Developing a multi-currency Expert Advisor (Part 17): Further preparation for real trading

Introduction

In one of the previous articles, we already turned our attention to the EA improvements necessary for working on real accounts. Until now, our efforts have been focused mainly on getting acceptable EA results in the strategy tester. Real trading requires much more preparations.

In addition to restoring the EA operation after restarting the terminal, the ability to use slightly different names of trading instruments and auto completion of trading when the specified indicators are reached, we also face the following issue: in order to form the initialization string, we use information obtained directly from the database, which stores all the results of optimizations of trading strategy instances and their groups.

To run the EA, we must have a file with the database in the shared terminal folder. The size of the database is already several gigabytes, and it will only grow in the future. So making the database an integral part of the EA is not rational - only a very small part of the information stored there is needed for launch. Therefore, it is necessary to implement a mechanism for extracting and using this information in the EA.

Mapping out the path

Let us recall that we have considered and implemented automation of two stages of testing. At the first stage, the parameters of a single instance of the trading strategy are optimized (part 11). The model trading strategy under study uses only one trading instrument (symbol) and one timeframe. Therefore, we consistently ran it through the optimizer, changing symbols and timeframes. For each combination of symbol and timeframe, optimization was carried out in turn according to different optimization criteria. All results of optimization passes were set in the 'passes' table of our database.

At the second stage, we optimized the selection of a group of parameter sets obtained in the first stage that yielded the best results when used together (part 6 and part 13). As in the first stage, we included sets of parameters using the same symbol-timeframe pair into one group. Information about the results of all groups reviewed during optimization was also saved in our database.

At the third stage, we no longer used the standard strategy tester optimizer, so we are not talking about its automation yet. The third stage consisted of selecting one of the best groups found in the second stage for each available combination of symbol and timeframe. We used optimization on three symbols (EURGBP, EURUSD, GBPUSD) and three timeframes (H1, M30, M15). Thus, the result of the third stage will be nine selected groups. But to simplify and accelerate calculations in the tester, we limited ourselves in the last articles to only the three best groups (with three different symbols and the H1 timeframe).

The result of the third stage was a set of row identifiers from the 'passes' table, which we passed through the input parameter to our final SimpleVolumesExpert.mq5 EA:

input string passes_ = "734469," "736121," "776928"; // - Comma-separated pass IDs

We could change this parameter before launching the EA test. Thus, it was possible to run the final EA with any desired subset of groups from the set of groups available in the database in the 'passes' table, or, to be more precise, with a subset, which does not exceed 247 characters in length. This is a limitation imposed by the MQL5 language on the values of input string parameters. According to the documentation, the maximum length of a string parameter value can be from 191 to 253 characters, depending on the length of the parameter name.

Therefore, if we want to include more than, roughly speaking, 40 groups into the work, then it will not be possible to do it this way. For example, we might have to make the passes_ variable a simple stirng variable rather than an input string parameter by removing the word input from the code. In this case, we can specify the required set of groups only in the source code. However, we do not need to use such large sets yet. Moreover, according to the experiments conducted in part 5, it is more profitable for us not to make one group from a large number of single copies of trading strategies or groups of trading strategies. It is more profitable to split the initial number of single copies of trading strategies into several subgroups, from which a smaller number of new groups can be assembled. These new groups can either be combined into one final group, or the grouping process can be repeated by division into new subgroups. Thus, at each level of unification, we will have to take a relatively small number of strategies or groups as a single group.

When the EA has access to the database with the results of all optimization passes, it is sufficient to pass a list of IDs of the required optimization passes via the input. The EA receives the initialization strings of those groups of trading strategies, that participated in the listed passes, from the database on its own. Based on the initialization strings received from the database, it will construct an initialization string for an EA object that includes all trading strategies from the listed groups. This EA will trade using all the trading strategy instances included in it.

If there is no access to the database, the EA still needs to somehow generate an initialization string for the EA object, containing the required composition of single instances of trading strategies or groups of trading strategies. For example, we can save it to a file and pass the name of the file to the EA it will load the initialization string from. Or we can insert the contents of the initialization string into the source code of the EA via an additional mqh library file. We can even combine the two methods by saving the initialization string to a file, then importing it using the file import facilities in MetaEditor (Edit → Insert → File).

However, if we want to provide the ability to work with different selected groups in one EA, choosing the desired one in the inputs, then this approach will quickly show its weak scalability. We will need to do a lot of manual, repetitive work. Therefore, let's try to formulate the problem a little differently: we want to form a library of good initialization strings, from which we can choose one for the current EA launch. The library should be an integral part of the EA, so that we do not have to use another separate file along with it.

Taking into account the above, the upcoming work can be divided into the following stages:

- Selection and saving. At this stage, we should have a tool that allows us to select groups and save their initialization strings for later use. It would probably be a good idea to provide the ability to save some additional information about the selected groups (name, brief description, approximate composition, creation date, etc.)

- Forming the library. From the groups selected in the previous stage, a final selection is made of those that will be used in the library for a specific release of the EA, and an include file with all the necessary information is formed.

- Creating the final EA. By modifying the EA from the previous part, we will turn it into a new final EA using the created group library. This EA will no longer need access to our optimization database, as all the necessary information about the trading strategy groups used will be included in it.

Let's start implementing our plans.

Revisiting previous accomplishments

The steps mentioned are a prototype of the implementation of Stage 8 described in Part 9. Let us recall that in that article we listed a set of stages, the completion of which can allow us to get a ready-made EA with good trading performance. Stage 8 implied that we collect all the best groups of groups found for different trading strategies, symbols, timeframes and other parameters into one final EA. However, we have not yet considered in detail the question "How exactly should the best groups be selected?"

On the one hand, the answer to the question may turn out to be pretty simple. For example, we might simply select the best results from all the groups according to some parameter (total profit, Sharpe ratio, normalized average annual profit). But on the other hand, the answer may turn out to be much more complicated. For example, what if better test results are achieved if a complex criterion is used to select the best groups? Or what if some of the best groups should not be included in the final EA at all, since their inclusion will worsen the results achieved without them? This topic will most likely require its own detailed study.

Another issue that will also require separate study is the optimal division of groups into subgroups with normalization of subgroups. I have already touched upon this issue in part 5 even before we started implementing any automation of test stages. We then manually selected nine single instances of trading strategies, three instances for each of the three trading instruments (symbols) used.

It turned out that if you first make three normalized groups of three strategies for each symbol, and then combine them into one final normalized group, then the results in the tests will be somewhat better compared to combining nine single copies of trading strategies into a final normalized group. But we cannot say for sure whether this method of grouping will be optimal. And would it be more preferable for other trading strategies than simply combining them into one group? In general, there is room for further research here too.

Fortunately, we can postpone these two questions until later. To explore them, we would need auxiliary tools that have not yet been implemented. Without them, the work will be much less efficient and will take much more time.

Selecting and saving groups

It might seem we already have everything we need. Simply take the SimpleVolumesExpert.mq5 EA from the previous part, set comma-separated IDs of passes in the passes_ input, launch a single tester pass and get the required initialization string saved to the database. Seemingly, the only thing missing is some additional data. But it turned out that information about the pass does not enter the database.

The point is that we have only the results of optimization passes uploaded to the database. Single pass results are not uploaded. As you might remember, uploading is performed inside the CTesterHandler::ProcessFrames() method called from the OnTesterPass() handler in the upper level:

//+------------------------------------------------------------------+ //| Handling incoming frames | //+------------------------------------------------------------------+ void CTesterHandler::ProcessFrames(void) { // Open the database DB::Connect(); // Variables for reading data from frames ... // Go through frames and read data from them while(FrameNext(pass, name, id, value, data)) { // Convert the array of characters read from the frame into a string values = CharArrayToString(data); // Form a string with names and values of the pass parameters inputs = GetFrameInputs(pass); // Form an SQL query from the received data query = StringFormat("INSERT INTO passes " "VALUES (NULL, %d, %d, %s,\n'%s',\n'%s');", s_idTask, pass, values, inputs, TimeToString(TimeLocal(), TIME_DATE | TIME_SECONDS)); // Add it to the SQL query array APPEND(queries, query); } // Execute all requests DB::ExecuteTransaction(queries); // Close the database DB::Close(); }

When a single pass is launched, the handler is not called, as this is not provided for by the single pass event model. This handler is called only in an Expert Advisor running in data frame collection mode. Launching an EA instance of the EA in this mode occurs automatically when optimization starts, but does not occur when a single pass starts. Therefore, it turns out that the existing implementation does not save information about single passes to the database.

We can, of course, leave everything as is and develop an EA that will need to be launched for optimization according to some unnecessary parameter. The goal of such optimization will be to obtain the results of the first pass, after which the optimization will stop. This way, the results of the pass will be entered into the database. But this seems too ugly, so we will go another way.

When running a single pass in the EA, the OnTester() handler will be called upon completion. Therefore, we will have to insert the code for saving the results of a single pass either directly into the handler or into one of the methods called from the handler. Probably, the most appropriate place to insert the method is CTesterHandler::Tester(). However, it is worth considering that this method will also be called when the EA completes the optimization pass. This method now contains code that generates and sends the results of the optimization pass through the data frame mechanism.

When a single pass is started, the data for the frame is still generated, but the data frame itself, even if created, cannot be used. If we try to use the FrameNext() function for getting a frame, after creating the frame by the FrameAdd() function in the EA launched in single pass mode, FrameNext() will not read the created frame. It will behave as if no frames were created.

Therefoe, let's do the following. In the CTesterHandler::Tester() handler, we will check whether this pass is a single one or performed as part of optimization. Depending on the result, we will either immediately save the pass results to the database (for a single pass), or create a data frame to send to the main EA (for optimization). Let's add a new method called to save a single pass and another auxiliary method that generates an SQL query to insert the required data into the passes table. We will need the latter because now such an action will be performed in two places of the code, and not in one. Therefore, we will move it to a separate method.

//+------------------------------------------------------------------+ //| Optimization event handling class | //+------------------------------------------------------------------+ class CTesterHandler { ... static void ProcessFrame(string values); // Handle single pass data // Generate SQL query to insert pass results static string GetInsertQuery(string values, string inputs, ulong pass = 0); public: ... };

We already have the GetInsertQuery() implementation. All we have to do is move the code block from the ProcessFrames() method and call it at the right place in the ProcessFrames() method:

//+------------------------------------------------------------------+ //| Generate SQL query to insert pass results | //+------------------------------------------------------------------+ string CTesterHandler::GetInsertQuery(string values, string inputs, ulong pass) { return StringFormat("INSERT INTO passes " "VALUES (NULL, %d, %d, %s,\n'%s',\n'%s');", s_idTask, pass, values, inputs, TimeToString(TimeLocal(), TIME_DATE | TIME_SECONDS)); } //+------------------------------------------------------------------+ //| Handling incoming frames | //+------------------------------------------------------------------+ void CTesterHandler::ProcessFrames(void) { ... // Go through frames and read data from them while(FrameNext(pass, name, id, value, data)) { // Convert the array of characters read from the frame into a string values = CharArrayToString(data); // Form a string with names and values of the pass parameters inputs = GetFrameInputs(pass); // Form an SQL query from the received data query = GetInsertQuery(values, inputs, pass); // Add it to the SQL query array APPEND(queries, query); } ... }

