Applying L1 Trend Filtering in MetaTrader 5

- long-term dynamics of the data are preserved;

- short-term fluctuations and noise are suppressed;

- structural breakpoints (changes in trend slope) are automatically detected.

![]()

Contents

- Introduction

- 1. Problem formulation of trend filtering

1.1. Hodrick–Prescott filter

1.2. L1 trend filtering method

1.3. Role of the regularization parameter λ

1.4. Geometric interpretation

1.5. Algorithm for computing λmax - 2. MQL5 methods for calculation the L1 trend

2.1. L1TrendFilterLambdaMax

2.2. L1TrendFilter - 3. Examples of L1 trend computation

3.1. L1 trend on synthetic data (random walk)

3.2. L1 trend for S&P 500 price series

3.3. Scaling properties of λmax

3.3.1. Numerical experiment for Brownian motion

3.3.2. Scaling for financial time series

3.3.3. Practical implications of scaling

3.4. L1 trend indicators

3.4.1. L1TrendFilter.mq5 - L1 trend indicator

3.4.2. L1TrendFilterSlope.mq5 - L1 trend slope indicator

3.4.3. L1TrendFilterSlopeSign.mq5 - trend direction indicator - 3.4.4. Volatility Indicators Based on the L1 Trend

3.4.4.1. L1Volatility.mq5 - residual volatility indicator

3.4.4.2. L1VolatilitySmoothed.mq5 - smoothed residual volatility indicator

3.4.4.3. L1VolatilityAbsolute.mq5 - absolute volatility indicator

3.4.4.4. L1VolatilityNormalized.mq5 - normalized volatility indicator

3.4.4.5. L1VolatilityNormalizedSmoothed.mq5 - smoothed normalized volatility indicator

3.4.4.6. L1VolatilityRegime.mq5 - market regime detection based on volatility -

3.5. Application of L1 trend in trading strategies

3.5.1. Moving Average strategy

3.5.1.1. General methodology for evaluating L1 trend filtering efficiency

3.5.1.2. Results for Moving Average strategy

3.5.2. MACD strategy

3.5.2.1. Results for MACD strategy

3.5.3. ADX strategy

3.5.3.1. Results for ADX strategy

3.5.4. EMA strategy

3.5.4.1. Results for EMA strategy

3.5.5. Summary on the use of the L1 filter in MovingAverage, MACD, ADX, and EMA trading strategies - Conclusion

Introduction

Financial time series are characterized by high noise levels, frequent outliers, and changing market regimes. In practical trading systems, this manifests in a simple and measurable way: classical “smooth” filters (moving averages, HP) lag behind, blur the moments of slope changes, and often interpret local corrections as reversals — as a result, the number of false entries/exits increases, the Profit Factor decreases, and drawdown grows. In addition, the selection of the regularization parameter λ is usually reduced to manual tuning and does not transfer well across instruments, timeframes, and history lengths.This paper proposes a practical solution to these problems based on L1 trend filtering: optimization with L1 regularization of second differences automatically produces a piecewise-linear approximation with explicit breakpoints. The key advantages are a clear interpretation of breakpoints as regime changes, the ability to set the scale of regularization via computing λmax and moving to a relative parameter λ = coef · λmax, as well as linear computational complexity suitable for implementation in MQL5.

We present not only the theory, but also a complete practical roadmap: methods for computing λmax and the L1 trend, three indicators (trend, slope, slope sign), seven L1-trend volatility indicators, integration into Expert Advisors, and a reproducible testing protocol (four filtering modes, balance/equity export, and visualization).

1. Formulation of the Trend Filtering Problem

We consider a scalar time series represented as the sum of two components:

![]() ,

,

where ![]() is the trend component, and

is the trend component, and ![]() is a noise or an irregular component.

is a noise or an irregular component.

The objective is to estimate the trend ![]() from the observed data

from the observed data ![]() .

.

The problem can be expressed as a trade-off between fidelity to the original data and smoothness of the estimated trend.

1.1. Hodrick–Prescott Filter

The Hodrick–Prescott filter defines the trend as the solution to the minimization problem:

,

,

where the parameter λ controls the degree of smoothing.

Main properties of the HP filter:

- Linearity with respect to the data;

- Computational complexity O(n);

- For small λ, the trend approximates the original data;

- For large λ, the trend tends to the best linear approximation.

However, the HP filter always produces a smooth trend and poorly detects sharp changes in slope.

1.2. L1 Trend Filtering Method

The main idea of L1 trend filtering is to find a trend that is close to the original data but contains as few changes in slope as possible. Unlike classical smoothing methods that minimize the squared curvature, the L1 approach minimizes the sum of absolute values of second differences.

This leads to a fundamentally different result:

- most second differences become equal to zero,

- the trend is automatically split into linear segments.

Thus, the L1 filter does not attempt to make the trend smooth but instead finds the minimal number of structural changes that explain the observed data. This makes the method particularly suitable for financial time series, where dynamics often consist of sequences of quasi-linear growth and decline phases.

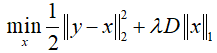

In L1 trend filtering, the quadratic penalty on second differences is replaced by the L1 norm, and the trend is defined as the solution to a convex optimization problem:

In matrix form:

where:

- y — input time series;

- x — the estimated trend;

- D — second-difference matrix;

- λ>=0 — regularization parameter.

The use of the L1 norm leads to a fundamentally different result: many second differences become zero, meaning that the trend is piecewise linear.

The second difference is defined as:

If ![]() , then the points

, then the points ![]() lie on a straight line.

lie on a straight line.

Therefore, a zero second difference corresponds to a linear segment of the trend, while a nonzero second difference corresponds to a breakpoint. The L1 norm promotes sparsity in the vector Dx, meaning that most second differences become zero. This implies that over the corresponding intervals, the trend is linear. Points where second differences are nonzero are interpreted as trend breakpoints.

Thus, the L1 Trend Filtering method automatically constructs the trend as a set of linear segments connected at points of structural change.

Main properties of L1 trend filtering:

- The trend consists of linear segments;

- Breakpoints are interpreted as structural changes in the time series;

- At λ = 0, the trend coincides with the original data;

- For sufficiently large λ, the trend becomes exactly the best linear approximation;

- Computational complexity remains linear in the number of observations.

1.3. Role of the Regularization Parameter λ

The parameter λ controls the trade-off between approximation accuracy and trend complexity:

| Value of λ | Nature of the solution |

|---|---|

| λ=0 | x=y, no smoothing |

| Small λ | Weak smoothing, many breakpoints |

| Medium λ | Piecewise-linear trend |

| Large λ | Nearly linear trend |

| λ≥λmax | Strictly linear trend |

Table 1. Dependence of the L1 trend on the regularization parameter λ

Thus, λ controls the number and locations of trend breakpoints.

1.4. Geometric Interpretation of the Problem

The desired trend x can be viewed as a point in an n-dimensional space. The first term of the objective function, responsible for approximation accuracy, defines a Euclidean ball centered at the observation point y: the closer x is to y, the smaller the error.The regularization term with the L1 norm of second differences defines a convex polyhedral set (polyhedron). Unlike smooth ellipsoids arising in L2 regularization, this polyhedron has sharp vertices. These vertices correspond to situations where some second differences of the trend are equal to zero.

It is precisely the presence of sharp corners in the L1 norm that leads to sparse solutions: the optimal solution tends to lie at a vertex of the polyhedron, where only some constraints are active. This means that most second differences become zero, and the trend automatically takes a piecewise-linear form.

The optimal solution corresponds to the first point of contact between the Euclidean ball and the L1 polyhedron. At this point, the trend consists of linear segments connected at a limited number of breakpoints.

The parameter λmax corresponds to the situation where the Euclidean ball touches the L1 polyhedron not at a vertex but along the subspace of linear functions. In this case, all second differences are zero, and the trend is strictly linear.

For λ ≥ λmax, none of the L1 constraints become active, so further increases in regularization do not change the solution, and the trend remains linear.

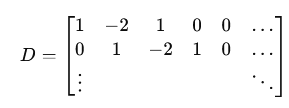

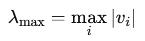

1.5. Algorithm for Computing λmax

Consider the computation of the maximum regularization parameter λmax for an input vector y of length N.

1. Construct the second-difference matrix D of size (N−2)×N:

2. Compute the curvature vector Dy.

3. Solve the system of linear equations:

![]()

4. Take the maximum (by absolute value) element of vector v:

For financial time series, the parameter λmax has important practical significance:

- It allows normalization of the regularization parameter;

- It makes the choice of λ independent of the data scale;

- It simplifies comparison across different time series;

- It allows interpreting λ as a fraction of the maximum regularization.

Using a relative parameter of the form: λ=coef_lambda_max⋅λmax, where coef_lambda_max ∈ (0,1), greatly simplifies practical application.

In the following examples of indicators and Expert Advisors, λ will be used in units of λmax, while the parameter settings will specify the multiplier coef_lambda_max.

2. MQL5 Methods for Calculation the L1 Trend

For practical use of L1 trend filtering, two methods are implemented for vectors of type double and float.

