Статистический арбитраж с прогнозами

Введение

Статистический арбитраж — это сложная финансовая стратегия, которая использует математические модели для извлечения выгоды из неэффективности цен между взаимосвязанными финансовыми инструментами. Этот подход, обычно применяемый к акциям, облигациям или производным финансовым инструментам, требует глубокого понимания корреляции, коинтеграции и коэффициента Пирсона — важнейших инструментов для выявления и использования рыночных возможностей.

Корреляция в финансах измеряет, насколько тесно две ценные бумаги движутся по отношению друг к другу, количественно определяя степень их взаимосвязи. Положительная корреляция указывает на то, что ценные бумаги обычно движутся в одном направлении, тогда как отрицательная означает, что они движутся в противоположных направлениях. Трейдеры анализируют эти взаимосвязи, чтобы прогнозировать будущие движения цен.

Коинтеграция, более тонкое статистическое свойство, выходит за рамки корреляции, исследуя, остается ли линейная комбинация двух или более переменных временного ряда стабильной с течением времени. Проще говоря, хотя отдельные ценные бумаги могут следовать разным путям, их относительные движения связаны неким равновесием, к которому они имеют тенденцию возвращаться. Эта концепция имеет решающее значение в парной торговле, цель которой — определить пары акций, цены которых исторически движутся вместе и, как ожидается, будут продолжать двигаться в том же направлении.

Коэффициент Пирсона - статистическая мера, которая вычисляет силу и направление линейной связи между двумя переменными. Значения коэффициента Пирсона находятся в диапазоне от -1 до 1, где 1 означает идеальную положительную линейную связь, -1 — идеальную отрицательную линейную связь, а 0 — отсутствие линейной связи. В статистическом арбитраже высокое абсолютное значение коэффициента Пирсона между двумя активами может указывать на потенциальную возможность торговли, если они вернутся к долгосрочному среднему соотношению.

Трейдеры, реализующие стратегии статистического арбитража, используют алгоритмы и высокочастотные торговые системы для мониторинга и исполнения сделок. Эти системы способны обрабатывать огромные объемы данных для быстрого обнаружения аномалий в отношениях цен на активы. Стратегия предполагает, что цены коррелируемых активов сойдутся к своему историческому среднему значению, что позволит трейдеру получить прибыль от корректировки цен.

Однако успех статистического арбитража зависит не только от сложных математических моделей, но и от способности трейдера интерпретировать данные и корректировать стратегии в зависимости от меняющихся рыночных условий. Такие факторы, как внезапные экономические изменения, рыночные настроения или политические события, могут нарушить даже самые стабильные отношения, повышая уровень риска.

Объяснение с простыми примерами

Корреляция измеряет, как связаны два объекта. Представьте, что вы вместе с вашим лучшим другом всегда ходите в кино по субботам. Это пример корреляции: когда вы идете в кино, ваш друг тоже идет. Если корреляция положительная, это означает, что при увеличении одного показателя увеличивается и другой. Если отрицательная, один увеличивается, а другой уменьшается. Если корреляция равна нулю, это означает, что между объектами нет никакой связи.

Коинтеграция - статистическая концепция, используемая для описания ситуации, когда две или более переменных имеют некоторую долгосрочную взаимосвязь, даже если они могут колебаться независимо в краткосрочной перспективе. Представьте себе двух пловцов, связанных веревкой: они могут свободно плавать в бассейне, но не могут отдаляться далеко друг от друга. Коинтеграция указывает на то, что, несмотря на временные различия, эти переменные всегда будут возвращаться к общему долгосрочному равновесию или тренду.

Коэффициент Пирсона измеряет, насколько линейно связаны две переменные. Если коэффициент близок к +1, это указывает на прямую зависимость: при увеличении одной переменной увеличивается и другая. Коэффициент, близкий к -1, означает, что при увеличении одной переменной другая уменьшается, что указывает на обратную зависимость. Значение 0 означает отсутствие линейной связи. Например, измерение температуры и объема продаж прохладительных напитков может помочь понять, как связаны эти факторы, с помощью коэффициента Пирсона.

Подводя итог, можно сказать, что статистический арбитраж — это сложная, но потенциально прибыльная торговая стратегия, сочетающая в себе элементы экономики, финансов и математики. Она требует не только понимания статистических терминов, но и способности применять высокоскоростные алгоритмы для анализа рынка и исполнения сделок.

Расчет

Чтобы узнать, какие пары коинтегрированы и коррелированы, вы можете использовать следующий python-код.

import MetaTrader5 as mt5 import pandas as pd from scipy.stats import pearsonr from statsmodels.tsa.stattools import coint import numpy as np # Connect with MetaTrader 5 if not mt5.initialize(): print("Failed to initialize MT5") mt5.shutdown() # Get the list of symbols symbols = mt5.symbols_get() symbols = [s.name for s in symbols if s.name.startswith('EUR') or s.name.startswith('USD') or s.name.endswith('USD')] # Filtrar símbolos por ejemplo # Download historical data and save in dictionary data = {} for symbol in symbols: rates = mt5.copy_rates_from_pos(symbol, mt5.TIMEFRAME_D1, 0, 365) # Último año, diario if rates is not None: df = pd.DataFrame(rates) df['time'] = pd.to_datetime(df['time'], unit='s') data[symbol] = df.set_index('time')['close'] # Close connection with MT5 mt5.shutdown() # Calculate the Pearson coefficient and test for cointegration for each pair of symbols cointegrated_pairs = [] for i in range(len(symbols)): for j in range(i + 1, len(symbols)): if symbols[i] in data and symbols[j] in data: common_index = data[symbols[i]].index.intersection(data[symbols[j]].index) if len(common_index) > 30: # Asegurarse de que hay suficientes puntos de datos corr, _ = pearsonr(data[symbols[i]][common_index], data[symbols[j]][common_index]) if abs(corr) > 0.8: # Correlación fuerte score, p_value, _ = coint(data[symbols[i]][common_index], data[symbols[j]][common_index]) if p_value < 0.05: # P-valor menor que 0.05 cointegrated_pairs.append((symbols[i], symbols[j], corr, p_value)) # Filter and show only cointegrated pairs with p-value less than 0.05 print(f'Total pairs with strong correlation and cointegration: {len(cointegrated_pairs)}') for sym1, sym2, corr, p_val in cointegrated_pairs: print(f'{sym1} - {sym2}: Correlación={corr:.4f}, P-valor de Cointegración={p_val:.4f}')

Результаты:

