German Ifo Business Climate (August): Forecast: 107.1, July: 108.0

As economic data shows a slowdown in the Eurozone, businesses are feeling the pinch. The German Ifo Business Climinate survey is expected to show the worst result in a year, since August 2013, when the reading was 106.2.

US New Home Sales (July): Forecast: 426K, June: 406K

Data for the US housing sector in July have been impressive. We saw strong building approvals, housing starts, and exisintg home sales data all improve and beat expectrations. New Home Sales is exected to improve in July and should help to keep the USD buoyed.

NZ Tade Balance (July): Forecast: -475M, June: 247M

New Zealand is expected to post its first month of trade deficit in 2014. The RBNZ’s rate cuts this year has been working through the economy, and we are seeing a bit of a slowdown, so it does seem like it will be a while before the central bank can consider raising rates again. A trade deficit should weigh on the NZD, which should continue to pare its first half-year of gains.

Tuesday (8/26)

US Durable Goods (July): Forecast: 7.4%, June 1.7% (revised up from 0.7%)

Core Durable Goods (July): 0.5%, June: 1.9% (revised up from 0.8%)

It looks like Q2 ended with a bang, and Q3 is starting with good demand

that should help sustain growth throughout the year. strong US data

continue to support the case for a rate hike earlier than mid-2015.

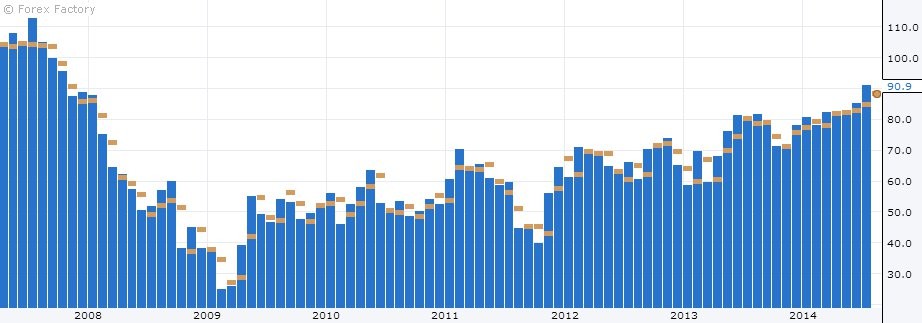

US Conference Board Consumer Confidence (August): Forecast: 89.1, July: 90.9

Consumer Confidence is expected to level off a bit in August, but it is

still strong, as July’s reading was the highst reading since Oct. 2007.

Wednesday (8/27)

GfK German Consumer Climate (August): 8.9, July: 9.0

Just businesses, consumers are expected to feel the slowdown in the Eurozone economy.

Thursday (8/28)

AUS Private Capital Expenditure q/q (Q2): Forecast: -0.8%, Previous: -4.2%

Look for a positive capital expenditure reading as a surprise that can

lift the Australian Dollar. It has slid and been consolidating. If we do

see capital investment rebound, the AUD should avoid sliding further,

and at least remain in consolidation.

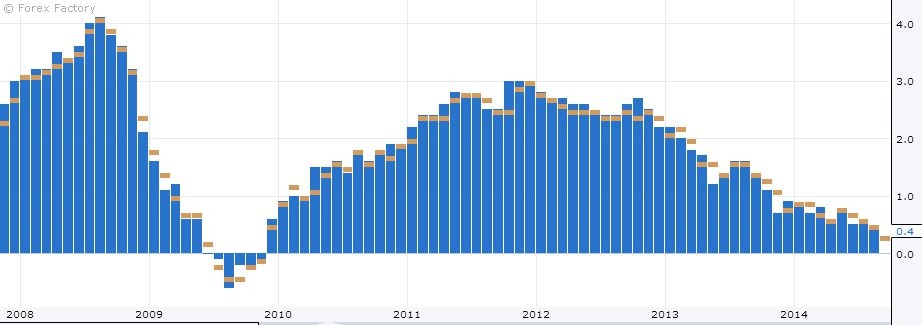

German Prelim CPI m/m (August): 0.0%, Previous 0.3%

Disinflationary pressure in the Eurozone is well noted. Soft inflation

data for Germany will continue to fan the expectation of more ECB

stimulus measures, which should also continue to pressure the Euro.

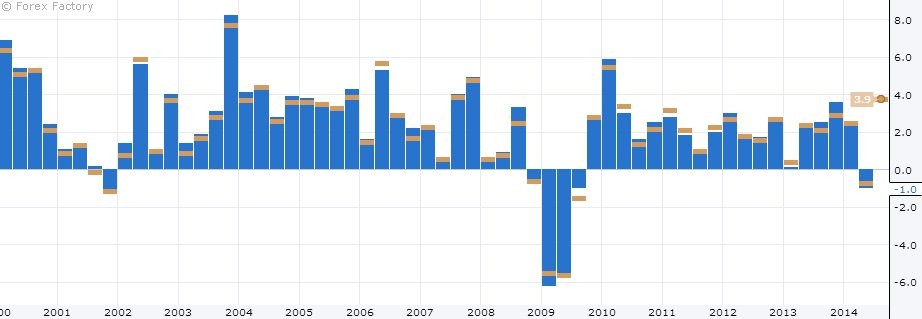

US Prelimary GDP Q2: 3.9%, Advanced Estiate: 4.0%

The GDP data for Q2 is expected to be a hair below the first “advanced”

estimate. Look for a boost for the USD if the reading stays at 4.0% or

better. A slide lower than 3.9% might cause the USD to pare its recent

gains if it hasn’t already done so throughout the week.

US Jobless Claims Forecast: 299K, Previous 298K

Jobs data continue to impress as jobless claims readings are starting to hold below 300K.

US Pending Home Sales (July) Forecast: 0.6%, June: -1.1%

Can we go 5 for 5 this month in terms of housing data? Not only have

housing data been improving in July they have beat forecasts, and have

been part of the reason for the strong USD in recent weeks.

Friday (8/29)

Eurozone Flash CPI Estimate y/y (August) Forecast: 0.3%, July: 0.4%.

A few months ago, Draghi predicted that the 0.5% y/y annual CPI growth

was the low on the year. However, the annual inflation rate fell in

July, and is expected to fall again in August. ECB stimulus soon?

CAN GDP m/m (June) Forecast: 0.3%, May: 0.4%

May’s reading was the strongest in 4 months, and June’s reading is

expected to almost just as strong, and would make it the 6th straigth

months of GDP growth in Canada. A reading above 0.3% will give CAD a

chance to pare some of its recent losses.

")

")