Articles on machine learning in trading

Creating AI-based trading robots: native integration with Python, matrices and vectors, math and statistics libraries and much more.

Find out how to use machine learning in trading. Neurons, perceptrons, convolutional and recurrent networks, predictive models — start with the basics and work your way up to developing your own AI. You will learn how to train and apply neural networks for algorithmic trading in financial markets.

Add a new article

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

Analyzing binary code of prices on the exchange (Part I): A new look at technical analysis

This article presents an innovative approach to technical analysis based on converting price movements into binary code. The author demonstrates how various aspects of market behavior — from simple price movements to complex patterns — can be encoded in a sequence of zeros and ones.

Neural networks made easy (Part 63): Unsupervised Pretraining for Decision Transformer (PDT)

We continue to discuss the family of Decision Transformer methods. From previous article, we have already noticed that training the transformer underlying the architecture of these methods is a rather complex task and requires a large labeled dataset for training. In this article we will look at an algorithm for using unlabeled trajectories for preliminary model training.

Population optimization algorithms: Binary Genetic Algorithm (BGA). Part I

In this article, we will explore various methods used in binary genetic and other population algorithms. We will look at the main components of the algorithm, such as selection, crossover and mutation, and their impact on the optimization. In addition, we will study data presentation methods and their impact on optimization results.

Detecting and Classifying Fractal Patterns Using Machine Learning

In this article, we will touch upon the intriguing topic of fractal analysis and market forecasting using machine learning. These are just the first steps towards exploring the diverse fractal structures that form on financial price charts. We will use the correlation to find patterns and the CatBoost algorithm to classify these patterns.

Population optimization algorithms: Artificial Multi-Social Search Objects (MSO)

This is a continuation of the previous article considering the idea of social groups. The article explores the evolution of social groups using movement and memory algorithms. The results will help to understand the evolution of social systems and apply them in optimization and search for solutions.

MQL5 Wizard Techniques you should know (Part 35): Support Vector Regression

Support Vector Regression is an idealistic way of finding a function or ‘hyper-plane’ that best describes the relationship between two sets of data. We attempt to exploit this in time series forecasting within custom classes of the MQL5 wizard.

Eigenvectors and eigenvalues: Exploratory data analysis in MetaTrader 5

In this article we explore different ways in which the eigenvectors and eigenvalues can be applied in exploratory data analysis to reveal unique relationships in data.

Quantization in machine learning (Part 2): Data preprocessing, table selection, training CatBoost models

The article considers the practical application of quantization in the construction of tree models. The methods for selecting quantum tables and data preprocessing are considered. No complex mathematical equations are used.

Market Microstructure in MQL5 (Part 1): Robust Foundation

This article builds the foundation layer of a twelve-part MQL5 market microstructure toolkit. It implements guarded math helpers (SafeDivide, SafeLog, SafeSqrt, SafeExp, SafeTanh), robust data validation (ValidateSymbolV2, SafeCopyClose), trimmed statistical estimators (robust mean var), a linear regression slope, shared structs, and an FFT. You compile a single include file that hardens indicators and expert advisors against silent numerical failures and standardizes data flow for later parts.