Total pairs with strong correlation and coitegration: 54 EURUSD - USDBGN: Correlación=-0.9957, P-valor de Cointegración=0.0000 EURUSD - USDHRK: Correlación=-0.9972, P-valor de Cointegración=0.0000 GBPUSD - USDPLN: Correlación=-0.8633, P-valor de Cointegración=0.0406 GBPUSD - GBXUSD: Correlación=0.9998, P-valor de Cointegración=0.0000 GBPUSD - EURSGD: Correlación=0.8061, P-valor de Cointegración=0.0191 USDCHF - EURCHF: Correlación=0.8324, P-valor de Cointegración=0.0356 USDJPY - EURDKK: Correlación=0.8338, P-valor de Cointegración=0.0200 USDJPY - USDTHB: Correlación=0.9012, P-valor de Cointegración=0.0330 AUDUSD - USDCNH: Correlación=-0.8074, P-valor de Cointegración=0.0390 EURCHF - USDKES: Correlación=-0.9104, P-valor de Cointegración=0.0048 EURJPY - EURRON: Correlación=0.8177, P-valor de Cointegración=0.0333 EURJPY - USDCOP: Correlación=-0.9361, P-valor de Cointegración=0.0125 EURJPY - USDLAK: Correlación=0.9508, P-valor de Cointegración=0.0410 EURJPY - EURDKK: Correlación=0.8525, P-valor de Cointegración=0.0136 EURJPY - EURMXN: Correlación=-0.8785, P-valor de Cointegración=0.0172 EURJPY - USDTRY: Correlación=0.9564, P-valor de Cointegración=0.0102 EURNZD - NZDUSD: Correlación=-0.8505, P-valor de Cointegración=0.0455 EURNZD - EURDKK: Correlación=0.8242, P-valor de Cointegración=0.0017 EURCZK - USDCLP: Correlación=0.9655, P-valor de Cointegración=0.0001 USDCLP - USDCZK: Correlación=0.8972, P-valor de Cointegración=0.0147 USDCLP - USDARS: Correlación=0.8077, P-valor de Cointegración=0.0231 USDCLP - USDIDR: Correlación=0.8569, P-valor de Cointegración=0.0423 USDCLP - USDNGN: Correlación=0.8468, P-valor de Cointegración=0.0436 USDCLP - USDVND: Correlación=0.9021, P-valor de Cointegración=0.0194 USDCZK - USDIDR: Correlación=0.9005, P-valor de Cointegración=0.0086 USDCZK - USDVND: Correlación=0.8306, P-valor de Cointegración=0.0195 USDMXN - USDCOP: Correlación=0.8686, P-valor de Cointegración=0.0286 USDMXN - EURMXN: Correlación=0.9522, P-valor de Cointegración=0.0328 NZDUSD - USDSGD: Correlación=-0.8145, P-valor de Cointegración=0.0097 NZDUSD - USDTHB: Correlación=-0.8094, P-valor de Cointegración=0.0255 ADAUSD - KSMUSD: Correlación=0.9429, P-valor de Cointegración=0.0071 ALGUSD - LNKUSD: Correlación=0.8038, P-valor de Cointegración=0.0454 ATMUSD - MTCUSD: Correlación=0.9423, P-valor de Cointegración=0.0146 BTCUSD - SOLUSD: Correlación=0.9736, P-valor de Cointegración=0.0112 DGEUSD - GLDUSD: Correlación=0.8933, P-valor de Cointegración=0.0136 DGEUSD - USDGHS: Correlación=0.8562, P-valor de Cointegración=0.0101 EOSUSD - UNIUSD: Correlación=0.8176, P-valor de Cointegración=0.0051 ETCUSD - ETHUSD: Correlación=0.9745, P-valor de Cointegración=0.0009 ETCUSD - SOLUSD: Correlación=0.9206, P-valor de Cointegración=0.0093 ETCUSD - UNIUSD: Correlación=0.9236, P-valor de Cointegración=0.0249 ETHUSD - SOLUSD: Correlación=0.9430, P-valor de Cointegración=0.0074 UNIUSD - USDNGN: Correlación=0.8074, P-valor de Cointegración=0.0195 EURNOK - USDNOK: Correlación=0.9065, P-valor de Cointegración=0.0430 EURRON - USDCOP: Correlación=-0.8010, P-valor de Cointegración=0.0097 EURRON - USDCRC: Correlación=-0.8015, P-valor de Cointegración=0.0159 EURRON - USDLAK: Correlación=0.8364, P-valor de Cointegración=0.0349 GBXUSD - EURSGD: Correlación=0.8067, P-valor de Cointegración=0.0180 USDARS - USDVND: Correlación=0.8093, P-valor de Cointegración=0.0268 USDBGN - USDHRK: Correlación=0.9944, P-valor de Cointegración=0.0000 USDCOP - USDTRY: Correlación=-0.9548, P-valor de Cointegración=0.0160 USDCRC - EURDKK: Correlación=-0.8519, P-valor de Cointegración=0.0153 USDHRK - USDDKK: Correlación=0.9954, P-valor de Cointegración=0.0000 USDIDR - USDVND: Correlación=0.8196, P-valor de Cointegración=0.0417 USDSEK - USDSGD: Correlación=0.8346, P-valor de Cointegración=0.0264

Пары отсортированы.

Для проверки значений с помощью MetaTrader 5 у нас есть индикатор (Pearson.mq5):

//+------------------------------------------------------------------+ //| PearsonIndicator.mq5 | //| Copyright Javier S. Gastón de Iriarte Cabrera | //| https://www.mql5.com/en/users/jsgaston/news | //+------------------------------------------------------------------+ #property copyright "Javier S. Gastón de Iriarte Cabrera" #property link "https://www.mql5.com/en/users/jsgaston/news/" #property version "1.00" #property indicator_separate_window #property indicator_buffers 1 #property indicator_color1 Red input string Symbol2 = "GBPUSD"; // Second financial instrument input int BarsBack = 100; // Number of bars to include in correlation calculation double CorrelationBuffer[]; //+------------------------------------------------------------------+ //| Custom indicator initialization function | //+------------------------------------------------------------------+ int OnInit() { SetIndexBuffer(0, CorrelationBuffer, INDICATOR_DATA); PlotIndexSetInteger(0, PLOT_DRAW_TYPE, DRAW_LINE); PlotIndexSetString(0, PLOT_LABEL, "Pearson Correlation"); IndicatorSetString(INDICATOR_SHORTNAME, "Pearson Correlation (" + Symbol() + " & " + Symbol2 + ")"); return INIT_SUCCEEDED; } //+------------------------------------------------------------------+ //| Custom indicator iteration function | //+------------------------------------------------------------------+ int OnCalculate(const int rates_total, const int prev_calculated, const datetime &time[], const double &open[], const double &high[], const double &low[], const double &close[], const long &tick_volume[], const long &volume[], const int &spread[]) { if (rates_total < BarsBack) return 0; // Ensure enough bars are present double prices1[], prices2[]; ArrayResize(prices1, BarsBack); ArrayResize(prices2, BarsBack); // Copy historical data for primary symbol if (CopyClose(Symbol(), PERIOD_CURRENT, 0, BarsBack, prices1) <= 0) { Print("Error copying prices for ", Symbol()); return 0; } // Copy historical data for secondary symbol if (CopyClose(Symbol2, PERIOD_CURRENT, 0, BarsBack, prices2) <= 0) { Print("Error copying prices for ", Symbol2); return 0; } // Calculate Pearson correlation for the entire buffer double correlation = CalculatePearsonCorrelation(prices1, prices2); Print("Pearson correlation: ", correlation); // Fill the buffer for the indicator for (int i = BarsBack; i < rates_total; i++) { CorrelationBuffer[i] = correlation; // Update the buffer correctly } return(rates_total); } //+------------------------------------------------------------------+ //| Calculate Pearson correlation coefficient | //+------------------------------------------------------------------+ double CalculatePearsonCorrelation(double &prices1[], double &prices2[]) { int length = BarsBack; double mean1 = 0, mean2 = 0; double sum1 = 0, sum2 = 0, sumProd = 0, stdev1 = 0, stdev2 = 0; for (int i = 0; i < length; i++) { mean1 += prices1[i]; mean2 += prices2[i]; } mean1 /= length; mean2 /= length; for (int i = 0; i < length; i++) { double dev1 = prices1[i] - mean1; double dev2 = prices2[i] - mean2; sum1 += dev1 * dev1; sum2 += dev2 * dev2; sumProd += dev1 * dev2; } stdev1 = sqrt(sum1); stdev2 = sqrt(sum2); if (stdev1 == 0 || stdev2 == 0) return 0; // Avoid division by zero return sumProd / (stdev1 * stdev2); } //+------------------------------------------------------------------+