To save the data of a single pass we will call a new method ProcessFrame() accepting a string, that is part of an SQL query and contains data about the pass for insertion into the passes table, as a parameter. Within the method itself, we simply connect to the database, form the final SQL query and execute it:

//+------------------------------------------------------------------+ //| Handle single pass data | //+------------------------------------------------------------------+ void CTesterHandler::ProcessFrame(string values) { // Open the database DB::Connect(); // Form an SQL query from the received data string query = GetInsertQuery(values, "", 0); // Execute the request DB::Execute(query); // Close the database DB::Close(); }

Taking into account the added methods, the pass completion event handler can be modified as follows:

//+------------------------------------------------------------------+ //| Handling completion of tester pass for agent | //+------------------------------------------------------------------+ void CTesterHandler::Tester(double custom, // Custom criteria string params // Description of EA parameters in the current pass ) { ... // Generate a string with pass data data = StringFormat("%s,'%s'", data, params); // If this is a pass within the optimization, if(MQLInfoInteger(MQL_OPTIMIZATION)) { // Open a file to write a frame data int f = FileOpen(s_fileName, FILE_WRITE | FILE_TXT | FILE_ANSI); // Write a description of the EA parameters FileWriteString(f, data); // Close the file FileClose(f); // Create a frame with data from the recorded file and send it to the main terminal if(!FrameAdd("", 0, 0, s_fileName)) { PrintFormat(__FUNCTION__" | ERROR: Frame add error: %d", GetLastError()); } } else { // Otherwise, it is a single pass, call the method to add its results to the database CTesterHandler::ProcessFrame(data); } }

Save the changes made to the TesterHandler.mqh file in the current folder.

Now, after each single pass, information about its results is entered into our database. We are not too interested in various statistical parameters of the pass in terms of the current task. The most important thing for us is the saved initialization string of the normalized strategy group used in the pass. The saved string is what we need the most here.

But the presence of the required initialization strings in one of the passes table columns is not sufficient for their further comfortable use. We also wanted to attach some information to the initialization string. However, it is not worth expanding the set of the passes table columns, since the vast majority of rows in this table will store information about the results of optimization passes, for which additional information is not needed.

Therefore, let's make a new table that will be used to store the selected results. This can already be attributed to the library formation stage.

Forming the library

Let's not overload the new table with redundant fields containing information that can be obtained from other database tables. For example, if an entry in the new table has a relationship with an entry in the passes table (passes) via an external key, then there is already a creation date. Also, using the pass ID, we can build a chain of connections and determine which project this pass belongs to, and therefore the group of strategies used in the pass.

Considering this, let's create the strategy_groups table with the following set of fields:

- id_pass. Pass ID from the passes table (external key)

- name. The name of the strategy group that will be used to generate enumerations for the strategy group selection input.

The SQL code to create the required table could be as follows:

-- Table: strategy_groups DROP TABLE IF EXISTS strategy_groups; CREATE TABLE strategy_groups ( id_pass INTEGER REFERENCES passes (id_pass) ON DELETE CASCADE ON UPDATE CASCADE PRIMARY KEY, name TEXT );

Let's create the CGroupsLibrary auxiliary class to perform most of the further actions. Its tasks include inserting and retrieving information about strategy groups from the database and forming an mqh file with the actual library of good groups that will be used by the final EA. We will get back to it a bit later. For now, let's make an EA that we will use to form the library.

The existing SimpleVolumesExpert.mq5 EA does almost everything it needs to but it still needs some improvement. We planned to use it as the final version of the final EA. So let's save it under a new name SimpleVolumesStage3.mq5. Now we should make the necessary additions to the new file. We are missing two things: the ability to specify the name of the group formed for the currently selected passes (in the passes_ parameter) and saving the initialization string of this group to the new strategy_groups table.

The former is quite simple to implement. Let's add a new EA input to be used as the group name later. If the parameter is empty, no saving to the library occurs.

input group "::: Saving to library" input string groupName_ = ""; // - Group name (if empty - no saving)

But in case of the former one, we will have to work a little harder. To insert data into the strategy_groups table, we need to know the ID assigned to the current pass record when inserted into the passes table. Since its value is automatically allocated by the database itself (in the query we simply pass NULL instead of its value), it does not exist in the code as the value of any variable. Therefore, we cannot currently use it in another place where it is needed. We need to somehow define this value.

This can be done in different ways. For example, knowing that the identifiers assigned to new rows form an increasing sequence, you can simply select the value of the currently largest ID after insertion. This can be done if we know for sure that no new strings are currently passed to the passes table. But if another first or second stage optimization is currently underway in parallel, its results may end up in the same database. In this case, we can no longer be sure that the last ID is the one that corresponds to the pass we launched to form the library. In general, this can be done only if we are ready to put up with some limitations and remember them.

