100 best optimization passes (part 1). Developing optimization analyzer

- Introduction

- Optimization analyzer structure

- Graphics

- Working with the database

- Calculations

- Presenter

- Conclusion

Introduction

Modern technology has now become so deeply ingrained into the field of financial trading that it is now almost impossible to imagine how we could do without it. Nevertheless, just a very short while ago, trading was conducted manually and there was a complex system of hand language (quickly heading into oblivion nowadays) describing how much asset to buy or sell.

Personal computers rapidly superseded traditional trading methods by bringing online trading literally into our homes. Now we can look at asset quotes in real time and make appropriate decisions. Moreover, the advent of online technologies in the market industry causes the ranks of manual traders to dwindle at an increasing speed. Now, more than half of the deals are made by trading algorithms, and it is worth to say that MetaTrader 5 is number one among the most convenient terminals for this.

But despite all the advantages of this platform, it has a number of drawbacks I tried to mitigate with the application described here. The article describes developing the program written entirely in MQL5 using the EasyAndFastGUI library designed to improve selection of trading algorithm optimization parameters. It also adds new features to the analysis of retrospective trading and general EA assessment.

First, optimization of EAs takes quite a long time. Of course, this is due to the fact that the tester generates ticks in a more high-quality manner (even when OHLC is selected, four ticks are generated for each candle), as well as other additions that allow for better EA evaluation. However, on home PCs that are not so powerful, optimization can take several days or weeks. It often happens that after choosing the EA parameters, we soon realize that they are incorrect, and there is nothing at hand besides optimization passes statistics and a few evaluation ratios.

It would be nice to have a full-fledged statistics per each optimization pass and filtration ability (including conditional filters) for each of them by multiple parameters. It would also be good to compare trading statistics with the Buy And Hold strategy and impose all statistics on each other. In addition, it is sometimes necessary to upload all the trading history data to a file for the subsequent processing of results of each deal.

Sometimes, we may also want to see what kind of slippage the algorithm is able to withstand and how the algorithm behaves on a certain time interval, since some strategies depend on the market type. A flat-based strategy can serve as an example. It loses during trend periods and makes profit during flat ones. It would also be good to view certain intervals (by dates) as a complete set of ratios and other additions (rather than simply on a price chart) separately from the general PL graph.

We should also pay attention to forward tests. They are very informative, but their graphs are displayed as a continuation of the previous one in the strategy tester's standard report. Novice traders may easily conclude that their robot sharply lost all profits and then started to recover (or worse — went negative). In the program described here, all data are reviewed in terms of optimization type (either forward, or history one).

It is also important to mention Grails many EA developers are so fond of searching for. Some robots make 1000% or more per month. It may seem that they outrun the market (Buy and Hold strategy), but in real practice, everything looks quite different. As the described program shows, these robots can really make 1000%, but they do not outrun the market.

The program features separation of an analysis between trading using a robot with a full lot (increasing/reducing it, etc…), as well as imitation of a trading by the robot using a single lot (minimum lot available for trading). When building the Buy and Hold trading graph, the described program considers lot management performed by the robot (i.e. it purchases some more asset when a lot is increased and reduces the amount of a purchased asset when a lot is decreased). If we compare these two graphs, it turns out that my test robot, which showed unrealistic results in one of its best optimization passes, could not outrun the market. Therefore, for more objective assessment of trading strategies, we should have a look at the one-lot trading graph, in which both the robot's and the Buy and Hold strategy's PL are displayed as if trading with the least allowable trading volume (PL= Profit/Loss — graph of obtained profit by time).

Now, let's have a more detailed look at how the program was developed.

Optimization analyzer structure

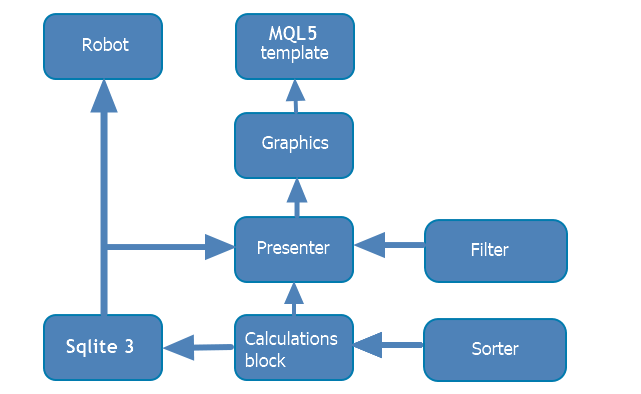

The program structure can be graphically expressed as follows:

The resulting optimization analyzer is not tied to any particular robot and is not part of it. However, due to the specifics of building graphical interfaces in MQL5, the MQL5 EA development template was used as the program's basis. Since the program turned out to be quite large (several thousands lines of code), for more specificity and consistency, it was divided into a number of blocks (displayed on the diagram above) that were in turn divided into classes. The robot template is only the starting point for launching the application. Each of the blocks will be considered in more details below. Here we will describe the relationships between them. To work with the application, we will need:

- The trading algorithm

- Dll Sqlite3

- The graphical interface library mentioned above with necessary edits (described in the graphics block below)

The robot itself can be developed in any way you like (using OOP, a function inside the robot template, imported from Dll…). Most importantly, it should apply the robot development template provided by MQL5 Wizard. It connects one file from the database block where the class uploading required data to the database after each optimization pass is located. This part is independent and does not depend on the application itself, since the database is formed when launching the robot in the strategy tester.

The calculation block is an improved continuation of my previous article "Custom presentation of trading history and creation of report diagrams".

Database and calculation block are used both in the analyzed robot and in the described application. Therefore, they are placed into the Include directory. These blocks perform the bulk of the work and are connected to the graphical interface via the presenter class.

Presenter class connects separate program blocks. Each of the blocks has its own function in the graphical interface. It handles button pressing and other events, as well as redirects to other logical blocks. The data obtained from them are returned to the presenter, where they are processed and the appropriate graphs are plotted, tables are filled, and other interaction with the graphic part takes place.

The graphical part of the program does not perform any conceptual logic. Instead, it only builds a window with the required interface and calls the appropriate presenter functions during the button pressing events.

The program itself is written as the MQL5 project allowing you to develop it in a more structured way and put all the required files with code in one place. The project features yet another class that will be described in the calculation block. This class was written specifically for this program. It sorts optimization passes using the method I developed. In fact, it serves the entire "Optimisation selection" tab reducing data sampling by certain criteria.

Universal sorting class is an independent addition to the program. It dies not fit into any of the blocks, but it still remains an important part of the program. Therefore, we briefly consider it in this part of the article.

As the name implies, the class deals with data sorting. Its algorithm was taken from a third-party website — Selection sort (in Russian).

//+------------------------------------------------------------------+ //| E-num with a sorting style | //+------------------------------------------------------------------+ enum SortMethod { Sort_Ascending,// Ascending Sort_Descendingly// Descending }; //+------------------------------------------------------------------+ //| Class sorting the passed data type | //+------------------------------------------------------------------+ class CGenericSorter { public: // Default constructor CGenericSorter(){method=Sort_Descendingly;} // Sorting method template<typename T> void Sort(T &out[],ICustomComparer<T>*comparer); // Select sorting type void Method(SortMethod _method){method=_method;} // Get sorting method SortMethod Method(){return method;} private: // Sorting method SortMethod method; };

The class contains the template Sort method, which sorts the data. The template method allows sorting any passed data, including classes and structures. The data comparison method should be described in a separate class that implements the IСustomComparer<T> interface. I had to develop my own interface of IСomparer type only because in the conventional IСomparer interface of the Compare method, comprised data are not passed by reference, while passing by reference is one of the conditions of passing structures to a method in MQL5 language.

CGenericSorter::Method class method overloads return and accept data sorting type (in ascending or descending order). This class is used in all blocks of the program where the data are sorted.

Graphics

| Warning!

When developing the graphical interface, a bug was detected in the applied library (EasyAndFastGUI) — the ComboBox graphical element cleared some variables incompletely during its refilling. According to the recommendations (in Russian) of the library developer, the following changes should be made to fix this: m_item_index_focus =WRONG_VALUE; to the method CListView::Clear(const bool redraw=false). The method is located on the 600 th string of the ListView.mqh file. The file's path: |

|---|

To create a window in MQL5 based on the EasyAndFastGUI library, a class is required that will serve as a container for all subsequent window filling. The class should be derived from the CwindEvents class. The methods should be redefined inside the class:

//--- Initialization/deinitialization void OnDeinitEvent(const int reason){CWndEvents::Destroy();}; //--- Chart event handler virtual void OnEvent(const int id,const long &lparam,const double &dparam,const string &sparam);//

The blank for creating the window should be as follows:

class CWindowManager : public CWndEvents { public: CWindowManager(void){presenter = NULL;}; ~CWindowManager(void){}; //=============================================================================== // Calling methods and events : //=============================================================================== //--- Initialization/deinitialization void OnDeinitEvent(const int reason){CWndEvents::Destroy();}; //--- Chart event handler virtual void OnEvent(const int id,const long &lparam,const double &dparam,const string &sparam); //--- Create the program's graphical interface bool CreateGUI(void); private: //--- Main window CWindow m_window; }

The window itself is created with the Cwindow type inside the class. However, a number of window properties should be defined before displaying the window. In this particular case, the window creation method looks as follows:

bool CWindowManager::CreateWindow(const string text) { //--- Add the window pointer to the window array CWndContainer::AddWindow(m_window); //--- Coordinates int x=(m_window.X()>0) ? m_window.X() : 1; int y=(m_window.Y()>0) ? m_window.Y() : 1; //--- Properties m_window.XSize(WINDOW_X_SIZE+25); m_window.YSize(WINDOW_Y_SIZE); m_window.Alpha(200); m_window.IconXGap(3); m_window.IconYGap(2); m_window.IsMovable(true); m_window.ResizeMode(false); m_window.CloseButtonIsUsed(true); m_window.FullscreenButtonIsUsed(false); m_window.CollapseButtonIsUsed(true); m_window.TooltipsButtonIsUsed(false); m_window.RollUpSubwindowMode(true,true); m_window.TransparentOnlyCaption(true); //--- Set tooltips m_window.GetCloseButtonPointer().Tooltip("Close"); m_window.GetFullscreenButtonPointer().Tooltip("Fullscreen/Minimize"); m_window.GetCollapseButtonPointer().Tooltip("Collapse/Expand"); m_window.GetTooltipButtonPointer().Tooltip("Tooltips"); //--- Create the form if(!m_window.CreateWindow(m_chart_id,m_subwin,text,x,y)) return(false); //--- return(true); }

The prerequisites for this method are the string that adds the window to the array of application windows and creating the form. Later, when the application is running and the OnEvent event is triggered, one of the library methods runs in a loop over all the windows listed in the array of windows. Then it goes over all the elements inside the window and looks for an event related to clicking on any management interface or highlighting a table row, etc. Therefore, when creating each new application window, a reference should be added to that window in the reference array.

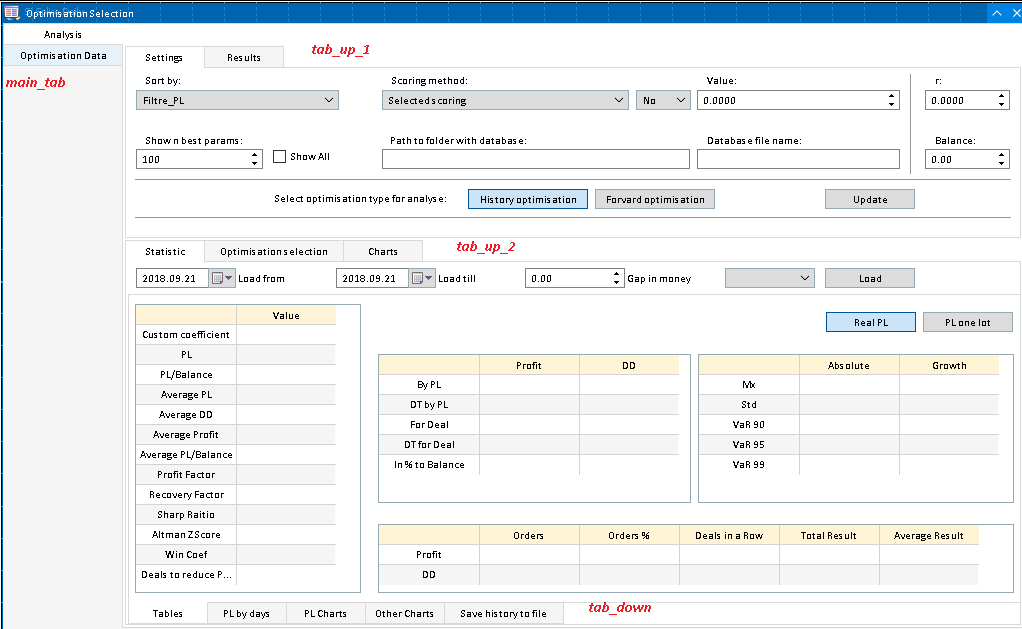

The developed application featues the interface divided by tabs. There are 4 tab containers:

//--- Tabs CTabs main_tab; // Main tabs CTabs tab_up_1; // Tabs with settings and results table CTabs tab_up_2; // Tabs with statistics and selection of parameters, as well as common graphs CTabs tab_down; // Tabs with statistics and uploading to a file

They look as follows on the form (signed in red on the screenshot):

- main_tab divides the table with all selected optimization passes ("Optimisation Data") from the rest of the program interface. This table contains all the results that satisfy the filter conditions on the settings tab. The results are then sorted by the ratio selected in ComboBox — Sort by. The obtained data are transferred to the described table in the sorted form. The tab with the rest of the program interface contains another 3 Tab containers.

- tab_up_1 contains a division into the initial settings of the program and the table with the sorted results. In addition to the mentioned conditional filters, the Settings tab serves for selecting the database and entering additional data. For example, you can select whether to enter all data already added to the Optimisation Data tab of the table to the data selection results table, or only a certain number of the best parameters (filtering in descending order by selected ratio) will be sufficient.

- tab_up_2 contains 3 tabs. Each of them contains the interface performing three different types of tasks. The first tab contains the full report on a selected optimization pass and allows simulating slippage, as well as considering trading history for a certain time period. The second one serves as the filter for optimization passes and helps define the strategy sensitivity to different parameters and narrow down the number of optimization results by selecting the most adequate intervals of the parameters of interest. The last tab serves as a graphical representation of the optimization results table and shows the total number of selected optimization parameters.

- tab_down features five tabs, four of which is presentation of an EA's trading report during optimization with selected parameters, while the last tab is uploading data to a file. The first tab presents a table with estimated ratios. The second tab provides profit/loss distribution by trading days. The third tab represents profit and loss graph imposed on the Buy and Hold strategy (black graph), while the fourth tab represents changes in some selected ratios over time, as well as some additional interesting and informative types of graphs that can be obtained by analyzing the EA trading results.

The process of creating tabs is similar — the only difference is the content. As an example, I will provide the method of creating the main tab:

//+------------------------------------------------------------------+ //| Main Tab | //+------------------------------------------------------------------+ bool CWindowManager::CreateTab_main(const int x_gap,const int y_gap) { //--- Save the pointer to the main element main_tab.MainPointer(m_window); //--- Array of tab width int tabs_width[TAB_MAIN_TOTAL]; ::ArrayInitialize(tabs_width,45); tabs_width[0]=120; tabs_width[1]=120; //--- string tabs_names[TAB_UP_1_TOTAL]={"Analysis","Optimisation Data"}; //--- Properties main_tab.XSize(WINDOW_X_SIZE-23); main_tab.YSize(WINDOW_Y_SIZE); main_tab.TabsYSize(TABS_Y_SIZE); main_tab.IsCenterText(true); main_tab.PositionMode(TABS_LEFT); main_tab.AutoXResizeMode(true); main_tab.AutoYResizeMode(true); main_tab.AutoXResizeRightOffset(3); main_tab.AutoYResizeBottomOffset(3); //--- main_tab.SelectedTab((main_tab.SelectedTab()==WRONG_VALUE)? 0 : main_tab.SelectedTab()); //--- Add tabs with specified properties for(int i=0; i<TAB_MAIN_TOTAL; i++) main_tab.AddTab((tabs_names[i]!="")? tabs_names[i]: "Tab "+string(i+1),tabs_width[i]); //--- Create a control element if(!main_tab.CreateTabs(x_gap,y_gap)) return(false); //--- Add an object to the common array of object groups CWndContainer::AddToElementsArray(0,main_tab); return(true); }

In addition to content that may vary, the main code strings are as follows:

- Adding a pointer to the main element — the tab container should know the element it is assigned to

- Control element creation string

- Adding an element to the general list of controls.

The control elements are next according to the hierarchy. 11 control element types were used in the application. They are all created in a similar manner, therefore the methods adding the control elements have been written to create each of them. Let's consider the implementation of only one of them:

bool CWindowManager::CreateLable(const string text, const int x_gap, const int y_gap, CTabs &tab_link, CTextLabel &lable_link, int tabIndex, int lable_x_size) { //--- Save the pointer to the main element lable_link.MainPointer(tab_link); //--- Assign to the tab tab_link.AddToElementsArray(tabIndex,lable_link); //--- Settings lable_link.XSize(lable_x_size); //--- Creating if(!lable_link.CreateTextLabel(text,x_gap,y_gap)) return false; //--- Add an object to the general object groups array CWndContainer::AddToElementsArray(0,lable_link); return true; }

The passed control element (CTextLabel), together with the tabs, should remember the element it is assigned to as a container. In turn, the tab container remembers the tab the element is located at. After that, the element is filled with required settings and initial data. Eventually, the object is added to the general array of objects.

Similar to labels, other elements defined inside the class container as fields are added. I separated certain elements and placed some of them to the 'protected' class area. These are the elements that do not require access via the presenter. Some other elements were placed to 'public'. These are the elements defining some conditions or radio buttons, the state of which should be checked from the presenter. In other words, all elements and methods, access to which is not desirable, have their headers in the 'protected' or 'private' parts of the class together with the reference to the presenter. Adding the presenter reference is made in the form of a public method where the presence of an already added presenter is checked first, and if the reference to it has not been added yet, the presenter is saved. This is done to avoid dynamic presenter substitution during the program execution.

The window itself is created in the CreateGUI method:

bool CWindowManager::CreateGUI(void) { //--- Create window if(!CreateWindow("Optimisation Selection")) return(false); //--- Create tabs if(!CreateTab_main(120,20)) return false; if(!CreateTab_up_1(3,44)) return(false); int indent=WINDOW_Y_SIZE-(TAB_UP_1_BOTTOM_OFFSET+TABS_Y_SIZE-TABS_Y_SIZE); if(!CreateTab_up_2(3,indent)) return(false); if(!CreateTab_down(3,33)) return false; //--- Create controls if(!Create_all_lables()) return false; if(!Create_all_buttons()) return false; if(!Create_all_comboBoxies()) return false; if(!Create_all_dropCalendars()) return false; if(!Create_all_textEdits()) return false; if(!Create_all_textBoxies()) return false; if(!Create_all_tables()) return false; if(!Create_all_radioButtons()) return false; if(!Create_all_SepLines()) return false; if(!Create_all_Charts()) return false; if(!Create_all_CheckBoxies()) return false; // Show window CWndEvents::CompletedGUI(); return(true); }

As can be seen from its implementation, it does not directly create any control element itself, but only calls other methods for creating these elements. The main code string that should be included as a final one in this method is CWndEvents::CompletedGUI();

This string completes graphics creation and plots it on a user's screen. Creation of each control element (be it separation lines, labels or buttons) is implemented into methods having a similar content and applying the above mentioned approaches to creating graphical control elements. The method headers can be found in the 'private' part of the class:

//=============================================================================== // Controls creation: //=============================================================================== //--- All Labels bool Create_all_lables(); bool Create_all_buttons(); bool Create_all_comboBoxies(); bool Create_all_dropCalendars(); bool Create_all_textEdits(); bool Create_all_textBoxies(); bool Create_all_tables(); bool Create_all_radioButtons(); bool Create_all_SepLines(); bool Create_all_Charts(); bool Create_all_CheckBoxies();

Talking about graphics, it is impossible to skip the event model part. For correct processing in graphic applications developed using EasyAndFastGUI, you will need to perform the following steps:

Create the event handler method (for example, button pressing). This method should accept 'id' and 'lparam' as parameters. The first parameter indicates the type of a graphical event, while the second indicates ID of an object the interaction took place with. Implementation of the methods is similar in all cases:

//+------------------------------------------------------------------+ //| Btn_Update_Click | //+------------------------------------------------------------------+ void CWindowManager::Btn_Update_Click(const int id,const long &lparam) { if(id==CHARTEVENT_CUSTOM+ON_CLICK_BUTTON && lparam==Btn_update.Id()) { presenter.Btn_Update_Click(); } }

First, check the condition (whether the button was pressed or the list element was selected…). Next, check lparam where ID passed to the method is compared to ID of the required list element.

All button pressing event declarations are located in the 'private' part of the class. The event should be called to obtain a respond to it. Declared events are called in the overloaded OnEvent method:

//+------------------------------------------------------------------+ //| OnEvent | //+------------------------------------------------------------------+ void CWindowManager::OnEvent(const int id,const long &lparam,const double &dparam,const string &sparam) { Btn_Update_Click(id,lparam); Btn_Load_Click(id,lparam); OptimisationData_inMainTable_selected(id,lparam); OptimisationData_inResults_selected(id,lparam); Update_PLByDays(id,lparam); RealPL_pressed(id,lparam); OneLotPL_pressed(id,lparam); CoverPL_pressed(id,lparam); RealPL_pressed_2(id,lparam); OneLotPL_pressed_2(id,lparam); RealPL_pressed_4(id,lparam); OneLotPL_pressed_4(id,lparam); SelectHistogrameType(id,lparam); SaveToFile_Click(id,lparam); Deals_passed(id,lparam); BuyAndHold_passed(id,lparam); Optimisation_passed(id,lparam); OptimisationParam_selected(id,lparam); isCover_clicked(id,lparam); ChartFlag(id,lparam); show_FriquencyChart(id,lparam); FriquencyChart_click(id,lparam); Filtre_click(id,lparam); Reset_click(id,lparam); RealPL_pressed_3(id,lparam); OneLotPL_pressed_3(id,lparam); ShowAll_Click(id,lparam); DaySelect(id,lparam); }

The method, in turn, is called from the robot template. Thus, the event model stretches from the robot template (provided below) to the graphical interface. GUI performs all processing, sorting out and redirection for subsequent handling in the presenter. The robot template itself is a starting point of the program. It looks as follows:

#include "Presenter.mqh" CWindowManager _window; CPresenter Presenter(&_window); //+------------------------------------------------------------------+ //| Expert initialization function | //+------------------------------------------------------------------+ int OnInit() { //--- if(!_window.CreateGUI()) { Print(__FUNCTION__," > Failed to create the graphical interface!"); return(INIT_FAILED); } //--- return(INIT_SUCCEEDED); } //+------------------------------------------------------------------+ //| Expert deinitialization function | //+------------------------------------------------------------------+ void OnDeinit(const int reason) { //--- _window.OnDeinitEvent(reason); } //+------------------------------------------------------------------+ //| | //+------------------------------------------------------------------+ void OnChartEvent(const int id, const long &lparam, const double &dparam, const string &sparam) { _window.ChartEvent(id,lparam,dparam,sparam); } //+------------------------------------------------------------------+

Working with the database

Before considering this rather extensive part of the project, it is worth saying a few words regarding the choice made. One of the initial project objectives was to provide ability to work with optimization results after completing the optimization itself, as well as availability of these results at any time. Saving data to a file was immediately discarded as unsuitable. It would require creation of multiple tables (forming, in fact, a single large table, but with a different number of rows) or files.

Neither is very convenient. Besides, the method is more difficult to implement. The second method is creating optimization frames. The toolkit itself is good but we are not going to work with optimizations during the optimization process. Besides, the frames functionality is not as good as the database one. In addition, frames are designed for MetaTrader, while the database can be used in any third-party analytical program if required.

Selecting the right database was easy enough. We needed a fast and popular database that would be convenient to link up with and not requiring any additional software. Sqlite database meets all that criteria. The mentioned characteristics make it so popular. To use it, connect databases supplied by the provider to the Dll project. Dll data are written in C and are easily linked up with MQL5 applications, which is a nice addition since you do not have to write a single code line in a third-party language complicating the project. Among the disadvantages of this approach is that Dll Sqlite does not provide a convenient API for working with the database, and therefore it is required to describe at least the minimum wrapper for working with the database. An example of writing this functionality was efficiently presented in the article "SQL and MQL5: Working with SQLite database". For this project, a part of the code related to interaction with WinApi and importing some functions from dll to MQL5 from the mentioned article was used. As for the wrapper, I decided to write it myself.

As a result, the database handling block consists of the Sqlite3 folder, where a convenient wrapper for working with the database is described, and the OptimisationSelector folder created specifically for the developed program. Both folders are located in the MQL5/Include directory. As mentioned earlier, a number of functions of the Windows standard library are used for working with the database. All functions of this part of the application are located in the WinApi directory. In addition to the mentioned borrowings, I also used the code for creating a shared resource (Mutex) from CodeBase. When working with the database from two sources (namely, if the optimization analyzer opens the database used during the optimization), data obtained by the program should always be complete. This is why a shared resource is required. It turns out that if one of the sides (optimization process or analyzer) activates the database, the second one waits till its counterpart completes its work. Sqlite database allows reading it from several threads. Due to the subject matter of the article, we will not consider in detail the resulting wrapper for working with the sqlite3 database from MQL5. Instead, we only describe some points of its implementation and application methods. As already mentioned, the wrapper of working with the database is located in the Sqlite3 folder. There are three files in it. Let's go over them in writing order.

- The first thing we need is to import the necessary functions for working with the database from the Dll. Since the goal was to create a wrapper containing the minimum required functionality, I did not import even 1% of the total number of functions provided by the database developers. All required functions are imported in the sqlite_amalgmation.mqh file. These functions are well commented on the developer’s website, and are also labeled in the above file. If desired, you can import the entire header file the same way. The result will be a complete list of all functions and, accordingly, the ability to access them. The list of the imported functions is as follows:

#import "Sqlite3_32.dll" int sqlite3_open(const uchar &filename[],sqlite3_p32 &paDb);// Open the database int sqlite3_close(sqlite3_p32 aDb); // Close the database int sqlite3_finalize(sqlite3_stmt_p32 pStmt);// Complete the statement int sqlite3_reset(sqlite3_stmt_p32 pStmt); // Reset the statement int sqlite3_step(sqlite3_stmt_p32 pStmt); // Move to the next line when reading the statement int sqlite3_column_count(sqlite3_stmt_p32 pStmt); // Calculate the number of columns int sqlite3_column_type(sqlite3_stmt_p32 pStmt,int iCol); // Get the type of the selected column int sqlite3_column_int(sqlite3_stmt_p32 pStmt,int iCol);// Convert the value into int long sqlite3_column_int64(sqlite3_stmt_p32 pStmt,int iCol); // Convert the value into int64 double sqlite3_column_double(sqlite3_stmt_p32 pStmt,int iCol); // Convert the value into double const PTR32 sqlite3_column_text(sqlite3_stmt_p32 pStmt,int iCol);// Get the text value int sqlite3_column_bytes(sqlite3_stmt_p32 apstmt,int iCol); // Get the number of bytes occupied by the line from the passed cell int sqlite3_bind_int64(sqlite3_stmt_p32 apstmt,int icol,long a);// Combine the request having a value (of int64 type) int sqlite3_bind_double(sqlite3_stmt_p32 apstmt,int icol,double a);// Combine the request having a value (of double type) int sqlite3_bind_text(sqlite3_stmt_p32 apstmt,int icol,char &a[],int len,PTRPTR32 destr);// Combine the request having a value (string type (char* - in C++)) int sqlite3_prepare_v2(sqlite3_p32 db,const uchar &zSql[],int nByte,PTRPTR32 &ppStmt,PTRPTR32 &pzTail);// Prepare a request int sqlite3_exec(sqlite3_p32 aDb,const char &sql[],PTR32 acallback,PTR32 avoid,PTRPTR32 &errmsg);// Sql execution int sqlite3_open_v2(const uchar &filename[],sqlite3_p32 &ppDb,int flags,const char &zVfs[]); // Open the database with parameters #import

Databases provided by the developers should be placed to the Libraries folder and named Sqlite3_32.dll and Sqlite3_64.dll according to their bit count for the dll database wrapper to work. You can take Dll data from the files attached to the article, compile them on your own from Sqlite Amalgmation or take them from the Sqlite developers' website. Their presence is a prerequisite for the program. You also need to allow the EA to import Dll.

- The second thing is to write a functional wrapper for connecting to the database. This should be a class that creates a connection to the database and releases it (disconnects from the database) in the destructor. Also, it should be able to execute simple string Sql commands, manage transactions and create queries (statements). All the described functionality was implemented in the CsqliteManager class — it is from its creation that the process of interacting with the database starts.

//+------------------------------------------------------------------+ //| Database connection and management class | //+------------------------------------------------------------------+ class CSqliteManager { public: CSqliteManager(){db=NULL;} // Empty constructor CSqliteManager(string dbName); // Pass the name CSqliteManager(string dbName,int flags,string zVfs); // Pass the name and connection flags CSqliteManager(CSqliteManager &other) { db=other.db; } // Copying constructor ~CSqliteManager(){Disconnect();};// Destructor void Disconnect(); // Disconnect from the database bool Connect(string dbName,int flags,string zVfs); // Parametric connection to the database bool Connect(string dbName); // Connect to the database by name void operator=(CSqliteManager &other){db=other.db;}// Assignment operator sqlite3_p64 DB() { return db; }; // Get the pointer to the database sqlite3_stmt_p64 Create_statement(const string sql); // Create the statement bool Execute(string sql); // Execute the command void Execute(string sql,int &result_code,string &errMsg); // Execute the command, and provide the error code and message void BeginTransaction(); // Transaction start void RollbackTransaction(); // Transaction roll-back void CommitTransaction(); // Confirm a transaction private: sqlite3_p64 db; // Database void stringToUtf8(const string strToConvert,// String to be converted into an array in utf-8 encoding uchar &utf8[],// Array in utf-8 encoding the converted strToConvert string is to be placed to const bool untilTerminator=true) { // Number of symbols converted to utf-8 encoding and to be copied to the utf-8 array //--- int count=untilTerminator ? -1 : StringLen(strToConvert); StringToCharArray(strToConvert,utf8,0,count,CP_UTF8); } };

As can be seen from the code, the resulting class has the ability to create two types of connections in the database (textual and specifying parameters). The Create_sttement method forms a request to the database and returns a pointer to it. Exequte method overloads perform simple string queries, while transaction methods create and accept/cancel transactions. Connection to the database itself is stored in the db variable. If we applied Disconnect method or just created the class using the default constructor (did not have time to connect to the database yet), the variable is NULL. When repeatedly calling the Connect method, we disconnect from the previously connected database and connect to the new one. Since connecting to the database requires passing of a string in the UTF-8 format, the class has a special 'private' method that converts the string to the required data format.

- The next task is creating a wrapper for convenient work with queries (statement). A request to the database should be created and destroyed. A request is created by CsqliteManager, while the memory is not managed by anything. In other words, after creating a request, it needs to be destroyed when it is no longer required, otherwise it will not allow to disconnect from the database, and when trying to complete the work with the database, we will get an exception indicating that the database is busy. Also, a statement wrapper class should be able to fill the request with passed parameters (when it is formed as "INSERT INTO table_1 VALUES(@ID,@Param_1,@Param_2);"). In addition, a given class should be able to execute the query placed in it (Exequte method).

typedef bool(*statement_callback)(sqlite3_stmt_p64); // call-back performed when executing a query. If successful, a 'true' is performed //+------------------------------------------------------------------+ //| Class of a query to the database | //+------------------------------------------------------------------+ class CStatement { public: CStatement(){stmt=NULL;} // empty constructor CStatement(sqlite3_stmt_p64 _stmt){this.stmt=_stmt;} // Constructor with the parameter - pointer to the statement ~CStatement(void){if(stmt!=NULL)Sqlite3_finalize(stmt);} // Destructor sqlite3_stmt_p64 get(){return stmt;} // Get pointer to statement void set(sqlite3_stmt_p64 _stmt); // Set pointer to statement bool Execute(statement_callback callback=NULL); // Execute statement bool Parameter(int index,const long value); // Add the parameter bool Parameter(int index,const double value); // Add the parameter bool Parameter(int index,const string value); // Add the parameter private: sqlite3_stmt_p64 stmt; };

Parameter method overloads fill the request parameters. The 'set' method saves the passed statement to the 'stmt' variable: if it is found out that an old request has alrady been saved in the class before saving the new one, the Sqlite3_finalize method is called for the previously saved request.

- The concluding class in the database handling wrapper is CSqliteReader able to read a response from the database. Similar to previous classes, the class calls the sqlite3_reset method in its destructor — it drops the request and allows you to work with it again. In the new versions of the database, calling this function is not necessary, but it has been left by the developers. I have used it in the wrapper just in case. Also this class should fulfill its main duties, namely, reading a response from the database string by string with the possibility of converting the read data into the appropriate format.

//+------------------------------------------------------------------+ //| Class reading responses from databases | //+------------------------------------------------------------------+ class CSqliteReader { public: CSqliteReader(){statement=NULL;} // empty constructor CSqliteReader(sqlite3_stmt_p64 _statement) { this.statement=_statement; }; // Constructor accepting the pointer to the statement CSqliteReader(CSqliteReader &other) : statement(other.statement) {} // Copying constructor ~CSqliteReader() { Sqlite3_reset(statement); } // Destructor void set(sqlite3_stmt_p64 _statement); // Add a reference to the statement void operator=(CSqliteReader &other){statement=other.statement;}// Reader assignment operator void operator=(sqlite3_stmt_p64 _statement) {set(_statement);}// Statement assignment operator bool Read(); // Read the string int FieldsCount(); // Count the number of columns int ColumnType(int col); // Get the column type bool IsNull(int col); // Check if the value == SQLITE_NULL long GetInt64(int col); // Convert into 'int' double GetDouble(int col);// Convert into 'double' string GetText(int col);// Convert into 'string' private: sqlite3_stmt_p64 statement; // pointer to the statement };

Now that we have implemented the described classes using the functions for working with the database uploaded from Sqlite3.dll, it is time to describe the classes working with the database from the described program.

The structure of the created database is as follows:

Buy And Hold table:

- Time — X axis (time interval label)

- PL_total — profit/loss if we increase a lot in proportion to the robot

- PL_oneLot — profit/loss if trading a single lot constantly

- DD_total — drawdown if trading a lot the same way the EA traded

- DD_oneLot — drawdown if trading a single lot

- isForvard — forward graph property

OptimisationParams table:

- ID — unique auto-filling entry index in the database

- HistoryBorder — history optimization completion date

- TF — timeframe

- Param_1...Param_n — parameter

- InitalBalance — initial balance size

ParamsCoefitients table:

- ID — external key, reference to OptimisationParams(ID)

- isForvard — forward optimization property

- isOneLot — property of the chart the ratio was based on

- DD — drawdown

- averagePL — average profit/loss by PL graph

- averageDD — average drawdown

- averageProfit — average profit

- profitFactor — profit factor

- recoveryFactor — recovery factor

- sharpRatio — Sharpe ratio

- altman_Z_Score — Altman Z score

- VaR_absolute_90 — VaR 90

- VaR_absolute_95 — VaR 95

- VaR_absolute_99 — VaR 99

- VaR_growth_90 — VaR 90

- VaR_growth_95 — VaR 95

- VaR_growth_99 — VaR 99

- winCoef — win ratio

- customCoef — custom ratio

ParamType table:

- ParamName — robot parameter name

- ParamType — robot parameter type (int/double/string)

TradingHistory table

- ID — external key reference to OptimisationParams(ID)

- isForvard — forward test flag

- Symbol — symbol

- DT_open — open date

- Day_open — open day

- DT_close — close date

- Day_close — close day

- Volume — number of lots

- isLong — long/short property

- Price_in — entry price

- Price_out — exit price

- PL_oneLot — profit when trading a single lot

- PL_forDeal — profit when trading as we did previously

- OpenComment — entry comment

- CloseComment — exit comment

Based on the provided database structure, we can see that some tables use the external key to refer to the OptimisationParams table where we store the EA parameters. Each column of an input parameter bears its name (for example, Fast/Slow — fast/slow moving average). Also, each column should have a specific data format. Many Sqlite databases are created without defining the table column data format. In this case, all data are stored as lines. However, we need to know the exact data format, since we should sort out ratios by a certain property, which means conversion of the data uploaded from the database to its original format.

To do this, we should know their format before entering the data into the database. Several options are possible: creating a template method and transfer converter into it or creating a class, which, in fact, is a universal storage of several data types (any data type can be converted to) combined with the name of the EA variable. I seleced the second option and created the CDataKeeper class. The described class can store 3 data types [int, double, string], while all other data types that can be used as the EA input formats can be converted to them one way or another.

//+------------------------------------------------------------------+ //| Types of input data of the EA parameter | //+------------------------------------------------------------------+ enum DataTypes { Type_INTEGER,// int Type_REAL,// double, float Type_Text // string }; //+------------------------------------------------------------------+ //| Result of comparing two CDataKeeper | //+------------------------------------------------------------------+ enum CoefCompareResult { Coef_Different,// different data types or variable names Coef_Equal,// variables are equal Coef_Less, // current variable is less than passed one Coef_More // current variable exceeds the passed one }; //+---------------------------------------------------------------------+ //| Class storing one specific robot input. | //| It can store the data of the following types: [int, double, string] | //+---------------------------------------------------------------------+ class CDataKeeper { public: CDataKeeper(); // Constructor CDataKeeper(const CDataKeeper&other); // Copying constructor CDataKeeper(string _variable_name,int _value); // Parametric constructor CDataKeeper(string _variable_name,double _value); // Parametric constructor CDataKeeper(string _variable_name,string _value); // Parametric constructor CoefCompareResult Compare(CDataKeeper &data); // Comparison method DataTypes getType(){return variable_type;}; // Get the data type string getName(){return variable_name;}; // Get the parameter name string valueString(){return value_string;}; // Get the parameter int valueInteger(){return value_int;}; // Get the parameter double valueDouble(){return value_double;}; // Get the parameter string ToString(); // Convert any parameter into string. If this is a string parameter, single quotes are added to the string from both sides <<'>> private: string variable_name,value_string; // variable name and string variable int value_int; // Int variable double value_double; // Double variable DataTypes variable_type; // Variable type int compareDouble(double x,double y) // Comparing Double types accurate up to 10 decimal places { double diff=NormalizeDouble(x-y,10); if(diff>0) return 1; else if(diff<0) return -1; else return 0; } };

Three constructor overloads accept the variable name as the first parameter, while the value converted to one of the mentioned types is accepted as the second one. These values are saved in class global variables starting with 'value_' followed by a type indication. The getType() method returns the type as an enumeration provided above, while the getName() method returns the variable name. Methods starting with 'value' return the variable of the required type, but if the valueDouble() method is called, while the variable stored in the class is of 'int' type, NULL is returned. The ToString() method converts the value of any of the variables to the string format. However, if the variable was a string initially, the single quotes are added to it (to form SQL requests more conveniently). The Compare(CDataKeeper &ther) method allows comparing two objects of the CDataKeeper type, while comparing:

- EA variable name

- Variable type

- Variable value

If the first two comparisons do not pass, then we are trying to compare two different parameters (for example, the period of the fast moving average with the period of the slow one), and accordingly, we cannot do this because we only need to compare data of the same type. Therefore, we return the Coef_Different value of the CoefCompareResult type. In other cases, a comparison is made and a required result is returned. The comparison method itself is implemented as follows:

//+------------------------------------------------------------------+ //| Compare the current parameter with the passed one | //+------------------------------------------------------------------+ CoefCompareResult CDataKeeper::Compare(CDataKeeper &data) { CoefCompareResult ans=Coef_Different; if(StringCompare(this. variable_name,data.getName())==0 && this.variable_type==data.getType()) // Compare names and types { switch(this.variable_type) // Compare values { case Type_INTEGER : ans=(this.value_int==data.valueInteger() ? Coef_Equal :(this.value_int>data.valueInteger() ? Coef_More : Coef_Less)); break; case Type_REAL : ans=(compareDouble(this.value_double,data.valueDouble())==0 ? Coef_Equal :(compareDouble(this.value_double,data.valueDouble())>0 ? Coef_More : Coef_Less)); break; case Type_Text : ans=(StringCompare(this.value_string,data.valueString())==0 ? Coef_Equal :(StringCompare(this.value_string,data.valueString())>0 ? Coef_More : Coef_Less)); break; } } return ans; }

The type-independent representation of variables allows using them in a more convenient form, taking into account both the name, the data type of the variable and its value.

The next task is creating the database described above. The CDatabaseWriter class is used for that.

//+---------------------------------------------------------------------------------+ //| Call-back calculating a user ratio | //| History data and flag of the history type the ratio calculation is required for | //| are passed to the input | //+---------------------------------------------------------------------------------+ typedef double(*customScoring_1)(const DealDetales &history[],bool isOneLot); //+---------------------------------------------------------------------------------+ //| Call-back calculating a user ratio | //| Connection to the database (read only), history and requested ratio type flag | //| are passed to the input | //+---------------------------------------------------------------------------------+ typedef double(*customScoring_2)(CSqliteManager *dbManager,const DealDetales &history[],bool isOneLot); //+---------------------------------------------------------------------------------+ //| Class saving the data in the database and creating the database before that | //+---------------------------------------------------------------------------------+ class CDBWriter { public: // Call one of resets to OnInit void OnInitEvent(const string DBPath,const CDataKeeper &inputData_array[],customScoring_1 scoringFunction,double r,ENUM_TIMEFRAMES TF=PERIOD_CURRENT); // call-back 1 void OnInitEvent(const string DBPath,const CDataKeeper &inputData_array[],customScoring_2 scoringFunction,double r,ENUM_TIMEFRAMES TF=PERIOD_CURRENT); // call-back 2 void OnInitEvent(const string DBPath,const CDataKeeper &inputData_array[],double r,ENUM_TIMEFRAMES TF=PERIOD_CURRENT);// No call-back and no user ratio (equal to zero) double OnTesterEvent();// Call in OnTester void OnTickEvent();// Call in OnTick private: CSqliteManager dbManager; // Connector to the database CDataKeeper coef_array[]; // Input parameters datetime DT_Border; // The last candle date (calculated in OnTickEvent) double r; // Risk free rate customScoring_1 scoring_1; // Call-back customScoring_2 scoring_2; // Call-back int scoring_type; // Call-back type [1,2] string DBPath; // Path to the database double balance; // Balance ENUM_TIMEFRAMES TF; // Timeframe void CreateDB(const string DBPath,const CDataKeeper &inputData_array[],double r,ENUM_TIMEFRAMES TF);// Create the database and everything that goes with it bool isForvard();// Define the current optimization type (history/forward) void WriteLog(string s,string where);// File log entry int setParams(bool IsForvard,CReportCreator *reportCreator,DealDetales &history[],double &customCoef);// Fill the inputs table void setBuyAndHold(bool IsForvard,CReportCreator *reportCreator);// Fill in the Buy And Hold history bool setTraidingHistory(bool IsForvard,DealDetales &history[],int ID);// Fill in the trading history bool setTotalResult(TotalResult &coefData,bool isOneLot,long ID,bool IsForvard,double customCoef);// Fill in the tables with ratios bool isHistoryItem(bool IsForvard,DealDetales &item,int ID); // Check if these parameters already exist in the trading history table };

The class is used only in the custom robot itself. Its objective is to create an input parameter for a described program, namely the database with a required structure and content. As we can see, it has 3 public methods (the overloaded method is considered as one):

- OnInitEvent

- OnTesterEvent

- OnTickEvent

Each of them is called in the corresponding call-backs of the robot template, where the required parameters are passed to them. The OnInitEvent method is designed to prepare the class for working with the database. Its overloads are implemented as follows:

//+------------------------------------------------------------------+ //| Create the database and connection | //+------------------------------------------------------------------+ void CDBWriter::OnInitEvent(const string _DBPath,const CDataKeeper &inputData_array[],customScoring_2 scoringFunction,double _r,ENUM_TIMEFRAMES _TF) { CreateDB(_DBPath,inputData_array,_r,_TF); scoring_2=scoringFunction; scoring_type=2; } //+------------------------------------------------------------------+ //| Create the database and connection | //+------------------------------------------------------------------+ void CDBWriter::OnInitEvent(const string _DBPath,const CDataKeeper &inputData_array[],customScoring_1 scoringFunction,double _r,ENUM_TIMEFRAMES _TF) { CreateDB(_DBPath,inputData_array,_r,_TF); scoring_1=scoringFunction; scoring_type=1; } //+------------------------------------------------------------------+ //| Create the database and connection | //+------------------------------------------------------------------+ void CDBWriter::OnInitEvent(const string _DBPath,const CDataKeeper &inputData_array[],double _r,ENUM_TIMEFRAMES _TF) { CreateDB(_DBPath,inputData_array,_r,_TF); scoring_type=0; }

As we can see in the method implementation, it assigns required values to the class fields and creates the database. Call-back methods should be implemented by a user personally (if a custom ratio should be calculated) or an overload without a call-back is used — in this case, a custom ratio is equal to zero. A user's ratio is a custom method of assessing the EA optimization pass. In order to implement it, the pointers to two functions with two types of possible required data were created.

- The first one (customScoring_1) receives the trading history and the flag defining the optimization pass the calculation is required for (actually traded lot or trading a single lot — all data for calculations are present in the passed array).

- The second call-back type (customScoring_2) gets access to the database the work is performed from, but only with read-only rights to avoid unexpected edits by the user.

- Assigning balance, timeframe and risk free rate values.

- Establishing connection to the database and occupying a shared resource (Mutex)

- Creating the table database if not created yet.

The OnTickEvent public tick saves the minute candle date at each tick. When testing a strategy, it is impossible to define if the current pass is forward or not, while the database has a similar parameter. But we know that the tester runs forward passes after historical ones. Thus, while overwriting the variable with a date at each tick, we find out the last date at the end of the optimization process. The OptimisationParams table features the HistoryBorder parameter. It is equal to the saved date. The lines are added to this table only during historical optimization. During the first pass with this parameters (same as historical optimization pass), the date is added to the required field in the database. If during one of the next passes, we see that the entry with these parameters is already present in the database, there are two options:

- either a user for some reasons stopped historical optimization and then re-launched it,

- or this is a forward optimization.

To filter one from another, we compare the last date stored in the current pass with the date from the database. If the current date is greater than the one in the database, then this is a forward pass, if it is less or equal, you deal with a historical one. Considering that optimization should be launched twice with the same ratios, we enter only the new data into the database or cancel all changes made during the current pass. The OnTesterEvent() method saves data in the database. It is implemented the following way:

//+------------------------------------------------------------------+ //| Save all the data in the database and return | //| a custom ratio | //+------------------------------------------------------------------+ double CDBWriter::OnTesterEvent() { DealDetales history[]; CDealHistoryGetter historyGetter; historyGetter.getDealsDetales(history,0,TimeCurrent()); // Get trading history CMutexSync sync; // synchronization object if(!sync.Create(getMutexName(DBPath))) { Print(Symbol()+" MutexSync create ERROR!"); return 0; } CMutexLock lock(sync,(DWORD)INFINITE); // lock the segment within the brackets bool IsForvard=isForvard(); // Find out if the current tester iteration is a forward one CReportCreator rc; string Symb[]; rc.Get_Symb(history,Symb); // Get the list of symbols rc.Create(history,Symb,balance,r); // Create a report (Buy And Hold report is created automatically) double ans=0; dbManager.BeginTransaction(); // Transaction start CStatement stmt(dbManager.Create_statement("INSERT OR IGNORE INTO ParamsType VALUES(@ParamName,@ParamType);")); // Request for saving the list of types of EA parameters if(stmt.get()!=NULL) { for(int i=0;i<ArraySize(coef_array);i++) { stmt.Parameter(1,coef_array[i].getName()); stmt.Parameter(2,(int)coef_array[i].getType()); stmt.Execute(); // save parameter types and their names } } int ID=setParams(IsForvard,&rc,history,ans); // Save EA parameters as well as valuation ratios and get ID if(ID>0)// If ID > 0, the parameters are saved successfully { if(setTraidingHistory(IsForvard,history,ID)) // Save the trading history and check if it is saved { setBuyAndHold(IsForvard,&rc); // Save the Buy And Hold history (saved only once - during the first saving) dbManager.CommitTransaction(); // Confirm the end of a transaction } else dbManager.RollbackTransaction(); // Otherwise, cancel the transaction } else dbManager.RollbackTransaction(); // Otherwise, cancel the transaction return ans; }

The first thing the method does is forming the trading history using the class described in my previous article. Then it takes the shared resource (Mutex) and saves the data. To achieve this, first define if the current optimization pass is forward (according to the method described above), then get the list of symbols (all symbols that were traded).

Accordingly, if a spread-trading EA was tested for instance, the trading history is uploaded on both symbols the trading was conducted on. After that, a report is generated (using the class reviewed below) and written to the database. A transaction is created for the correct record. The transaction is canceled if an error occurred when filling any of the tables or incorrect data were obtained. First, the ratios are saved, and then, if everything went smoothly, we save the trading history followed by the Buy and Hold history. The latter is saved only once during the first data entry. In case of a data saving error, Log File in the Common/Files folder is generated.

After creating the database, it should be read. The database reading class is already used in the described program. It is simpler and looks as follows:

//+------------------------------------------------------------------+ //| Class reading data from the database | //+------------------------------------------------------------------+ class CDBReader { public: void Connect(string DBPath);// Method connecting to the database bool getBuyAndHold(BuyAndHoldChart_item &data[],bool isForvard);// Method reading Buy And Hold history bool getTraidingHistory(DealDetales &data[],long ID,bool isForvard);// Method reading history traded by the EA bool getRobotParams(CoefData_item &data[],bool isForvard);// Method reading the EA parameters and ratios private: CSqliteManager dbManager; // Database manager string DBPath; // Path to the database bool getParamTypes(ParamType_item &data[]);// Read input types and their names. };

It implements 3 public methods reading 4 tables we are interested in and creating structure arrays with data from these tables.

- The first method (getBuyAndHold) returns BuyAndHold history by reference for forward and historical periods depending on the passed flag. If the upload is successful, the method returns 'true', otherwise 'false'. The upload is performed from the Buy And Hold table.

- The getTradingHistory method also returns trading history for passed ID and the isForvard flag accordingly. The upload is performed from the TradingHistory table.

- The getRobotParams method combines uploads from the two tables: ParamsCoefitients — from where the robot parameters are taken and OptimisationParams where calculated valuation ratios are located.

Thus, the written classes allow you to no longer work directly with the database, but with the classes that provide the required data hiding the entire algorithm for working with the database. These classes, in turn, work with the written wrapper for the database, which also simplifies the work. The mentioned wrapper works with the database via Dll provided by the database developers. The database itself meets all required conditions and in fact is a file making it convenient for transportation and processing both in this program and in other analytical applications. Another advantage of this approach is the fact that the long-term operation of a single algorithm enables you to collect databases from each optimization, thereby accumulating history and tracking parameter change patterns.

Calculations

The block consists of two classes. The first one is meant for generating a trading report and is an improved version of the class generating a trading report described in the previous article.

The second one is a filter class. It sorts optimization samples in a passed range and is able to create a graph displaying a frequency of profitable and loss-making trades for each individual optimization ratio value. Another objective of this class is to create a normal distribution graph for the actually traded PL as of the end of optimization (i.e. PL for the entire optimization period). In other words, if there are 1000 optimization passes, we have 1000 optimization results (PL as of the optimization end). The distribution we are interested in is based on them.

This distribution shows, in which direction the asymmetry of the obtained values is shifted. If the larger tail and the distribution center are in the profit zone, the robot generates mostly profitable optimization passes and, accordingly, is good, otherwise it generates mostly unprofitable passes. If the definition asymmetry is shifted to the loss-making zone, this also means that the selected parameters mostly cause losses rather than profits.

Let's have a look at this block starting with the class generating a trading report. The described class is located in the Include directory of the "History manager" folder and has the following header:

//+------------------------------------------------------------------+ //| Class for generating the trading history statistics | //+------------------------------------------------------------------+ class CReportCreator { public: //============================================================================================================================================= // Calculation/ Recalculation: //============================================================================================================================================= void Create(DealDetales &history[],DealDetales &BH_history[],const double balance,const string &Symb[],double r); void Create(DealDetales &history[],DealDetales &BH_history[],const string &Symb[],double r); void Create(DealDetales &history[],const string &Symb[],const double balance,double r); void Create(DealDetales &history[],double r); void Create(const string &Symb[],double r); void Create(double r=0); //============================================================================================================================================= // Getters: //============================================================================================================================================= bool GetChart(ChartType chart_type,CalcType calc_type,PLChart_item &out[]); // Get PL graphs bool GetDistributionChart(bool isOneLot,DistributionChart &out); // Get distribution graphs bool GetCoefChart(bool isOneLot,CoefChartType type,CoefChart_item &out[]); // Get ratio graphs bool GetDailyPL(DailyPL_calcBy calcBy,DailyPL_calcType calcType,DailyPL &out); // Get PL graph by days bool GetRatioTable(bool isOneLot,ProfitDrawdownType type,ProfitDrawdown &out); // Get the table of extreme points bool GetTotalResult(TotalResult &out); // Get the TotalResult table bool GetPL_detales(PL_detales &out); // Get the PL_detales table void Get_Symb(const DealDetales &history[],string &Symb[]); // Get the array of symbols that were traded void Clear(); // Clear statistics private: //============================================================================================================================================= // Private data types: //============================================================================================================================================= // Structure of PL graph types struct PL_keeper { PLChart_item PL_total[]; PLChart_item PL_oneLot[]; PLChart_item PL_Indicative[]; }; // Types structure of daily Profit/Loss graph struct DailyPL_keeper { DailyPL avarage_open,avarage_close,absolute_open,absolute_close; }; // Structure of the extreme points table struct RatioTable_keeper { ProfitDrawdown Total_max,Total_absolute,Total_percent; ProfitDrawdown OneLot_max,OneLot_absolute,OneLot_percent; }; // Structures for calculating the amount of profits and losses in a row struct S_dealsCounter { int Profit,DD; }; struct S_dealsInARow : public S_dealsCounter { S_dealsCounter Counter; }; // Structures for calculating auxiliary data struct CalculationData_item { S_dealsInARow dealsCounter; int R_arr[]; double DD_percent; double Accomulated_DD,Accomulated_Profit; double PL; double Max_DD_forDeal,Max_Profit_forDeal; double Max_DD_byPL,Max_Profit_byPL; datetime DT_Max_DD_byPL,DT_Max_Profit_byPL; datetime DT_Max_DD_forDeal,DT_Max_Profit_forDeal; int Total_DD_numDeals,Total_Profit_numDeals; }; struct CalculationData { CalculationData_item total,oneLot; int num_deals; bool isNot_firstDeal; }; // Structure for creating ratio graphs struct CoefChart_keeper { CoefChart_item OneLot_ShartRatio_chart[],Total_ShartRatio_chart[]; CoefChart_item OneLot_WinCoef_chart[],Total_WinCoef_chart[]; CoefChart_item OneLot_RecoveryFactor_chart[],Total_RecoveryFactor_chart[]; CoefChart_item OneLot_ProfitFactor_chart[],Total_ProfitFactor_chart[]; CoefChart_item OneLot_AltmanZScore_chart[],Total_AltmanZScore_chart[]; }; // Class participating in sorting trading history by close date. class CHistoryComparer : public ICustomComparer<DealDetales> { public: int Compare(DealDetales &x,DealDetales &y); }; //============================================================================================================================================= // Keepers: //============================================================================================================================================= CHistoryComparer historyComparer; // Comparing class CChartComparer chartComparer; // Comparing class // Auxiliary structures PL_keeper PL,PL_hist,BH,BH_hist; DailyPL_keeper DailyPL_data; RatioTable_keeper RatioTable_data; TotalResult TotalResult_data; PL_detales PL_detales_data; DistributionChart OneLot_PDF_chart,Total_PDF_chart; CoefChart_keeper CoefChart_data; double balance,r; // Initial deposit and no-risk rate // Sorting class CGenericSorter sorter; //============================================================================================================================================= // Calculations: //============================================================================================================================================= // Calculate PL void CalcPL(const DealDetales &deal,CalculationData &data,PLChart_item &pl_out[],CalcType type); // Calculate PL histograms void CalcPLHist(const DealDetales &deal,CalculationData &data,PLChart_item &pl_out[],CalcType type); // Calculate auxiliary structures used for plotting void CalcData(const DealDetales &deal,CalculationData &out,bool isBH); void CalcData_item(const DealDetales &deal,CalculationData_item &out,bool isOneLot); // Calculate daily profit/loss void CalcDailyPL(DailyPL &out,DailyPL_calcBy calcBy,const DealDetales &deal); void cmpDay(const DealDetales &deal,ENUM_DAY_OF_WEEK etalone,PLDrawdown &ans,DailyPL_calcBy calcBy); void avarageDay(PLDrawdown &day); // Compare symbols bool isSymb(const string &Symb[],string symbol); // Calculate profit factor void ProfitFactor_chart_calc(CoefChart_item &out[],CalculationData &data,const DealDetales &deal,bool isOneLot); // Calculate recovery factor void RecoveryFactor_chart_calc(CoefChart_item &out[],CalculationData &data,const DealDetales &deal,bool isOneLot); // Calculate win ratio void WinCoef_chart_calc(CoefChart_item &out[],CalculationData &data,const DealDetales &deal,bool isOneLot); // Calculate Sharpe ratio double ShartRatio_calc(PLChart_item &data[]); void ShartRatio_chart_calc(CoefChart_item &out[],PLChart_item &data[],const DealDetales &deal); // Calculate distribution void NormalPDF_chart_calc(DistributionChart &out,PLChart_item &data[]); double PDF_calc(double Mx,double Std,double x); // Calculate VaR double VaR(double quantile,double Mx,double Std); // Calculate Z score void AltmanZScore_chart_calc(CoefChart_item &out[],double N,double R,double W,double L,const DealDetales &deal); // Calculate the TotalResult_item structure void CalcTotalResult(CalculationData &data,bool isOneLot,TotalResult_item &out); // Calculate the PL_detales_item structure void CalcPL_detales(CalculationData_item &data,int deals_num,PL_detales_item &out); // Get day from the date ENUM_DAY_OF_WEEK getDay(datetime DT); // Clear data void Clear_PL_keeper(PL_keeper &data); void Clear_DailyPL(DailyPL &data); void Clear_RatioTable(RatioTable_keeper &data); void Clear_TotalResult_item(TotalResult_item &data); void Clear_PL_detales(PL_detales &data); void Clear_DistributionChart(DistributionChart &data); void Clear_CoefChart_keeper(CoefChart_keeper &data); //============================================================================================================================================= // Copy: //============================================================================================================================================= void CopyPL(const PLChart_item &src[],PLChart_item &out[]); // Copy PL graphs void CopyCoefChart(const CoefChart_item &src[],CoefChart_item &out[]); // Copy ratio graphs };

This class, unlike its previous version, calculates two times more data and builds more types of graphs. 'Create' method overloads also calculate the report.

In fact, the report is generated only once — at the time of the Create method call. Later on, only the previously calculated data are obtained in the methods starting with the Get word. The main loop, iterating over the input parameters once, is located in the Create method with the most arguments. This method iterates over arguments and immediately calculates a series of data, based on which all required data are built in the same iteration.

This allows building everything we are interested in within a single pass, while the previous version of this class for getting the graph iterated over initial data again. As a result, the calculation of all ratios lasts milliseconds, while obtaining the required data takes even less time. In the 'private' area of the class, there is a series of structures used only inside that class as more convenient data containers. Sorting trading history is performed using the Generic sorting method described above.

Let's describe data obtained when calling each of the getters:

| Method | Parameters | chart type |

|---|---|---|

| GetChart | chart_type = _PL, calc_type = _Total | PL graph — according to actual trading history |

| GetChart | chart_type = _PL, calc_type = _OneLot | PL graph — when trading a single lot |

| GetChart | chart_type = _PL, calc_type = _Indicative | PL graph — indicative |

| GetChart | chart_type = _BH, calc_type = _Total | BH graph — if managing a lot as a robot |

| GetChart | chart_type = _BH, calc_type = _OneLot | BH graph — if trading a single lot |

| GetChart | chart_type = _BH, calc_type = _Indicative | BH graph — indicative |

| GetChart | chart_type = _Hist_PL, calc_type = _Total | PL histogram — according to actual traded history |

| GetChart | chart_type = _Hist_PL, calc_type = _OneLot | PL histogram — if trading a single lot |

| GetChart | chart_type = _Hist_PL, calc_type = _Indicative | PL histogram — indicative |

| GetChart | chart_type = _Hist_BH, calc_type = _Total | BH histogram — if managing a lot as a robot |

| GetChart | chart_type = _Hist_BH, calc_type = _OneLot | BH histogram — if trading a single lot |

| GetChart | chart_type = _Hist_BH, calc_type = _Indicative | BH histogram — indicative |

| GetDistributionChart | isOneLot = true | Distributions and VaR when trading a single lot |

| GetDistributionChart | isOneLot = false | Distributions and VaR when trading like we did previously |

| GetCoefChart | isOneLot = true, type=_ShartRatio_chart | Sharpe ratio by time when trading a single lot |

| GetCoefChart | isOneLot = true, type=_WinCoef_chart | Win ratio by time when trading a single lot |

| GetCoefChart | isOneLot = true, type=_RecoveryFactor_chart | Recovery factor by time when trading a single lot |

| GetCoefChart | isOneLot = true, type=_ProfitFactor_chart | Profit factor by time when trading a single lot |

| GetCoefChart | isOneLot = true, type=_AltmanZScore_chart | Z — Altman score by time when trading a single lot |

| GetCoefChart | isOneLot = false, type=_ShartRatio_chart | Sharpe ratio by time when trading like we did previously |

| GetCoefChart | isOneLot = false, type=_WinCoef_chart | Win ratio by time when trading like we did previously |

| GetCoefChart | isOneLot = false, type=_RecoveryFactor_chart | Recovery factor by time when trading like we did previously |

| GetCoefChart | isOneLot = false, type=_ProfitFactor_chart | Profit factor by time when trading like we did previously |

| GetCoefChart | isOneLot = false, type=_AltmanZScore_chart | Z — Altman score by time when trading like we did previously |

| GetDailyPL | calcBy=CALC_FOR_CLOSE, calcType=AVERAGE_DATA | Average PL by days as of closing time |

| GetDailyPL | calcBy=CALC_FOR_CLOSE, calcType=ABSOLUTE_DATA | Total PL by days as of closing time |

| GetDailyPL | calcBy=CALC_FOR_OPEN, calcType=AVERAGE_DATA | Average PL by days as of opening time |

| GetDailyPL | calcBy=CALC_FOR_OPEN, calcType=ABSOLUTE_DATA | Total PL by days as of opening time |

| GetRatioTable | isOneLot = true, type = _Max | If trading one lot — maximum obtained profit/loss per trade |

| GetRatioTable | isOneLot = true, type = _Absolute | If trading one lot — total profit/loss |

| GetRatioTable | isOneLot = true, type = _Percent | If trading one lot — amount of profits/losses in % |

| GetRatioTable | isOneLot = false, type = _Max | If trading like we did previously — maximum obtained profit/loss per trade |

| GetRatioTable | isOneLot = false, type = _Absolute | If trading like we did previously — total profit/loss |

| GetRatioTable | isOneLot = false, type = _Percent | If trading like we did previously — amount of profits/losses in % |

| GetTotalResult | Table with ratios | |

| GetPL_detales | PL curve brief summary | |

| Get_Symb | Array of symbols present in the trading history |

PL graph — according to actual trading history:

The graph is equal to a usual PL graph. We can see this in the terminal after all the tester passes.

PL graph — when trading a single lot:

This graph is similar to the previously described one differing in a traded volume. It is calculated as if we were trading a single lot all the time. Entry and exit prices are calculated as averaged prices by the total number of EA market entries and exits. A trading profit is also calculated based on the profit traded by the EA, but it is converted into the profit obtained as if trading a single lot via the proportion.

PL graph — indicative:

Normalized PL graph. If PL > 0, PL is divided by the maximum loss-making deal reached by this moment, otherwise PL is divided by the maximum profitable deal reached so far.

Histogram graphs are constructed in a similar way.

Distributions and VaR

Parametric VaR is built using both absolute data and growth.

The same is true for the distribution graph.

Ratio graphs:

Built at each loop iteration according to the appropriate equations throughout the entire history available for this particular iteration.

Daily profit graphs:

Built by 4 possible profit combinations mentioned in the table. Looks like a histogram.

The method creating all mentioned data looks as follows: