconds //--- No connection to the trade server case 10031 : trade_obj.SetResultRetcode(10031); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT - wait 5 seconds //--- Proximity to the order activation level is handled by five-second waiting - during this time, the price may go beyond the freeze level case MSG_LIB_TEXT_SL_LESS_FREEZE_LEVEL : case MSG_LIB_TEXT_TP_LESS_FREEZE_LEVEL : case MSG_LIB_TEXT_PR_LESS_FREEZE_LEVEL : return (ENUM_ERROR_CODE_PROCESSING_METHOD)5000; // ERROR_CODE_PROCESSING_METHOD_WAIT - wait 5 seconds default: break; } } //--- No errors - return ОК trade_obj.SetResultRetcode(0); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); return ERROR_CODE_PROCESSING_METHOD_OK; } //+------------------------------------------------------------------+

The code comments of the method listing feature all actions directed at handling of errors returned by the trade server.

Implement the private method for opening a position:

//+------------------------------------------------------------------+ //| Open a position | //+------------------------------------------------------------------+ template<typename SL,typename TP> bool CTrading::OpenPosition(const ENUM_POSITION_TYPE type, const double volume, const string symbol, const ulong magic=ULONG_MAX, const SL sl=0, const TP tp=0, const string comment=NULL, const ulong deviation=ULONG_MAX) { //--- Set the trading request result as 'true' and the error flag as "no errors" bool res=true; this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_NO_ERROR; ENUM_ORDER_TYPE order_type=(ENUM_ORDER_TYPE)type; ENUM_ACTION_TYPE action=(ENUM_ACTION_TYPE)order_type; //--- Get a symbol object by a symbol name. If failed to get CSymbol *symbol_obj=this.m_symbols.GetSymbolObjByName(symbol); //--- If failed to get - write the "internal error" flag, display the message in the journal and return 'false' if(symbol_obj==NULL) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_ERROR_FAILED_GET_SYM_OBJ)); return false; } //--- get a trading object from a symbol object CTradeObj *trade_obj=symbol_obj.GetTradeObj(); //--- If failed to get - write the "internal error" flag, display the message in the journal and return 'false' if(trade_obj==NULL) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_ERROR_FAILED_GET_TRADE_OBJ)); return false; } //--- Set the prices //--- If failed to set - write the "internal error" flag, set the error code in the return structure, //--- display the message in the journal and return 'false' if(!this.SetPrices(order_type,0,sl,tp,0,DFUN,symbol_obj)) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; trade_obj.SetResultRetcode(10021); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(10021)); // No quotes to process the request return false; } //--- Write the volume to the request structure this.m_request.volume=volume; //--- Get the method of handling errors from the CheckErrors() method while checking for errors in the request parameters ENUM_ERROR_CODE_PROCESSING_METHOD method=this.CheckErrors(this.m_request.volume,symbol_obj.Ask(),action,order_type,symbol_obj,trade_obj,DFUN,0,this.m_request.sl,this.m_request.tp); //--- In case of trading limitations, funds insufficiency, //--- if there are limitations by StopLevel or FreezeLevel ... if(method!=ERROR_CODE_PROCESSING_METHOD_OK) { //--- If trading is completely disabled, set the error code to the return structure, //--- display a journal message, play the error sound and exit if(method==ERROR_CODE_PROCESSING_METHOD_DISABLE) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_TRADING_DISABLE); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRADING_DISABLE)); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); return false; } //--- If the check result is "abort trading operation" - set the last error code to the return structure, //--- display a journal message, play the error sound and exit if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { int code=this.m_list_errors.At(this.m_list_errors.Total()-1); if(code!=NULL) { trade_obj.SetResultRetcode(code); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); } if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRADING_OPERATION_ABORTED)); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); return false; } //--- If the check result is "waiting" - set the last error code to the return structure and display the message in the journal if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { int code=this.m_list_errors.At(this.m_list_errors.Total()-1); if(code!=NULL) { trade_obj.SetResultRetcode(code); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); } if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_CREATE_PENDING_REQUEST)); //--- Instead of creating a pending request, we temporarily wait the required time period (the CheckErrors() method result is returned) ::Sleep(method); //--- after waiting, update all data symbol_obj.Refresh(); } //--- If the check result is "create a pending request", do nothing temporarily if(this.m_err_handling_behavior==ERROR_HANDLING_BEHAVIOR_PENDING_REQUEST) { if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_CREATE_PENDING_REQUEST)); } } //--- In the loop by the number of attempts for(int i=0;i<this.m_total_try;i++) { //--- Send the request res=trade_obj.OpenPosition(type,this.m_request.volume,this.m_request.sl,this.m_request.tp,magic,comment,deviation); //--- If the request is executed successfully or the asynchronous order sending mode is set, play the success sound //--- set for a symbol trading object for this type of trading operation and return 'true' if(res || trade_obj.IsAsyncMode()) { if(this.IsUseSounds()) trade_obj.PlaySoundSuccess(action,order_type); return true; } //--- If the request is not successful, play the error sound set for a symbol trading object for this type of trading operation else { if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRY_N),string(i+1),". ",CMessage::Text(MSG_LIB_SYS_ERROR),": ",CMessage::Text(trade_obj.GetResultRetcode())); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); //--- Get the error handling method method=this.ResultProccessingMethod(trade_obj.GetResultRetcode()); //--- If "Disable trading for the EA" is received as a result of sending a request, enable the disabling flag and end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_DISABLE) { this.SetTradingDisableFlag(true); break; } //--- If "Exit the trading method" is received as a result of sending a request, end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { break; } //--- If "Correct the parameters and repeat" is received as a result of sending a request - //--- correct the parameters and start the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_CORRECT) { this.RequestErrorsCorrecting(this.m_request,order_type,trade_obj.SpreadMultiplier(),symbol_obj,trade_obj); continue; } //--- If "Update data and repeat" is received as a result of sending a request - //--- update data and start the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_REFRESH) { symbol_obj.Refresh(); continue; } //--- If "Wait and repeat" is received as a result of sending a request - //--- in this implementation, we wait the number of milliseconds equal to the 'method' value and move on to the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_WAIT) { ::Sleep(method); continue; } //--- If "Create a pending request" is received as a result of sending a request - //--- create a pending request with the trading request parameters and end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_PENDING) { break; } } } //--- Return the result of sending a trading request in a symbol trading object return res; } //+------------------------------------------------------------------+This method is commented in details directly in the listing and is to be used to open Buy and Sell positions:

