MQL5 Programming Articles

Study the MQL5 language for programming trading strategies in numerous published articles mostly written by you - the community members. The articles are grouped into categories to help you quicker find answers to any questions related to programming: Integration, Tester, Trading Strategies, etc.

Follow our new publications and discuss them on the Forum!

Add a new article

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

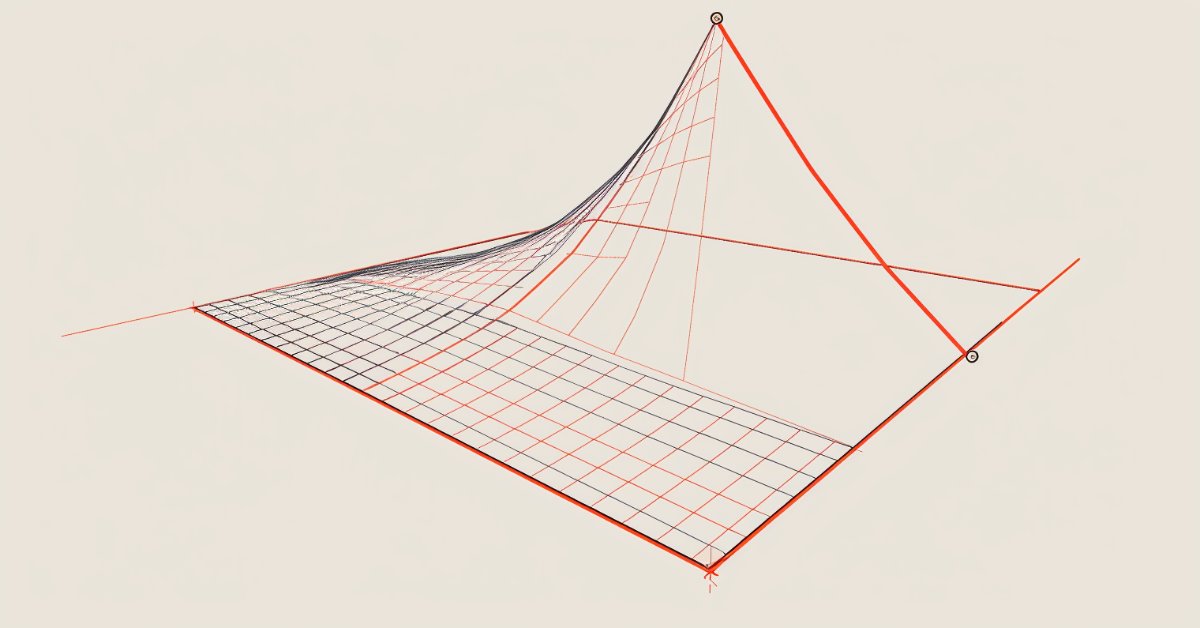

Biological neuron for forecasting financial time series

We will build a biologically correct system of neurons for time series forecasting. The introduction of a plasma-like environment into the neural network architecture creates a kind of "collective intelligence," where each neuron influences the system's operation not only through direct connections, but also through long-range electromagnetic interactions. Let's see how the neural brain modeling system will perform in the market.

Reimagining Classic Strategies (Part 14): High Probability Setups

High probability Setups are well known in our trading community, but regrettably they are not well-defined. In this article, we will aim to find an empirical and algorithmic way of defining exactly what is a high probability setup, identifying and exploiting them. By using Gradient Boosting Trees, we demonstrated how the reader can improve the performance of an arbitrary trading strategy and better communicate the exact job to be done to our computer in a more meaningful and explicit manner.

From CPU to GPU in MQL5: A Practical OpenCL Framework for Accelerating Research, Optimizations, and Patterns

Find out how to build a practical CPU-to-GPU migration path in MQL5 using OpenCL. We will focus on context initialization, buffer organization, large batches, kernel startup, and minimizing data exchanges. Typical errors and ways to eliminate them will be considered as well. An example with candlestick patterns illustrates the practical benefit of the approach.

From Basic to Intermediate: Array (IV)

In this article, we'll look at how you can do something very similar to what's implemented in languages like C, C++, and Java. I am talking about passing a virtually infinite number of parameters inside a function or procedure. While this may seem like a fairly advanced topic, in my opinion, what will be shown here can be easily implemented by anyone who has understood the previous concepts. Provided that they were really properly understood.