Результаты:

Создание моделей ONNX

После определения пары символов, которые коррелируют и коинтегрируются, и проверки коэффициента Пирсона в MQL5, мы можем создать модель ONNX для изучения двух пар на истории.

# python libraries import MetaTrader5 as mt5 import tensorflow as tf import numpy as np import pandas as pd import tf2onnx # input parameters inp_history_size = 120 sample_size = 120*20 symbol = "AUDUSD" optional = "D1" inp_model_name = str(symbol)+"_"+str(optional)+".onnx" if not mt5.initialize(): print("initialize() failed, error code =",mt5.last_error()) quit() # we will save generated onnx-file near the our script to use as resource from sys import argv data_path=argv[0] last_index=data_path.rfind("\\")+1 data_path=data_path[0:last_index] print("data path to save onnx model",data_path) # and save to MQL5\Files folder to use as file terminal_info=mt5.terminal_info() file_path=terminal_info.data_path+"\\MQL5\\Files\\" print("file path to save onnx model",file_path) # set start and end dates for history data from datetime import timedelta, datetime #end_date = datetime.now() end_date = datetime(2023, 1, 1, 0) start_date = end_date - timedelta(days=inp_history_size*20) # print start and end dates print("data start date =",start_date) print("data end date =",end_date) # get rates eurusd_rates = mt5.copy_rates_from(symbol, mt5.TIMEFRAME_D1, end_date, sample_size) # create dataframe df = pd.DataFrame(eurusd_rates) # get close prices only data = df.filter(['close']).values # scale data from sklearn.preprocessing import MinMaxScaler scaler=MinMaxScaler(feature_range=(0,1)) scaled_data = scaler.fit_transform(data) # training size is 80% of the data training_size = int(len(scaled_data)*0.80) print("Training_size:",training_size) train_data_initial = scaled_data[0:training_size,:] test_data_initial = scaled_data[training_size:,:1] # split a univariate sequence into samples def split_sequence(sequence, n_steps): X, y = list(), list() for i in range(len(sequence)): # find the end of this pattern end_ix = i + n_steps # check if we are beyond the sequence if end_ix > len(sequence)-1: break # gather input and output parts of the pattern seq_x, seq_y = sequence[i:end_ix], sequence[end_ix] X.append(seq_x) y.append(seq_y) return np.array(X), np.array(y) # split into samples time_step = inp_history_size x_train, y_train = split_sequence(train_data_initial, time_step) x_test, y_test = split_sequence(test_data_initial, time_step) # reshape input to be [samples, time steps, features] which is required for LSTM x_train =x_train.reshape(x_train.shape[0],x_train.shape[1],1) x_test = x_test.reshape(x_test.shape[0],x_test.shape[1],1) # define model from keras.models import Sequential from keras.layers import Dense, Activation, Conv1D, MaxPooling1D, Dropout, Flatten, LSTM from keras.metrics import RootMeanSquaredError as rmse from tensorflow.keras import callbacks model = Sequential() model.add(Conv1D(filters=256, kernel_size=2, activation='relu',padding = 'same',input_shape=(inp_history_size,1))) model.add(MaxPooling1D(pool_size=2)) model.add(LSTM(100, return_sequences = True)) model.add(Dropout(0.3)) model.add(LSTM(100, return_sequences = False)) model.add(Dropout(0.3)) model.add(Dense(units=1, activation = 'sigmoid')) model.compile(optimizer='adam', loss= 'mse' , metrics = [rmse()]) # Set up early stopping early_stopping = callbacks.EarlyStopping( monitor='val_loss', patience=20, restore_best_weights=True, ) # model training for 300 epochs history = model.fit(x_train, y_train, epochs = 300 , validation_data = (x_test,y_test), batch_size=32, callbacks=[early_stopping], verbose=2) # evaluate training data train_loss, train_rmse = model.evaluate(x_train,y_train, batch_size = 32) print(f"train_loss={train_loss:.3f}") print(f"train_rmse={train_rmse:.3f}") # evaluate testing data test_loss, test_rmse = model.evaluate(x_test,y_test, batch_size = 32) print(f"test_loss={test_loss:.3f}") print(f"test_rmse={test_rmse:.3f}") # save model to ONNX output_path = data_path+inp_model_name onnx_model = tf2onnx.convert.from_keras(model, output_path=output_path) print(f"saved model to {output_path}") output_path = file_path+inp_model_name onnx_model = tf2onnx.convert.from_keras(model, output_path=output_path) print(f"saved model to {output_path}") # finish mt5.shutdown() #prediction using testing data #prediction using testing data test_predict = model.predict(x_test) print(test_predict) print("longitud total de la prediccion: ", len(test_predict)) print("longitud total del sample: ", sample_size) plot_y_test = np.array(y_test).reshape(-1, 1) # Selecciona solo el último elemento de cada muestra de prueba plot_y_train = y_train.reshape(-1,1) train_predict = model.predict(x_train) #print(plot_y_test) #calculate metrics from sklearn import metrics from sklearn.metrics import r2_score #transform data to real values value1=scaler.inverse_transform(plot_y_test) #print(value1) # Escala las predicciones inversas al transformarlas a la escala original value2 = scaler.inverse_transform(test_predict.reshape(-1, 1)) #print(value2) #calc score score = np.sqrt(metrics.mean_squared_error(value1,value2)) print("RMSE : {}".format(score)) print("MSE :", metrics.mean_squared_error(value1,value2)) print("R2 score :",metrics.r2_score(value1,value2)) #sumarize model model.summary() #Print error value11=pd.DataFrame(value1) value22=pd.DataFrame(value2) #print(value11) #print(value22) value111=value11.iloc[:,:] value222=value22.iloc[:,:] print("longitud salida (tandas de 1 hora): ",len(value111) ) print("en horas son " + str((len(value111))*60*24)+ " minutos") print("en horas son " + str(((len(value111)))*60*24/60)+ " horas") print("en horas son " + str(((len(value111)))*60*24/60/24)+ " dias") # Calculate error error = value111 - value222 import matplotlib.pyplot as plt # Plot error plt.figure(figsize=(10, 6)) plt.scatter(range(len(error)), error, color='blue', label='Error') plt.axhline(y=0, color='red', linestyle='--', linewidth=1) # Línea horizontal en y=0 plt.title('Error de Predicción ' + str(symbol)) plt.xlabel('Índice de la muestra') plt.ylabel('Error') plt.legend() plt.grid(True) plt.savefig(str(symbol)+str(optional)+'.png') rmse_ = format(score) mse_ = metrics.mean_squared_error(value1,value2) r2_ = metrics.r2_score(value1,value2) resultados= [rmse_,mse_,r2_] # Abre un archivo en modo escritura with open(str(symbol)+str(optional)+"results.txt", "w") as archivo: # Escribe cada resultado en una línea separada for resultado in resultados: archivo.write(str(resultado) + "\n") # finish mt5.shutdown() #show iteration-rmse graph for training and validation plt.figure(figsize = (18,10)) plt.plot(history.history['root_mean_squared_error'],label='Training RMSE',color='b') plt.plot(history.history['val_root_mean_squared_error'],label='Validation-RMSE',color='g') plt.xlabel("Iteration") plt.ylabel("RMSE") plt.title("RMSE" + str(symbol)) plt.legend() plt.savefig(str(symbol)+str(optional)+'1.png') #show iteration-loss graph for training and validation plt.figure(figsize = (18,10)) plt.plot(history.history['loss'],label='Training Loss',color='b') plt.plot(history.history['val_loss'],label='Validation-loss',color='g') plt.xlabel("Iteration") plt.ylabel("Loss") plt.title("LOSS" + str(symbol)) plt.legend() plt.savefig(str(symbol)+str(optional)+'2.png') #show actual vs predicted (training) graph plt.figure(figsize=(18,10)) plt.plot(scaler.inverse_transform(plot_y_train),color = 'b', label = 'Original') plt.plot(scaler.inverse_transform(train_predict),color='red', label = 'Predicted') plt.title("Prediction Graph Using Training Data" + str(symbol)) plt.xlabel("Hours") plt.ylabel("Price") plt.legend() plt.savefig(str(symbol)+str(optional)+'3.png') #show actual vs predicted (testing) graph plt.figure(figsize=(18,10)) plt.plot(scaler.inverse_transform(plot_y_test),color = 'b', label = 'Original') plt.plot(scaler.inverse_transform(test_predict),color='g', label = 'Predicted') plt.title("Prediction Graph Using Testing Data" + str(symbol)) plt.xlabel("Hours") plt.ylabel("Price") plt.legend() plt.savefig(str(symbol)+str(optional)+'4.png')

