The 3 Numbers Every Gold Trader Should Know Before Opening a Position

Back in late 2022 I had an EA running on XAUUSD through a US CPI release. I was on a VPS in Singapore at the time - latency was already sketchy on normal days. Backtest was clean, equity curve straight enough that I genuinely thought I'd worked something out. Live, it burned in under an hour. Spread hit 38 points at entry. SL was sized for normal conditions, not news. The risk ratio I thought I had was a tester fiction.

Three numbers wrong. Account dropped hard. Not catastrophic, but the kind of hit that makes you sit there staring at the terminal for a while.

I'm not writing this as someone who fixed everything after that. I still take losses. But those three numbers - spread, ATR, risk ratio - are the ones that keep showing up. Not in backtests. In the trades that actually cost something.

🚀 Number 1: Spread

Everyone knows gold has a spread. Most people don't look at it before they click.

The spec sheet number - say 2.0 points - is not the number that matters. What matters is the spread at the exact moment your entry fires. During late New York into early Asia, it's already 8 - 15 points on most ECN accounts with no news at all. During CPI, NFP, Fed decisions - I've watched it go past 60, 70 points. Not occasionally. Regularly.

If your SL is 120 points and spread is 40 at entry, a third of your stop is already gone before price moves a tick. Your risk calculator says one thing. The broker took a different amount off the top.

Most traders know this. They know it the same way they know they shouldn't overtrade after a loss. When price is moving and the setup looks right, spread isn't in the room anymore.

I built Gold Spread Monitor MT5 because I never reliably checked spread manually under pressure. Not once, not consistently. The tool puts the number on the chart with a threshold alert. That's the only version of "I'll check spread first" that has ever actually worked for me.

And yes, I still occasionally ignore the alert when gold starts ripping and the setup looks perfect. Usually regret it.

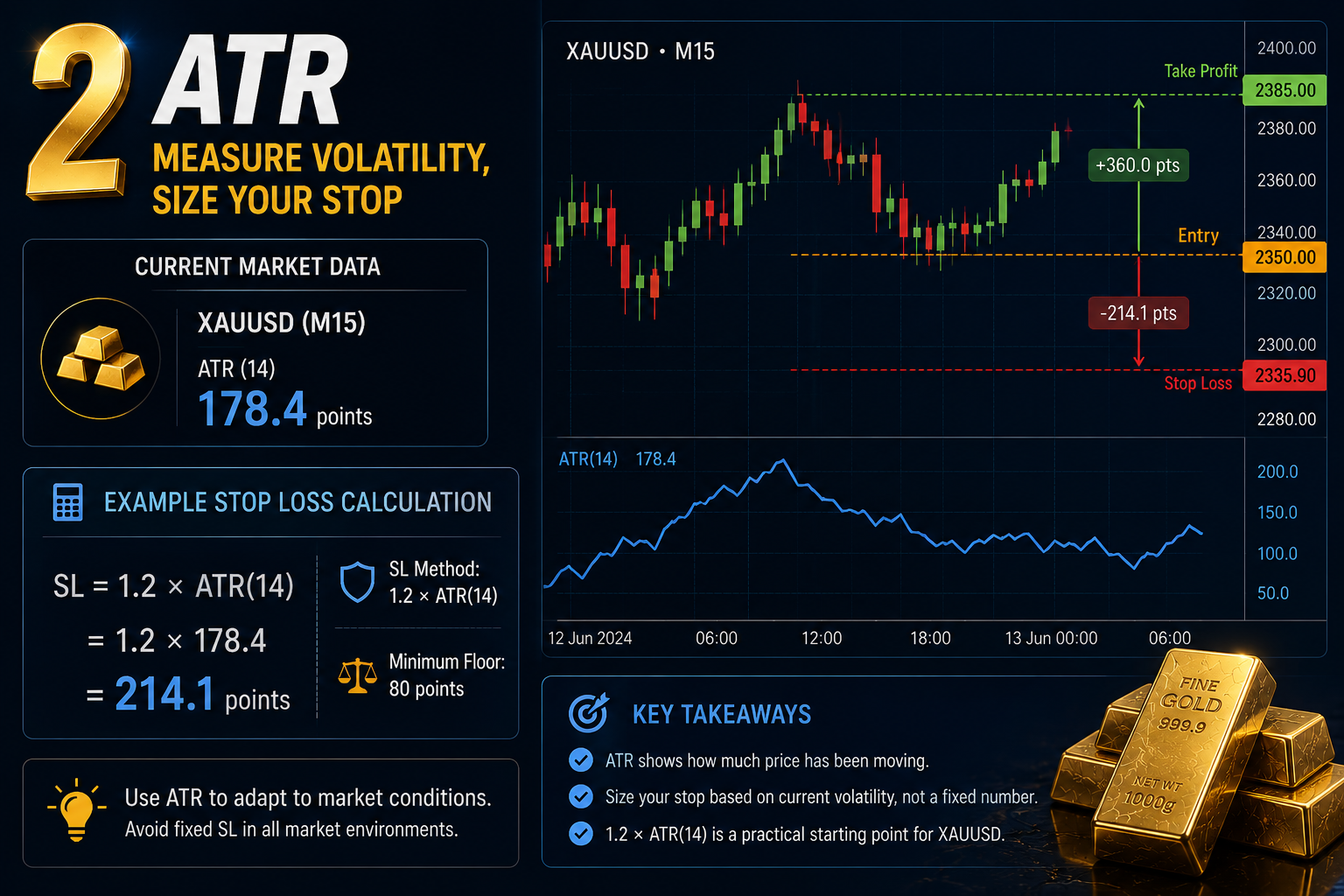

🚀 Number 2: ATR

ATR is not a signal. I've seen people trade it like one. It doesn't work that way.

Average True Range tells you how much price has been moving. That's it. A 14-period ATR of 180 points on XAUUSD M15 is historical. It says nothing about what happens next. What it does tell you: how wide your stop needs to be to survive normal noise.

Fixed SL is the error I see most often. Same 200 points regardless of conditions. During a slow consolidation week, ATR on gold M15 can sit at 80 - 90 points. A 200-point stop in that environment still gets hit - price just grinds back and forth through a 150-point range until your level gets tagged, then reverses. Then during a volatile week, ATR pushes to 250 and that same 200-point stop is too tight. Taken out on a wick, move happens 15 minutes later.

Fixed stop, variable instrument. Doesn't hold up.

My current live EA setup: SL at 1.2× ATR(14) on the entry timeframe, minimum 80-point floor so I'm not putting in a 40-point stop at 3am. The 1.2 isn't from any formula. It's trauma insurance - too many times watching XAUUSD wick me out by 3 points then run 400 points in the direction I called. You might land on a different multiplier. The point is it should move with the market, not sit fixed while the market does whatever it wants.

Gold ATR Risk Calculator MT5 runs the lot size calculation from that automatically. Risk percentage in, ATR-adjusted lot size out. Removes the mental arithmetic when you're watching a fast move and your brain is already on the entry.

🚀 Number 3: Risk Ratio - The Real One

The ratio most traders quote: TP distance divided by SL distance. 2R, 3R. That's the chart number.

The number that actually hits your account: TP minus spread, minus entry slippage, minus exit slippage, minus swap if you're holding overnight.

A trade you're calling 2R - say 60-point SL, 120-point TP - with 12-point spread and 4 points of average round-trip slippage. That's 1.7R delivered. Not 2R.

Sounds small. On a system running 48% win rate targeting 2R, the difference between 2R and 1.7R delivered isn't small across 500 trades. That gap is the margin between a system that compounds and a system that slowly bleeds while you keep tweaking parameters trying to figure out what's wrong.

Partial fills add to this. On bigger lot sizes, some brokers fill your order across several ticks. You don't always get the price you see. Exit slippage is usually worse than entry slippage - market orders to close during fast moves get filled wherever liquidity sits, not where you clicked. Tester never shows you any of this. Live, it's normal.

Risk to Reward Planner shows the adjusted ratio on the chart - spread factored in, real number visible before you enter. Not complicated. But there's a difference between knowing the right number and seeing it clearly before you click.

🌟 They Only Work Together

A 2R setup with a 35-point spread and 80-point TP is not a 2R setup. An ATR-sized SL you set during a quiet period and didn't update before news isn't ATR-sized anymore. Checking spread but not ATR still leaves you over-sized into the wrong volatility regime.

All three or it's incomplete.

My pre-entry check for manual gold trades:

- Spread above session threshold → trade waits. No exceptions, or the exception becomes the habit.

- ATR-based SL → does it land near an actual structure level? If the math says 180-point SL and there's clean support 60 points away, that's a conflict. Resolve it before entering.

- Real risk ratio after friction → is there enough room for a valid TP before the next obvious block? If not, the trade doesn't meet criteria.

One fails, no trade. I miss setups. Some of them were probably good. I've also dodged setups that looked good and weren't.

🌟 The Tester Problem

The tester gives you clean numbers. The market doesn't.

MT5 Strategy Tester uses modeled spreads that understate news spikes. Fill logic is optimistic. Slippage is whatever you configured, not what your broker delivers. VPS latency is zero. Partial fills don't exist. Broker freezes during high volatility - the moment you actually need to close - don't exist either. If you're on a B-book broker, the execution model in live is entirely different from what the tester simulates anyway.

Your backtest looks clean because the environment is clean. That's not what you're trading in.

I ran an EA live for six months before finding out the spread assumption in my tester was off by a factor of three. Six months of live capital, slow bleed, endless parameter tweaks - all of it tracing back to one wrong input at the start.

Run demo with real spreads logged, real session timing, minimum a month. Then live at reduced size. I know everyone knows this. Most people still skip it when the backtest looks good.

🔥 Closing

I've built a lot of MT5 tools. The ones that actually get used - by me, by traders using my products - are the ones that do one thing clearly.

Spread visible on the chart. ATR-based lot size handled automatically. Real risk ratio before entry.

That's the floor. You can build whatever system you want on top of it. But if those three numbers are wrong going in, the more sophisticated the system, the faster it loses money.

The three tools I mentioned - the spread monitor, the ATR calculator, the risk planner - are on MQL5 Market. They're utilities. They do one thing each. Whether that's worth anything depends on whether you actually use them before clicking.

🎁 New to Gold Algo Lab?

Start with the Gold Algo Lab Tool Map - a practical guide that organizes our MT5 tools into 6 connected stages: market context, setup selection, risk planning, trade execution, position management and account protection.

→ Gold Algo Lab Tool Map: Where to Actually Start With MT5 Tools for XAUUSD

https://www.mql5.com/en/blogs/post/771930

Do not choose a tool by its name alone. Start with the part of your trading process that needs the most control, then build your workflow one layer at a time.

Gold Algo Lab builds practical, risk-first MT5 tools for serious XAUUSD traders - shaped by 8 years of building and trading real systems, with no hype, no profit guarantees, and no unrealistic promises.

Trading Guide")

")