- L1TrendFilterLambdaMax computes the maximum regularization parameter;

- L1TrendFilter computes the L1 trend for a given value of the regularization parameter λ, which can also be specified in units of λmax.

2.1. L1TrendFilterLambdaMax

Method for calculation the maximum regularization parameter λmax for a data vector.

Calculation for vector<double>:

bool vector::L1TrendFilterLambdaMax( double &lambda_max // the maximum value of the regularization parameter lambda )Calculation for vector<float>:

bool vectorf::L1TrendFilterLambdaMax( float &lambda_max // the maximum value of the regularization parameter lambda );

Parameters

lambda

[out] The maximum value of the regularization parameter λmax, or -1 in case of an error.

Return value

Returns true if successful.

Note

Memory consumption grows linearly with the vector size.

2.2. L1TrendFilter

Method for calculation the L1 trend for a data vector.

Calculation for vector<double>:

bool vector::L1TrendFilter( double lambda, // regularization parameter bool relative, // flag indicating lambda is in λmax units vector& result // output vector with L1 filtering result );

Calculation for vector<float>:

bool vectorf::L1TrendFilter( float lambda, // regularization parameter bool relative, // flag indicating lambda is in λmax units vectorf& result // output vector with L1 filtering result );

Parameters

lambda

[in] Value of the regularization parameter lambda (if relative = true the lambda is defined in range [0, 1] as fraction of λmax).

relative

[in] Flag indicating how λ is specified. If true, λ is given in units of λmax; otherwise, the absolute value is used.

result

[out] Vector containing the result of L1 filtering.

Return value

Returns true if successful.

Note

Memory consumption grows linearly with the vector size.

Recommended ranges for λ (relative mode).

| λ multiplier | Result |

|---|---|

| 0.005 – 0.015 | almost L2, noisy |

| 0.02 – 0.04 | micro-segments |

| 0.04 – 0.07 | optimal for signals |

| 0.07 – 0.12 | medium-term trends |

| 0.12 – 0.25 | market regimes |

| > 0.3 | few segments |

Table.2. Working ranges of λ in units of λmax

For practical applications, it is recommended to use multipliers in the range 0.04–0.25.

3. Examples of Application

In this section, we consider L1 trend calculations on simulated Brownian motion data, on S&P 500 price data, as well as scaling properties of λmax for both Brownian motion and FOREX market data.

We also present three indicator variants that help determine optimal regularization parameters (multipliers of λmax) for obtaining the best L1 trend decomposition for specific symbols and timeframes.

Additionally, results of filtering trading signals (alignment with the L1 trend) are presented for the MovingAverage, MACD, ADX, and EMA strategies.

3.1. L1 Trend Calculation on Simulated Data (Random Walk)

As an example, consider computing the L1 trend with different values of the regularization parameter λ on simulated Brownian motion data.

Script code:

//+------------------------------------------------------------------+ //| TestL1Trend.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| http://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #property script_show_inputs #include <Graphics\Graphic.mqh> //+------------------------------------------------------------------+ //| Generate Brown movement data | //+------------------------------------------------------------------+ void BMData(vector<double> &data,int &data_count) { data.Resize(data_count); data[0] = 0.0; for(int i=1; i<data_count; i++) data[i] = data[i-1] + (MathRand()/32767.0 - 0.5); } //+------------------------------------------------------------------+ //| CopyValues | //+------------------------------------------------------------------+ bool CopyValues(vector<double> &data_v,double &data[]) { int data_count=(int)data.Size(); if(data_count==0) return(false); ArrayResize(data,data.Size()); for(int i=0; i<data_count; i++) data[i]=data_v[i]; return(true); } //+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart() { MathSrand(1); int data_count=1000; vector<double> data_test; BMData(data_test,data_count); //--- prepare arrays for chart double x[],y[]; ArrayResize(x,data_count); ArrayResize(y,data_count); for(int i=0; i<data_count; i++) x[i]=i; //--- CGraphic graphic; long chart=0; string name="test"; if(ObjectFind(chart,name)<0) graphic.Create(chart,name,0,0,0,1000,600); else graphic.Attach(chart,name); graphic.BackgroundMain("L1 Trend filtering (random walk) with different lambda"); graphic.BackgroundMainSize(16); graphic.HistoryNameWidth(60); graphic.HistoryColor(ColorToARGB(clrGray,255)); graphic.XAxis().AutoScale(false); graphic.XAxis().Min(0); graphic.XAxis().Max(data_count); //--- CopyValues(data_test,y); graphic.CurveAdd(x,y,CURVE_LINES,"Data").LinesWidth(1); //--- L1TrendFilterLambdaMax double lambda_max=0.0; if(data_test.L1TrendFilterLambdaMax(lambda_max)) PrintFormat("lambda_max=%f",lambda_max); //--- vector<double> data_l1; const double lambda_factors[]= {1.0,0.9,0.8,0.5,0.25,0.1,0.01,0.05,0.001,0.0005}; for(int i=0; i<ArraySize(lambda_factors); i++) { double lambda=lambda_max*lambda_factors[i]; PrintFormat("%d. lambda=%f",i+1,lambda); bool res=data_test.L1TrendFilter(lambda_factors[i],true,data_l1); if(res) { CopyValues(data_l1,y); graphic.CurveAdd(x,y,CURVE_LINES,"lambda="+DoubleToString(lambda,0)).LinesWidth(3); } } //--- graphic.CurvePlotAll(); graphic.Update(); DebugBreak(); } //+------------------------------------------------------------------+Output:

TestL1Trend (EURUSD,H1) lambda_max=51703.353749 TestL1Trend (EURUSD,H1) 1. lambda=51703.353749 TestL1Trend (EURUSD,H1) 2. lambda=46533.018374 TestL1Trend (EURUSD,H1) 3. lambda=41362.682999 TestL1Trend (EURUSD,H1) 4. lambda=25851.676874 TestL1Trend (EURUSD,H1) 5. lambda=12925.838437 TestL1Trend (EURUSD,H1) 6. lambda=5170.335375 TestL1Trend (EURUSD,H1) 7. lambda=517.033537 TestL1Trend (EURUSD,H1) 8. lambda=2585.167687 TestL1Trend (EURUSD,H1) 9. lambda=51.703354 TestL1Trend (EURUSD,H1) 10. lambda=25.851677

In this example, it can be seen that decreasing the regularization parameter λ allows for a more detailed decomposition into trend segments (Fig.1).

If λ ≥ λmax, the solution becomes a straight line corresponding to linear regression (the global trend).

Fig.1. Example of L1 filter computation with different values of λ on Brownian motion data

Functions for computing the L1 trend are available for both double and float vectors.

Test script for comparing the calculations is presented below.

//+------------------------------------------------------------------+ //| TestL1TrendFloatDouble.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| http://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include <Graphics\Graphic.mqh> uint32_t ExtSeed=1; //+------------------------------------------------------------------+ //| Generate Brown movement data | //+------------------------------------------------------------------+ template<typename T> void BMData(vector<T> &data,uint64_t data_count) { MathSrand(ExtSeed); data.Resize(data_count); data[0] = 0.0; for(uint64_t i=1; i<data_count; i++) data[i] = data[i-1] + T(MathRand()/32767.0 - 0.5); } //+------------------------------------------------------------------+ //| CopyValues | //+------------------------------------------------------------------+ template<typename T> bool CopyValues(double &data[],const vector<T> &data_v) { if(ArrayResize(data,data.Size())!=data.Size()) return(false); for(uint64_t i=0; i<data.Size(); i++) data[i]=data_v[i]; return(true); } //+------------------------------------------------------------------+ //| L1TrendCalculate | //+------------------------------------------------------------------+ template<typename T> bool L1TrendCalculate(double &result[],uint64_t data_count,double lambda,bool lambda_is_relative) { vector<T> data_test; BMData(data_test,data_count); vector<T> vres; if(!data_test.L1TrendFilter((T)lambda,lambda_is_relative,vres)) return(false); if(ArrayResize(result,(uint32_t)vres.Size())!=vres.Size()) return(false); for(uint64_t n=0; n<result.Size(); n++) result[n]=vres[n]; return(true); } //+------------------------------------------------------------------+ //| TestRun | //+------------------------------------------------------------------+ bool TestRun(uint32_t data_count,uint32_t mode) { //--- create graph CGraphic graphic; long chart=0; string name="L1TrendTest"; if(ObjectFind(chart,name)<0) graphic.Create(chart,name,0,0,0,1280,600); else graphic.Attach(chart,name); string mode_name="("; if((mode&1)==1) mode_name+="DOUBLE"; if((mode&3)==3) mode_name+=" & "; if((mode&2)==2) mode_name+="FLOAT"; mode_name+=")"; graphic.BackgroundMain("L1Trend filtering (random walk) with different lambda "+mode_name); graphic.BackgroundMainSize(16); graphic.HistoryNameWidth(60); graphic.HistoryColor(ColorToARGB(clrGray,255)); graphic.XAxis().AutoScale(false); graphic.XAxis().Min(0); graphic.XAxis().Max(data_count); //--- prepare arrays double x[]; double y[]; if(ArrayResize(x,data_count)!=data_count) return(false); for(uint32_t i=0; i<data_count; i++) x[i]=i; vector<double> v; BMData(v,data_count); v.Swap(y); graphic.CurveAdd(x,y,CURVE_LINES,"Data").LinesWidth(1); //--- calculate const double lambda_factors[]= {1.0,0.9,0.8,0.5,0.25,0.1,0.01,0.05,0.001,0.0005}; //--- double if((mode&1)==1) { for(uint64_t i=0; i<lambda_factors.Size(); i++) { if(L1TrendCalculate<double>(y,data_count,lambda_factors[i],true)) graphic.CurveAdd(x,y,CURVE_LINES,"DBL="+DoubleToString(lambda_factors[i],4)).LinesWidth(4); } } //--- float if((mode&2)==2) { for(uint64_t i=0; i<lambda_factors.Size(); i++) { if(L1TrendCalculate<float>(y,data_count,(float)lambda_factors[i],true)) graphic.CurveAdd(x,y,CURVE_LINES,"FLT="+DoubleToString(lambda_factors[i],4)).LinesWidth(2); } } //--- update graphic.CurvePlotAll(); graphic.Update(); return(true); } //+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart() { for(uint32_t n=0; !IsStopped(); n++,Sleep(1000)) { TestRun(1000,1+n%3); if((n%3)==2) ExtSeed++; } } //+------------------------------------------------------------------+

Output:

3.2. L1 Trend Calculation for S&P 500 Price Series

Consider the computation of log(S&P 500) from the original paper l_1 Trend Filtering, S.J. Kim, K. Koh, S. Boyd, and D. Gorinevsky, SIAM Review, problems and techniques section, 51(2):339–360, May 2009.

To run the script, data from the file "snp500.txt" is used. It must be placed in the folder: terminal_data_folder\MQL5\Files

//+------------------------------------------------------------------+ //| TestL1TrendFilterSP500.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| http://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #property script_show_inputs #include <Graphics\Graphic.mqh> //+------------------------------------------------------------------+ //| LoadData | //+------------------------------------------------------------------+ void LoadData(string filename,vector<double> &data,int &data_count) { data_count=0; ResetLastError(); int file_handle=FileOpen(filename,FILE_READ|FILE_TXT|FILE_ANSI); if(file_handle!=INVALID_HANDLE) { while(!FileIsEnding(file_handle)) { string str=FileReadString(file_handle); if(data.Size()<=(ulong)data_count) data.Resize(data_count+1); data[data_count]=StringToDouble(str); data_count++; } FileClose(file_handle); } else PrintFormat("Failed to open %s file, Error code = %d",filename,GetLastError()); //--- data.Resize(data_count); } //+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart() { long chart=0; string name="log SP500"; int data_count=0; vector<double> data_sp500; LoadData("snp500.txt",data_sp500,data_count); vector<double> data_l1_sp500; data_l1_sp500.Resize(data_count); //--- L1TrendFilterLambdaMax double lambda_max=0.0; if(data_sp500.L1TrendFilterLambdaMax(lambda_max)) PrintFormat("Lambda_max=%f",lambda_max); double lambda=50; //--- L1TrendFilter if(data_sp500.L1TrendFilter(lambda,false,data_l1_sp500)) { //--- prepare arrays for chart double x[],y[],y2[]; ArrayResize(x,data_count); ArrayResize(y,data_count); ArrayResize(y2,data_count); for(int i=0; i<data_count; i++) { x[i]=i; y[i]=data_sp500[i]; y2[i]=data_l1_sp500[i]; } //--- CGraphic graphic; if(ObjectFind(chart,name)<0) graphic.Create(chart,name,0,0,0,1000,600); else graphic.Attach(chart,name); graphic.BackgroundMain("log SP500 L1 trend filtering"); graphic.BackgroundMainSize(16); graphic.HistoryNameWidth(60); graphic.HistoryColor(ColorToARGB(clrGray,255)); graphic.XAxis().AutoScale(false); graphic.XAxis().Min(0); graphic.XAxis().Max(data_count); graphic.XAxis().DefaultStep(100); graphic.CurveAdd(x,y,CURVE_LINES,"SP500").LinesWidth(1); graphic.CurveAdd(x,y2,CURVE_LINES,"L1 trend").LinesWidth(3); graphic.CurvePlotAll(); graphic.Update(); DebugBreak(); } } //+------------------------------------------------------------------+

The result of the script execution is shown in Fig.2.

Fig.2. Example of L1-trend estimation for log price series of the S&P 500 index

In the Experts tab, the value of λmax for the given time series will be displayed:

TestL1TrendFilterSP500 (EURUSD,H1) Lambda_max=37394.835512

This script demonstrates the use of the methods L1TrendFilterLambdaMax and L1TrendFilter with a fixed value λ = 50, as in the original paper by the method’s authors.

In the following examples, instead of absolute values of the regularization parameter λ, relative values (in units of λmax) will be used with the flag relative = true.

3.3. Scaling Properties of λmax

The parameter λmax plays a key role in L1 filtering, as it defines the upper bound of regularization at which the solution degenerates into a global linear approximation. An interesting property of this quantity is its scaling dependence on the length of the time series.

Numerical experiments show that λmax grows according to a power law with respect to the number of observations:

![]()

where: T — length of the time series, α — scaling exponent.

For a random walk (Brownian motion), it can be shown that the exponent should be close to α ≈ 2.5. The amplitude of Brownian motion grows as

As a result, the combined scaling leads to the relationship:

![]()

which corresponds to an exponent α ≈ 2.5.

Thus, as the length of the time series increases, the value of λmax grows significantly faster than linearly.

3.3.1. Numerical Experiment for Brownian Motion

To verify the scaling law, a numerical experiment was conducted.

For different time series lengths T, realizations of Brownian motion were generated, after which the average value of λmax was computed.

A logarithmic approximation was used:

![]()

which allows estimating the exponent α using linear regression.

The code for the experiment is given below.

//+------------------------------------------------------------------+ //| TestScalingLambdaMaxBrownMovement.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| http://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #include <Graphics\Graphic.mqh> //+------------------------------------------------------------------+ //| Generate Brownian motion | //+------------------------------------------------------------------+ void GenerateBrownian(int N,vector<double> &data) { data.Resize(N); data[0] = 0.0; for(int i=1; i<N; i++) data[i] = data[i-1] + (MathRand()/32767.0 - 0.5); } //+------------------------------------------------------------------+ //| LinearRegression | //+------------------------------------------------------------------+ void LinearRegression(const double &x[], const double &y[], int n, double &a, double &b) { double sx = 0.0, sy = 0.0, sxx = 0.0, sxy = 0.0; for(int i = 0; i < n; i++) { sx += x[i]; sy += y[i]; sxx += x[i] * x[i]; sxy += x[i] * y[i]; } double denom = n * sxx - sx * sx; a = (n * sxy - sx * sy) / denom; b = (sy - a * sx) / n; } //+------------------------------------------------------------------+ //| TestScaling with statistics | //+------------------------------------------------------------------+ void TestScalingStatistics() { MathSrand(42); int RUNS = 10; // int MC = 10; // Monte Carlo double alpha_values[]; ArrayResize(alpha_values, RUNS); // --- geometric grid of T int nT = 8; int Tvals[]; ArrayResize(Tvals, nT); int T0 = 64; for(int i = 0; i < nT; i++) Tvals[i] = T0 << i; Print("Scaling test with statistics"); //--- double logT[]; double logLambda[]; vector<double> bm; vector<double> l1_trend; for(int run = 0; run < RUNS; run++) { ArrayResize(logT, nT); ArrayResize(logLambda, nT); //--- for(int i = 0; i < nT; i++) { int T = Tvals[i]; double lambda_sum = 0.0; l1_trend.Resize(T); for(int k = 0; k < MC; k++) { GenerateBrownian(T, bm); double lambda_max=0.0; if (bm.L1TrendFilterLambdaMax(lambda_max)) lambda_sum += lambda_max; bm.L1TrendFilter(0.2,true,l1_trend); } double lambda_avg = lambda_sum / MC; logT[i] = MathLog((double)T); logLambda[i] = MathLog(lambda_avg); } // --- regression double alpha, c; LinearRegression(logT, logLambda, nT, alpha, c); alpha_values[run] = alpha; PrintFormat("run %d -> alpha = %.6f", run+1, alpha); } //--- statistics double mean = 0.0; for(int i=0;i<RUNS;i++) mean += alpha_values[i]; mean /= RUNS; // --- standard deviation double var = 0.0; for(int i=0;i<RUNS;i++) var += (alpha_values[i]-mean)*(alpha_values[i]-mean); var /= (RUNS - 1); double stddev = MathSqrt(var); // --- standard error of mean double sem = stddev / MathSqrt((double)RUNS); // --- theoretical comparison double alpha_theory=2.5; double percent_error=MathAbs(mean-alpha_theory)/alpha_theory*100.0; //--- results PrintFormat("mean alpha = %.6f", mean); PrintFormat("std deviation = %.6f", stddev); PrintFormat("standard error = %.6f", sem); PrintFormat("theory = %.4f", alpha_theory); PrintFormat("percent error from theory = %.4f %%", percent_error); } //+------------------------------------------------------------------+ //| TestScaling | //+------------------------------------------------------------------+ void TestScaling() { MathSrand(1); // --- geometric grid of T int nT = 8; int Tvals[]; ArrayResize(Tvals,nT); //--- int T0 = 64; for(int i=0; i<nT; i++) Tvals[i]=T0<<i; // 64 * 2^i //--- double logT[], logLambda[]; ArrayResize(logT,nT); ArrayResize(logLambda,nT); //--- Print("scaling test for lambda_max"); for(int i=0; i<nT; i++) { int T = Tvals[i]; //--- Monte-Carlo simulations int MC=1000; double lambda_sum = 0.0; for(int k=0; k<MC; k++) { vector<double> bm; GenerateBrownian(T, bm); double lambda_max=0.0; if(bm.L1TrendFilterLambdaMax(lambda_max)) lambda_sum += lambda_max; } double lambda_avg=lambda_sum/MC; logT[i]= MathLog((double)T); logLambda[i]=MathLog(lambda_avg); PrintFormat("T=%5d <lambda_max>=%.6f",T,lambda_avg); } // --- linear regression in log-log double alpha, c; LinearRegression(logT,logLambda,nT,alpha,c); //--- PrintFormat("estimated scaling exponent alpha = %.4f",alpha); double alpha_theory=2.5; PrintFormat("theoretical value = %.4f",alpha_theory); //--- plot scaling law CGraphic g; g.Create(0, "ScalingLaw",0,0,0,1000,600); g.BackgroundMain("Scaling law of lambda_max (Brownian motion)"); g.BackgroundMainSize(16); g.CurveAdd(logT, logLambda, CURVE_POINTS, "Simulation"); //--- double xfit[2], yfit[2]; xfit[0] = logT[0]; xfit[1] = logT[nT-1]; //--- yfit[0] = alpha*xfit[0] + c; yfit[1] = alpha*xfit[1] + c; //---least squares fit g.CurveAdd(xfit, yfit, CURVE_LINES, "LS fit"); g.CurvePlotAll(); g.Update(); DebugBreak(); } //+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart() { //--- calculate scaling with statistics TestScalingStatistics(); //--- show sample results TestScaling(); } //+------------------------------------------------------------------+

Output:

TestScalingLambdaMaxBrownMovement (EURUSD,H1) Scaling test with statistics TestScalingLambdaMaxBrownMovement (EURUSD,H1) run 1 -> alpha = 2.480774 TestScalingLambdaMaxBrownMovement (EURUSD,H1) run 2 -> alpha = 2.530977 TestScalingLambdaMaxBrownMovement (EURUSD,H1) run 3 -> alpha = 2.435511 TestScalingLambdaMaxBrownMovement (EURUSD,H1) run 4 -> alpha = 2.461984 TestScalingLambdaMaxBrownMovement (EURUSD,H1) run 5 -> alpha = 2.467093 TestScalingLambdaMaxBrownMovement (EURUSD,H1) run 6 -> alpha = 2.487965 TestScalingLambdaMaxBrownMovement (EURUSD,H1) run 7 -> alpha = 2.532371 TestScalingLambdaMaxBrownMovement (EURUSD,H1) run 8 -> alpha = 2.455831 TestScalingLambdaMaxBrownMovement (EURUSD,H1) run 9 -> alpha = 2.483485 TestScalingLambdaMaxBrownMovement (EURUSD,H1) run 10 -> alpha = 2.420283 TestScalingLambdaMaxBrownMovement (EURUSD,H1) mean alpha = 2.475627 TestScalingLambdaMaxBrownMovement (EURUSD,H1) std deviation = 0.036281 TestScalingLambdaMaxBrownMovement (EURUSD,H1) standard error = 0.011473 TestScalingLambdaMaxBrownMovement (EURUSD,H1) theory = 2.5000 TestScalingLambdaMaxBrownMovement (EURUSD,H1) percent error from theory = 0.9749 % TestScalingLambdaMaxBrownMovement (EURUSD,H1) scaling test for lambda_max TestScalingLambdaMaxBrownMovement (EURUSD,H1) T= 64 <lambda_max>=97.302362 TestScalingLambdaMaxBrownMovement (EURUSD,H1) T= 128 <lambda_max>=566.626861 TestScalingLambdaMaxBrownMovement (EURUSD,H1) T= 256 <lambda_max>=3162.076116 TestScalingLambdaMaxBrownMovement (EURUSD,H1) T= 512 <lambda_max>=18271.204936 TestScalingLambdaMaxBrownMovement (EURUSD,H1) T= 1024 <lambda_max>=100057.796790 TestScalingLambdaMaxBrownMovement (EURUSD,H1) T= 2048 <lambda_max>=578620.887399 TestScalingLambdaMaxBrownMovement (EURUSD,H1) T= 4096 <lambda_max>=3192555.936035 TestScalingLambdaMaxBrownMovement (EURUSD,H1) T= 8192 <lambda_max>=17895314.647170 TestScalingLambdaMaxBrownMovement (EURUSD,H1) estimated scaling exponent alpha = 2.4967 TestScalingLambdaMaxBrownMovement (EURUSD,H1) theoretical value = 2.5000

The double-log plot (in double-logarithmic scale) shows the presence of a power-law dependence of the function λmax on the number of data points for Brownian motion.

.

Fig.3. Power-law dependence of LambdaMax for Brownian motion

The simulation results show:

mean alpha = 2.4756 std deviation = 0.036 theory = 2.5 percent error ≈ 1%

Thus, the experiment confirms the theoretical relationship:

![]()

The double-log plot in double-logarithmic scale demonstrates a linear relationship between log(λmax) and log(T).

3.3.2. Scaling for financial time series

A similar experiment was conducted for FOREX market price series. For different currency pairs and timeframes, the exponent α was estimated.

The results show that for real financial data the value of α also lies in the range α ≈ 2.45–2.60, which is very close to the theoretical value for Brownian motion. This means that the scaling behavior of λmax is nearly universal and holds across different markets and timeframes.

The script TestScalingLambdaMaxSymbol.mq5 computes the exponent of λmax for a given symbol across standard timeframes M1–H1.

//+------------------------------------------------------------------+ //| TestScalingLambdaMaxSymbol.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| http://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #property script_show_inputs //--- input parameters input string WorkSymbol = "EURUSD"; // Symbol input int YearStart = 2024; input int YearEnd = 2025; #include <Graphics\Graphic.mqh> //+------------------------------------------------------------------+ //| GetHistoricalData | //+------------------------------------------------------------------+ bool GetHistoricalData(double &data[], string symbol, ENUM_TIMEFRAMES tf, int year_start, int year_end) { datetime from = StringToTime(IntegerToString(year_start) + ".01.01 00:00"); datetime to = StringToTime(IntegerToString(year_end) + ".12.31 23:59"); int copied = CopyClose(symbol, tf, from, to, data); if(copied <= 0) { Print("Error in CopyClose: ", GetLastError()); ArrayResize(data, 0); return false; } //PrintFormat("Loaded bars: %d (%s %s)", ArraySize(data), symbol, EnumToString(tf)); return true; } //+------------------------------------------------------------------+ //| LinearRegression | //+------------------------------------------------------------------+ void LinearRegression(const double &x[], const double &y[], int n, double &a, double &b) { double sx = 0, sy = 0, sxx = 0, sxy = 0; for(int i = 0; i < n; i++) { sx += x[i]; sy += y[i]; sxx += x[i] * x[i]; sxy += x[i] * y[i]; } double denom = n*sxx - sx*sx; if(denom!=0) { a = (n*sxy-sx*sy)/denom; b = (sy-a*sx)/n; } } //+------------------------------------------------------------------+ //| Scaling test for one timeframe | //+------------------------------------------------------------------+ bool TestScalingLambaMaxTF(string symbol, ENUM_TIMEFRAMES tf, double &logT_out[], double &logLambda_out[], double &alpha_out) { MathSrand(42); double prices[]; if(!GetHistoricalData(prices, symbol, tf, YearStart, YearEnd)) return false; int Tvals[]; int nT=8; int T0=64; ArrayResize(Tvals, nT); for(int i = 0; i < nT; i++) Tvals[i] = T0 << i; ArrayResize(logT_out, nT); ArrayResize(logLambda_out, nT); int data_size = ArraySize(prices); vector<double> data_prices; for(int i = 0; i < nT; i++) { int T = Tvals[i]; int MC = 1000; double lambda_sum = 0.0; for(int k = 0; k < MC; k++) { if(data_size < T) break; int start = MathRand() % (data_size - T); data_prices.Resize(T); for(int j=0; j<T; j++) data_prices[j]=prices[start+j]; double lambda_max=0.0; if(data_prices.L1TrendFilterLambdaMax(lambda_max)) lambda_sum += lambda_max; } double lambda_avg = lambda_sum / MC; logT_out[i]=MathLog((double)T); logLambda_out[i]=MathLog(lambda_avg); //PrintFormat("TF=%s T=%5d <lambda_max>=%.6f", EnumToString(tf), T, lambda_avg); } double c; LinearRegression(logT_out, logLambda_out, nT, alpha_out, c); PrintFormat("%s (%s) estimated scaling exponent = %.4f", symbol,EnumToString(tf), alpha_out); return true; } //+------------------------------------------------------------------+ //| TestScalingLambdaMaxSymbol | //+------------------------------------------------------------------+ void TestScalingLambdaMaxSymbol(string symbol) { ENUM_TIMEFRAMES timeframes[] = {PERIOD_M1, PERIOD_M2, PERIOD_M3, PERIOD_M4, PERIOD_M5, PERIOD_M6, PERIOD_M10, PERIOD_M12, PERIOD_M15, PERIOD_M20, PERIOD_M30, PERIOD_H1 }; uint colors[] = {clrRed,clrBlue,clrGreen,clrOrange,clrPurple,clrDarkGreen,clrCyan, clrNavy,clrOrangeRed,clrDodgerBlue,clrCrimson,clrDarkRed }; //--- CGraphic g; g.Create(0,"ScalingLawTest",0,0,0,1000,600); g.BackgroundMain("Scaling law of lambda_max ("+symbol+")"); g.BackgroundMainSize(16); PrintFormat("%s scaling test for standard timeframes",symbol); for(int i = 0; i < ArraySize(timeframes); i++) { double logT[], logLambda[], alpha; // Print("processing timeframe: ", EnumToString(timeframes[i]), " -----"); if(TestScalingLambaMaxTF(symbol,timeframes[i],logT,logLambda,alpha)) { g.CurveAdd(logT,logLambda,ColorToARGB(colors[i % ArraySize(colors)],255),CURVE_POINTS_AND_LINES,EnumToString(timeframes[i])); } } g.CurvePlotAll(); g.Update(); //--- DebugBreak(); } //+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart() { //--- estimate lambda_max scale exponent for price data TestScalingLambdaMaxSymbol(WorkSymbol); } //+------------------------------------------------------------------+

Results for EURUSD:

TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD scaling test for standard timeframes TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD (PERIOD_M1) estimated scaling exponent = 2.5038 TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD (PERIOD_M2) estimated scaling exponent = 2.5350 TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD (PERIOD_M3) estimated scaling exponent = 2.5034 TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD (PERIOD_M4) estimated scaling exponent = 2.5422 TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD (PERIOD_M5) estimated scaling exponent = 2.5341 TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD (PERIOD_M6) estimated scaling exponent = 2.5132 TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD (PERIOD_M10) estimated scaling exponent = 2.5188 TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD (PERIOD_M12) estimated scaling exponent = 2.5126 TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD (PERIOD_M15) estimated scaling exponent = 2.5208 TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD (PERIOD_M20) estimated scaling exponent = 2.4887 TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD (PERIOD_M30) estimated scaling exponent = 2.5695 TestScalingLambdMaxSymbol (EURUSD,H1) EURUSD (PERIOD_H1) estimated scaling exponent = 2.6118

The results for EURUSD (standard timeframes M1–H1) are shown in Fig. 4.

Fig.4. Power-law dependence of λmax for the different EURUSD timeframes

Similarly, other currency pairs can be analyzed.

For USDJPY:

TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY scaling test for standard timeframes TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY (PERIOD_M1) estimated scaling exponent = 2.5851 TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY (PERIOD_M2) estimated scaling exponent = 2.5825 TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY (PERIOD_M3) estimated scaling exponent = 2.4889 TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY (PERIOD_M4) estimated scaling exponent = 2.5099 TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY (PERIOD_M5) estimated scaling exponent = 2.5059 TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY (PERIOD_M6) estimated scaling exponent = 2.4939 TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY (PERIOD_M10) estimated scaling exponent = 2.5548 TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY (PERIOD_M12) estimated scaling exponent = 2.5641 TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY (PERIOD_M15) estimated scaling exponent = 2.5525 TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY (PERIOD_M20) estimated scaling exponent = 2.5390 TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY (PERIOD_M30) estimated scaling exponent = 2.5805 TestScalingLambdMaxSymbol (EURUSD,H1) USDJPY (PERIOD_H1) estimated scaling exponent = 2.4645

The results for USDJPY are also well approximated by a power-law relationship.

Fig.5. Power-law dependence of λmax for the different USDJPY timeframes

For GBPUSD:

TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD scaling test for standard timeframes TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD (PERIOD_M1) estimated scaling exponent = 2.5235 TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD (PERIOD_M2) estimated scaling exponent = 2.5449 TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD (PERIOD_M3) estimated scaling exponent = 2.5439 TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD (PERIOD_M4) estimated scaling exponent = 2.5427 TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD (PERIOD_M5) estimated scaling exponent = 2.5248 TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD (PERIOD_M6) estimated scaling exponent = 2.5308 TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD (PERIOD_M10) estimated scaling exponent = 2.5293 TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD (PERIOD_M12) estimated scaling exponent = 2.5235 TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD (PERIOD_M15) estimated scaling exponent = 2.5069 TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD (PERIOD_M20) estimated scaling exponent = 2.4977 TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD (PERIOD_M30) estimated scaling exponent = 2.5659 TestScalingLambdMaxSymbol (EURUSD,H1) GBPUSD (PERIOD_H1) estimated scaling exponent = 2.5524

A similar situation is observed for GBPUSD price series (Fig. 6).

Fig.6. Power-law dependence of λmax for the different GBPUSD timeframes

For the considered EURUSD, USDJPY, and GBPUSD series, the estimated exponent values are also close to 2.5.

Linear relationships in log-log scale for the function λmax across multiple timeframes and currency pairs indicate a power-law dependence of λmax on the number of observations.

3.3.3. Practical implications of scaling

The existence of a power-law dependence for λmax has an important practical implication.

Since λmax ∝ T^2.5, the absolute value of λ strongly depends on:

- the length of the data window,

- the timeframe,

- the scale of the time series.

Therefore, using an absolute value of λ is inconvenient in practice.

A much more robust approach is to use a relative parameter λ=c⋅λmax, where 0<c<1.

Such an approach:

- makes the regularization parameter scale-invariant,

- simplifies parameter transfer between different instruments,

- allows using the same settings across different timeframes.

For this reason, in all subsequent examples the parameter λ will be specified in units of λmax.

3.4. L1 trend indicators

In this section, three types of indicators are considered:

- Computation of the L1 trend based on closing prices;

- Computation of the linear growth coefficients (slope) of the L1 trend;

- Computation of the sign of the L1 trend slope;

3.4.1. L1TrendFilter.mq5 - L1 trend indicator

In this example, the L1 filter is computed using closing prices for a specified number of bars (in the example, BarsToShow = 1000) with the lambda coefficient specified in units of λmax.

The calculation uses the method call L1TrendFilter(relative = true), where the parameter λ is defined in units of λmax. The indicator values are displayed directly in the chart window.

The code of the L1TrendFilter.mq5 indicator is provided below.

//+------------------------------------------------------------------+ //| L1TrendFilter.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #property indicator_chart_window #property indicator_buffers 1 #property indicator_plots 1 //--- #property indicator_label1 "L1TrendFilter" #property indicator_type1 DRAW_LINE #property indicator_color1 clrDodgerBlue #property indicator_width1 2 //--- input int BarsToShow = 1000; // Number of bars to calculate L1 input double CoefLambda = 0.015; // Lambda in lambda_max units //--- double Trend[]; //+------------------------------------------------------------------+ //| Indicator initialization function | //+------------------------------------------------------------------+ int OnInit() { SetIndexBuffer(0,Trend,INDICATOR_DATA); ArrayInitialize(Trend,EMPTY_VALUE); //--- PlotIndexSetDouble(0,PLOT_EMPTY_VALUE,EMPTY_VALUE); IndicatorSetInteger(INDICATOR_DIGITS,_Digits); //--- return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Indicator iteration function | //+------------------------------------------------------------------+ int OnCalculate(const int rates_total, const int prev_calculated, const datetime &time[], const double &open[], const double &high[], const double &low[], const double &close[], const long &tick_volume[], const long &volume[], const int &spread[]) { //--- check bars static bool warned=false; if(rates_total < BarsToShow) { if(!warned) { Print("Waiting for enough bars: ",BarsToShow); warned=true; } ArrayInitialize(Trend,EMPTY_VALUE); return(0); } //--- check new bar static datetime last_bar_time=0; bool new_bar=(time[0]!=last_bar_time); bool need_recalc=(prev_calculated==0) || new_bar || (rates_total!=prev_calculated); if(!need_recalc) return(prev_calculated); last_bar_time=time[0]; //--- range int start=rates_total-BarsToShow; //--- hide old bars for(int i=0; i<start; i++) Trend[i]=EMPTY_VALUE; //--- int data_count=BarsToShow; //--- copy Close vector<double> DataClose; DataClose.Resize(data_count); for(int i=0; i<data_count; i++) DataClose[i]=close[start+i]; //--- lambda max double lambda_max=0.0; bool res=DataClose.L1TrendFilterLambdaMax(lambda_max); if(res) { PrintFormat("lambda_max=%f (%s,%s) Coef=%f lambda=%f", lambda_max,Symbol(),EnumToString(Period()),CoefLambda,lambda_max*CoefLambda); } //--- L1 trend filtering vector<double> filtered_data; filtered_data.Resize(data_count); if(DataClose.L1TrendFilter(CoefLambda,true,filtered_data)) { for(int i=0; i<data_count; i++) Trend[start+i]=filtered_data[i]; } //--- return(rates_total); } //+------------------------------------------------------------------+

In Fig. 7, an example of calculating the L1TrendFilter.mq5 indicator with CoefLambda = 0.015 is shown.