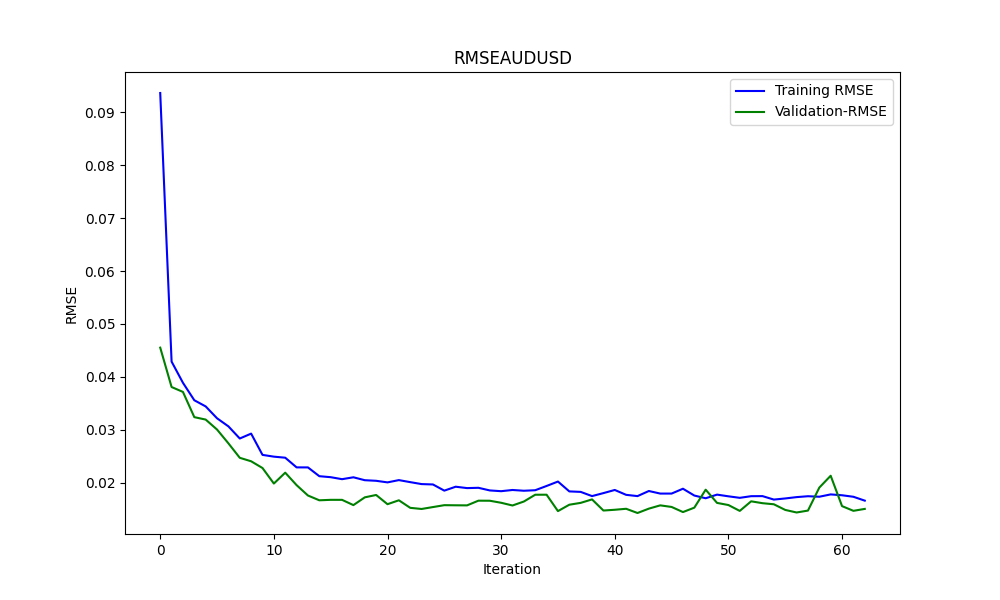

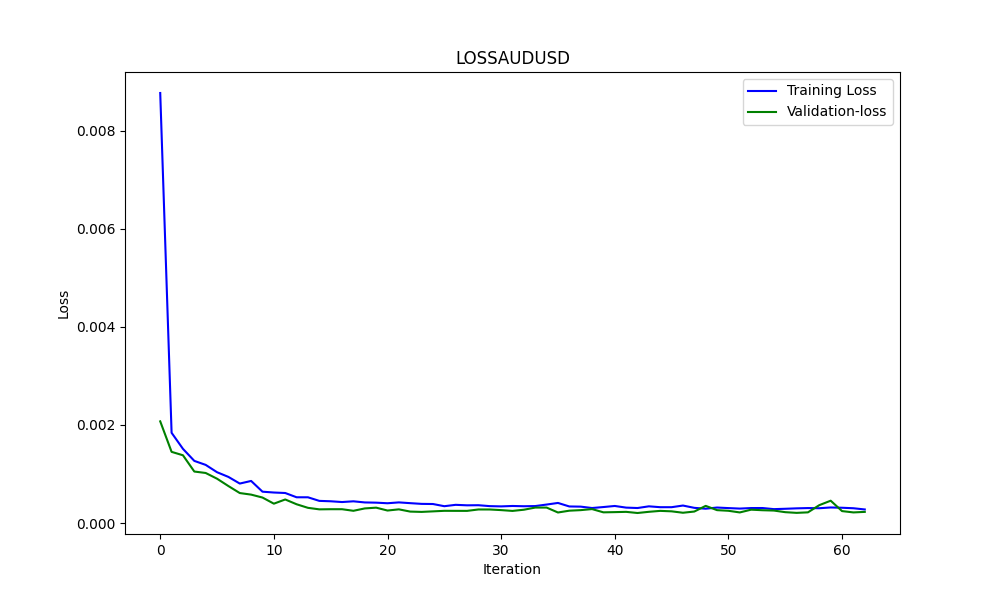

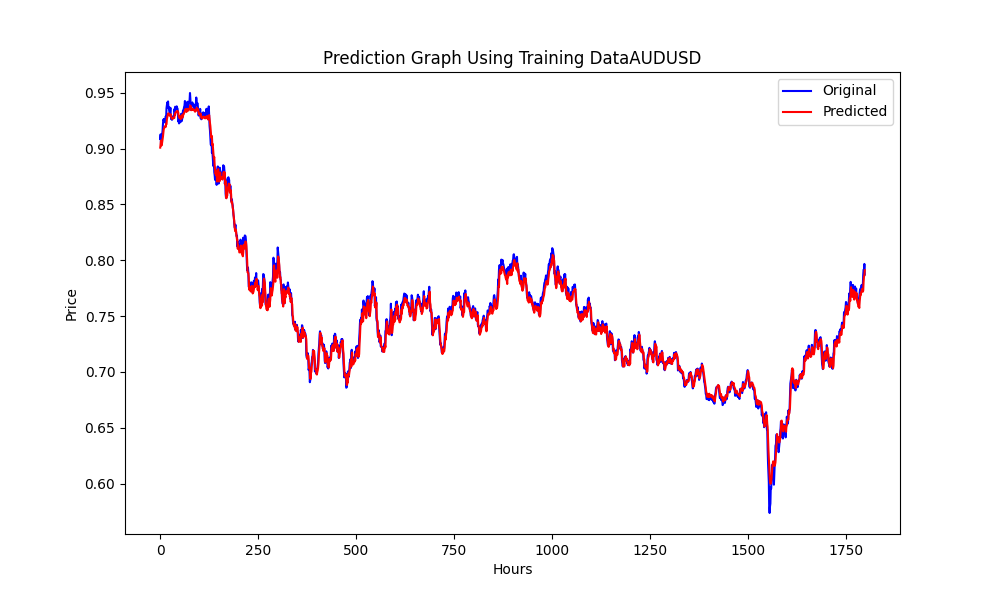

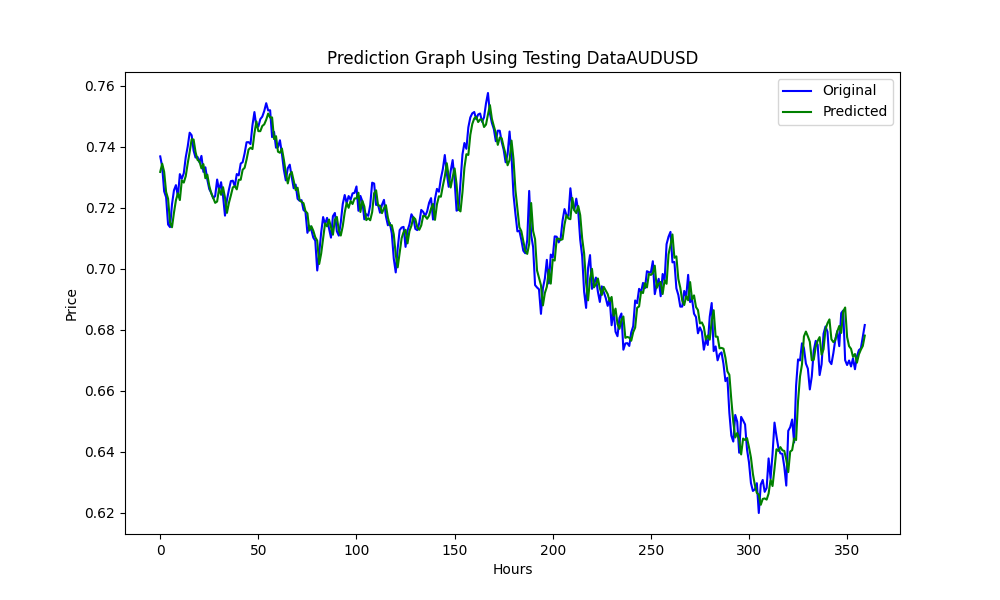

Результатом является модель ONNX. Ниже представлены некоторые графики и значения. Нам понадобятся обе модели из выбранных нами пар корреляции и коинтеграции:

Результаты:

0.005679790676089899 3.226002212419775e-05 0.9670613229880559

Это RMSE, MSE и R2 соответственно.

Тестирование на истории с помощью Python

Вы можете использовать следующий код. Просто измените стратегию и проверьте результаты тестирования на истории:

import MetaTrader5 as mt5 import pandas as pd from scipy.stats import pearsonr from statsmodels.tsa.stattools import coint import numpy as np # Función para la estrategia de Pairs Trading def pairs_trading_strategy(data0, data1): spread = data0 - data1 short_entry = np.mean(spread) - 2 * np.std(spread) short_exit = np.mean(spread) long_entry = np.mean(spread) + 2 * np.std(spread) long_exit = np.mean(spread) positions = [] for i in range(len(spread)): if spread[i] > long_entry and (not positions or positions[-1][1] != 1): positions.append((spread[i], 1)) elif spread[i] < short_entry and (not positions or positions[-1][1] != -1): positions.append((spread[i], -1)) elif spread[i] < long_exit and positions and positions[-1][1] == 1: positions.append((spread[i], 0)) elif spread[i] > short_exit and positions and positions[-1][1] == -1: positions.append((spread[i], 0)) return positions # Conectar con MetaTrader 5 if not mt5.initialize(): print("No se pudo inicializar MT5") mt5.shutdown() # Obtener