The Hidden Cost of Bad Entry Timing: How Spread, Sessions, and Daily Range Destroy Your Edge

My backtest showed a 63% win rate with a smooth equity curve. Clean drawdown. Respectable Sharpe. I deployed it live.

Three weeks later the account was bleeding and I couldn't figure out why.

The logic wasn't wrong. The entries were sound. The exits were mathematically reasonable. The problem was something I'd completely discounted: the EA was running 24/5, and a significant chunk of its entries were firing during dead hours - wide spread, thin order book, nobody serious on the other side. My backtest assumed 1.2 pips average entry cost. Live was running 3.8 pips. On a scalp system targeting 6 - 8 pips, that's not a rounding error. That's the structural difference between an edge and a slow bleed.

I've seen this pattern in my own builds and in client EAs more times than I'd like to admit. The signal is usually fine. The execution environment is not.

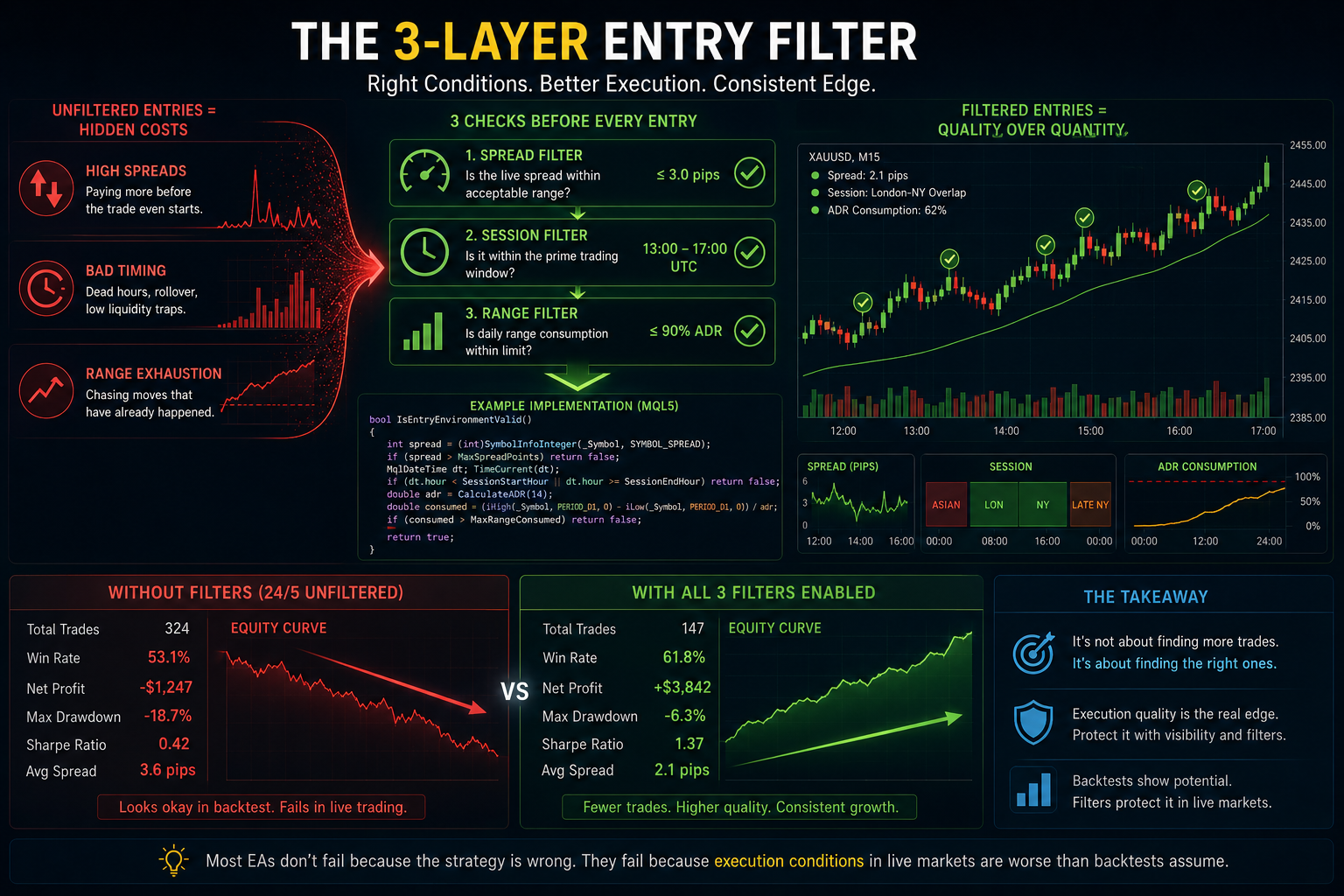

Spread, session timing, and daily range exhaustion. Almost nobody handles all three correctly. Most don't handle even one correctly.

🌟 Spread Is Not a Fixed Number

This sounds obvious. But the way MT5's Strategy Tester handles spread makes it easy to forget in practice.

By default - even with "variable spread" enabled - the tester applies a heavily smoothed spread model. It has no real concept of what happens during the rollover window, the 90 seconds after an NFP print, or 2am server time on a thin Sunday. Those conditions don't exist in the tester. They absolutely exist live.

Gold on a decent ECN broker: 1.5 - 2.5 pips during London-NY overlap. That same broker during Asian pre-session: 4 - 7 pips. During CPI or NFP: I've personally seen 20 - 35 pip spikes that last 10–15 seconds. Lower-tier liquidity providers are worse. I've watched a spread hit 60+ pips for a few seconds on a news release and come back like nothing happened - except the EA had already entered.

If your EA fires on a breakout or momentum signal without checking live spread first, you are entering at whatever the broker decides to offer at that exact moment. Sometimes fine. Sometimes you're 15 pips deep before the trade even registers.

The fix itself is simple:

// Use integer points — cleaner and no digit confusion int liveSpread = (int)SymbolInfoInteger(_Symbol, SYMBOL_SPREAD); int maxSpreadPoints = 30; // ~3.0 pips on Gold (5-digit broker) if (liveSpread > maxSpreadPoints) { // skip, log if needed return; }

The harder question is: what threshold actually makes sense for your strategy? That requires knowing your spread distribution by hour - not a single average across the week. The 3am spread profile on Gold is genuinely different from the 14:00 profile, and backtests flatten that completely.

This is why I keep Gold Spread Monitor MT5 running on a background chart during any live session where I'm evaluating EA behavior. It color-codes spread in real time against configurable thresholds. When you overlay that against your EA's entry log, you start seeing patterns - a cluster of entries firing right in the windows where spread is worst. The backtest never showed that because the backtest never had that problem.

🌟 Sessions Matter, But Not in the Way People Think

The standard advice is: avoid Asian session, trade London-NY overlap. That's directionally correct but too coarse to be useful.

The real issue is what happens within sessions, not just which session you're in.

London open - the first 30 - 45 minutes - is frequently brutal for breakout systems. Volume comes in fast, price moves aggressively, and in hindsight the setup looks obvious. Live, you get stop-hunted on the initial spike before the real move forms. I've had EAs hit 4 consecutive stops in the first hour of London open because the false breakout swept stops before committing to direction. The equity curve looks clean in backtest because the eventual trend is what gets captured. The entries that got stopped out before it started don't exist in the tester.

The NY-London overlap (roughly 13:00 - 16:00 UTC) is the most reliable window for Gold in terms of spread compression, liquidity depth, and follow-through on valid signals. Not perfect. But meaningfully better execution environment than most other hours.

What does consistent damage in production EAs: the 20:00 - 01:00 UTC window. Volume drops, spread widens, and whatever signal fires has less structural support. I've pulled trade logs and found EAs that looked fine on aggregate stats but were losing heavily concentrated in that window. You'd never see it from the equity curve alone.

There's also the rollover trap. Around 21:00 - 22:00 UTC depending on broker, liquidity goes nearly dead for a few minutes. Spread on Gold can jump from 2 pips to 25+ pips in that window. Any EA running without a time filter can get absolutely destroyed at rollover and the equity curve won't clearly show why.

MQL5-correct time handling:

MqlDateTime dt; TimeCurrent(dt); int serverHour = dt.hour; // London-NY overlap example — adjust for your broker's GMT offset bool inPrimeWindow = (serverHour >= 13 && serverHour < 17); // Avoid rollover and dead hours bool inDeadZone = (serverHour >= 20 || serverHour < 6);

One thing worth noting: the exact UTC offsets depend on your broker's server time, and that offset can shift by an hour during DST transitions. I had an EA filtering the wrong session window for nearly three weeks because I hadn't accounted for a broker running GMT+3 shifting to GMT+2 in winter. That kind of thing doesn't show in backtests. You find it by watching the EA run live and noticing entries happening at times that shouldn't be allowed.

Gold Session Box MT5 gives me the session high/low boundaries drawn directly on chart - visually anchored so during post-session review I can immediately see where entries were clustering relative to session structure. Not a signal generator. Just context, which is what you actually need when you're trying to diagnose why a live system is diverging from expectations.

🌟 Daily Range: The Variable Nobody Integrates Properly

Gold is not a constant-volatility instrument. Its average daily range shifts based on macro conditions, news cycle, and broader risk environment. A system calibrated to a 150-pip average day will be over-leveraged on a 280-pip trending day and under-participating on a 60-pip compression day. Both create problems. Neither shows clearly in aggregate backtest stats.

The basic concept is simple: scale your trade parameters to a percentage of recent ADR rather than fixed pip values.

// 14-day ADR calculation on daily bars double CalculateADR(int period) { double totalRange = 0; for (int i = 1; i <= period; i++) { totalRange += (iHigh(_Symbol, PERIOD_D1, i) - iLow(_Symbol, PERIOD_D1, i)); } return totalRange / period; } double adr = CalculateADR(14); double dynamicTP = adr * 0.20; // 20% of ADR double dynamicSL = adr * 0.12; // 12% of ADR

The part most people skip: range exhaustion filtering.

If Gold has already moved 170 pips from the session open and the 14-day ADR is 140 pips, you're at 121% of average daily movement. A breakout signal at that point is fighting against exhaustion. The move has probably already happened. Sometimes extended range days push further - I'm not saying block entries completely - but entering full size on a breakout when price has already run 120% of its average daily range is a different risk profile than entering at 40% consumption. You should be sizing down and targeting faster exits, not treating it the same.

double adr = CalculateADR(14); double todayRange = iHigh(_Symbol, PERIOD_D1, 0) - iLow(_Symbol, PERIOD_D1, 0); double consumed = todayRange / adr; // Optional: reduce lot size or skip entry if range heavily consumed if (consumed > 0.90) { // Either skip or scale down — depends on your strategy logic return; }

The frustrating part is that this doesn't show clearly in an equity curve. You lose a few trades on exhaustion days, they blend into the noise, and you attribute it to "bad luck" or "signal failure." It's not. It's range context.

I track this live with Gold Daily Range MT5 - shows current day progress against ADR and where price sits relative to day structure. During active sessions, when consumption hits 85 - 90% mid-session, that's a flag to tighten filters or skip new entries entirely.

🌟 Putting the Three Together

The entry filter I use across most Gold EA builds now runs all three checks before any position is considered:

bool IsEntryEnvironmentValid() { // 1. Spread int spread = (int)SymbolInfoInteger(_Symbol, SYMBOL_SPREAD); if (spread > MaxSpreadPoints) return false; // 2. Session MqlDateTime dt; TimeCurrent(dt); if (dt.hour < SessionStartHour || dt.hour >= SessionEndHour) return false; // 3. Range exhaustion double adr = CalculateADR(14); double consumed = (iHigh(_Symbol, PERIOD_D1, 0) - iLow(_Symbol, PERIOD_D1, 0)) / adr; if (consumed > MaxRangeConsumed) return false; return true; }

In backtesting, these filters look like they're leaving money on the table. Some of the filtered entries would have worked. That's always the case with entry quality filters - you're not trying to catch every move, you're trying to stop entering in conditions that are structurally worse than what your edge was built for.

Some days the filter blocks more than it lets through. That's fine. The goal isn't maximum entries.

🌟 The Tester Lies About All Three

I want to be direct about something before closing.

The MT5 Strategy Tester - even with real tick data and variable spread - does not accurately model what a live broker does during news events, session transitions, or rollover. The spread model is approximate. Slippage is simplified or absent. There are no partial fills. No latency. No freeze during volatile conditions. No broker-side requote that eats 2 - 3 pips before confirmation.

I've had systems with completely clean backtests fall apart live because the entry timing logic was depending on execution conditions that simply don't replicate outside the tester. The spread was assumed to behave normally. The session transitions were assumed to be clean. The fills were assumed to be instant.

None of these monitoring tools - spread tracking, session visualization, range progress - are backtest setup aids. Their real value is in live diagnosis. Running them alongside an active EA makes the gap between what the tester showed and what the broker is actually delivering visible. That gap exists in every live deployment I've ever run. The only question is how wide it is and whether you can see it clearly enough to act.

Most EAs don't fail because the signal logic is wrong. They fail because execution quality in real markets is consistently worse than backtests assume, and nobody built any visibility into that gap.

🎁 New to Gold Algo Lab?

Start with the Gold Algo Lab Tool Map - a practical guide that organizes our MT5 tools into 6 connected stages: market context, setup selection, risk planning, trade execution, position management and account protection.

→ Gold Algo Lab Tool Map: Where to Actually Start With MT5 Tools for XAUUSD

https://www.mql5.com/en/blogs/post/771930

Do not choose a tool by its name alone. Start with the part of your trading process that needs the most control, then build your workflow one layer at a time.

Gold Algo Lab builds practical, risk-first MT5 tools for serious XAUUSD traders - shaped by 8 years of building and trading real systems, with no hype, no profit guarantees, and no unrealistic promises.