Join our fan page

The class for drawing the MFI using the ring buffer - indicator for MetaTrader 5

My main creative contribution to the MQL5-coding and the community:

- Views:

- 8787

- Rating:

- Published:

- Updated:

-

You are missing trading opportunities:

You are missing trading opportunities:- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration Log inYou agree to website policy and terms of use

If you do not have an account, please register -

Need a robot or indicator based on this code? Order it on Freelance

Go to Freelance

Need a robot or indicator based on this code? Order it on Freelance

Go to Freelance

Description

The CMFIOnRingBuffer class is designed to calculate the technical indicator Money Flow Index (Money Flow Index, MFI) using the algorithm of the ring buffer.

Declaration

class CMFIOnRingBuffer : public CArrayRing

Title

#include <IncOnRingBuffer\CMFIOnRingBuffer.mqh>File of the CMFIOnRingBuffer.mqh class must be placed in IncOnRingBuffer folder that need to be established in MQL5\Include\. Two files with the examples used by the class from this folder are attached to the description. File with the class of the ring buffer and the class of Moving Average also must be in this folder.

Class methods

//--- initialization method: bool Init( // if error it returns false, // if successful - true int period = 14, // the period of the MFI ENUM_MA_METHOD method = MODE_SMA, // the method of smoothibg ENUM_APPLIED_PRICE applied_price = PRICE_TYPICAL, // price used for calculation ENUM_APPLIED_VOLUME applied_volume = VOLUME_TICK, // volume used for calculation int size_buffer = 256, // the size of the ring buffer bool as_series = false // true, if a time series, otherwise - false );

//--- the method of calculation based on the time series or indicator buffers: int MainOnArray( // returns the number of the processed elements const int rates_total, // the size of the arrays const int prev_calculated, // processed elements on the previous call const double& open[], // open prices const double& high[], // the maximum prices const double& low[], // the minimum prices const double& close[], // close prices const long& tick_volume[], // tick volume const long& volume[]); // stock volume );

//--- method of calculation on the basis of the separate series elements of the array double MainOnValue( // returns the MFI value for the set element (bar) const int rates_total, // the size of the array const int prev_calculated, // processed elements of the array const int begin, // from where the significant data of the array starts const double open, // price of bar opening const double high, // the maximum price of the bar const double low, // the minimum price of the bar const double close, // price of bar closing const long tick_volume, // tick volume of the bar const long volume, // stock volume of the bar const int index // the element (bar) index );

//--- the methods of access to the data: int BarsRequired(); // Returns the necessary number of bars to draw the indicator string Name(); // Returns the name of the indicator int Period(); // Returns the period string Method(); // Returns the method in the form of the text line ENUM_APPLIED_PRICE Price(); // Returns the type of the used price ENUM_APPLIED_VOLUME Volume(); // Returns the type of the used volume int Size(); // Returns the size of the ring buffer

To get the calculated data of the indicator from the ring buffer is possible as from the usual array. For example:

//--- the class with the methods of calculation of the MFI indicator: #include <IncOnRingBuffer\CMFIOnRingBuffer.mqh> CMFIOnRingBuffer mfi; ... //+------------------------------------------------------------------+ //| Custom indicator iteration function | //+------------------------------------------------------------------+ int OnCalculate(const int rates_total, const int prev_calculated, const datetime& time[], const double& open[], const double& high[], const double& low[], const double& close[], const long& tick_volume[], const long& volume[], const int& spread[]) { //--- calculation of the indicator based on time series: mfi.MainOnArray(rates_total,prev_calculated,open,high,low,close,tick_volume,volume); ... //--- use data from the ring buffers "mfi", // for example, copy data in the indicator buffer: for(int i=start;i<rates_total && !IsStopped();i++) MFI_Buffer[i] = mfi[rates_total-1-i]; // indicator line ... //--- return value of prev_calculated for next call: return(rates_total); }

Please note that indexing in the ring buffer is the same as in the time series.

Examples

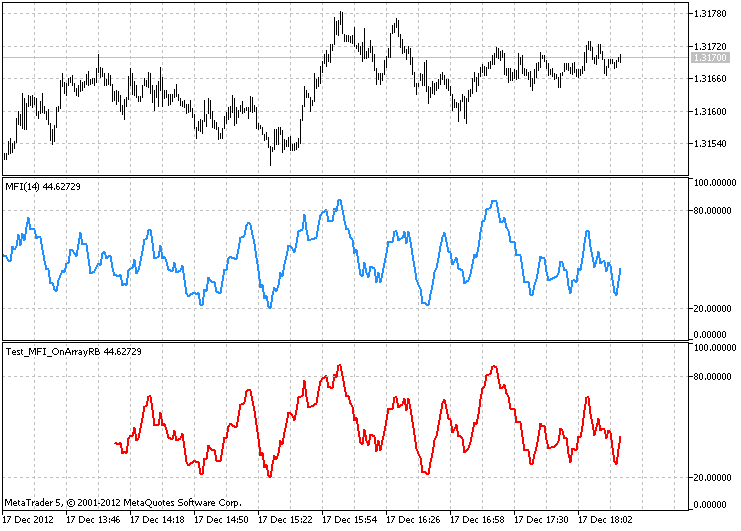

- The Test_MFI_OnArrayRB.mq5 file calculates the indicator based on the price time series. The MainOnArray() method application is demonstrated

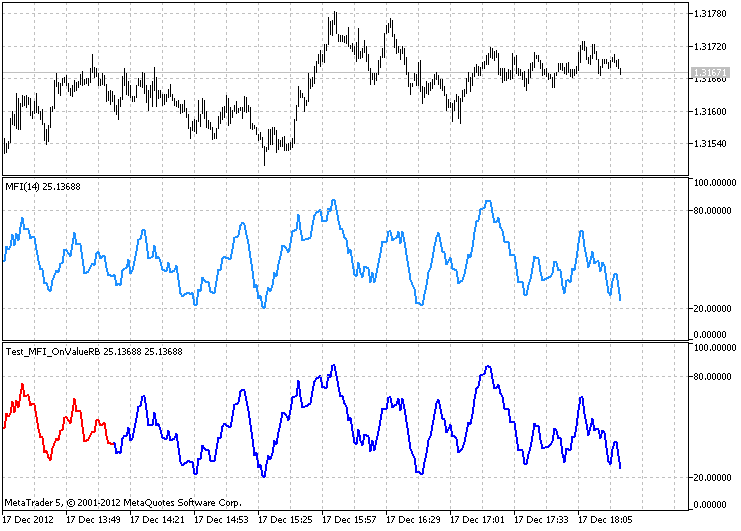

- The Test_MFI_OnValueRB.mq5 file demonstrates the use of the MainOnValue() method. At first the MFI indicator is calculated and drawn. Then on the basis of this ring buffer of this indicator one more MFI indicator is drawn.

The result of the work of the Test_MFI_OnArrayRB.mq5 with the size of the ring buffer of 256 elements When writing code the developments of MetaQuotes Software Corp., Integer and GODZILLA were used.

The result of the work of the Test_MFI_OnValueRB.mq5 with the size of the ring buffer of 256 elements

Translated from Russian by MetaQuotes Ltd.

Original code: https://www.mql5.com/ru/code/1395

The class for drawing the AMA using the ring buffer

The class is designed for calculation of the technical indicator Adaptive Moving Average (Adaptive Moving Average, AMA) using the algorithm of the ring buffer.

RD-TrendTrigger

The oscillator using T3 averaging from the Technical Analysis of Stocks and Commodities (Dec. 2004).

MACDWaterlineCrossExpectator, the effectiveness of a MACD system

MACDWaterlineCrossExpectator, the effectiveness of a MACD system

This is the classical trading system which consists in buying when MACD crosses above the waterline line and selling when crosses below it. This EA works along with a monetary management system which has a positive mathematical expectation.

T3MACO

The oscillator using T3 averaging.