la lista de símbolos symbols = mt5.symbols_get() symbols = [s.name for s in symbols if 'EUR' in s.name or 'USD' in s.name] # Filtrar símbolos data = {} for symbol in symbols: rates = mt5.copy_rates_from_pos(symbol, mt5.TIMEFRAME_D1, 0, 365) if rates is not None: df = pd.DataFrame(rates) df['time'] = pd.to_datetime(df['time'], unit='s') # Convertir a datetime df.set_index('time', inplace=True) data[symbol] = df['close'] mt5.shutdown() # Identificar pares cointegrados cointegrated_pairs = [] for i in range(len(symbols)): for j in range(i + 1, len(symbols)): if symbols[i] in data and symbols[j] in data: common_index = data[symbols[i]].index.intersection(data[symbols[j]].index) if len(common_index) > 30: corr, _ = pearsonr(data[symbols[i]][common_index], data[symbols[j]][common_index]) if abs(corr) > 0.8: score, p_value, _ = coint(data[symbols[i]][common_index], data[symbols[j]][common_index]) if p_value < 0.05: cointegrated_pairs.append((symbols[i], symbols[j], corr, p_value)) print(cointegrated_pairs) # Ejecutar estrategia de Pairs Trading para pares cointegrados for sym1, sym2, _, _ in cointegrated_pairs: positions = [] df0 = data[sym1] df1 = data[sym2] positions = pairs_trading_strategy(df0.values, df1.values) print(f'Backtesting completed for pair: {sym1} - {sym2}') print('Positions:', positions)

Тестирование на истории с помощью тестера стратегий MetaTrader 5

Теперь у нас есть модели ONNX и мы можем запустить советник. Я решил использовать простую стратегию. Вы же можете выбрать любую стратегию по вашему желанию. Буду рад, если вы покажете свою стратегию и результаты.