//+------------------------------------------------------------------+ //| Open Buy position | //+------------------------------------------------------------------+ template<typename SL,typename TP> bool CTrading::OpenBuy(const double volume, const string symbol, const ulong magic=ULONG_MAX, const SL sl=0, const TP tp=0, const string comment=NULL, const ulong deviation=ULONG_MAX) { //--- Return the result of sending a trading request from the OpenPosition() method return this.OpenPosition(POSITION_TYPE_BUY,volume,symbol,magic,sl,tp,comment,deviation); } //+------------------------------------------------------------------+ //| Open a Sell position | //+------------------------------------------------------------------+ template<typename SL,typename TP> bool CTrading::OpenSell(const double volume, const string symbol, const ulong magic=ULONG_MAX, const SL sl=0, const TP tp=0, const string comment=NULL, const ulong deviation=ULONG_MAX) { //--- Return the result of sending a trading request from the OpenPosition() method return this.OpenPosition(POSITION_TYPE_SELL,volume,symbol,magic,sl,tp,comment,deviation); } //+------------------------------------------------------------------+

The common private method for opening a position indicating the opened

position type is simply called in these methods.

Implementing the private method for placing pending orders:

//+------------------------------------------------------------------+ //| Place a pending order | //+------------------------------------------------------------------+ template<typename PS,typename PL,typename SL,typename TP> bool CTrading::PlaceOrder(const ENUM_ORDER_TYPE order_type, const double volume, const string symbol, const PS price_stop, const PL price_limit=0, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { bool res=true; this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_NO_ERROR; ENUM_ACTION_TYPE action=(ENUM_ACTION_TYPE)order_type; //--- Get a symbol object by a symbol name CSymbol *symbol_obj=this.m_symbols.GetSymbolObjByName(symbol); if(symbol_obj==NULL) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_ERROR_FAILED_GET_SYM_OBJ)); return false; } //--- Get a trading object from a symbol object CTradeObj *trade_obj=symbol_obj.GetTradeObj(); if(trade_obj==NULL) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(MSG_LIB_SYS_ERROR_FAILED_GET_TRADE_OBJ)); return false; } //--- Set the prices //--- If failed to set - write the "internal error" flag, set the error code in the return structure, //--- display the message in the journal and return 'false' if(!this.SetPrices(order_type,price_stop,sl,tp,price_limit,DFUN,symbol_obj)) { this.m_error_reason_flags=TRADE_REQUEST_ERR_FLAG_INTERNAL_ERR; trade_obj.SetResultRetcode(10021); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(DFUN,CMessage::Text(10021)); // No quotes to process the request return false; } //--- In case of trading limitations, funds insufficiency, //--- there are limitations on StopLevel - play the error sound and exit this.m_request.volume=volume; this.m_request.type_filling=type_filling; this.m_request.type_time=type_time; this.m_request.expiration=expiration; ENUM_ERROR_CODE_PROCESSING_METHOD method=this.CheckErrors(this.m_request.volume, this.m_request.price, action, order_type, symbol_obj, trade_obj, DFUN, this.m_request.stoplimit, this.m_request.sl, this.m_request.tp); if(method!=ERROR_CODE_PROCESSING_METHOD_OK) { //--- If trading is completely disabled if(method==ERROR_CODE_PROCESSING_METHOD_DISABLE) { trade_obj.SetResultRetcode(MSG_LIB_TEXT_TRADING_DISABLE); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRADING_DISABLE)); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); return false; } //--- If the check result is "abort trading operation" - set the last error code to the return structure, //--- display a journal message, play the error sound and exit if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { int code=this.m_list_errors.At(this.m_list_errors.Total()-1); if(code!