A much more reliable method, free from the possible errors described above, is the following one. We can slightly modify the SQL query for inserting data, turning it into a query that will return the generated ID of the new table row as its result. To do this, simply add the "RETURNING rowid" operator to the end of the SQL query. Let's do this in the GetInsertQuery() method, which generates an SQL query to insert a new row into the passes table. Even though the ID column in the passes table is named id_pass, we can name it rowid, since it has the appropriate type (INTEGER PRIMARY KEY AUTOINCREMENT) and replaces the hidden rowid column automatically present in SQLite tables .

//+------------------------------------------------------------------+ //| Generate SQL query to insert pass results | //+------------------------------------------------------------------+ string CTesterHandler::GetInsertQuery(string values, string inputs, ulong pass) { return StringFormat("INSERT INTO passes " "VALUES (NULL, %d, %d, %s,\n'%s',\n'%s') RETURNING rowid;", s_idTask, pass, values, inputs, TimeToString(TimeLocal(), TIME_DATE | TIME_SECONDS)); }

We will also need to modify the MQL5 code that sends this request. Currently, we use the DB::Execute(query) method for that. It implies that the query passed to it is not a query that returns any data.

Therefore, the CDatabase class receives the new method Insert(), which will execute the passed insert query and return a single read result value. Inside, instead of the DatabaseExecute() function, we will use the DatabasePrepare() function, which then allows us to access the query results:

//+------------------------------------------------------------------+ //| Class for handling the database | //+------------------------------------------------------------------+ class CDatabase { ... public: ... // Execute a query to the database for insertion with return of the new entry ID static ulong Insert(string query); }; ... //+------------------------------------------------------------------+ //| Execute a query to the database for insertion returning the | //| new entry ID | //+------------------------------------------------------------------+ ulong CDatabase::Insert(string query) { ulong res = 0; // Execute the request int request = DatabasePrepare(s_db, query); // If there is no error if(request != INVALID_HANDLE) { // Data structure for reading a single string of a query result struct Row { int rowid; } row; // Read data from the first result string if(DatabaseReadBind(request, row)) { res = row.rowid; } else { // Report an error if necessary PrintFormat(__FUNCTION__" | ERROR: Reading row for request \n%s\nfailed with code %d", query, GetLastError()); } } else { // Report an error if necessary PrintFormat(__FUNCTION__" | ERROR: Request \n%s\nfailed with code %d", query, GetLastError()); } return res; } //+------------------------------------------------------------------+

I decided to not complicate this method with additional checks that the submitted query is indeed an INSERT query, that it contains a command to return an ID, and that the returned value is not composite. Deviation from these conditions will lead to errors when executing this code, but since this method will be used in only one place in the project, we will try to be able to pass a correct request to it.

Save the changes in the Database.mqh file of the current folder.

The next issue that arose during implementation was how to pass the ID value to the higher level of code, since processing it at the point of receipt led to the need to endow existing methods with external functionality and additional passed parameters. Therefore, we decided to do the following way: the CTesterHandler class received the s_idPass static property. The ID of the current pass was written into it. From here, we can get the value at any point in the program:

//+------------------------------------------------------------------+ //| Optimization event handling class | //+------------------------------------------------------------------+ class CTesterHandler { ... public: ... static ulong s_idPass; }; ... ulong CTesterHandler::s_idPass = 0; ... //+------------------------------------------------------------------+ //| Handle single pass data | //+------------------------------------------------------------------+ void CTesterHandler::ProcessFrame(string values) { // Open the database DB::Connect(); // Form an SQL query from the received data string query = GetInsertQuery(values, "", 0); // Execute the request s_idPass = DB::Insert(query); // Close the database DB::Close(); }

Save the changes made to the TesterHandler.mqh file in the current folder.

Now it is time to return to the declared CGroupsLibrary auxiliary class. We ended up with the need to declare two public methods in it - one private method and one static array:

//+------------------------------------------------------------------+ //| Class for working with a library of selected strategy groups | //+------------------------------------------------------------------+ class CGroupsLibrary { private: // Exporting group names and initialization strings extracted from the database as MQL5 code static void ExportParams(string &p_names[], string &p_params[]); public: // Add the pass name and ID to the database static void Add(ulong p_idPass, string p_name); // Export passes to mqh file static void Export(string p_idPasses); // Array to fill with initialization strings from mqh file static string s_params[]; };

In the library-forming EA, only the Add() method will be used. It will receive the pass ID and group name to save to be saved to the library. The method code itself is very simple: form an SQL query for inserting a new entry to the strategy_groups table out of the input data and execute it.

//+------------------------------------------------------------------+ //| Add the pass name and ID to the database | //+------------------------------------------------------------------+ void CGroupsLibrary::Add(ulong p_idPass, string p_name) { string query = StringFormat("INSERT INTO strategy_groups VALUES(%d, '%s')", p_idPass, p_name); // Open the database if(DB::Connect()) { // Execute the request DB::Execute(query); // Close the database DB::Close(); } }

Now, to complete the development of the library formation tool, we only need to add calling the Add() method to the SimpleVolumesStage3.mq5 EA after the tester pass is complete:

//+------------------------------------------------------------------+ //| Test results | //+------------------------------------------------------------------+ double OnTester(void) { // Handle the completion of the pass in the EA object double res = expert.Tester(); // If the group name is not empty, save the pass to the library if(groupName_ != "") { CGroupsLibrary::Add(CTesterHandler::s_idPass, groupName_); } return res; }

Let's save the changes made to the SimpleVolumesStage3.mq5 and GroupsLibrary.mqh files in the current folder. If we add stubs for the rest of the CGroupsLibrary class methods, then we can already use the compiled SimpleVolumesStage3.mq5 EA.

Filling in the library

Let's try to form a library from the nine good pass IDs selected earlier. To do this, launch the SimpleVolumesStage3.ex5 EA in the tester specifying various combinations selected from nine IDs in the passes_ input. In the groupName_ input, we will set a clear name that reflects the composition of the current group of single instances of trading strategies combined into one group.

After several runs, let's look at the results that appear in the strategy_groups table adding some parameters for the passes made with different groups for informational purposes. For example, the following SQL query will help us with this:

SELECT sg.id_pass, sg.name, p.custom_ontester, p.sharpe_ratio, p.profit, p.profit_factor, p.equity_dd_relative FROM strategy_groups sg JOIN passes p ON sg.id_pass = p.id_pass;

The query resulted in the following table:

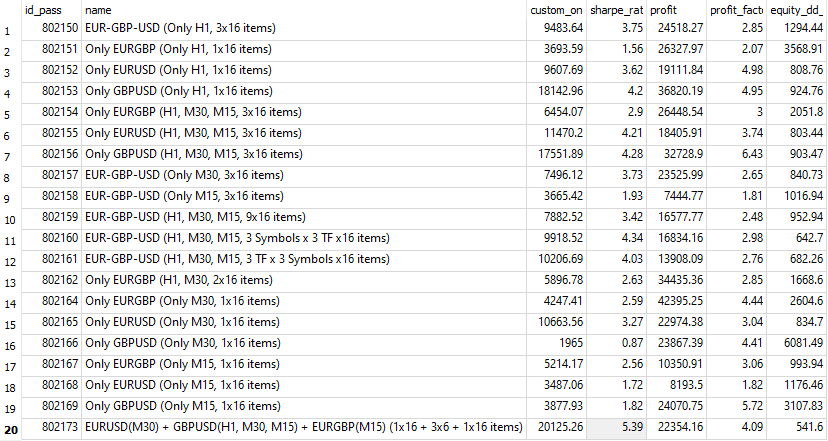

Fig. 1. Group library composition

In the name column, we see the names of the groups, which reflect the trading instruments (symbols), timeframes and the number of instances of trading strategies used in this group. For example, the presence of "EUR-GBP-USD" means that this group includes instances of trading strategies that work on three symbols: EURGBP, EURUSD and GBPUSD. If the group name starts with "Only EURGBP", then it includes instances of strategies only for the EURGBP symbol. The timeframes used are denoted in a similar way. The number of instances of trading strategies is specified at the end of the name. For example, "3x16 items" indicates that this group combines three standardized groups of 16 strategies each.

The custom_ontester column displays the normalized average annual profit for each group. It should be noted that the range of values for this parameter exceeded the expected value, so in the future it would be necessary to understand the reasons for this phenomenon. For example, the results of groups where only GBPUSD was used were significantly higher than those of groups with several symbols. The best result was saved last in line 20. In this group, we have included subgroups that yield the best results for each symbol and one or more timeframes.

Exporting the library

The next step is to transfer the group library from the database to an mqh file that can be connected to the final EA. To do this, let's implement the methods in the CGroupsLibrary class responsible for export, and one more auxiliary EA, which will be used to run these methods.

In the Export() method, we will get from the database and add to the corresponding arrays the names of library groups and their initialization strings. The generated arrays will be passed to the next method ExportParams():

//+------------------------------------------------------------------+ //| Exporting passes to mqh file | //+------------------------------------------------------------------+ void CGroupsLibrary::Export(string p_idPasses) { // Array of group names string names[]; // Array of group initialization strings string params[]; // If the connection to the main database is established, if(DB::Connect()) { // Form a request to receive passes with the specified IDs string query = "SELECT sg.id_pass," " sg.name," " p.params" " FROM strategy_groups sg" " JOIN" " passes p ON sg.id_pass = p.id_pass"; query = StringFormat("%s " "WHERE p.id_pass IN (%s);", query, p_idPasses); // Prepare and execute the request int request = DatabasePrepare(DB::Id(), query); // If the request is successful if(request != INVALID_HANDLE) { // Structure for reading results struct Row { ulong idPass; string name; string params; } row; // For all query results, add the name and initialization string to the arrays while(DatabaseReadBind(request, row)) { APPEND(names, row.name); APPEND(params, row.params); } } DB::Close(); // Export to mqh file ExportParams(names, params); } }

In the ExportParams() method, form a string with MQL5 code, which will create an enumeration (enum) with a given name ENUM_GROUPS_LIBRARY and fill it with elements. Each element will have a comment containing the group name. Next, the code will declare a static string array CGroupsLibrary::s_params[], which will be filled with initialization strings for groups from the library. Each initialization string will be preprocessed: all line feeds will be replaced with spaces, and a backslash will be added before double quotes. This is necessary in order to place the initialization string inside double quotes in the generated code.

Once the code is fully formed in the data variable, we create the file named ExportedGroupsLibrary.mqh and save the received code in it.