При первом запуске NZDUSD и AUDUSD были коинтегрированы и коррелированы, но на данный момент они не проходят фильтр (коинтеграция меньше 0,05). В учебных целях и для того, чтобы избежать необходимости снова создавать модели ONNX, я продолжу использовать эти два символа.

//+------------------------------------------------------------------+ //| Hybrid Arbitrage_Statistic ONNX.mq5| //| Copyright 2024, Javier S. Gastón de Iriarte Cabrera. | //| https://www.mql5.com/en/users/jsgaston/news | //+------------------------------------------------------------------+ #property copyright "Copyright 2024, Javier S. Gastón de Iriarte Cabrera." #property link "https://www.mql5.com/en/users/jsgaston/news" #property version "1.00" #property strict #include <Trade\Trade.mqh> input double lotSize = 0.1; //input double slippage = 3; input double stopLoss = 1500; input double takeProfit = 1500; //input double maxSpreadPoints = 10.0; #resource "/Files/art/hybrid/NZDUSD_D1.onnx" as uchar ExtModel[] #resource "/Files/art/hybrid/AUDUSD_D1.onnx" as uchar ExtModel2[] #define SAMPLE_SIZE 120 string symbol1 = _Symbol; input string symbol2 = "AUDUSD"; ulong ticket1 = 0; ulong ticket2 = 0; input bool isArbitrageActive = true; CTrade ExtTrade; double spreads[1000]; // Array para almacenar hasta 1000 spreads int spreadIndex = 0; // Índice para el próximo spread a almacenar long ExtHandle=INVALID_HANDLE; //int ExtPredictedClass=-1; datetime ExtNextBar=0; datetime ExtNextDay=0; float ExtMin=0.0; float ExtMax=0.0; long ExtHandle2=INVALID_HANDLE; //int ExtPredictedClass=-1; datetime ExtNextBar2=0; datetime ExtNextDay2=0; float ExtMin2=0.0; float ExtMax2=0.0; float predicted=0.0; float predicted2=0.0; float lastPredicted1=0.0; float lastPredicted2=0.0; int Order=0; //+------------------------------------------------------------------+ //| Expert initialization function | //+------------------------------------------------------------------+ int OnInit() { Print("EA de arbitraje ONNX iniciado"); //--- create a model from static buffer ExtHandle=OnnxCreateFromBuffer(ExtModel,ONNX_DEFAULT); if(ExtHandle==INVALID_HANDLE) { Print("OnnxCreateFromBuffer error ",GetLastError()); return(INIT_FAILED); } //--- since not all sizes defined in the input tensor we must set them explicitly //--- first index - batch size, second index - series size, third index - number of series (only Close) const long input_shape[] = {1,SAMPLE_SIZE,1}; if(!OnnxSetInputShape(ExtHandle,ONNX_DEFAULT,input_shape)) { Print("OnnxSetInputShape error ",GetLastError()); return(INIT_FAILED); } //--- since not all sizes defined in the output tensor we must set them explicitly //--- first index - batch size, must match the batch size of the input tensor //--- second index - number of predicted prices (we only predict Close) const long output_shape[] = {1,1}; if(!OnnxSetOutputShape(ExtHandle,0,output_shape)) { Print("OnnxSetOutputShape error ",GetLastError()); return(INIT_FAILED); } //--- create a model from static buffer ExtHandle2=OnnxCreateFromBuffer(ExtModel2,ONNX_DEFAULT); if(ExtHandle2==INVALID_HANDLE) { Print("OnnxCreateFromBuffer error ",GetLastError()); return(INIT_FAILED); } //--- since not all sizes defined in the input tensor we must set them explicitly //--- first index - batch size, second index - series size, third index - number of series (only Close) const long input_shape2[] = {1,SAMPLE_SIZE,1}; if(!OnnxSetInputShape(ExtHandle2,ONNX_DEFAULT,input_shape2)) { Print("OnnxSetInputShape error ",GetLastError()); return(INIT_FAILED); } //--- since not all sizes defined in the output tensor we must set them explicitly //--- first index - batch size, must match the batch size of the input tensor //--- second index - number of predicted prices (we only predict Close) const long output_shape2[] = {1,1}; if(!OnnxSetOutputShape(ExtHandle2,0,output_shape2)) { Print("OnnxSetOutputShape error ",GetLastError()); return(INIT_FAILED); } return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Expert deinitialization function | //+------------------------------------------------------------------+ void OnDeinit(const int reason) { if(ExtHandle!=INVALID_HANDLE) { OnnxRelease(ExtHandle); ExtHandle=INVALID_HANDLE; } if(ExtHandle2!=INVALID_HANDLE) { OnnxRelease(ExtHandle2); ExtHandle2=INVALID_HANDLE; } } //+------------------------------------------------------------------+ //| Expert tick function | //+------------------------------------------------------------------+ void OnTick() { //--- check new day if(TimeCurrent()>=ExtNextDay) { GetMinMax(); GetMinMax2(); //--- set next day time ExtNextDay=TimeCurrent(); ExtNextDay-=ExtNextDay%PeriodSeconds(PERIOD_D1); ExtNextDay+=PeriodSeconds(PERIOD_D1); /*ExtTrade.PositionClose(symbol1); ExtTrade.PositionClose(symbol2); ticket1 = 0; ticket2 = 0;*/ } //--- check new bar if(TimeCurrent()<ExtNextBar) { return; } //--- set next bar time ExtNextBar=TimeCurrent(); ExtNextBar-=ExtNextBar%PeriodSeconds(); ExtNextBar+=PeriodSeconds(); //--- check min and max float close=(float)iClose(symbol1,PERIOD_D1,0); if(ExtMin>close) ExtMin=close; if(ExtMax<close) ExtMax=close; float close2=(float)iClose(symbol2,PERIOD_D1,0); if(ExtMin2>close2) ExtMin2=close2; if(ExtMax2<close2) ExtMax2=close2; lastPredicted1=predicted; lastPredicted2=predicted2; //--- predict next price PredictPrice(); PredictPrice2(); if(!isArbitrageActive || ArePositionsOpen()) { Print("Arbitraje inactivo o ya hay posiciones abiertas."); return; } double price1 = SymbolInfoDouble(symbol1, SYMBOL_BID); double price2 = SymbolInfoDouble(symbol2, SYMBOL_ASK); double currentSpread = MathAbs(price1 - price2); Print("current spread ", currentSpread); Print("Price1 ",price1); Print("Price2 ",price2); Print("PricePredicted1 ",predicted); Print("PricePredicted2 ",predicted2); Print("Last PricePredicted1 ",lastPredicted1); Print("Last PricePredicted2 ",lastPredicted2); double predictedSpread = MathAbs(predicted - predicted2); Print("Predicted spread ", predictedSpread); double LastpredictedSpread = MathAbs(lastPredicted1 - lastPredicted2); Print("Last Predicted spread ", LastpredictedSpread); // Almacenar el spread actual en el array y actualizar el índice spreads[spreadIndex % 1000] = currentSpread; spreadIndex++; // Verifica si hay suficientes datos para calcular la desviación estándar int count = MathMin(spreadIndex, 1000); // Utiliza todos los datos disponibles hasta 1000 double stdDevSpread = CalculateStdDev(spreads, 0, count); //Print("StdDevSpread ", stdDevSpread); // Verifica si el spread es lo suficientemente bajo para el arbitraje if(LastpredictedSpread< currentSpread) { // Inicia el arbitraje si aún no está activo if(isArbitrageActive) { //Print("max spread : ",maxSpreadPoints * _Point); double meanSpread = (lastPredicted1 + lastPredicted2) / 2.0; Print("mean spread: ",meanSpread); double stdDevSpread = CalculateStdDev(spreads, 0, ArraySize(spreads)); Print("StdDevSpread ", stdDevSpread); double shortEntry = meanSpread - 2 * stdDevSpread ; double shortExit = meanSpread; double longEntry = meanSpread + 2 * stdDevSpread ; double longExit = meanSpread; Print("Long Entry: ", longEntry, " Short Entry: ", shortEntry); // Comprueba si la condición de entrada corta se cumple para el arbitraje if(price1 < shortEntry && (ticket1 == 0 || ticket2 == 0)) { Print("Preparando para abrir órdenes"); Order = 1; Print("Error al abrir posiciones de arbitraje: ", GetLastError()); ticket1 = ExtTrade.PositionOpen(symbol1, ORDER_TYPE_BUY, lotSize, price1, price1 - stopLoss * _Point, price1 + takeProfit * _Point, "Arbitraje"); ticket2 = ExtTrade.PositionOpen(symbol2, ORDER_TYPE_SELL, lotSize, price2, price2 + stopLoss * _Point, price2 - takeProfit * _Point, "Arbitraje"); ticket1=0; ticket2=0; } else if(price2 < shortEntry && (ticket1 == 0 || ticket2 == 0)) { Print("Preparando para abrir órdenes"); Order = 2; Print("Error al abrir posiciones de arbitraje: ", GetLastError()); ticket1 = ExtTrade.PositionOpen(symbol1, ORDER_TYPE_SELL, lotSize, price1, price1 + stopLoss * _Point, price1 - takeProfit * _Point, "Arbitraje"); ticket2 = ExtTrade.PositionOpen(symbol2, ORDER_TYPE_BUY, lotSize, price2, price2 - stopLoss * _Point, price2 + takeProfit * _Point, "Arbitraje"); ticket1=0; ticket2=0; } else if(price1 > longEntry && (ticket1 == 0 || ticket2 == 0)) { Print("Preparando para abrir órdenes"); Order = 3; Print("Error al abrir posiciones de arbitraje: ", GetLastError()); ticket1 = ExtTrade.PositionOpen(symbol1, ORDER_TYPE_SELL, lotSize, price1, price1 + stopLoss * _Point, price1 - takeProfit * _Point, "Arbitraje"); ticket2 = ExtTrade.PositionOpen(symbol2, ORDER_TYPE_BUY, lotSize, price2, price2 - stopLoss * _Point, price2 + takeProfit * _Point, "Arbitraje"); ticket1=0; ticket2=0; } else if(price2 > longEntry && (ticket1 == 0 || ticket2 == 0)) { Print("Preparando para abrir órdenes"); Order = 4; Print("Error al abrir posiciones de arbitraje: ", GetLastError()); ticket1 = ExtTrade.PositionOpen(symbol1, ORDER_TYPE_BUY, lotSize, price1, price1 - stopLoss * _Point, price1 + takeProfit * _Point, "Arbitraje"); ticket2 = ExtTrade.PositionOpen(symbol2, ORDER_TYPE_SELL, lotSize, price2, price2 + stopLoss * _Point, price2 - takeProfit * _Point, "Arbitraje"); ticket1=0; ticket2=0; } } } //+------------------------------------------------------------------+ //| | //+------------------------------------------------------------------+ double meanSpread = (lastPredicted1 + lastPredicted2) / 2.0; //Print("mean spread: ",meanSpread); double stdDevSpread2 = CalculateStdDev(spreads, 0, ArraySize(spreads)); //Print("StdDevSpread ", stdDevSpread); double shortEntry = meanSpread - 2 * stdDevSpread2 ; double shortExit = meanSpread; double longEntry = meanSpread + 2 * stdDevSpread2 ; double longExit = meanSpread; if((price2 < longExit && ticket2 != 0 && Order==4) || (price1 > shortExit && ticket1 != 0 && Order==1) || (price2 > shortExit && ticket1 != 0 && Order==2) || (price1 < longExit && ticket2 != 0 && Order==3)) { ExtTrade.PositionClose(ticket1); ExtTrade.PositionClose(ticket2); ticket1 = 0; ticket2 = 0; Print("Arbitraje detenido - Cerrando órdenes"); } } //+------------------------------------------------------------------+ //| | //+------------------------------------------------------------------+ double CalculateStdDev(double &data[], int start, int count) { double sum = 0; double sumSq = 0; for(int i = start; i < start + count; i++) { sum += data[i]; sumSq += data[i] * data[i]; } double mean = sum / count; double variance = (sumSq / count) - (mean * mean); return MathSqrt(variance); } //+------------------------------------------------------------------+ //| | //+------------------------------------------------------------------+ bool ArePositionsOpen() { // Check for positions on symbol1 if(PositionSelect(symbol1) && PositionGetDouble(POSITION_VOLUME) > 0) return true; // Check for positions on symbol2 if(PositionSelect(symbol2) && PositionGetDouble(POSITION_VOLUME) > 0) return true; return false; } //+------------------------------------------------------------------+ void PredictPrice(void) { static vectorf output_data(1); // vector to get result static vectorf x_norm(SAMPLE_SIZE); // vector for prices normalize //--- check for normalization possibility if(ExtMin>=ExtMax) { Print("ExtMin>=ExtMax"); //ExtPredictedClass=-1; return; } //--- request last bars if(!x_norm.CopyRates(_Symbol,PERIOD_D1,COPY_RATES_CLOSE,1,SAMPLE_SIZE)) { Print("CopyRates ",x_norm.Size()); //ExtPredictedClass=-1; return; } float last_close=x_norm[SAMPLE_SIZE-1]; //--- normalize prices x_norm-=ExtMin; x_norm/=(ExtMax-ExtMin); //--- run the inference if(!OnnxRun(ExtHandle,ONNX_NO_CONVERSION,x_norm,output_data)) { Print("OnnxRun"); //ExtPredictedClass=-1; return; } //--- denormalize the price from the output value predicted=output_data[0]*(ExtMax-ExtMin)+ExtMin; //return predicted; } //+------------------------------------------------------------------+ //| | //+------------------------------------------------------------------+ void PredictPrice2(void) { static vectorf output_data2(1); // vector to get result static vectorf x_norm2(SAMPLE_SIZE); // vector for prices normalize //--- check for normalization possibility if(ExtMin2>=ExtMax2) { Print("ExtMin2>=ExtMax2"); //ExtPredictedClass=-1; return; } //--- request last bars if(!x_norm2.CopyRates(symbol2,PERIOD_D1,COPY_RATES_CLOSE,1,SAMPLE_SIZE)) { Print("CopyRates ",x_norm2.Size()); //ExtPredictedClass=-1; return; } float last_close2=x_norm2[SAMPLE_SIZE-1]; //--- normalize prices x_norm2-=ExtMin2; x_norm2/=(ExtMax2-ExtMin2); //--- run the inference if(!OnnxRun(ExtHandle2,ONNX_NO_CONVERSION,x_norm2,output_data2)) { Print("OnnxRun"); //ExtPredictedClass=-1; return; } //--- denormalize the price from the output value predicted2=output_data2[0]*(ExtMax2-ExtMin2)+ExtMin2; //--- classify predicted price movement //return predicted2; } //+------------------------------------------------------------------+ //| Get minimal and maximal Close for last 120 days | //+------------------------------------------------------------------+ void GetMinMax(void) { vectorf close; close.CopyRates(_Symbol,PERIOD_D1,COPY_RATES_CLOSE,0,SAMPLE_SIZE); ExtMin=close.Min(); ExtMax=close.Max(); } //+------------------------------------------------------------------+ //| Get minimal and maximal Close for last 120 days | //+------------------------------------------------------------------+ void GetMinMax2(void) { vectorf close2; close2.CopyRates(symbol2,PERIOD_D1,COPY_RATES_CLOSE,0,SAMPLE_SIZE); ExtMin2=close2.Min(); ExtMax2=close2.Max(); }

