Session Overlap Is Where Gold Moves - Here's How to Trade It Without Getting Wrecked

Back in 2017, I thought I had the overlap figured out.

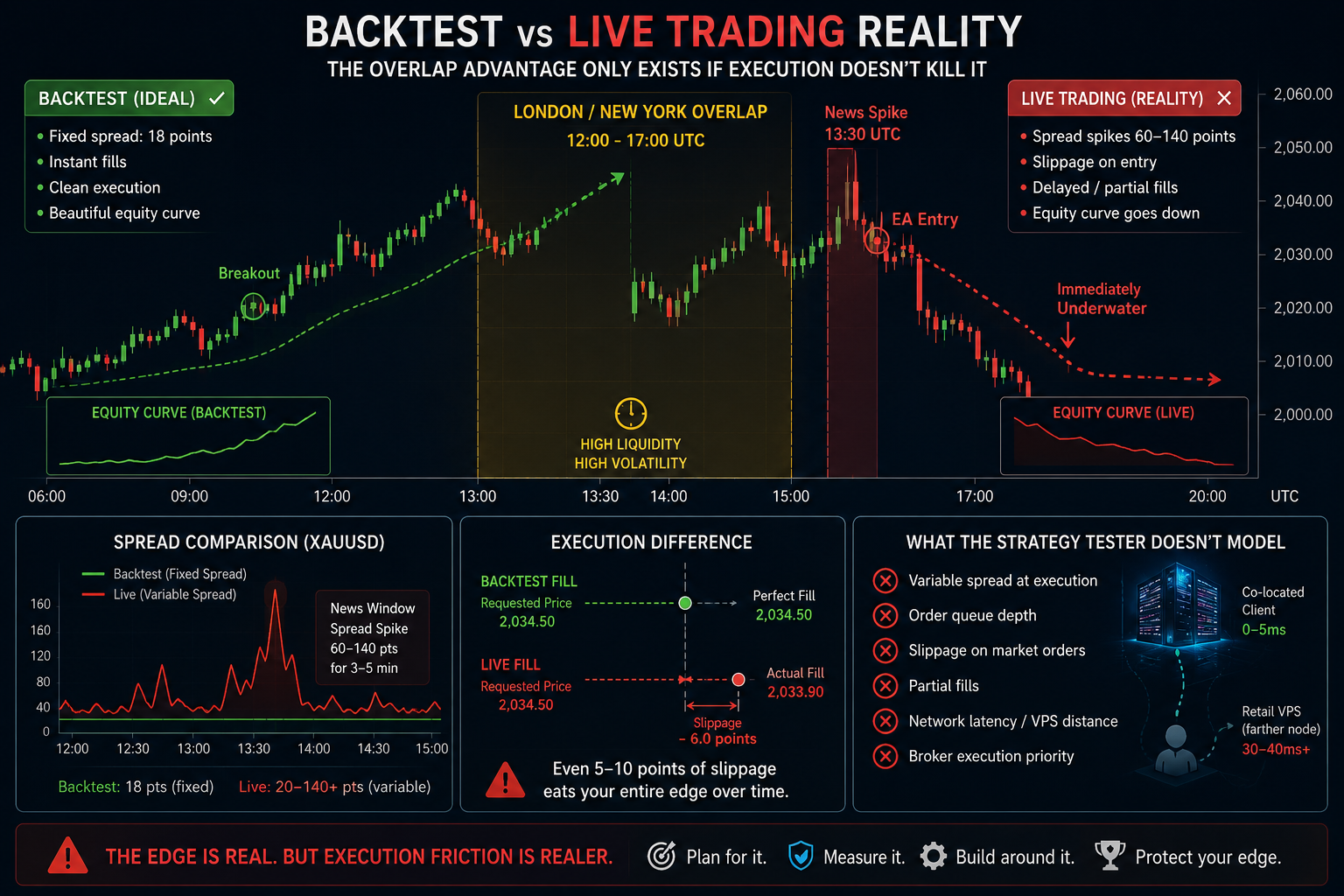

Six months of M15 backtest on XAUUSD. Fixed spread. Clean equity curve going up-right like a textbook diagram. The London/NY window - roughly 12:00 to 17:00 server time - kept printing the best setups. High ATR, directional momentum, clear structure breaks. The kind of results that make you feel like you've found something real.

Three weeks into live trading, the account was down 11%. Not catastrophically. But enough to force an honest post-mortem.

The backtest was using 18-point fixed spread. My live broker's XAUUSD spread during the 13:30 UTC news window was jumping to 60, 90, sometimes 140 points for 3–5 minutes straight. The EA was firing entries directly into that. Not once. Every relevant session for three weeks.

That was the first expensive lesson.

The second: the overlap doesn't show up the same every day. Clean Monday breakouts after Asian consolidation trade completely differently from choppy mid-week sessions on no-news Wednesdays. My strategy wasn't "working during the overlap" - it was working on specific overlap days. The backtest had no way to tell me that.

🌟 What Actually Happens During This Window

The London/New York overlap is roughly 12:00 - 17:00 UTC. Adjust by an hour during DST transitions - which will silently break your session logic if you hard-code the window as fixed hours. More on that later.

During this window, two major institutional liquidity pools are active simultaneously. For XAUUSD specifically, the combination of US dollar flow, macro data releases, and real-money positioning creates conditions where the market actually moves. Not Asian session noise. Directional moves with follow-through.

That's the opportunity side. The friction side gets less attention.

Spread on XAUUSD is not stable during this window. Pre-news it's manageable. Post-news it can spike hard and stay wide for several minutes. Partial fills happen on fast moves. If your VPS is routing through a node 30–40ms further from the broker's execution server than their co-located clients, you're regularly entering 5–8 points worse than your signal price. The Strategy Tester models none of this - it doesn't simulate order queue depth, spread-at-execution, or the reality that your market order lands in a book that's already moved.

I've had EAs that looked solid in testing become consistent small losers in live for exactly this reason. The edge existed. Execution friction ate it.

🌟 The Timing Problem

Most retail traders I've talked to aren't struggling with signal logic. They're trading at the wrong times.

Entering at 08:30 server time because "the setup looked good." Holding through Asian hours with a wide stop because they don't want to miss continuation. Running a fixed ATR-based stop calculated once at the daily open - on a number that has nothing to do with what XAUUSD is doing at 14:15 UTC.

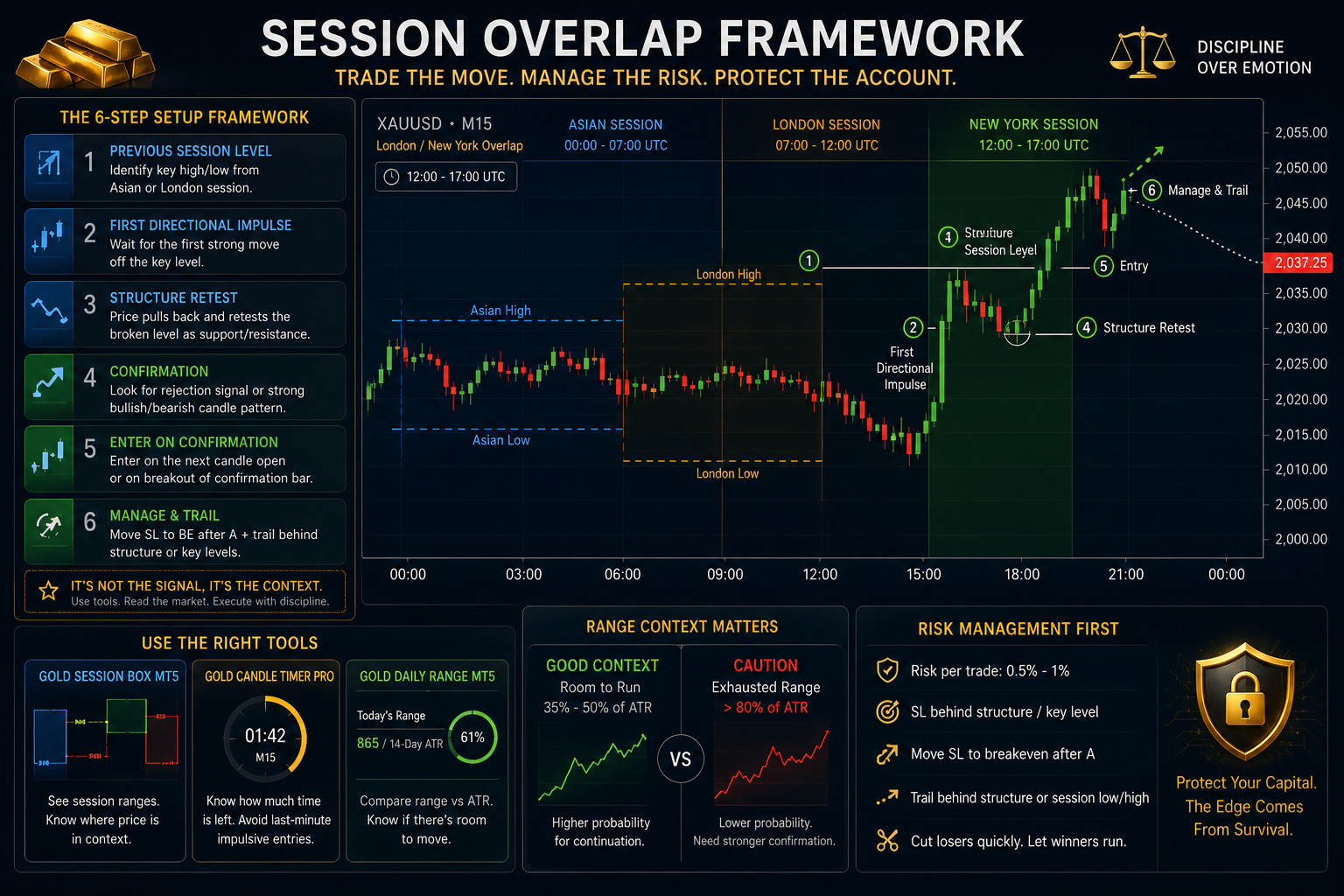

This is where Gold Session Box MT5 earns its place - not as a signal generator, but as a reference layer. It draws defined price ranges for each session so you can see whether price is inside the prior London range, just now breaking it, or already extended. The distinction matters. If price is still compressing inside the London range 45 minutes into the NY open, the probability of a clean directional break is lower. That's a filter, not a signal. But filters are what keep you out of bad trades.

I don't use session boxes to enter. I use them to decide whether the setup makes structural sense before I look at anything else.

🌟 Candle Close During High-Volatility Windows

This sounds like a minor detail. It isn't.

A 1H candle closing at 13:00 UTC might have spent 45 seconds spiking 30 points on a news print and the remaining 14:15 minutes mean-reverting. The close looks exactly the same as a smooth directional candle. Your EA doesn't know the difference. The setup logic fires on the close. You enter on the open of the next candle.

I've been burned by this specifically during NFP months - March 2022 being the one I remember clearly. Spread went from 22 to 108 points in under a minute. The EA entered on what looked like a valid M15 breakout close. Position was immediately underwater 60 points before any directional move happened. Stop hit. Trade log looked like a clean setup. It wasn't.

Gold Candle Timer Pro is the tool I use to manage this. Knowing there are 90 seconds left on the current candle versus 4 minutes left changes the decision - specifically for manual confirmation when I'm watching setups around news windows. If my EA flags something with less than 2 minutes left on the candle, I treat that confirmation as provisional until close is confirmed. That one rule has eliminated a category of bad entries for me.

🌟 Range Context Before You Enter

If XAUUSD has already moved 85% of its 14-day ATR by 14:00 UTC, buying a breakout is statistically fighting an exhausted range. You might still get a move. But the probability profile is different from entering when the day's range is 40% of ATR and there's room to expand.

Gold Daily Range MT5 shows the current day's range as a percentage of ATR alongside the prior day's range for comparison. It's one number. But that number changes how I read setups during the overlap.

I use it primarily as a late-entry filter. If we're already stretched above 80% of ATR and a setup forms at 14:30, I require more confirmation before taking it - tighter structure, cleaner rejection, more obvious level. If the daily range is 35 - 45% and there's clearly room to move, I'm more willing to take standard confirmation.

That's not a rule I can hard-code efficiently into an EA. It's a judgment call informed by a single metric. The tool makes that call faster.

🌟 The Setup Framework - And How It Actually Breaks

The core framework I use for the overlap:

First directional impulse off a prior session's key level. Specifically: M15 close outside the London session range with less than 25% wick-to-body ratio. Daily range below 70% of 14-day ATR. Entry on the first pullback candle, not the break candle. Stop below the session range edge. Exit before 17:00 UTC unless price is extended and has a visible continuation structure.

That's the setup. Here's where it breaks in live:

✅ News events. 13:30 UTC CPI or NFP invalidates anything building in the first 90 minutes of the overlap. My EA now runs a hard pause from T-5 to T+15 on high-impact events. When the news calendar check fails - connection drop, API timeout - the fallback is a 30-minute expanded pause on known data-heavy days. First Friday of the month. Second Tuesday. This has prevented exactly the kind of wrecked entries that killed the 2017 account.

✅ Spread spikes on normal days. Not just news. I've seen 110-point spreads on XAUUSD at 14:52 UTC on what showed as a calm Tuesday. No obvious catalyst. Liquidity provider pulled bids. The EA validates spread before every order submission and aborts above a threshold. That check never fires in the tester. In live, it fires occasionally - and those aborted trades would have been disasters.

✅ Broker time drift. DST transitions are the one that catches people. Not all brokers shift server time by the same amount - or at the same time as your local clock changes. If you hard-code Hour >= 12 && Hour <= 17, you will be wrong for portions of the year on some brokers. The correct approach: configurable GMT offset input, documented clearly, let the trader set it for their specific broker.

✅ Pre-overlap compression traps. Slow Asian session, slow early London. Price barely moves. Setup looks clean - range is tight, level is obvious. Overlap starts and a large institutional order drops, breaks both sides of the range, then finds direction. These sessions produce the worst slippage and the most confused trade logs. I have no systematic solution for this beyond being more selective on days where the Asian range is abnormally narrow.

🌟 On Backtesting This Honestly

If you're backtesting an overlap strategy with fixed spread, the results are unreliable.

A Sharpe ratio of 2.5 in a fixed-spread backtest on XAUUSD can turn into near-breakeven in live because the edge lives in those 3-4 minutes of high-spread execution per session. Remove those from the backtest with realistic variable spread and watch what happens to the curve.

I also want to flag 2020 and 2022 specifically. Multi-year backtests that include COVID volatility and the 2022 rate shock period will show outsized gains during those windows. If your strategy's best months are concentrated there, scrutinize forward performance assumptions carefully. Markets that behaved like that for 6-month stretches are not the baseline.

Test with variable spread. Run demo for at minimum 60 trading sessions. Track slippage as a separate line item from PnL - if you don't know your real execution cost, you don't know your real edge.

Was convinced once that my broker was manipulating fills. Turned out my VPS routing was going through an intermediary node adding 55ms to every execution. The fills were fine. My infrastructure was slow.

The overlap is a real edge. But cheap infrastructure will surface every flaw in your execution model. Sort that out before you size up.

🎁 New to Gold Algo Lab?

Start with the Gold Algo Lab Tool Map - a practical guide that organizes our MT5 tools into 6 connected stages: market context, setup selection, risk planning, trade execution, position management and account protection.

→ Gold Algo Lab Tool Map: Where to Actually Start With MT5 Tools for XAUUSD

https://www.mql5.com/en/blogs/post/771930

Do not choose a tool by its name alone. Start with the part of your trading process that needs the most control, then build your workflow one layer at a time.

Gold Algo Lab builds practical, risk-first MT5 tools for serious XAUUSD traders - shaped by 8 years of building and trading real systems, with no hype, no profit guarantees, and no unrealistic promises.

Products referenced in this article:

- Gold Session Box MT5 - Session range visualization for timing context

- Gold Candle Timer Pro - Candle countdown with session-aware display

- Gold Daily Range MT5 - Live ATR range tracker for daily context