Fig.7. Example of L1TrendFilter.mq5 indicator calculation with CoefLambda = 0.015

For comparison, one can compute several variants with different regularization parameters.

Fig. 8 shows calculations with parameters CoefLambda = 0.015, CoefLambda = 0.025, and CoefLambda = 0.055.

Fig.8. Examples of L1TrendFilter.mq5 indicator calculation with the different CoefLambda values

3.4.2. L1TrendFilterSlope.mq5 - indicator of L1 trend dynamics

To display the trend slope, one can use the increment of the L1TrendFilter indicator values.

As an example, consider the L1TrendFilterSlope indicator, which displays values in a separate window.

The code of the indicator is provided below.

//+------------------------------------------------------------------+ //| L1TrendFilterSlope.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #property indicator_separate_window #property indicator_buffers 1 #property indicator_plots 1 //--- #property indicator_label1 "L1TrendFilterSlope" #property indicator_type1 DRAW_LINE #property indicator_color1 clrDodgerBlue #property indicator_width1 2 //--- input int BarsToShow = 1000; // Number of bars to calculate L1 input double CoefLambda = 0.015; // Lambda in lambda_max units //--- double Trend[]; //+------------------------------------------------------------------+ //| Indicator initialization function | //+------------------------------------------------------------------+ int OnInit() { SetIndexBuffer(0,Trend,INDICATOR_DATA); ArrayInitialize(Trend,EMPTY_VALUE); //--- PlotIndexSetDouble(0,PLOT_EMPTY_VALUE,EMPTY_VALUE); IndicatorSetInteger(INDICATOR_DIGITS,_Digits); //--- return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Indicator iteration function | //+------------------------------------------------------------------+ int OnCalculate(const int rates_total, const int prev_calculated, const datetime &time[], const double &open[], const double &high[], const double &low[], const double &close[], const long &tick_volume[], const long &volume[], const int &spread[]) { //--- check bars static bool warned=false; if(rates_total < BarsToShow) { if(!warned) { Print("Waiting for enough bars: ",BarsToShow); warned=true; } ArrayInitialize(Trend,EMPTY_VALUE); return(0); } //--- check new bar static datetime last_bar_time=0; bool new_bar=(time[0]!=last_bar_time); bool need_recalc= (prev_calculated==0) || new_bar || (rates_total!=prev_calculated); if(!need_recalc) return(prev_calculated); last_bar_time=time[0]; //--- int start=rates_total-BarsToShow; int data_count=BarsToShow; //--- hide old bars for(int i=0;i<start;i++) Trend[i]=EMPTY_VALUE; //--- copy Close vector<double> DataClose; DataClose.Resize(data_count); for(int i=0;i<data_count;i++) DataClose[i]=close[start+i]; //--- lambda max double lambda_max=0.0; if(DataClose.L1TrendFilterLambdaMax(lambda_max)) { PrintFormat("lambda_max=%f (%s,%s) Coef=%f lambda=%f", lambda_max,Symbol(),EnumToString(Period()),CoefLambda,lambda_max*CoefLambda); } //--- L1 filtering vector<double> filtered_data; filtered_data.Resize(data_count); bool res=DataClose.L1TrendFilter(CoefLambda,true,filtered_data); if(res) { //--- slope (first difference) for(int i=1; i<data_count; i++) { double delta=filtered_data[i]-filtered_data[i-1]; Trend[start+i]=delta; } //--- copy first element Trend[start]=Trend[start+1]; } return(rates_total); } //+------------------------------------------------------------------+

The result of the joint L1TrendFilter.mq5 and L1TrendFilterSlope.mq5 indicators is shown in Fig. 9.

Fig.9. Example of L1TrendFilter.mq5 and L1TrendFilterSlope.mq5 indicators calculation with CoefLambda = 0.015

3.4.3. L1TrendFilterSlopeSign.mq5 - indicator of L1 trend direction

Similarly, one can compute an indicator that displays the sign of the increment of the L1TrendFilterSlope.mq5 indicator.

Code of the L1TrendFilterSlopeSign.mq5 indicator:

//+------------------------------------------------------------------+ //| L1TrendFilterSlopeSign.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #property indicator_separate_window #property indicator_buffers 1 #property indicator_plots 1 //--- #property indicator_label1 "L1TrendFilterSlope" #property indicator_type1 DRAW_LINE #property indicator_color1 clrDodgerBlue #property indicator_width1 2 //--- input int BarsToShow = 1000; // Number of bars to calculate L1 input double CoefLambda = 0.015; // Lambda in lambda_max units //--- double Trend[]; //+------------------------------------------------------------------+ //| Signum | //+------------------------------------------------------------------+ double Signum(const double value) { return((value>0)-(value<0)); } //+------------------------------------------------------------------+ //| Indicator initialization function | //+------------------------------------------------------------------+ int OnInit() { SetIndexBuffer(0,Trend,INDICATOR_DATA); ArrayInitialize(Trend,EMPTY_VALUE); //--- PlotIndexSetDouble(0,PLOT_EMPTY_VALUE,EMPTY_VALUE); IndicatorSetInteger(INDICATOR_DIGITS,_Digits); //--- return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Indicator iteration function | //+------------------------------------------------------------------+ int OnCalculate(const int rates_total, const int prev_calculated, const datetime &time[], const double &open[], const double &high[], const double &low[], const double &close[], const long &tick_volume[], const long &volume[], const int &spread[]) { //--- check bars static bool warned=false; if(rates_total < BarsToShow) { if(!warned) { Print("Waiting for enough bars: ",BarsToShow); warned=true; } ArrayInitialize(Trend,EMPTY_VALUE); return(0); } //--- check new bar static datetime last_bar_time=0; bool new_bar=(time[0]!=last_bar_time); bool need_recalc=(prev_calculated==0) || new_bar || (rates_total!=prev_calculated); if(!need_recalc) return(prev_calculated); last_bar_time=time[0]; //--- int start=rates_total-BarsToShow; int data_count=BarsToShow; //--- hide old bars for(int i=0; i<start; i++) Trend[i]=EMPTY_VALUE; //--- copy Close vector<double> DataClose; DataClose.Resize(data_count); for(int i=0; i<data_count; i++) DataClose[i]=close[start+i]; //--- lambda max double lambda_max=0.0; bool res=DataClose.L1TrendFilterLambdaMax(lambda_max); if(res) { PrintFormat("lambda_max=%f (%s,%s) Coef=%f lambda=%f", lambda_max,Symbol(),EnumToString(Period()),CoefLambda,lambda_max*CoefLambda); } //--- L1 filtering vector<double> filtered_data; filtered_data.Resize(data_count); res=DataClose.L1TrendFilter(CoefLambda,true,filtered_data); if(res) { Trend[start]=0; for(int i=1; i<data_count; i++) { double delta=filtered_data[i]-filtered_data[i-1]; Trend[start+i]=Signum(delta); } } return(rates_total); } //+------------------------------------------------------------------+

An example of the joint all three indicators is shown in Fig. 10 (the same coefficient value CoefLambda = 0.015 was used).

Fig.10. Example of L1TrendFilter.mq5, L1TrendFilterSlope.mq5, and L1TrendFilterSlopeSign.mq5 indicators calculation with CoefLambda = 0.015

3.4.4. Volatility Indicators Based on the L1 Trend

This section presents indicators designed to evaluate the volatility of a financial instrument based on the L1 trend.

These tools make it possible to identify periods of market instability and stability, analyze current market dynamics, and make more informed trading decisions.

The indicators considered in this section are:

- L1Volatility.mq5 — residual volatility relative to the L1 trend;

- L1VolatilitySmoothed.mq5 — smoothed residual volatility;

- L1VolatilityAbsolute.mq5 — absolute volatility;

- L1VolatilityNormalized.mq5 — normalized volatility;

- L1VolatilityNormalizedSmoothed.mq5 — smoothed normalized volatility;

- L1VolatilityRegime.mq5 — market regime detection based on volatility.

All indicators are built upon a unified L1-trend framework, which ensures analytical consistency and simplifies interpretation of the obtained results.

The use of these indicators allows visual identification of periods of high and low volatility, as well as determination of the current market regime — range, trend, expansion, or panic.

As a result, a trader can adapt trading strategies to prevailing market conditions, for example by applying more conservative approaches during low-volatility periods or more active strategies during strong market movements.

3.4.4.1. L1Volatility.mq5 — L1 Volatility Indicator

The indicator calculates residual volatility as the difference between the closing prices and the corresponding value of the L1 trend.

This approach allows identification of unstable market periods and precise entry or exit moments.

Visually, the indicator is displayed in a separate chart window as an orange line.

The indicator helps to:

- Evaluate price deviations from the L1 trend and measure market movement strength;

- Detect local volatility spikes for more accurate risk management;

- Compare the dynamics of different instruments within the same timeframe.

The indicator is particularly useful in systems where short-term volatility changes must be monitored without losing the broader trend context.

The code of the L1Volatility.mq5 indicator is provided below.

//+------------------------------------------------------------------+ //| L1Volatility.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #property indicator_separate_window #property indicator_buffers 1 #property indicator_plots 1 //--- #property indicator_label1 "L1Volatility" #property indicator_type1 DRAW_LINE #property indicator_color1 clrOrangeRed #property indicator_width1 2 //--- input int BarsToShow = 1000; // Number of bars to calculate L1 input double CoefLambda = 0.015; // Lambda in lambda_max units //--- double Volatility[]; //--- //+------------------------------------------------------------------+ //| Indicator initialization function | //+------------------------------------------------------------------+ int OnInit() { SetIndexBuffer(0,Volatility,INDICATOR_DATA); ArrayInitialize(Volatility,EMPTY_VALUE); //--- PlotIndexSetDouble(0,PLOT_EMPTY_VALUE,EMPTY_VALUE); IndicatorSetInteger(INDICATOR_DIGITS,_Digits); //--- return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Indicator iteration function | //+------------------------------------------------------------------+ int OnCalculate(const int rates_total, const int prev_calculated, const datetime &time[], const double &open[], const double &high[], const double &low[], const double &close[], const long &tick_volume[], const long &volume[], const int &spread[]) { //--- check bars static bool warned=false; if(rates_total<BarsToShow) { if(!warned) { Print("Waiting for enough bars: ",BarsToShow); warned=true; } ArrayInitialize(Volatility,EMPTY_VALUE); return(0); } //--- check new bar static datetime last_bar_time=0; bool new_bar=(time[0]!=last_bar_time); bool need_recalc=(prev_calculated==0) || new_bar || (rates_total!=prev_calculated); if(!need_recalc) return(prev_calculated); last_bar_time=time[0]; //--- int start=rates_total-BarsToShow; int data_count=BarsToShow; //--- hide old bars for(int i=0;i<start;i++) Volatility[i]=EMPTY_VALUE; //--- copy Close vector<double> DataClose; DataClose.Resize(data_count); for(int i=0; i<data_count; i++) DataClose[i]=close[start+i]; //--- lambda max double lambda_max=0.0; bool res=DataClose.L1TrendFilterLambdaMax(lambda_max); if(res) { PrintFormat("lambda_max=%f (%s,%s) Coef=%f lambda=%f", lambda_max,Symbol(),EnumToString(Period()),CoefLambda,lambda_max*CoefLambda); } //--- L1 filter vector<double> filtered_data; filtered_data.Resize(data_count); res=DataClose.L1TrendFilter(CoefLambda,true,filtered_data); if(res) { for(int i=0; i<data_count; i++) { double residual=close[start+i]-filtered_data[i]; Volatility[start+i]=residual; } } //--- return(rates_total); } //+------------------------------------------------------------------+

The calculation result is shown in Fig. 11.

Fig. 11. L1Volatility.mq5 Indicator

3.4.4.2. L1VolatilitySmoothed.mq5 — Smoothed Residual Volatility Indicator

This indicator represents a smoothed version of L1Volatility, where a Simple Moving Average (SMA) is applied.

Smoothing allows:

- Reduction of short-term noise and outliers;

- Clearer and more interpretable visualization;

- Focus on persistent changes in volatility.

The indicator is useful for strategies requiring evaluation of longer-term volatility trends, for example in adaptive trading systems or when filtering false signals during trending and ranging market phases.

The code of the L1VolatilitySmoothed.mq5 indicator is provided below.

//+------------------------------------------------------------------+ //| L1VolatilitySmoothed.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #property indicator_separate_window #property indicator_buffers 1 #property indicator_plots 1 #property indicator_label1 "L1VolatilitySmoothed" #property indicator_type1 DRAW_LINE #property indicator_color1 clrMediumVioletRed #property indicator_width1 2 //--- input int BarsToShow = 1000; // Number of bars to calculate L1 input double CoefLambda = 0.015; // Lambda in lambda_max units input int SmoothPeriod = 10; // Smooth period //--- double VolSmoothed[]; //+------------------------------------------------------------------+ //| Indicator initialization function | //+------------------------------------------------------------------+ int OnInit() { SetIndexBuffer(0, VolSmoothed, INDICATOR_DATA); ArrayInitialize(VolSmoothed, EMPTY_VALUE); PlotIndexSetDouble(0, PLOT_EMPTY_VALUE, EMPTY_VALUE); IndicatorSetInteger(INDICATOR_DIGITS, _Digits); //--- return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Indicator iteration function | //+------------------------------------------------------------------+ int OnCalculate(const int rates_total, const int prev_calculated, const datetime &time[], const double &open[], const double &high[], const double &low[], const double &close[], const long &tick_volume[], const long &volume[], const int &spread[]) { if(rates_total<BarsToShow) { ArrayInitialize(VolSmoothed,EMPTY_VALUE); return(0); } //--- recalc only on new bar static datetime last_bar_time = 0; if(time[0] == last_bar_time && prev_calculated > 0) return(prev_calculated); last_bar_time=time[0]; //--- int start=rates_total-BarsToShow; for(int i=0; i<start; i++) VolSmoothed[i]=EMPTY_VALUE; //--- copy close prices vector<double> price(BarsToShow); for(int i=0; i<BarsToShow; i++) price[i] = close[start+i]; vector<double> l1(BarsToShow); bool res=price.L1TrendFilter(CoefLambda,true,l1); if(res) { //--- calculate raw volatility vector<double> rawVol(BarsToShow); for(int i=0; i<BarsToShow; i++) rawVol[i]=close[start+i]-l1[i]; //--- apply simple moving average smoothing for(int i=0; i<BarsToShow; i++) { double sum = 0.0; int count = 0; for(int j=MathMax(0,i-SmoothPeriod+1); j<=i; j++) { sum+=rawVol[j]; count++; } VolSmoothed[start+i]=sum/count; } } //--- return(rates_total); } //+------------------------------------------------------------------+

Figure 12 shows both L1Volatility.mq5 and L1VolatilitySmoothed.mq5 indicators.

Fig.12. L1Volatility.mq5 and L1VolatilitySmoothed.mq5 Indicators

3.4.4.3. L1VolatilityAbsolute.mq5 — Absolute Volatility Indicator

The indicator computes the absolute value of the difference between the closing prices and the L1 trend.

Features and applications:

- Ignores movement direction and evaluates only fluctuation magnitude;

- Convenient for analyzing price oscillation amplitude independently of trend direction;

- Useful for systems based on extreme-value statistics and risk analysis.

Absolute volatility reflects the true magnitude of price deviations, enabling the trader to observe the strength of market movement without being distracted by its direction.

The code of the L1VolatilityAbsolute.mq5 indicator is provided below.

//+------------------------------------------------------------------+ //| L1VolatilityAbsolute.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #property indicator_separate_window #property indicator_buffers 1 #property indicator_plots 1 //--- #property indicator_label1 "L1VolatilityAbsolute" #property indicator_type1 DRAW_LINE #property indicator_color1 clrOrange #property indicator_width1 2 //--- input int BarsToShow = 1000; // Number of bars to calculate L1 input double CoefLambda = 0.015; // Lambda in lambda_max units //--- double Vol[]; //+------------------------------------------------------------------+ //| Indicator initialization function | //+------------------------------------------------------------------+ int OnInit() { SetIndexBuffer(0,Vol,INDICATOR_DATA); ArrayInitialize(Vol,EMPTY_VALUE); PlotIndexSetDouble(0,PLOT_EMPTY_VALUE,EMPTY_VALUE); IndicatorSetInteger(INDICATOR_DIGITS,_Digits); //--- return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Indicator iteration function | //+------------------------------------------------------------------+ int OnCalculate(const int rates_total, const int prev_calculated, const datetime &time[], const double &open[], const double &high[], const double &low[], const double &close[], const long &tick_volume[], const long &volume[], const int &spread[]) { //--- static bool warned=false; if(rates_total < BarsToShow) { if(!warned) { Print("Waiting bars ",BarsToShow); warned=true; } ArrayInitialize(Vol,EMPTY_VALUE); return(0); } static datetime last_bar=0; bool new_bar=(time[0]!=last_bar); //--- if(!(prev_calculated==0 || new_bar || rates_total!=prev_calculated)) return(prev_calculated); //--- last_bar=time[0]; int start=rates_total-BarsToShow; int N=BarsToShow; for(int i=0; i<start; i++) Vol[i]=EMPTY_VALUE; //--- vector<double> price; price.Resize(N); for(int i=0; i<N; i++) price[i]=close[start+i]; vector<double> l1; l1.Resize(N); bool res=price.L1TrendFilter(CoefLambda,true,l1); if(res) { for(int i=0; i<N; i++) Vol[start+i]=MathAbs(close[start+i]-l1[i]); } //--- return(rates_total); } //+------------------------------------------------------------------+

An example of the indicator calculation is shown in Fig.13.