=NULL) { trade_obj.SetResultRetcode(code); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); } if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRADING_OPERATION_ABORTED)); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); return false; } //--- If the check result is "waiting" - set the last error code to the return structure and display the message in the journal if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { int code=this.m_list_errors.At(this.m_list_errors.Total()-1); if(code!=NULL) { trade_obj.SetResultRetcode(code); trade_obj.SetResultComment(CMessage::Text(trade_obj.GetResultRetcode())); } if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_CREATE_PENDING_REQUEST)); //--- Instead of creating a pending request, we temporarily wait the required time period (the CheckErrors() method result is returned) ::Sleep(method); symbol_obj.Refresh(); } //--- If the check result is "create a pending request", do nothing temporarily if(this.m_err_handling_behavior==ERROR_HANDLING_BEHAVIOR_PENDING_REQUEST) { if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_CREATE_PENDING_REQUEST)); } } //--- In the loop by the number of attempts for(int i=0;i<this.m_total_try;i++) { //--- Send the request res=trade_obj.SetOrder(order_type, this.m_request.volume, this.m_request.price, this.m_request.sl, this.m_request.tp, this.m_request.stoplimit, magic, comment, this.m_request.expiration, this.m_request.type_time, this.m_request.type_filling); //--- If the request is executed successfully or the asynchronous order sending mode is set, play the success sound //--- set for a symbol trading object for this type of trading operation and return 'true' if(res || trade_obj.IsAsyncMode()) { if(this.IsUseSounds()) trade_obj.PlaySoundSuccess(action,order_type); return true; } //--- If the request is not successful, play the error sound set for a symbol trading object for this type of trading operation else { if(this.m_log_level>LOG_LEVEL_NO_MSG) ::Print(CMessage::Text(MSG_LIB_TEXT_TRY_N),string(i+1),". ",CMessage::Text(MSG_LIB_SYS_ERROR),": ",CMessage::Text(trade_obj.GetResultRetcode())); if(this.IsUseSounds()) trade_obj.PlaySoundError(action,order_type); method=this.ResultProccessingMethod(trade_obj.GetResultRetcode()); //--- If "Disable trading for the EA" is received as a result of sending a request, enable the disabling flag and end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_DISABLE) { this.SetTradingDisableFlag(true); break; } //--- If "Exit the trading method" is received as a result of sending a request, end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_EXIT) { break; } //--- If "Correct the parameters and repeat" is received as a result of sending a request - //--- correct the parameters and start the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_CORRECT) { this.RequestErrorsCorrecting(this.m_request,order_type,trade_obj.SpreadMultiplier(),symbol_obj,trade_obj); continue; } //--- If "Update data and repeat" is received as a result of sending a request - //--- update data and start the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_REFRESH) { symbol_obj.Refresh(); continue; } //--- If "Wait and repeat" is received as a result of sending a request - //--- in this implementation, we wait the number of milliseconds equal to the 'method' value and move on to the next iteration if(method==ERROR_CODE_PROCESSING_METHOD_WAIT) { Sleep(method); continue; } //--- If "Create a pending request" is received as a result of sending a request - //--- create a pending request with the trading request parameters and end the attempt loop if(method==ERROR_CODE_PROCESSING_METHOD_PENDING) { break; } } } //--- Return the result of sending a trading request in a symbol trading object return res; } //+------------------------------------------------------------------+