Это результаты для NZDUSD и AUDUSD M1 с моделями ONNX для однодневного периода времени со стоп-лоссом в 1500 пунктов и тейк-профитом в 1500 пунктов с моделями, которые дают прогноз с первого января 2023 до первого января 2024 года :

Чтобы выбрать другие пары для сортировки, измените эту строку:

symbols = [s.name for s in symbols if s.name.startswith('EUR') or s.name.startswith('USD') or s.name.endswith('USD')]

Пример 2

Арбитраж очень часто используется в торговле акциями, поэтому мне интересно рассмотреть еще один пример с парами из NASDAQ.

В моем случае я заменил эту строку:

symbols = [s.name for s in symbols if s.name.startswith('EUR') or s.name.startswith('USD') or s.name.endswith('USD')]

следующей:

# Crea un DataFrame con la información completa de los símbolos

symbols_df = pd.DataFrame([{'Symbol': symbol.name, 'Path': symbol.path} for symbol in all_symbols])

# Filtra adicionalmente para obtener solo los CFDs de NASDAQ

# Asumiendo que los CFDs tienen un identificador único en el 'Path'

nasdaq_group4_df = symbols_df[symbols_df['Path'].str.contains('NASDAQ')]

# Filtra aún más para obtener solo los símbolos que NO contienen '.'

nasdaq_group4_df3 = nasdaq_group4_df[nasdaq_group4_df['Symbol'].str.contains('#')]

nasdaq_group4_df2 = nasdaq_group4_df3[~nasdaq_group4_df3['Symbol'].str.contains('\.')]

# Ahora, obtenemos la lista de símbolos filtrados

filtered_symbols = nasdaq_group4_df2['Symbol'].tolist()

# Descargar datos históricos y almacenar en un diccionario

symbols = filtered_symbols Здесь отсортированы пары:

(Было так много пар, коинтегрированных и коррелированных, что мне пришлось изменить скрипт. Я модифицировал скрипт .py, чтобы вывести его в csv.)

Изменения:

# Filtrar y guardar solo los pares cointegrados con p-valor menor de 0.05 en un archivo CSV

result_df = pd.DataFrame(cointegrated_pairs, columns=['Symbol1', 'Symbol2', 'Correlation', 'Cointegration P-value'])

result_df.to_csv('cointegrated_pairs.csv', index=False)

# Imprimir el total de pares cointegrados

print(f'Total de pares con fuerte correlación y cointegrados: {len(cointegrated_pairs)}') Это пары, отфильтрованные из NASDAQ (Excel с результатами прилагается).

На данный момент я продолжу работу с моделями Amazon и Netflix, которые прогнозируют период с первого января 2023 года по первое января 2024 года.

#AMZN #NFLX 0.966605859 0.021683012

Для получения лучших результатов размер выборки был увеличен в три раза.

sample_size = 120*25*3

Вот пример результата:

6.856399020501732 47.010207528337105 0.9395402850007741

25.975755379462548 674.7398675336775 0.9735838717570285

Сто стоп-лоссом 400 и тейк-профитом 800

Затем я настроил стоп-лоссы и тейк-профиты. Вот что мы получили в результате быстрой оптимизации:

Все скрипты и ONNX с советниками прилагаются к данной статье. Вы можете скачать их и использовать для получения результатов. Вам нужно будет самостоятельно создавать новые ONNX в нужные вам даты (не забудьте изменить даты в обучающих файлах .py), а также даты в тестере стратегий. Пример: модели ONNX для периодов времени D1 и 120*3*25 данных можно использовать максимум в течение года (но на вашем месте я бы создавал их каждую неделю или месяц).

Помните, это всего лишь пример, а не готовый к использованию торговый робот. Вы вряд ли найдете готового робота бесплатно в Интернете.

Заключение

Мы увидели, как использовать корреляцию и коинтеграцию, и создали индикатор коэффициента Пирсона и советник для арбитражной торговли с использованием прогнозов. Лучшие результаты можно получить при использовании правильных пар из фильтра .py. Вы можете точно настроить стоп-уровни, чтобы добиться лучших результатов, а также усложнить стратегию.

Не забудьте сохранить модели ONNX в папке MQL5/Files, индикатор mq5 - в папке Indicator, а советник - в папке Experts.

Перевод с английского произведен MetaQuotes Ltd.

Оригинальная статья: https://www.mql5.com/en/articles/14846

Предупреждение: все права на данные материалы принадлежат MetaQuotes Ltd. Полная или частичная перепечатка запрещена.

Данная статья написана пользователем сайта и отражает его личную точку зрения. Компания MetaQuotes Ltd не несет ответственности за достоверность представленной информации, а также за возможные последствия использования описанных решений, стратегий или рекомендаций.

- Бесплатные приложения для трейдинга

- 8 000+ сигналов для копирования

- Экономические новости для анализа финансовых рынков

Вы принимаете политику сайта и условия использования