Feature Engineering With Python And MQL5 (Part III): Angle Of Price (2) Polar Coordinates

In this article, we take our second attempt to convert the changes in price levels on any market, into a corresponding change in angle. This time around, we selected a more mathematically sophisticated approach than we selected in our first attempt, and the results we obtained suggest that our change in approach may have been the right decision. Join us today, as we discuss how we can use Polar coordinates to calculate the angle formed by changes in price levels, in a meaningful way, regardless of which market you are analyzing.

Building Volatility Models in MQL5 (Part II): Implementing GJR-GARCH and TARCH in MQL5

The article implements GJR-GARCH and TARCH in an MQL5 volatility library and explains why asymmetry improves on standard ARCH/GARCH. It covers model formulation, parameterization, and usage through derived classes and scripts. Readers get code examples for calibration and one-step-ahead forecasting on real data to support risk and diagnostics.

Developing a Replay System (Part 67): Refining the Control Indicator

In this article, we'll look at what can be achieved with a little code refinement. This refinement is aimed at simplifying our code, making more use of MQL5 library calls and, above all, making it much more stable, secure and easy to use in other projects that we may develop in the future.

Causal inference in time series classification problems

In this article, we will look at the theory of causal inference using machine learning, as well as the custom approach implementation in Python. Causal inference and causal thinking have their roots in philosophy and psychology and play an important role in our understanding of reality.

Formulating Dynamic Multi-Pair EA (Part 8): Time-of-Day Capital Rotation Approach

This article presents a Time-of-Day capital rotation engine for MQL5 that allocates risk by trading session instead of using uniform exposure. We detail session budgets within a daily risk cap, dynamic lot sizing from remaining session risk, and automatic daily resets. Execution uses session-specific breakout and fade logic with ATR-based volatility confirmation. Readers gain a practical template to deploy capital where session conditions are statistically strongest while keeping exposure controlled throughout the day.

Anarchic Society Optimization (ASO) algorithm

In this article, we will get acquainted with the Anarchic Society Optimization (ASO) algorithm and discuss how an algorithm based on the irrational and adventurous behavior of participants in an anarchic society (an anomalous system of social interaction free from centralized power and various kinds of hierarchies) is able to explore the solution space and avoid the traps of local optimum. The article presents a unified ASO structure applicable to both continuous and discrete problems.

Neural Networks Made Easy (Part 90): Frequency Interpolation of Time Series (FITS)

By studying the FEDformer method, we opened the door to the frequency domain of time series representation. In this new article, we will continue the topic we started. We will consider a method with which we can not only conduct an analysis, but also predict subsequent states in a particular area.

Implementing Practical Modules from Other Languages in MQL5 (Part 04): time, date, and datetime modules from Python

Unlike MQL5, Python programming language offers control and flexibility when it comes to dealing with and manipulating time. In this article, we will implement similar modules for better handling of dates and time in MQL5 as in Python.

Account Audit System in MQL5 (Part 1): Designing the User Interface

This article builds the user interface layer of an Account Audit System in MQL5 using CChartObject classes. We construct an on-chart dashboard that displays key metrics such as start/end balance, net profit, total trades, wins/losses, win rate, withdrawals, and a star-based performance rating. A menu button lets you show or hide the panel and restores one-click trading, delivering a clean, usable foundation for the broader audit pipeline.

3D Visualization Without External Libraries: How MetaTrader 5 Reveals Optimization Results via MQL5 + DX11

The article describes the practical application of DirectX 11 and built-in MQL5 tools for creating 3D visualizations and interactive interfaces in MetaTrader 5. The focus is on cognitive efficiency - the ability of 3D charts and guided scenes to help in understanding optimization data, liquidity clusters, and multi-dimensional trading scenarios. The basics of the DX pipeline, working with shaders, binding mouse and keyboard events, and objective technological limitations are discussed in detail. The article is intended for MQL5 developers and algorithmic traders who are ready to transform strategy metrics into understandable 3D analytical landscapes, where the visual layer accelerates decision-making.

From Basic to Intermediate: Arrays and Strings (II)

In this article I will show that although we are still at a very basic stage of programming, we can already implement some interesting applications. In this case, we will create a fairly simple password generator. This way we will be able to apply some of the concepts that have been explained so far. In addition, we will look at how solutions can be developed for some specific problems.

Neural Networks in Trading: Generalized 3D Referring Expression Segmentation

While analyzing the market situation, we divide it into separate segments, identifying key trends. However, traditional analysis methods often focus on one aspect and thus limit the proper perception. In this article, we will learn about a method that enables the selection of multiple objects to ensure a more comprehensive and multi-layered understanding of the situation.

Introduction to MQL5 (Part 32): Mastering API and WebRequest Function in MQL5 (VI)

This article will show you how to visualize candle data obtained via the WebRequest function and API in candle format. We'll use MQL5 to read the candle data from a CSV file and display it as custom candles on the chart, since indicators cannot directly use the WebRequest function.

From Basic to Intermediate: Template and Typename (III)

In this article, we will discuss the first part of the topic, which is not so easy for beginners to understand. In order not to get even more confused and to explain this topic correctly, we will divide the explanation into stages. We will devote this article to the first stage. However, although at the end of the article it may seem that we have reached the deadlock, in fact we will take a step towards another situation, which will be better understood in the next article.

Neural Network in Practice: Least Squares

In this article, we'll look at a few ideas, including how mathematical formulas are more complex in appearance than when implemented in code. In addition, we will consider how to set up a chart quadrant, as well as one interesting problem that may arise in your MQL5 code. Although, to be honest, I still don't quite understand how to explain it. Anyway, I'll show you how to fix it in code.

An introduction to Receiver Operating Characteristic curves

ROC curves are graphical representations used to evaluate the performance of classifiers. Despite ROC graphs being relatively straightforward, there exist common misconceptions and pitfalls when using them in practice. This article aims to provide an introduction to ROC graphs as a tool for practitioners seeking to understand classifier performance evaluation.

Market Simulation (Part 21): First Steps with SQL (IV)

Many of you may have far more experience working with databases than I do, and therefore may have a different opinion. Since it was necessary to explain why databases are designed the way they are, and why SQL has the form it does—especially why primary and foreign keys emerged—some things had to remain somewhat abstract.

Neural networks are easy (Part 59): Dichotomy of Control (DoC)

In the previous article, we got acquainted with the Decision Transformer. But the complex stochastic environment of the foreign exchange market did not allow us to fully implement the potential of the presented method. In this article, I will introduce an algorithm that is aimed at improving the performance of algorithms in stochastic environments.

Requesting in Connexus (Part 6): Creating an HTTP Request and Response

In this sixth article of the Connexus library series, we will focus on a complete HTTP request, covering each component that makes up a request. We will create a class that represents the request as a whole, which will help us bring together the previously created classes.

Self Optimizing Expert Advisor With MQL5 And Python (Part VI): Taking Advantage of Deep Double Descent

Traditional machine learning teaches practitioners to be vigilant not to overfit their models. However, this ideology is being challenged by new insights published by diligent researches from Harvard, who have discovered that what appears to be overfitting may in some circumstances be the results of terminating your training procedures prematurely. We will demonstrate how we can use the ideas published in the research paper, to improve our use of AI in forecasting market returns.

Overcoming The Limitation of Machine Learning (Part 7): Automatic Strategy Selection

This article demonstrates how to automatically identify potentially profitable trading strategies using MetaTrader 5. White-box solutions, powered by unsupervised matrix factorization, are faster to configure, more interpretable, and provide clear guidance on which strategies to retain. Black-box solutions, while more time-consuming, are better suited for complex market conditions that white-box approaches may not capture. Join us as we discuss how our trading strategies can help us carefully identify profitable strategies under any circumstance.

From Static MA to Adaptive Filtering (Part 2): Implementing the SAMA_NLMS Indicator in MQL5

This article implements the NLMS-based Self-Adaptive Moving Average as a working MQL5 indicator. It provides the complete source code and explains the key design choices, including inline execution, uniform weight seeding, closed‑bar updates, and stability bounds, along with installation, usage, and limitations. The result is a compiled, chart‑ready SAMA_NLMS indicator and a clear basis for subsequent EA benchmarking.

Category Theory in MQL5 (Part 17): Functors and Monoids

This article, the final in our series to tackle functors as a subject, revisits monoids as a category. Monoids which we have already introduced in these series are used here to aid in position sizing, together with multi-layer perceptrons.

Neural networks made easy (Part 82): Ordinary Differential Equation models (NeuralODE)

In this article, we will discuss another type of models that are aimed at studying the dynamics of the environmental state.

Most notable Artificial Cooperative Search algorithm modifications (ACSm)

Here we will consider the evolution of the ACS algorithm: three modifications aimed at improving the convergence characteristics and the algorithm efficiency. Transformation of one of the leading optimization algorithms. From matrix modifications to revolutionary approaches regarding population formation.

The MQL5 Standard Library Explorer (Part 2): Connecting Library Components

Today, we take an important step toward helping every developer understand how to read class structures and quickly build Expert Advisors using the MQL5 Standard Library. The library is rich and expandable, yet it can feel like being handed a complex toolkit without a manual. Here we share and discuss an alternative integration routine—a concise, repeatable workflow that shows how to connect classes reliably in real projects.

Overcoming The Limitation of Machine Learning (Part 2): Lack of Reproducibility

The article explores why trading results can differ significantly between brokers, even when using the same strategy and financial symbol, due to decentralized pricing and data discrepancies. The piece helps MQL5 developers understand why their products may receive mixed reviews on the MQL5 Marketplace, and urges developers to tailor their approaches to specific brokers to ensure transparent and reproducible outcomes. This could grow to become an important domain-bound best practice that will serve our community well if the practice were to be widely adopted.

Data Science and ML (Part 44): Forex OHLC Time series Forecasting using Vector Autoregression (VAR)

Explore how Vector Autoregression (VAR) models can forecast Forex OHLC (Open, High, Low, and Close) time series data. This article covers VAR implementation, model training, and real-time forecasting in MetaTrader 5, helping traders analyze interdependent currency movements and improve their trading strategies.

Developing a Replay System (Part 69): Getting the Time Right (II)

Today we will look at why we need the iSpread feature. At the same time, we will understand how the system informs us about the remaining time of the bar when there is not a single tick available for it. The content presented here is intended solely for educational purposes. Under no circumstances should the application be viewed for any purpose other than to learn and master the concepts presented.

Chemical reaction optimization (CRO) algorithm (Part I): Process chemistry in optimization

In the first part of this article, we will dive into the world of chemical reactions and discover a new approach to optimization! Chemical reaction optimization (CRO) uses principles derived from the laws of thermodynamics to achieve efficient results. We will reveal the secrets of decomposition, synthesis and other chemical processes that became the basis of this innovative method.

Building a Dynamic STF Liquidity Sweep Indicator in MQL5

The article delivers a dynamic MetaTrader 5 indicator that detects liquidity sweeps via swing‑point logic, wick‑ratio thresholds, and engulfing confirmation. It recognizes single‑wick and dual‑candle patterns without a fixed window, updates buy‑/sell‑side targets as price evolves, and invalidates broken levels to maintain a reliable liquidity map.

Developing a Replay System (Part 33): Order System (II)

Today we will continue to develop the order system. As you will see, we will be massively reusing what has already been shown in other articles. Nevertheless, you will receive a small reward in this article. First, we will develop a system that can be used with a real trading server, both from a demo account or from a real one. We will make extensive use of the MetaTrader 5 platform, which will provide us with all the necessary support from the beginning.

Using the MQL5 Economic Calendar for News Filter (Part 3): Surviving Terminal Restarts During News Window

The article introduces a restart-safe storage model for news-time stop removal. Suspension state and original SL/TP per position are written to terminal global variables, reconstructed on OnInit, and cleaned after restoration. This lets the EA resume an active suspension window after recompiles or restarts and restore stops only when the news window ends.

Population optimization algorithms: Whale Optimization Algorithm (WOA)

Whale Optimization Algorithm (WOA) is a metaheuristic algorithm inspired by the behavior and hunting strategies of humpback whales. The main idea of WOA is to mimic the so-called "bubble-net" feeding method, in which whales create bubbles around prey and then attack it in a spiral motion.

Market Simulation (Part 10): Sockets (IV)

In this article, we'll look at what you need to do to start using Excel to manage MetaTrader 5, but in a very interesting way. To do this, we will use an Excel add-in to avoid using built-in VBA. If you don't know what add-in is meant, read this article and learn how to program in Python directly in Excel.

Neural Networks in Trading: Hierarchical Dual-Tower Transformer (Final Part)

We continue to build the Hidformer hierarchical dual-tower transformer model designed for analyzing and forecasting complex multivariate time series. In this article, we will bring the work we started earlier to its logical conclusion — we will test the model on real historical data.