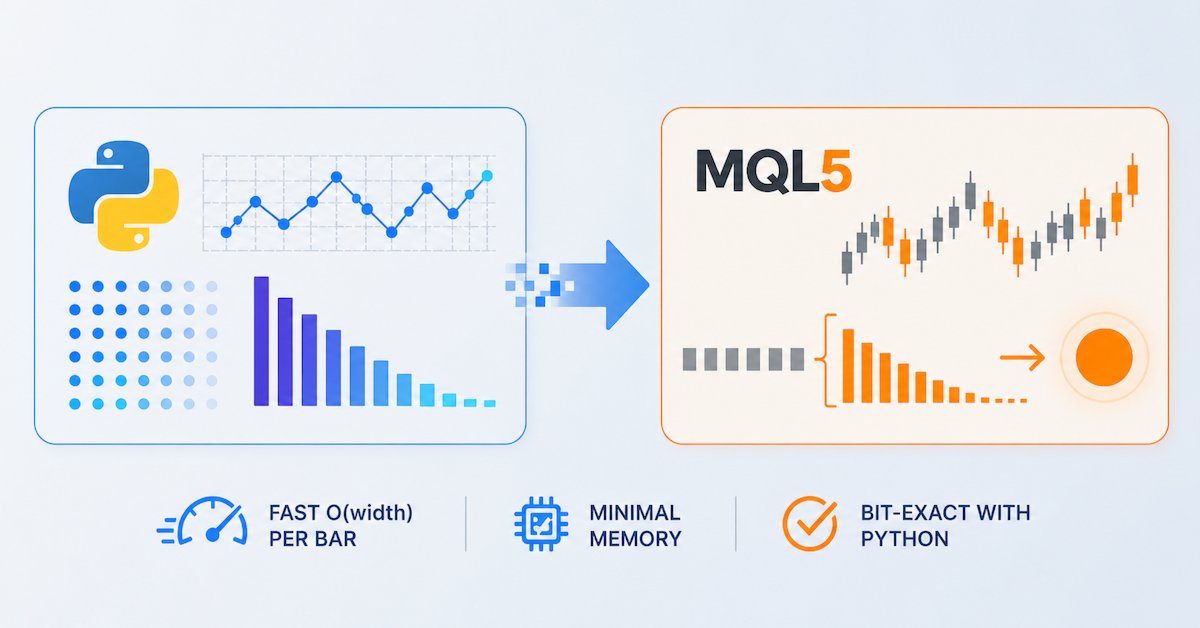

Feature Engineering for ML (Part 2): Implementing Fixed-Width Fractional Differentiation in MQL5

This article delivers a production-grade MQL5 implementation of fixed-width fractional differentiation for live MetaTrader 5 feeds. We introduce a header-only CFFDEngine that precomputes weights without a fixed cap, performs O(width) per-bar updates, and avoids per-tick allocations. The FFD.mq5 indicator supports all ENUM_APPLIED_PRICE types and prev_calculated optimization. Validation scripts confirm numerical equivalence with the standard Python frac diff_ffd pipeline.

Artificial Showering Algorithm (ASHA)

The article presents the Artificial Showering Algorithm (ASHA), a new metaheuristic method developed for solving general optimization problems. Based on simulation of water flow and accumulation processes, this algorithm constructs the concept of an ideal field, in which each unit of resource (water) is called upon to find an optimal solution. We will find out how ASHA adapts flow and accumulation principles to efficiently allocate resources in a search space, and see its implementation and test results.

The Group Method of Data Handling: Implementing the Multilayered Iterative Algorithm in MQL5

In this article we describe the implementation of the Multilayered Iterative Algorithm of the Group Method of Data Handling in MQL5.

Neuro-Structural Trading Engine — NSTE (Part II): Jardine's Gate Six-Gate Quantum Filter

This article introduces Jardine's Gate, a six-gate orthogonal signal filter for MetaTrader 5 that validates LSTM predictions across entropy, expert interference, confidence, regime-adjusted probability, trend direction, and consecutive-loss kill switch dimensions. Out of 43,200 raw signals per month, only 127 pass all six gates. Readers get the complete QuantumEdgeFilter MQL5 class, threshold calibration logic, and gate performance analytics.

Population optimization algorithms: Micro Artificial immune system (Micro-AIS)

The article considers an optimization method based on the principles of the body's immune system - Micro Artificial Immune System (Micro-AIS) - a modification of AIS. Micro-AIS uses a simpler model of the immune system and simple immune information processing operations. The article also discusses the advantages and disadvantages of Micro-AIS compared to conventional AIS.

The Disagreement Problem: Diving Deeper into The Complexity Explainability in AI

In this article, we explore the challenge of understanding how AI works. AI models often make decisions in ways that are hard to explain, leading to what's known as the "disagreement problem". This issue is key to making AI more transparent and trustworthy.

Defining your Edge (Part 1): Using a Discrete Fourier Transform and a Spiking Neural Network in a Trading Robot

In this article we make the case for pairing the Discrete Fourier Transform with a Spiking Neural Network in a Trading Robot. The Fourier Transform helps represent data as oscillations instead of its raw values. To govern how we interpret these cycles, we engage a Spiking Neural Network that unlike regular networks, uses time dependent electrical charges to accumulate potential and only "spike" when a target threshold is met. Combining these two engines allows us better control on the timing of discrete market movements, that in theory should give us entry signals with rigorous mathematical confirmation.

Gaussian Processes in Machine Learning (Part 2): Implementing and Testing a Classification Model in MQL5

In this section, we will look at the implementation of the key interfaces of the library of Gaussian processes in MQL5: IKernel, ILikelihood, and IInference. We will also demonstrate its operation on synthetic data and implement indicators for classification and regression, demonstrating its operation in online mode - with retraining of the model on each new bar.

Analyzing Price Time Gaps in MQL5 (Part II): Creating a Heat Map of Liquidity Distribution Over Time

A detailed guide on how to create a heat map indicator for MetaTrader 5 that visualizes the price distribution over time. The article reveals the mathematical basis of time density analysis, where each price level is colored from red (minimum stay time) to blue (maximum stay time).

Arithmetic Optimization Algorithm (AOA): From AOA to SOA (Simple Optimization Algorithm)

In this article, we present the Arithmetic Optimization Algorithm (AOA) based on simple arithmetic operations: addition, subtraction, multiplication and division. These basic mathematical operations serve as the foundation for finding optimal solutions to various problems.

Feature Engineering for ML (Part 4): Implementing Time Features in MQL5

Applying Python session boundaries to MQL5 broker timestamps misclassifies session membership by two to three hours on any non-UTC broker, corrupting session flags across the full backtest history. We implement CTimeFeatures.mqh, containing CRingBuffer and CTimeFeatures, with three EA-facing methods: Initialize (UTC offset capture and frequency gate configuration), Update (log return push to session-conditional ring buffers), and Calculate (cyclical encoding, session flags, and session volatility). The output is a flat double array drop-compatible with Python's get_time_features for sub-hourly, hourly, and daily timeframes.

Analyzing Price Time Gaps in MQL5 (Part II): Creating a Heat Map of Liquidity Distribution Over Time

A detailed guide on how to create a heat map indicator for MetaTrader 5 that visualizes the price distribution over time. The article reveals the mathematical basis of time density analysis, where each price level is colored from red (minimum stay time) to blue (maximum stay time).

MQL5 Wizard Techniques you should know (Part 18): Neural Architecture Search with Eigen Vectors

Neural Architecture Search, an automated approach at determining the ideal neural network settings can be a plus when facing many options and large test data sets. We examine how when paired Eigen Vectors this process can be made even more efficient.

Neural Networks in Trading: Actor—Director—Critic

We invite you to explore the Actor-Director-Critic framework, which combines hierarchical learning and a multi-component architecture for creating adaptive trading strategies. In this article, we take a detailed look at how using the Director to classify the Actor's actions helps to effectively optimize trading decisions and improve the robustness of models in financial market conditions.

Neural network trading EA based on PatchTST

The article presents the revolutionary architecture of PatchTST, a tailored transformer for financial time series analysis that breaks market data into 16-bar patches for efficient processing. We will discuss the full implementation of a trading robot in MQL5 covering everything from mathematical fundamentals and data structures to a ready-made EA with risk management and continuous learning systems.

Overcoming The Limitation of Machine Learning (Part 8): Nonparametric Strategy Selection

This article shows how to configure a black-box model to automatically uncover strong trading strategies using a data-driven approach. By using Mutual Information to prioritize the most learnable signals, we can build smarter and more adaptive models that outperform conventional methods. Readers will also learn to avoid common pitfalls like overreliance on surface-level metrics, and instead develop strategies rooted in meaningful statistical insight.

MQL5 Wizard Techniques you should know (Part 23): CNNs

Convolutional Neural Networks are another machine learning algorithm that tend to specialize in decomposing multi-dimensioned data sets into key constituent parts. We look at how this is typically achieved and explore a possible application for traders in another MQL5 wizard signal class.

Meta-Labeling the Classics (Part 1): Filtering and Sizing RSI Trades

RSI accumulates losses in trending conditions by firing at every threshold crossing regardless of market regime. A Random Forest secondary classifier trained on 12 contextual features — RSI momentum slope, EMA50 trend velocity, ATR-normalised trend stretch, and nine others — filters raw signals and scales position size by classifier confidence on EURUSD H1. Results compare plain RSI, meta-filtered RSI, and bet-sized RSI across a 16-month out-of-sample period with per-trade metrics and drawdown diagnostics.

MQL5 Wizard Techniques you should know (Part 88): Using Blooms Filter with a Custom Trailing Class

Our next focus in these series on ideas that can be rapidly prototyped with the MQL5 Wizard, is a Custom Trailing class that uses the Blooming Filter. Trailing Stop systems are an optional but very resourceful part to any trading system that we want to explore more in these series besides the traditional Entry Signals.

Neural networks made easy (Part 77): Cross-Covariance Transformer (XCiT)

In our models, we often use various attention algorithms. And, probably, most often we use Transformers. Their main disadvantage is the resource requirement. In this article, we will consider a new algorithm that can help reduce computing costs without losing quality.

Neural networks made easy (Part 70): Closed-Form Policy Improvement Operators (CFPI)

In this article, we will get acquainted with an algorithm that uses closed-form policy improvement operators to optimize Agent actions in offline mode.

MQL5 Wizard Techniques you should know (Part 10). The Unconventional RBM

Restrictive Boltzmann Machines are at the basic level, a two-layer neural network that is proficient at unsupervised classification through dimensionality reduction. We take its basic principles and examine if we were to re-design and train it unorthodoxly, we could get a useful signal filter.

MetaTrader 5 Machine Learning Blueprint (Part 17): CPCV Backtesting — From Python Model to Tick-Level Evidence

We bridge Python-native artifacts to MQL5 for tick-accurate CPCV backtesting. The export script converts the ONNX model, calibrator, feature spec, and path masks to flat files, while the expert advisor rebuilds features, performs ONNX inference with calibration, and trades on real ticks. The Strategy Tester runs each combinatorial path, and Python aggregates per-path equities into a path Sharpe distribution to assess robustness after spread, slippage, and commission.

Neural Networks in Trading: Hyperbolic Latent Diffusion Model (HypDiff)

The article considers methods of encoding initial data in hyperbolic latent space through anisotropic diffusion processes. This helps to more accurately preserve the topological characteristics of the current market situation and improves the quality of its analysis.

Covariance Matrix Adaptation Evolution Strategy (CMA-ES)

The article explores one of the most interesting non-gradient optimization algorithms, which learns to understand the geometry of the objective function. We will focus on the classical implementation of CMA-ES with a slight modification - replacing the normal distribution with the power one. We will thoroughly examine the math behind the algorithm, as well as practical implementation, and check where CMA-ES is unbeatable and where it should be avoided.

Atmosphere Clouds Model Optimization (ACMO): Theory

The article is devoted to the metaheuristic Atmosphere Clouds Model Optimization (ACMO) algorithm, which simulates the behavior of clouds to solve optimization problems. The algorithm uses the principles of cloud generation, movement and propagation, adapting to the "weather conditions" in the solution space. The article reveals how the algorithm's meteorological simulation finds optimal solutions in a complex possibility space and describes in detail the stages of ACMO operation, including "sky" preparation, cloud birth, cloud movement, and rain concentration.

Neural Networks in Trading: LSTM Optimization for Multivariate Time Series Forecasting (Final Part)

We continue to implement the DA-CG-LSTM framework, which offers innovative methods for time series analysis and forecasting. The use of CG-LSTM and dual attention allows for more accurate detection of both long-term and short-term dependencies in data, which is particularly useful for working with financial markets.

Data Science and ML (Part 48): Are Transformers a Big Deal for Trading?

From ChatGPT to Gemini and many model AI tools for text, image, and video generation. Transformers have rocked the AI-world. But, are they applicable in the financial (trading) space? Let's find out.

Neural networks made easy (Part 69): Density-based support constraint for the behavioral policy (SPOT)

In offline learning, we use a fixed dataset, which limits the coverage of environmental diversity. During the learning process, our Agent can generate actions beyond this dataset. If there is no feedback from the environment, how can we be sure that the assessments of such actions are correct? Maintaining the Agent's policy within the training dataset becomes an important aspect to ensure the reliability of training. This is what we will talk about in this article.

Atmosphere Clouds Model Optimization (ACMO): Practice

In this article, we will continue diving into the implementation of the ACMO (Atmospheric Cloud Model Optimization) algorithm. In particular, we will discuss two key aspects: the movement of clouds into low-pressure regions and the rain simulation, including the initialization of droplets and their distribution among clouds. We will also look at other methods that play an important role in managing the state of clouds and ensuring their interaction with the environment.

Population optimization algorithms: Bacterial Foraging Optimization - Genetic Algorithm (BFO-GA)

The article presents a new approach to solving optimization problems by combining ideas from bacterial foraging optimization (BFO) algorithms and techniques used in the genetic algorithm (GA) into a hybrid BFO-GA algorithm. It uses bacterial swarming to globally search for an optimal solution and genetic operators to refine local optima. Unlike the original BFO, bacteria can now mutate and inherit genes.