Fig.13. L1VolatilityAbsolute.mq5 Indicator

3.4.4.4. L1VolatilityNormalized.mq5 — Normalized Volatility Indicator

The indicator normalizes volatility using ATR (Average True Range) together with the L1 trend.

It calculates the ratio of the absolute price deviation from the trend to the average price range over the ATR period.Normalization removes price-scale dependence, allowing comparison across different instruments and timeframes.

Applications include:

- Identification of relatively strong and weak market movements;

- Comparison of volatility between different assets;

- Evaluation of market conditions independently of price level.

The code of the L1VolatilityNormalized.mq5 indicator is provided below.

//+------------------------------------------------------------------+ //| L1VolatilityNormalized.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #property indicator_separate_window #property indicator_buffers 1 #property indicator_plots 1 #property indicator_label1 "L1VolatilityNormalized" #property indicator_type1 DRAW_LINE #property indicator_color1 clrDodgerBlue #property indicator_width1 2 //--- input int BarsToShow = 1000; // Number of bars to calculate L1 input double CoefLambda = 0.015; // Lambda in lambda_max units //--- double VolNormalized[]; //--- //+------------------------------------------------------------------+ //| Indicator initialization function | //+------------------------------------------------------------------+ int OnInit() { //--- prepare SetIndexBuffer(0, VolNormalized,INDICATOR_DATA); ArrayInitialize(VolNormalized,EMPTY_VALUE); PlotIndexSetDouble(0,PLOT_EMPTY_VALUE,EMPTY_VALUE); IndicatorSetInteger(INDICATOR_DIGITS,_Digits); //--- return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Indicator iteration function | //+------------------------------------------------------------------+ int OnCalculate(const int rates_total, const int prev_calculated, const datetime &time[], const double &open[], const double &high[], const double &low[], const double &close[], const long &tick_volume[], const long &volume[], const int &spread[]) { //--- check bars static bool warned=false; if(rates_total<BarsToShow) { if(!warned) { Print("Waiting for enough bars: ",BarsToShow); warned=true; } ArrayInitialize(VolNormalized,EMPTY_VALUE); return(0); } //--- check new bar static datetime last_bar_time=0; bool new_bar=(time[0]!=last_bar_time); bool need_recalc=(prev_calculated==0) || new_bar || (rates_total!=prev_calculated); if(!need_recalc) return(prev_calculated); last_bar_time=time[0]; int start=rates_total-BarsToShow; //--- for(int i=0; i<start; i++) VolNormalized[i]=EMPTY_VALUE; //--- copy close prices vector<double> price(BarsToShow); for(int i=0; i<BarsToShow; i++) price[i]=close[start+i]; //--- vector<double> l1(BarsToShow); bool res=price.L1TrendFilter(CoefLambda,true,l1); if(res) { //--- compute normalized volatility double mean=0.0; double stddev=0.0; for(int i=0; i<BarsToShow; i++) mean+=close[start+i]-l1[i]; mean/=BarsToShow; //--- for(int i=0; i<BarsToShow; i++) stddev+=MathPow(close[start+i]-l1[i]-mean,2); stddev=MathSqrt(stddev/BarsToShow); //--- for(int i=0; i<BarsToShow; i++) VolNormalized[start+i]=stddev>0?(close[start+i]-l1[i])/stddev:0; } //--- return(rates_total); } //+------------------------------------------------------------------+

The calculation result is shown in Fig.14.

Fig.14. L1VolatilityNormalized.mq5 Indicator

3.4.4.5. L1VolatilityNormalizedSmoothed.mq5 — Smoothed Normalized Volatility Indicator

This indicator extends the normalization approach by adding exponential moving average (EMA) smoothing.

Advantages:

- Reduces the influence of short-term noise and sharp spikes;

- Produces a clearer and more interpretable volatility profile;

- Helps evaluate persistent volatility and the current market regime.

The indicator is especially useful for adaptive strategies requiring stable volatility estimation, for example when automatically selecting trading modes.

The code of the L1VolatilityNormalizedSmoothed.mq5 indicator is provided below.

//+------------------------------------------------------------------+ //| L1VolatilityNormalizedSmoothed.mq5 | //| Copyright 2000-2026, MetaQuotes Ltd. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2000-2026, MetaQuotes Ltd." #property link "https://www.mql5.com" #property version "1.00" #property indicator_separate_window #property indicator_buffers 1 #property indicator_plots 1 #property indicator_label1 "L1VolatilityNormalizedSmoothed" #property indicator_type1 DRAW_LINE #property indicator_color1 clrDeepSkyBlue #property indicator_width1 2 //--- input int BarsToShow = 1000; // Number of bars to calculate L1 input double CoefLambda = 0.015; // Lambda in lambda_max units input int SmoothPeriod = 10; // EMA smoothing period (1=no smoothing) //--- double NormVolSmooth[]; //+------------------------------------------------------------------+ //| Indicator initialization function | //+------------------------------------------------------------------+ int OnInit() { //--- prepare SetIndexBuffer(0,NormVolSmooth,INDICATOR_DATA); ArrayInitialize(NormVolSmooth,EMPTY_VALUE); PlotIndexSetDouble(0,PLOT_EMPTY_VALUE,EMPTY_VALUE); IndicatorSetInteger(INDICATOR_DIGITS,_Digits); //--- return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Indicator iteration function | //+------------------------------------------------------------------+ int OnCalculate(const int rates_total, const int prev_calculated, const datetime &time[], const double &open[], const double &high[], const double &low[], const double &close[], const long &tick_volume[], const long &volume[], const int &spread[]) { //--- check bars static bool warned=false; if(rates_total < BarsToShow) { if(!warned) { Print("Waiting for enough bars: ",BarsToShow); warned=true; } ArrayInitialize(NormVolSmooth,EMPTY_VALUE); return(0); } //--- check new bar static datetime last_bar_time=0; bool new_bar=(time[0]!=last_bar_time); bool need_recalc= (prev_calculated==0) || new_bar || (rates_total!=prev_calculated); if(!need_recalc) return(prev_calculated); last_bar_time=time[0]; int start=rates_total-BarsToShow; //--- for(int i=0; i<start; i++) NormVolSmooth[i]=EMPTY_VALUE; //--- copy close prices vector<double> price(BarsToShow); for(int i=0; i<BarsToShow; i++) price[i]=close[start+i]; //--- vector<double> l1(BarsToShow); bool res=price.L1TrendFilter(CoefLambda,true,l1); if(res) { //--- compute normalized volatility vector<double> VolNormalized(BarsToShow); double mean = 0, stddev = 0; for(int i=0; i<BarsToShow; i++) mean += close[start+i]-l1[i]; mean /= BarsToShow; //--- for(int i=0; i<BarsToShow; i++) stddev += MathPow(close[start+i]-l1[i]-mean,2); stddev = MathSqrt(stddev/BarsToShow); //--- for(int i=0; i<BarsToShow; i++) VolNormalized[i]=stddev>0 ? (close[start+i]-l1[i])/stddev: 0; //--- EMA smoothing vector<double> Smooth(BarsToShow); double alpha=(SmoothPeriod<=1) ? 1.0: 2.0/(SmoothPeriod+1.0); //--- Smooth[0] = VolNormalized[0]; for(int i=1; i<BarsToShow; i++) Smooth[i]=alpha*VolNormalized[i]+(1.0-alpha)*Smooth[i-1]; //--- copy to indicator buffer for(int i=0; i<BarsToShow; i++) NormVolSmooth[start+i]=Smooth[i]; } //--- return(rates_total); } //+------------------------------------------------------------------+

The calculation result is shown in Fig.15.

Fig.15. L1VolatilityNormalized.mq5 and L1VolatilityNormalizedSmoothed.mq5 Indicators

3.4.4.6. L1VolatilityRegime.mq5 — Market Regime Detection Indicator

The indicator classifies the current market regime based on normalized and smoothed volatility, identifying four market states.

Indicator features:

- Fully autonomous and does not require external data;

- Provides clear visualization of market dynamics for adaptive strategies;

- Threshold parameters LowVolThresh and HighVolThresh can be adjusted for different instruments and timeframes.

| Value | Regime | Description |

|---|---|---|

| 0 | Range | Low volatility, sideways market |

| 1 | Trend | Moderate volatility, presence of a trend |

| 2 | Expansion | Strong movement, market expansion |

| 3 | Panic | Extreme volatility, sharp movements |

Table 3. Regimes of the L1VolatilityRegime.mq5 Indicator

- Quickly determine the current market regime;

- Adapt trading strategies to prevailing conditions;

- Reduce risk during extreme movements and improve trading efficiency.

The code of the L1VolatilityRegime.mq5 indicator is provided below.