This method is commented in details directly in the listing and is to be used to set various types of pending orders:

//+------------------------------------------------------------------+ //| Place BuyStop pending order | //+------------------------------------------------------------------+ template<typename PS,typename SL,typename TP> bool CTrading::PlaceBuyStop(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_BUY_STOP,volume,symbol,price,0,sl,tp,magic,comment,expiration,type_time,type_filling); } //+------------------------------------------------------------------+ //| Place BuyLimit pending order | //+------------------------------------------------------------------+ template<typename PS,typename SL,typename TP> bool CTrading::PlaceBuyLimit(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_BUY_LIMIT,volume,symbol,price,0,sl,tp,magic,comment,expiration,type_time,type_filling); } //+------------------------------------------------------------------+ //| Place BuyStopLimit pending order | //+------------------------------------------------------------------+ template<typename PS,typename PL,typename SL,typename TP> bool CTrading::PlaceBuyStopLimit(const double volume, const string symbol, const PS price_stop, const PL price_limit, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { #ifdef __MQL5__ //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_BUY_STOP_LIMIT,volume,symbol,price_stop,price_limit,sl,tp,magic,comment,expiration,type_time,type_filling); //--- MQL4 #else return true; #endif } //+------------------------------------------------------------------+ //| Place SellStop pending order | //+------------------------------------------------------------------+ template<typename PS,typename SL,typename TP> bool CTrading::PlaceSellStop(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_SELL_STOP,volume,symbol,price,0,sl,tp,magic,comment,expiration,type_time,type_filling); } //+------------------------------------------------------------------+ //| Place SellLimit pending order | //+------------------------------------------------------------------+ template<typename PS,typename SL,typename TP> bool CTrading::PlaceSellLimit(const double volume, const string symbol, const PS price, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_SELL_LIMIT,volume,symbol,price,0,sl,tp,magic,comment,expiration,type_time,type_filling); } //+------------------------------------------------------------------+ //| Place SellStopLimit pending order | //+------------------------------------------------------------------+ template<typename PS,typename PL,typename SL,typename TP> bool CTrading::PlaceSellStopLimit(const double volume, const string symbol, const PS price_stop, const PL price_limit, const SL sl=0, const TP tp=0, const ulong magic=ULONG_MAX, const string comment=NULL, const datetime expiration=0, const ENUM_ORDER_TYPE_TIME type_time=WRONG_VALUE, const ENUM_ORDER_TYPE_FILLING type_filling=WRONG_VALUE) { #ifdef __MQL5__ //--- Return the result of sending a trading request using the PlaceOrder() method return this.PlaceOrder(ORDER_TYPE_SELL_STOP_LIMIT,volume,symbol,price_stop,price_limit,sl,tp,magic,comment,expiration,type_time,type_filling); //--- MQL4 #else return true; #endif } //+------------------------------------------------------------------+

The remaining methods are necessary for closing positions and removing pending orders. The methods modifying positions and orders are similar to private methods for opening positions/placing pending orders. All method codes have detailed comments. All files are attached below.

This concludes all the work with the trading class at this stage.

Now it only remains to make some changes in the library's CEngine base object class.

Considering the floating nature of the minimum stop and pending order levels (StopLevel), we need to set the spread multiplier since a spread

multiplied by a certain value is often used in such cases to specify acceptable stop order distance. This means we need the method allowing to

set the spread multiplier for the trading class.

Declare the following method

in the public section of the class:

//--- Set the spread multiplier for symbol trading objects in the symbol collection void SetSpreadMultiplier(const uint value=1,const string symbol=NULL) { this.m_trading.SetSpreadMultiplier(value,symbol); } //--- Open (1) Buy, (2) Sell position

The method simply calls the trading class method of the same name we already examined in the previous article allowing to set both a single common multiplier for all used symbols and individual multipliers for specified symbols.

Since the trading class will soon use the timer to work with pending requests, create

the new timer counter for the trading class in the CEngine class constructor:

//+------------------------------------------------------------------+ //| CEngine constructor | //+------------------------------------------------------------------+ CEngine::CEngine() : m_first_start(true), m_last_trade_event(TRADE_EVENT_NO_EVENT), m_last_account_event(WRONG_VALUE), m_last_symbol_event(WRONG_VALUE), m_global_error(ERR_SUCCESS) { this.m_is_hedge=#ifdef __MQL4__ true #else bool(::AccountInfoInteger(ACCOUNT_MARGIN_MODE)==ACCOUNT_MARGIN_MODE_RETAIL_HEDGING) #endif; this.m_is_tester=::MQLInfoInteger(MQL_TESTER); this.m_list_counters.Sort(); this.m_list_counters.Clear(); this.CreateCounter(COLLECTION_ORD_COUNTER_ID,COLLECTION_ORD_COUNTER_STEP,COLLECTION_ORD_PAUSE); this.CreateCounter(COLLECTION_ACC_COUNTER_ID,COLLECTION_ACC_COUNTER_STEP,COLLECTION_ACC_PAUSE); this.CreateCounter(COLLECTION_SYM_COUNTER_ID1,COLLECTION_SYM_COUNTER_STEP1,COLLECTION_SYM_PAUSE1); this.CreateCounter(COLLECTION_SYM_COUNTER_ID2,COLLECTION_SYM_COUNTER_STEP2,COLLECTION_SYM_PAUSE2); this.CreateCounter(COLLECTION_REQ_COUNTER_ID,COLLECTION_REQ_COUNTER_STEP,COLLECTION_REQ_PAUSE); ::ResetLastError(); #ifdef __MQL5__ if(!::EventSetMillisecondTimer(TIMER_FREQUENCY)) { ::Print(DFUN_ERR_LINE,CMessage::Text(MSG_LIB_SYS_FAILED_CREATE_TIMER),(string)::GetLastError()); this.m_global_error=::GetLastError(); } //---__MQL4__ #else if(!this.IsTester() && !::EventSetMillisecondTimer(TIMER_FREQUENCY)) { ::Print(DFUN_ERR_LINE,CMessage::Text(MSG_LIB_SYS_FAILED_CREATE_TIMER),(string)::GetLastError()); this.m_global_error=::GetLastError(); } #endif //--- } //+------------------------------------------------------------------+

In the CEngine class timer, add the block of working with the trading class timer:

//+------------------------------------------------------------------+ //| CEngine timer | //+------------------------------------------------------------------+ void CEngine::OnTimer(void) { //--- Timer of the collections of historical orders and deals, as well as of market orders and positions int index=this.CounterIndex(COLLECTION_ORD_COUNTER_ID); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If unpaused, work with the order, deal and position collections events if(counter.IsTimeDone()) this.TradeEventsControl(); } //--- If this is a tester, work with collection events by tick else this.TradeEventsControl(); } } //--- Account collection timer index=this.CounterIndex(COLLECTION_ACC_COUNTER_ID); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If unpaused, work with the account collection events if(counter.IsTimeDone()) this.AccountEventsControl(); } //--- If this is a tester, work with collection events by tick else this.AccountEventsControl(); } } //--- Timer 1 of the symbol collection (updating symbol quote data in the collection) index=this.CounterIndex(COLLECTION_SYM_COUNTER_ID1); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If the pause is over, update quote data of all symbols in the collection if(counter.IsTimeDone()) this.m_symbols.RefreshRates(); } //--- In case of a tester, update quote data of all collection symbols by tick else this.m_symbols.RefreshRates(); } } //--- Timer 2 of the symbol collection (updating all data of all symbols in the collection and tracking symbl and symbol search events in the market watch window) index=this.CounterIndex(COLLECTION_SYM_COUNTER_ID2); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If the pause is over if(counter.IsTimeDone()) { //--- update data and work with events of all symbols in the collection this.SymbolEventsControl(); //--- When working with the market watch list, check the market watch window events if(this.m_symbols.ModeSymbolsList()==SYMBOLS_MODE_MARKET_WATCH) this.MarketWatchEventsControl(); } } //--- If this is a tester, work with events of all symbols in the collection by tick else this.SymbolEventsControl(); } } //--- Trading class timer index=this.CounterIndex(COLLECTION_REQ_COUNTER_ID); if(index>WRONG_VALUE) { CTimerCounter* counter=this.m_list_counters.At(index); if(counter!=NULL) { //--- If this is not a tester if(!this.IsTester()) { //--- If unpaused, work with the list of pending requests if(counter.IsTimeDone()) this.m_trading.OnTimer(); } //--- In case of the tester, work with the list of pending orders by tick else this.m_trading.OnTimer(); } } } //+------------------------------------------------------------------+

Slightly change the method for the complete position closure:

//+------------------------------------------------------------------+ //| Close a position in full | //+------------------------------------------------------------------+ bool CEngine::ClosePosition(const ulong ticket,const string comment=NULL,const ulong deviation=ULONG_MAX) { return this.m_trading.ClosePosition(ticket,WRONG_VALUE,comment,deviation); } //+------------------------------------------------------------------+

Since we now have the common position closure method both for the complete and partial closure, we need to pass -1 as the closed position volume

for the complete position closure.

This concludes the necessary changes and improvements for handling the trade server return codes.

Testing

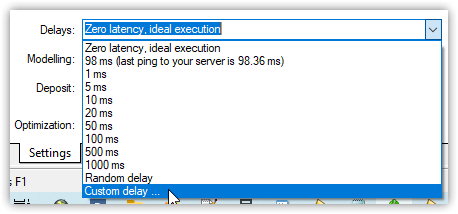

To check handling of errors returned by the trade server, it would be reasonable to set the trading conditions causing errors, for example execution delays. During the delay, the price changes causing the appropriate error.

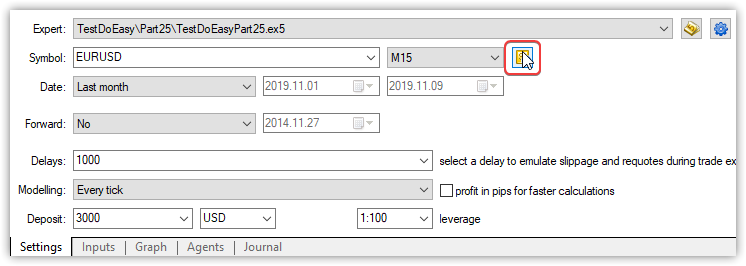

To perform the test, let's use the EA from the previous article and save it to \MQL5\Experts\TestDoEasy\ Part25\ under the name TestDoEasyPart25.mq5.

We can launch the EA with no changes, but let's make some improvements first.

In the block of the EA inputs, change

the default slippage from zero to five points and add the spread

multiplier:

//--- input variables input ulong InpMagic = 123; // Magic number input double InpLots = 0.1; // Lots input uint InpStopLoss = 50; // StopLoss in points input uint InpTakeProfit = 50; // TakeProfit in points input uint InpDistance = 50; // Pending orders distance (points) input uint InpDistanceSL = 50; // StopLimit orders distance (points) input uint InpSlippage = 5; // Slippage in points input uint InpSpreadMultiplier = 1; // Spread multiplier for adjusting stop-orders by StopLevel sinput double InpWithdrawal = 10; // Withdrawal funds (in tester) sinput uint InpButtShiftX = 40; // Buttons X shift sinput uint InpButtShiftY = 10; // Buttons Y shift input uint InpTrailingStop = 50; // Trailing Stop (points) input uint InpTrailingStep = 20; // Trailing Step (points) input uint InpTrailingStart = 0; // Trailing Start (points) input uint InpStopLossModify = 20; // StopLoss for modification (points) input uint InpTakeProfitModify = 60; // TakeProfit for modification (points) sinput ENUM_SYMBOLS_MODE InpModeUsedSymbols = SYMBOLS_MODE_CURRENT; // Mode of used symbols list sinput string InpUsedSymbols = "EURUSD,AUDUSD,EURAUD,EURCAD,EURGBP,EURJPY,EURUSD,GBPUSD,NZDUSD,USDCAD,USDJPY"; // List of used symbols (comma - separator) sinput bool InpUseSounds = true; // Use sounds

In the library initialization function, set the spread multiplier for all

trading objects of all used symbols and comment out the block setting control

over the increase in symbol parameter values to avoid tracking and sending redundant entries to the tester journal: