We no longer run a Telegram channel. If you have any questions, please contact @Official_InrexEA on Telegram, or DM me here on MQL5.

Stay updated with us on our new MQL5 channel — Inrexea Official Channel:

https://www.mql5.com/en/channels/inrexea

Brokers we trust:

https://one.exnessonelink.com/a/t13mo13m

https://icmarkets.com/?camp=6671

https://vigco.co/la-com-inv/Iz57OmXz

Stay updated with us on our new MQL5 channel — Inrexea Official Channel:

https://www.mql5.com/en/channels/inrexea

Brokers we trust:

https://one.exnessonelink.com/a/t13mo13m

https://icmarkets.com/?camp=6671

https://vigco.co/la-com-inv/Iz57OmXz

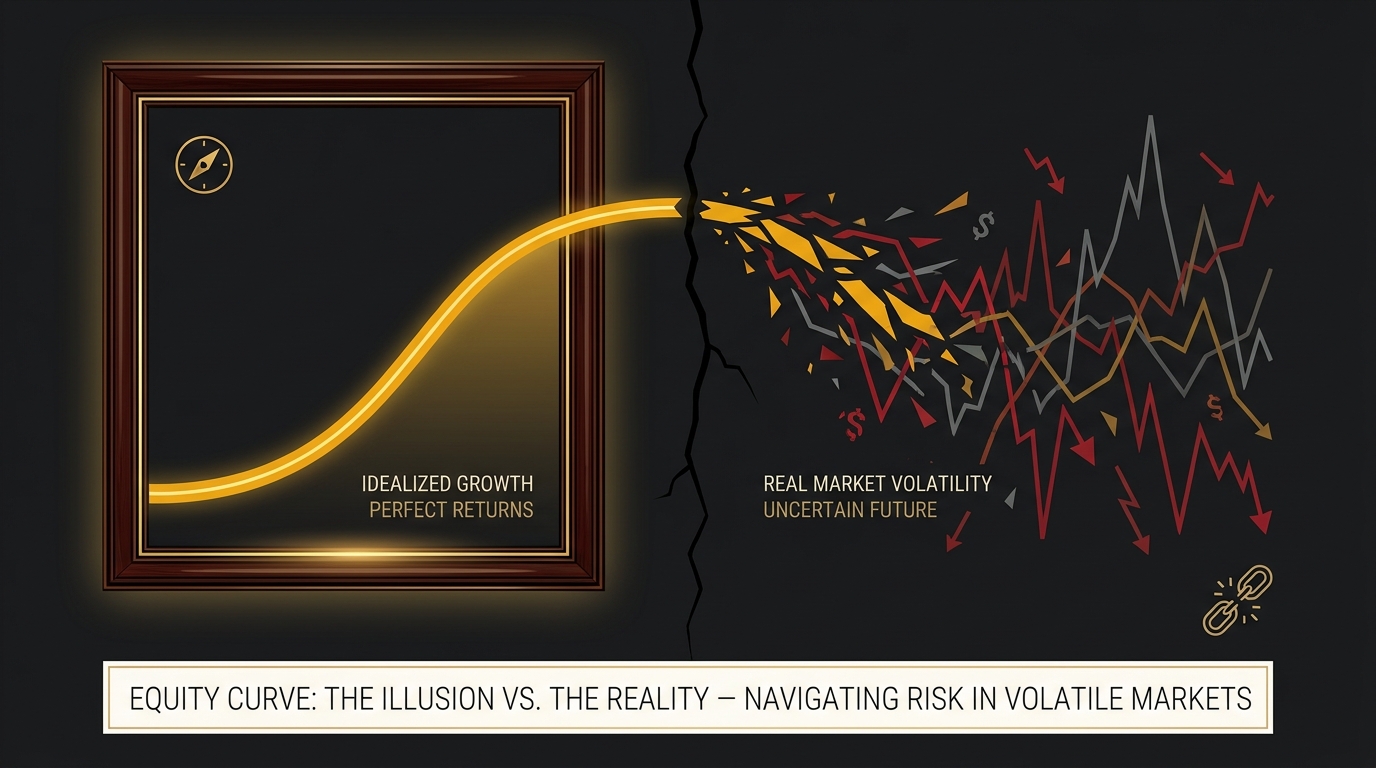

WHY WE STILL DON'T BELIEVE IN BACKTESTING — 2026 (PART 3)

InrexEA

Eight years ago I wrote that a backtest is a debugging tool, not a promise. Nothing since then has changed my mind. Everything since then has confirmed it.

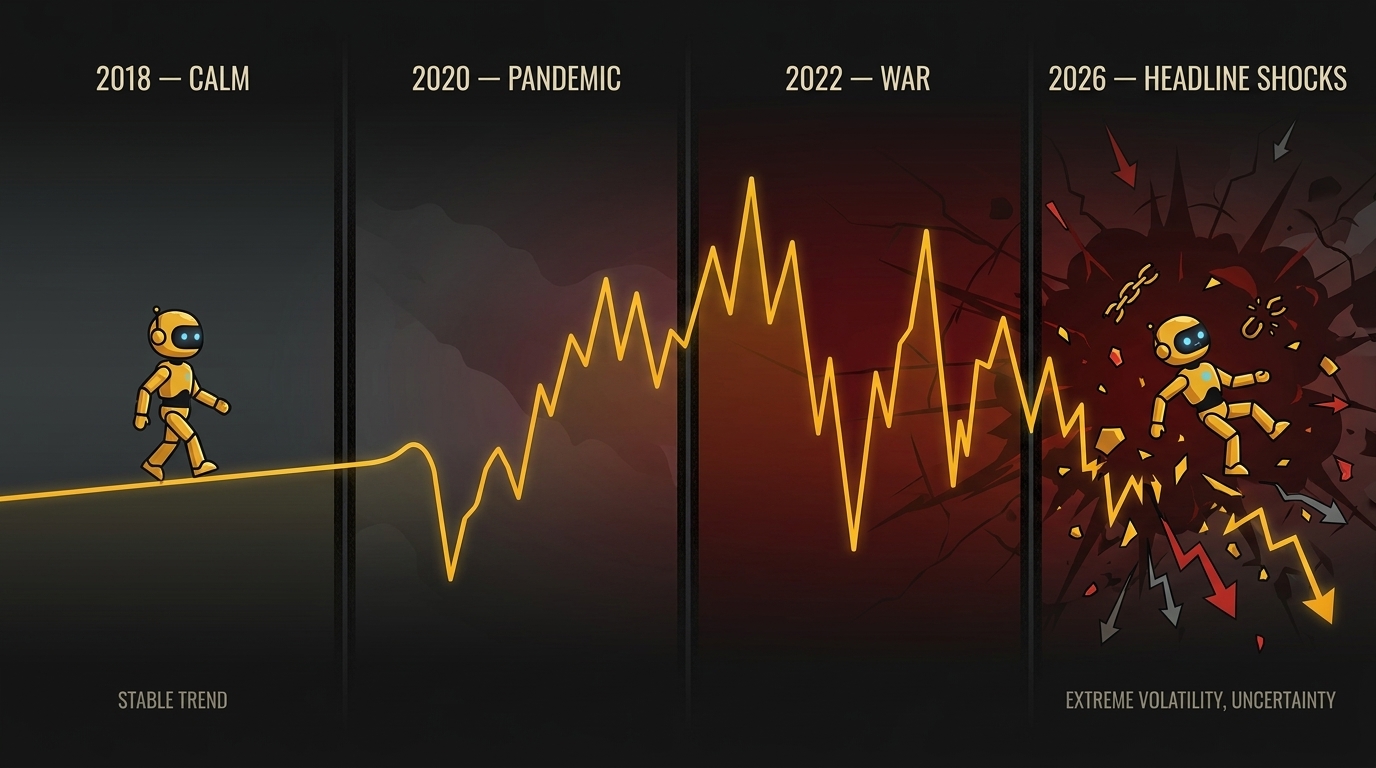

I first wrote about this in 2018. I wrote about it again in 2022. It is now 2026: gold trades at levels nobody in 2018 would have believed, the market can reprice on a single headline, and the number one question I still receive from buyers is:

"Can you show me the backtest?"

So let me say it one more time, as plainly as I can: we do not trust backtest results — including our own. Here is why, and here is what I think you should look at instead.

PART 1 RECAP (2018) — THE MACHINE LIES TO YOU

My 2018 argument was mechanical. The tester is not the market, and it never was.

- Slippage cannot be simulated. Not by the tester, not by third-party tools. Nobody — not even your broker — knows what your slippage will be before the order executes, because the book changes every second. You can guess it. You cannot know it.

- Spread is dynamic in the market and static in the tester. Real spreads widen on news, on rollover, on holidays, on thin liquidity. A fixed-spread test is a fantasy.

- The tester's trading conditions are not your account's trading conditions. Years ago I compared symbol properties between tester and live and found several that simply did not match — tick size, tick value, digits, point, step level. These are the values that decide whether an account survives or dies. And your broker can change them on your account without telling you.

- Multi-symbol and multi-timeframe logic could not be tested honestly in the old tester, so developers wrote code paths that only run inside it. Think about what that means for the "result" you are being shown.

That was 2018. The tooling has improved since — MT5's real-tick mode is far better than what MT4 offered. It has not solved a single one of the problems above. It has only made the picture more convincing.

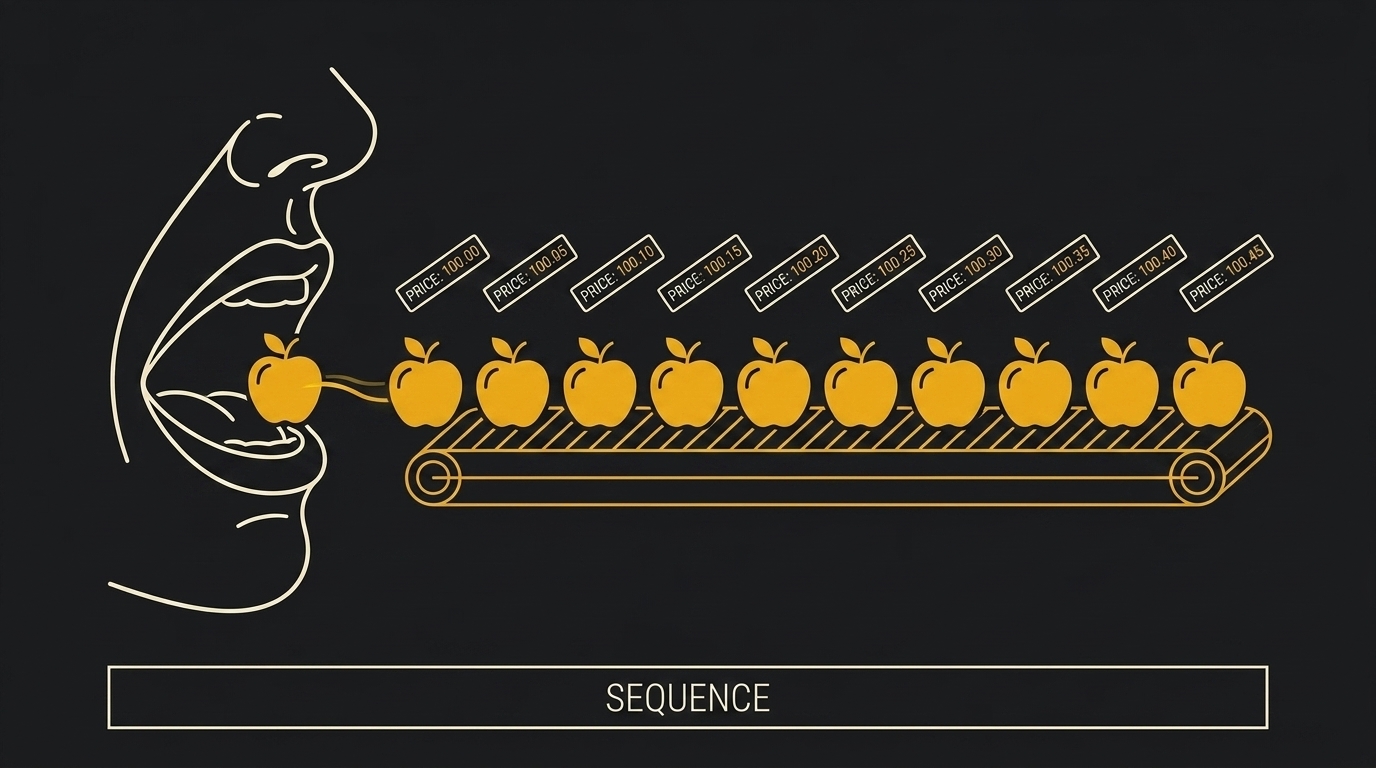

By 2022 I had stopped arguing about tick-data quality, because the deeper problem is structural. Three words: Sequence. Slippage. Latency.

Sequence, and market depth

A man with one mouth cannot eat ten apples at once. However fast he chews, he takes one bite at a time. That is market depth. When many participants buy and sell in the same moment, they do not all receive the same fill — they are filled in order. MT brokers quote you Bid and Ask. They do not show you the queue standing behind it.

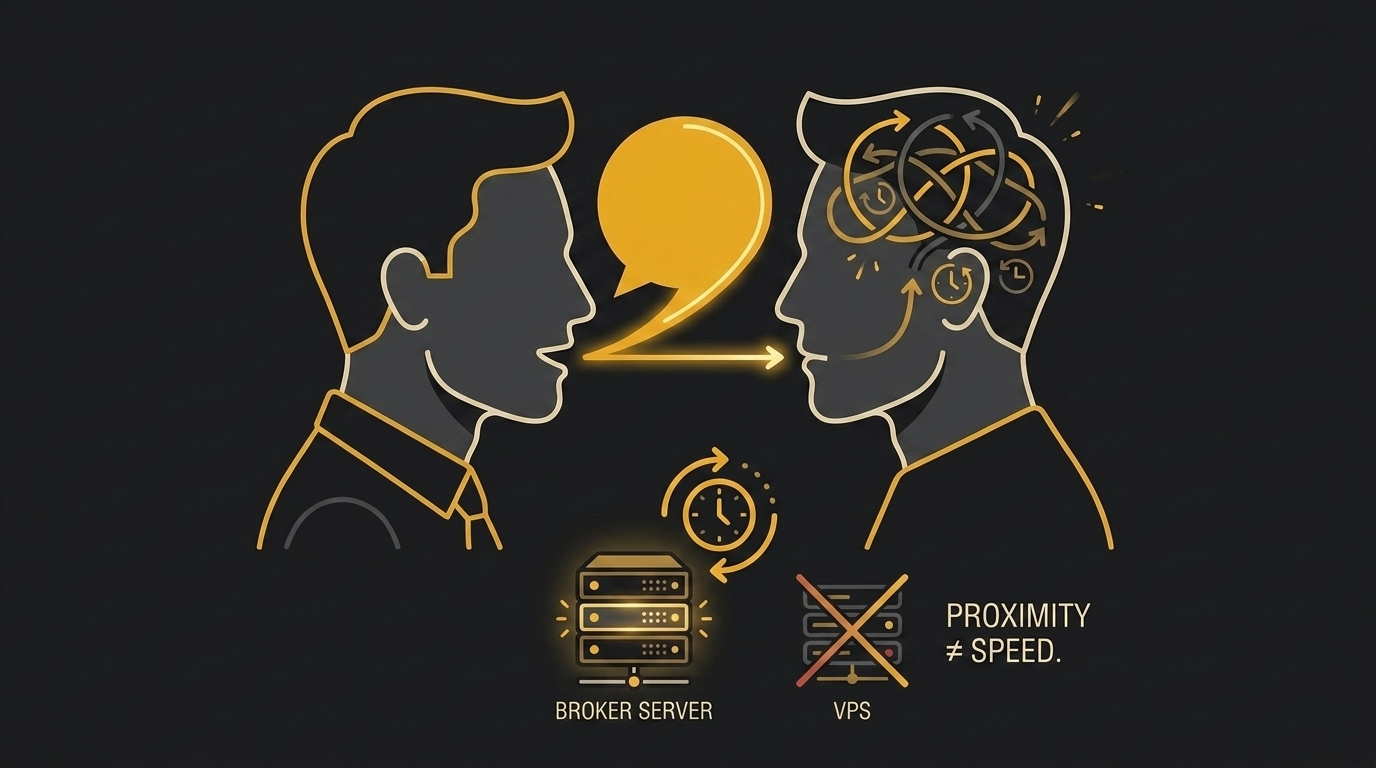

Latency

Some traders believe a VPS close to the broker's server solves execution delay. This is one of the most widespread pieces of miseducation in the industry. The bottleneck is usually the quality of the broker's internal server, not your distance from it. If I stand right in front of you and speak, my brain still needs time to react — standing closer does not fix that.

Two identical accounts diverge

I ran this test years ago: same funds, same server, same start time, same machine, same EA. Over a long enough run, the two accounts produced different results.

>>> If a real account cannot be reproduced by another real account, a backtest reproduces nothing at all.

PART 3 (2026) — THREE THINGS THAT MAKE IT WORSE THAN EVER

1. Overfitting is now industrial-scale

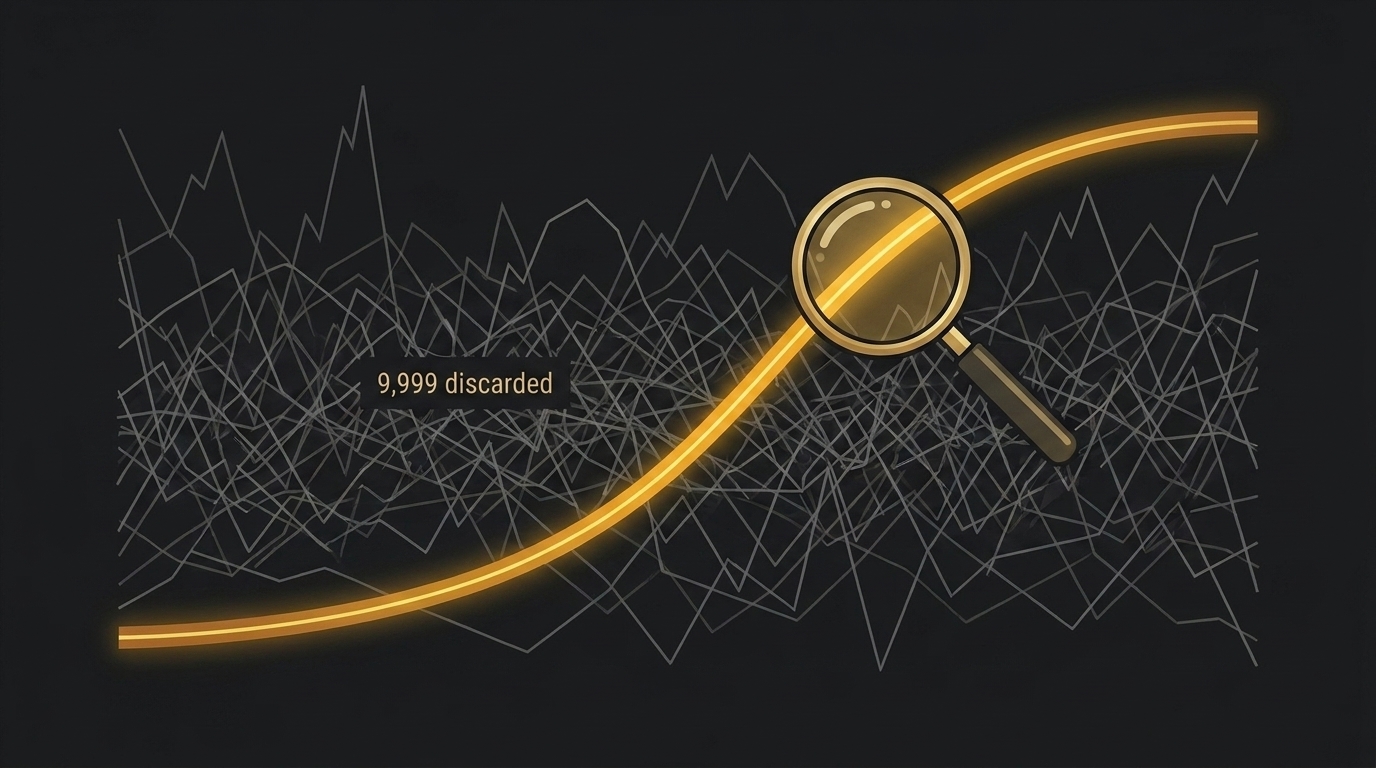

Here is the part most sellers will never explain to you.

Suppose you test ONE configuration and it looks good. Mildly interesting. Now suppose you test TEN THOUSAND — different periods, filters, sessions — and you present the best one. That result is not evidence of an edge. It is close to a mathematical certainty. Given enough attempts, a strong-looking curve appears even in pure random data.

Academic literature calls this backtest overfitting, or selection bias under multiple testing. Bailey and Lopez de Prado's work on the probability of backtest overfitting and the deflated Sharpe ratio exists precisely because this industry kept publishing beautiful, meaningless equity curves.

The uncomfortable truth: the more you optimise, the less your backtest means. A curve that looks TOO clean is not a mark of quality. It is a warning.

And in 2026, with cheap compute and AI-assisted parameter search, anyone can grind through millions of combinations over a weekend. The tools that make overfitting easy have improved far faster than the tools that detect it.

2. The market you fitted no longer exists

Every strategy is fitted — consciously or not — to a regime.

Consider what gold has lived through in a handful of years: a pandemic, a war, an inflation shock, a hiking cycle, a cutting cycle, central-bank accumulation, and now a market that can gap violently on one policy headline before most humans have finished reading it.

A model tuned on gold at $1,200, with orderly sessions and a narrow spread, is being asked to trade an instrument that behaves nothing like that today. The candles have the same shape. The regime underneath them does not.

3. The buyer is trained to want the wrong thing

Let me be honest about the ecosystem, because I am part of it.

Most new traders are pulled in by a gorgeous profit curve. I was one of them — I chased a video promising $500 turning into $130,000, and I lost money in my first year BECAUSE of beautiful backtests. When I learned to code properly, I understood the machinery well enough to stop using them to promote my own products.

But here is the trap for sellers: buyers demand a stunning backtest, so the market supplies stunning backtests. A seller who shows an honest, realistic, unglamorous curve loses the sale to the one who over-optimised. The incentive does not reward truth. It rewards the picture.

So that "low drawdown, high return" curve on the product page is often not the developer's best work. It is the developer's best marketing — and very often, the buyer's nightmare.

THE MISCONCEPTION THAT KILLS ACCOUNTS

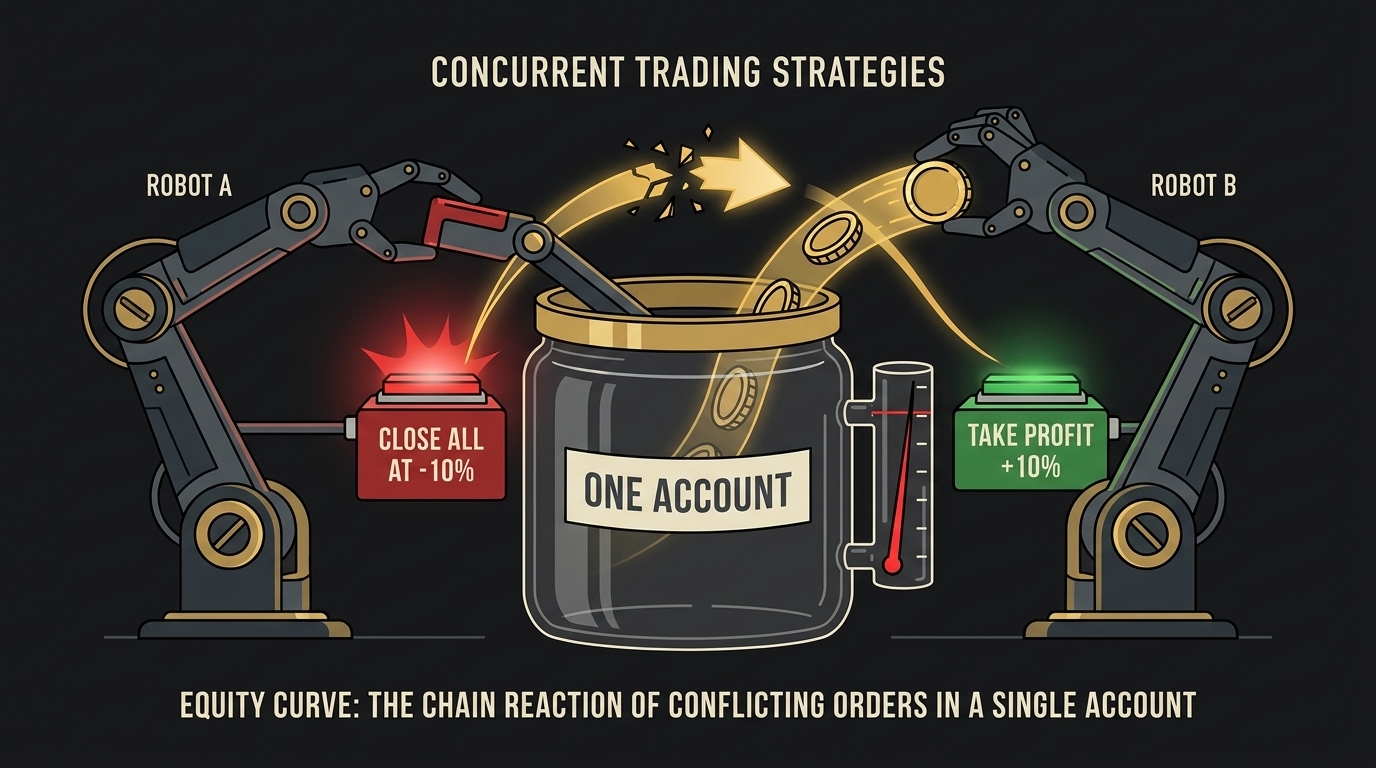

This has nothing to do with backtesting, and it destroys more accounts than bad strategies do: running several EAs on one account.

Different authors write risk logic differently. Some don't use magic numbers at all — they calculate from the state of the entire terminal.

WORKED EXAMPLE — HOW TWO HEALTHY EAs KILL EACH OTHER

EA-A closes everything when the account's floating loss reaches -10%. EA-B closes its own basket at +10% profit. At the moment EA-B takes profit, account floating loss sits at -5% — but EA-B's WINNING orders were the thing holding that number down. The instant they close, the remaining floating loss jumps past -10%, and EA-A liquidates the account.

Neither EA is broken. Together, they are.

Too many pairs, too much size. Two martingale-style systems on one account, one adverse move, and neither has the margin left to manage its own positions. Alone, either might have recovered. Together, both die. Cash is king.

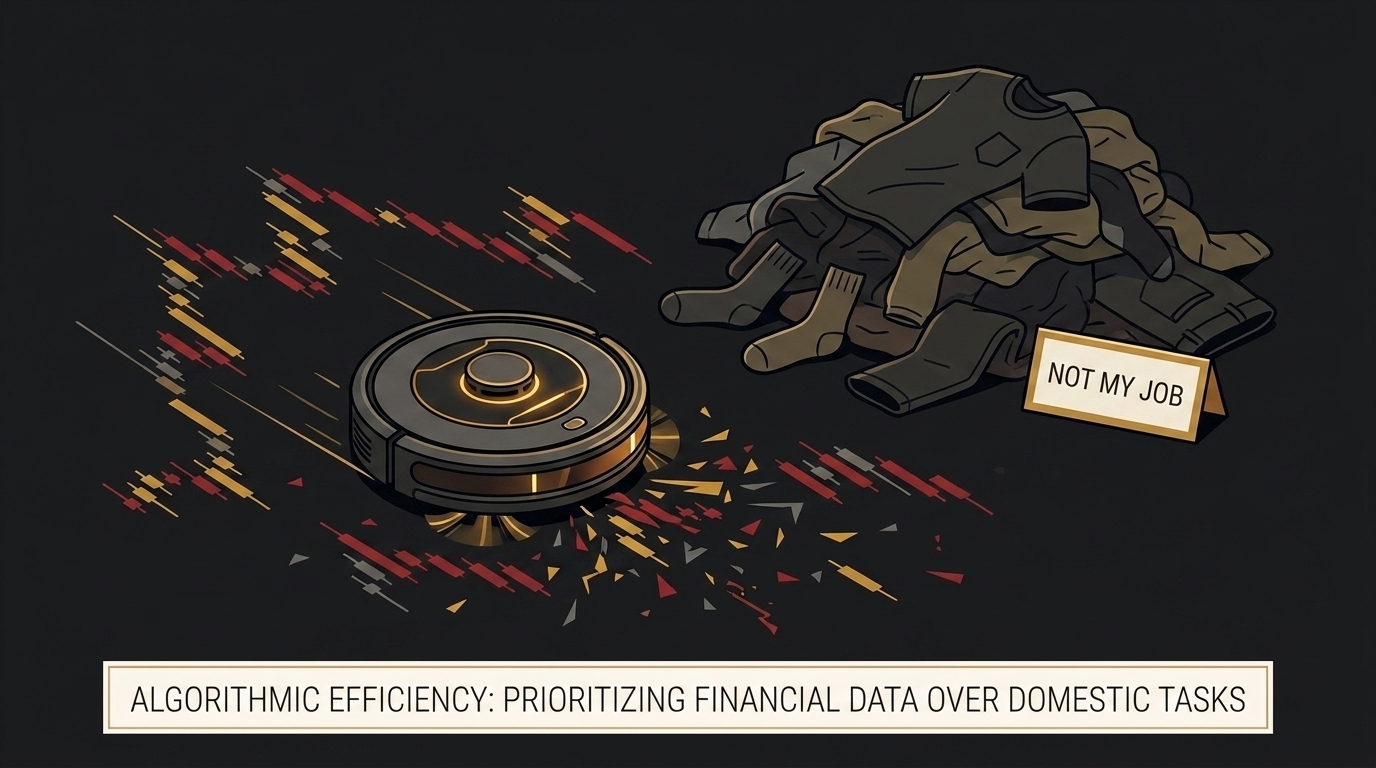

An EA is not a magic machine. To borrow my own line: it is a semi-automatic vacuum cleaner. It will not wash your clothes. I have been in this business for a decade and I am BUSIER than when I traded by hand.

>>> You will hear a thousand stories of traders who went broke from greed. You will never hear one about a man who went broke from being patient.

SO WHAT SHOULD YOU ACTUALLY LOOK AT?

If you throw away the backtest, what is left? This is our checklist. Apply it to us as strictly as you apply it to anyone else.

1. Live results, with real money. Not a demo. Not a tester. Real capital, real fills, real slippage.

2. Skin in the game. Does the developer trade this with their own money before selling it? If not, ask why.

3. Broker-agnostic logic. If a strategy needs one broker's exact quotes to work, it doesn't work. It is fitted to a data source, not to a market.

4. A defined worst case. Not "low drawdown." A number. What closes the basket? What halts the EA? Where is the floor?

5. No martingale, no lot escalation. With gold's current volatility, doubling into a loser is not a strategy. It is a countdown.

6. A developer who tells you what can go wrong. If every question is met with reassurance, you are not talking to an engineer. You are talking to a salesman.

7. Simplicity you can explain. If you cannot describe how it makes money in two sentences, you cannot judge when it stops working.

HOW THIS SHAPED MY LAST STRATEGY

None of the above is theory for us. It was the design brief. My Last Strategy is the last system I felt the need to build, and it was built by inverting every complaint in this article.

- No fitting to history. The engine reacts to live price structure rather than depending on the exact shape or timing of each candle — because a curve fitted to the past is fitted to a regime that has already ended.

- No single-broker dependency. Our clients run it across many different brokers. That is the test that matters — not a tester report.

- No martingale. Every grid level is the same size. No doubling, no escalation. Exposure stays bounded.

- A defined worst case. An optional hard stop — by percentage of balance, by fixed cash amount, or both — plus an optional circuit breaker that halts the EA entirely after a stop fires.

- Cushion over prediction. A grid engine survives on reserve, not on being right. Keep ~90% of the balance untouched. Risk the 10%.

- Skin in the game. We run our own private fund, and every strategy is traded with our own capital before it reaches anyone else.

My Last Strategy is capped at 200 copies. Once they are gone it is delisted permanently — no relisting. A smaller user base means better support, a protected edge, and improvements driven by real clients rather than by volume.

>>> What convinces us is not a pretty equity curve. It is real money, in real conditions, over real time.

COME AND ARGUE WITH US

Every verified customer is invited to our private Discord, where we share live results, settings and improvements — and where you are very welcome to challenge everything written here.

MQL5 Channel: https://www.mql5.com/en/channels/inrexea

Telegram: @Official_InrexEA

Website: https://www.inrexea.com

Earlier in this series:

Part 1 (2018) — Why I do not believe in backtest results

Part 2 (2022) — Why do we still not believe in backtesting

Risk disclaimer: Trading leveraged products carries substantial risk. Past performance, including backtests and live results, does not guarantee future returns. Test on a demo account first and trade only with capital you can afford to lose.

Trading Guide")