//+------------------------------------------------------------------+ //| Export group names extracted from the database and | //| initialization strings in the form of MQL5 code | //+------------------------------------------------------------------+ void CGroupsLibrary::ExportParams(string &p_names[], string &p_params[]) { // ENUM_GROUPS_LIBRARY enumeration header string data = "enum ENUM_GROUPS_LIBRARY {\n"; // Fill the enumeration with group names FOREACH(p_names, { data += StringFormat(" GL_PARAMS_%d, // %s\n", i, p_names[i]); }); // Close the enumeration data += "};\n\n"; // Group initialization string array header and its opening bracket data += "string CGroupsLibrary::s_params[] = {"; // Fill the array by replacing invalid characters in the initialization strings string param; FOREACH(p_names, { param = p_params[i]; StringReplace(param, "\r", ""); StringReplace(param, "\n", " "); StringReplace(param, "\"", "\\\""); data += StringFormat("\"%s\",\n", param); }); // Close the array data += "};\n"; // Open the file to write data int f = FileOpen("ExportedGroupsLibrary.mqh", FILE_WRITE | FILE_TXT | FILE_ANSI); // Write the generated code FileWriteString(f, data); // Close the file FileClose(f); }

Next comes the very important part:

// Connecting the exported mqh file. // It will initialize the CGroupsLibrary::s_params[] static variable // and ENUM_GROUPS_LIBRARY enumeration #include "ExportedGroupsLibrary.mqh"

We include the file that will be received after the export directly into the GroupsLibrary.mqh file. In this case, the final EA will only need to include this file in order to be able to use the exported library. This approach creates a small inconvenience: in order to be able to compile the EA that will handle the library export, the ExportedGroupsLibrary.mqh file, which appears only after export, should already exist. However, only the presence of this file is important, not its contents. Therefore, we should simply create an empty file with this name in the current folder, and compilation will proceed without errors.

To run the EA method, we need a script or EA, in which this will happen. It might look like this:

//+------------------------------------------------------------------+ //| Inputs | //+------------------------------------------------------------------+ input group "::: Exporting from library" input string passes_ = "802150,802151,802152,802153,802154," "802155,802156,802157,802158,802159," "802160,802161,802162,802164,802165," "802166,802167,802168,802169,802173"; // - Comma-separated IDs of the saved passes //+------------------------------------------------------------------+ //| Expert initialization function | //+------------------------------------------------------------------+ int OnInit() { // Call the group library export method CGroupsLibrary::Export(passes_); // Successful initialization return(INIT_SUCCEEDED); } void OnTick() { ExpertRemove(); }

By changing the passes_ parameter, we can choose the composition and order, in which the groups will be exported from the library to the database. After running the EA once on the chart, the ExportedGroupsLibrary.mqh, file will appear in the terminal data folder. It should be transferred to the current folder containing the project code.

Creating the final EA

We have finally reached the final phase. All that remains is to make some minor changes to the SimpleVolumesExpert.mq5 EA. First, we need to include the GroupsLibrary.mqh file:

#include "GroupsLibrary.mqh"

Next, replace the passes_ input with a new one allowing us to select a group from the library:

input group "::: Selection for the group" input ENUM_GROUPS_LIBRARY groupId_ = -1; // - Group from the library

In the OnInit() function, instead of getting initialization strings from the database by pass IDs (as before), we will now simply take the initialization string from the CGroupsLibrary::s_params[] array with an index corresponding to the selected value of the groupId_ input:

//+------------------------------------------------------------------+ //| Expert initialization function | //+------------------------------------------------------------------+ int OnInit() { ... // Initialization string with strategy parameter sets string strategiesParams = NULL; // If the selected strategy group index from the library is valid, then if(groupId_ >= 0 && groupId_ < ArraySize(CGroupsLibrary::s_params)) { // Take the initialization string from the library for the selected group strategiesParams = CGroupsLibrary::s_params[groupId_]; } // If the strategy group from the library is not specified, then we interrupt the operation if(strategiesParams == NULL) { return INIT_FAILED; } ... // Successful initialization return(INIT_SUCCEEDED); }

Save the changes made to the SimpleVolumesExpert.mq5 file in the current folder.

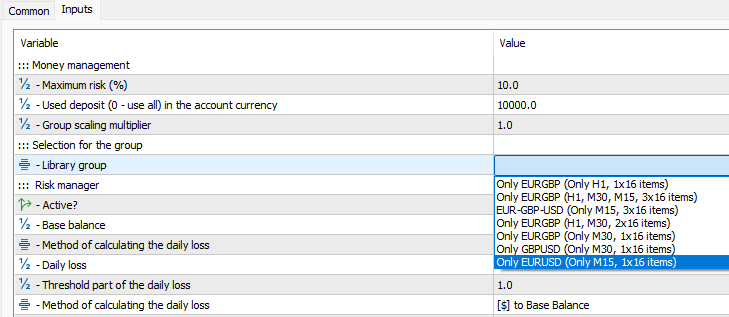

Since we have added comments with names to the ENUM_GROUPS_LIBRARY enumeration elements, then we will be able to see understandable names, and not just a sequence of numbers, in the dialog for selecting the EA parameters:

Fig. 2. Selecting a group from the library by name in the EA parameters

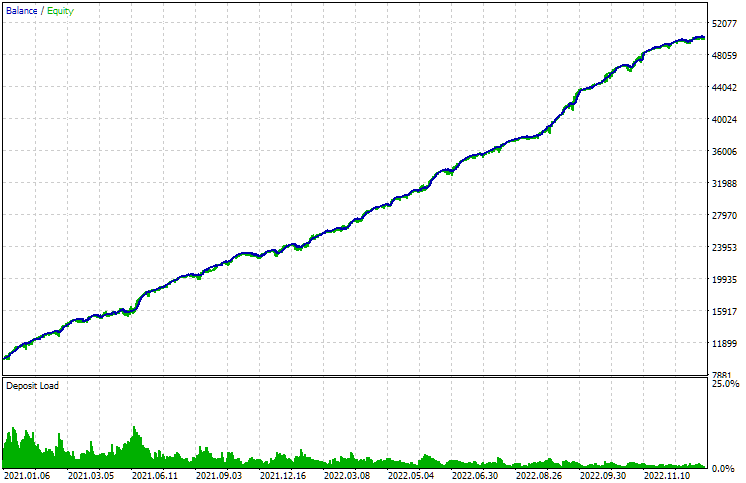

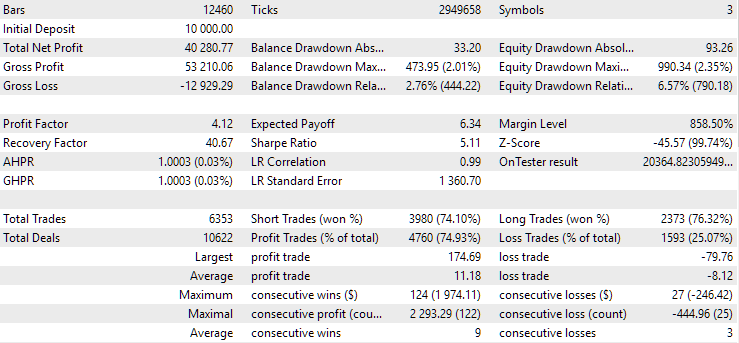

Let's run the EA with the last group from the list and look at the result:

Fig. 3. Results of testing the final EA with the most attractive group from the library

It is clear that the results for the average annual normalized profit indicator were close to those stored in the database. Small differences are primarily due to the fact that the final EA used a standardized group (this can be verified by looking at the value of the maximum relative drawdown, which is approximately 10% of the deposit used). When generating the initialization string for this group in the SimpleVolumesStage3.ex5 EA, the group was not yet standardized during the pass, so the drawdown there was approximately 5.4%.

Conclusion

We have received the final EA, which can work independently of the database filled in the optimization process. Perhaps, we will return to this issue again, since practice can make its own adjustments, and the method proposed in this article may turn out to be less convenient than some other. But in any case, achieving the set goal is a step forward.

While working on the code for this article, new circumstances were discovered that require further investigation. For example, it turned out that the results of testing this EA are sensitive not only to the quote server, but also to the symbol selected as the main one in the strategy tester settings. We may need to make some adjustments to the optimization automation in the first and second stages. But more about that next time.

Finally, I want to make a warning that was implicitly present before. I never said in the previous parts that following the proposed direction will allow you to get a guaranteed profit. On the contrary, we received disappointing test results at some points. Also, despite the efforts expended to prepare the EA for real trading, we are unlikely to be able to say at some point that we have done everything possible and impossible to ensure the correct operation of the EA on real accounts. This is a perfect outcome that can and should be strived for, but achieving it always seems like a matter of the foggy future. This, however, does not prevent us from approaching it.

All results presented in this article and all previous articles in the series are based only on historical testing data and are not a guarantee of any profit in the future. The work within this project is of a research nature. All published results can be used by anyone at their own risk.

Thank you for your attention! See you soon!

Archive contents

| # | Name | Version | Description | Recent changes |

|---|---|---|---|---|

| MQL5/Experts/Article.15360 | ||||

| 1 | Advisor.mqh | 1.04 | EA base class | Part 10 |

| 2 | Database.mqh | 1.04 | Class for handling the database | Part 17 |

| 3 | ExpertHistory.mqh | 1.00 | Class for exporting trade history to file | Part 16 |

| 4 | ExportedGroupsLibrary.mqh | — | Generated file listing strategy group names and the array of their initialization strings | Part 17 |

| 5 | Factorable.mqh | 1.01 | Base class of objects created from a string | Part 10 |

| 6 | GroupsLibrary.mqh | 1.00 | Class for working with a library of selected strategy groups | Part 17 |

| 7 | HistoryReceiverExpert.mq5 | 1.00 | EA for replaying the history of deals with the risk manager | Part 16 |

| 8 | HistoryStrategy.mqh | 1.00 | Class of the trading strategy for replaying the history of deals | Part 16 |

| 9 | Interface.mqh | 1.00 | Basic class for visualizing various objects | Part 4 |

| 10 | LibraryExport.mq5 | 1.00 | EA that saves initialization strings of selected passes from the library to the ExportedGroupsLibrary.mqh file | Part 17 |

| 11 | Macros.mqh | 1.02 | Useful macros for array operations | Part 16 |

| 12 | Money.mqh | 1.01 | Basic money management class | Part 12 |

| 13 | NewBarEvent.mqh | 1.00 | Class for defining a new bar for a specific symbol | Part 8 |

| 14 | Receiver.mqh | 1.04 | Base class for converting open volumes into market positions | Part 12 |

| 15 | SimpleHistoryReceiverExpert.mq5 | 1.00 | Simplified EA for replaying the history of deals | Part 16 |

| 16 | SimpleVolumesExpert.mq5 | 1.20 | EA for parallel operation of several groups of model strategies. The parameters will be taken from the built-in group library. | Part 17 |

| 17 | SimpleVolumesStage3.mq5 | 1.00 | The EA that saves a generated standardized group of strategies to a library of groups with a given name. | Part 17 |

| 18 | SimpleVolumesStrategy.mqh | 1.09 | Class of trading strategy using tick volumes | Part 15 |

| 19 | Strategy.mqh | 1.04 | Trading strategy base class | Part 10 |

| 20 | TesterHandler.mqh | 1.03 | Optimization event handling class | Part 17 |

| 21 | VirtualAdvisor.mqh | 1.06 | Class of the EA handling virtual positions (orders) | Part 15 |

| 22 | VirtualChartOrder.mqh | 1.00 | Graphical virtual position class | Part 4 |

| 23 | VirtualFactory.mqh | 1.04 | Object factory class | Part 16 |

| 24 | VirtualHistoryAdvisor.mqh | 1.00 | Trade history replay EA class | Part 16 |

| 25 | VirtualInterface.mqh | 1.00 | EA GUI class | Part 4 |

| 26 | VirtualOrder.mqh | 1.04 | Class of virtual orders and positions | Part 8 |

| 27 | VirtualReceiver.mqh | 1.03 | Class for converting open volumes to market positions (receiver) | Part 12 |

| 28 | VirtualRiskManager.mqh | 1.02 | Risk management class (risk manager) | Part 15 |

| 29 | VirtualStrategy.mqh | 1.05 | Class of a trading strategy with virtual positions | Part 15 |

| 30 | VirtualStrategyGroup.mqh | 1.00 | Class of trading strategies group(s) | Part 11 |

| 31 | VirtualSymbolReceiver.mqh | 1.00 | Symbol receiver class | Part 3 |

Translated from Russian by MetaQuotes Ltd.

Original article: https://www.mql5.com/ru/articles/15360

Warning: All rights to these materials are reserved by MetaQuotes Ltd. Copying or reprinting of these materials in whole or in part is prohibited.

This article was written by a user of the site and reflects their personal views. MetaQuotes Ltd is not responsible for the accuracy of the information presented, nor for any consequences resulting from the use of the solutions, strategies or recommendations described.

Price Action Analysis Toolkit Development (Part 17): TrendLoom EA Tool

Price Action Analysis Toolkit Development (Part 17): TrendLoom EA Tool

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

The work of the Expert Advisor consists of two parts: opening virtual positions and synchronisation of open virtual positions with real ones. The set TF is used only in the first part to determine the opening signal. And synchronisation should ideally be performed on each tick or at least on each new bar of the minimum timeframe M1, because at any moment the virtual position may reach TP or SL.

In the VirtualAdvisor::Tick() method, there is a check at the beginning for the occurrence of a new bar on all monitored symbols and timeframes, including M1. If it has not occurred, the Expert Advisor does not perform any more actions. It will do something else only when a new bar occurs on M1. In this case, you can optimise in OHLC mode on M1 and get almost the same results when the EA works on the chart (where there are all ticks). And optimisation is much faster this way. The line of code you mentioned is just a safety net in case we don't need to track a new bar on M1 in the strategy. This way it is guaranteed to be tracked at least on one symbol.

If you want, you can, of course, disable this mode of operation through the variable useOnlyNewBars_ = false. Then the Expert Advisor will check and synchronise positions on every available tick.

I see. But for example, can we make synchronisation of positions work on every tick, and opening of virtual (new) positions occurs when a new bar occurs on the TF specified in the strategy (m15,m30,h1)?

Opening of a new M1 bar can occur inside a bar of a higher timeframe. Note that SignalForOpen() uses the current timeframe, which is usually H1, M30 or M15. Therefore, there will no longer be a coincidence of the opening and closing prices of the current timeframe. In addition, this check comes only when the tick volume of the current bar on the current timeframe has significantly exceeded the typical tick volume of one bar. This cannot happen on the first tick, when the tick volume is only 1.

I don't understand you a little bit here. Yes, SignalForOpen() uses the TF set in the settings of the current virtual strategy instance, I can see that. But for example, if I want the EA to work strictly on the closed last bars, then here I have to specify units instead of zeros.

I should specify units instead of zeros ? Do I understand correctly ?

For example, can we make position synchronisation work on every tick, and opening of virtual (new) positions occurs when a new bar occurs on the TF specified in the strategy (m15,m30,h1)?

Yes, this will be the case if useOnlyNewBars_ = false. This variable is not used by strategies, they themselves determine when to check for an opening signal and when to open positions when a signal has been received earlier. For example, only when a new bar occurs on H1. In this case, you must then modify the code so that the signal received in the middle of the bar survives until the beginning of the next bar. Now the received signal is used immediately (leads to the opening of virtual positions), so it is not saved anywhere.

I don't understand you a bit here. Yes, SignalForOpen() uses the TF set in the settings of the current instance of the virtual strategy, I can see that. But for example, if I want the EA to work strictly on the closed last bars, then here I should specify units instead of zeros ? Do I understand correctly ?

If by the words"EA worked strictly on closed last bars" you mean that when the tick volume exceeds the threshold value on the current bar to determine the direction of the signal to open, we will take the previous bar and look at its direction, then you have understood everything correctly.

Yuri hello. I have an error when executing the Expert Advisor SimpleVolumesStage3.mq5 and saving information to the database:

What does it mean and how to fix it? The table was added to the database using your query from the article.

Yuri, I have been looking through your code and I see that the error occurs a little earlier in the CDatabase::Insert function, the log writes this:

Cannot execute

What can this be related to? The second stage is passed and the test itself passes (the Expert Advisor trades and passes from the database are loaded).

Hello Victor.

I will be back soon to continue working on this project and will try to sort out the errors I found. Thank you for finding them. I managed to reproduce some of the errors you wrote about earlier. They turned out to be related to the fact that in later parts, edits were made that were aimed at one thing, but in addition had an impact on other things that were not considered in the next article. This influence created errors. In the next article we will go through all the steps of automated optimisation again, eliminating all the errors that were detected.