Reality Check: Backtesting an EA on Live Trade Data - No "Painting" the Past

21 March 2025, 02:20

0

487

Dear fellow traders,

In the vast and diverse world of Expert Advisors (EAs), finding a reliable one to entrust your capital to is always a challenging task. Amidst countless advertisements and promises of "huge" profits, transparency becomes the "guiding star" leading to wise investment decisions.

Have you ever wondered if the "dreamy" backtest results presented by EA providers truly reflect actual trading performance? Can an EA "survive" and generate stable profits when facing the unpredictable fluctuations of the live market?

In this article, we will explore this question by conducting a special backtest, not on distant historical data, but on actual live market data. We’ll use an example EA referred to here as "Example EA" to illustrate how backtesting on live data can provide a more realistic view of an EA’s performance.

Backtest Period: From Live Trade Start to Present

To provide the most objective and realistic view, we have backtested Example EA during the period from March 2nd, 2025, to today, March 21st, 2025. This timeframe is significant because it mirrors the actual market conditions the EA encountered during live trading. Testing on live data like this offers a clearer picture of how an EA performs compared to traditional historical backtests.

Backtest Parameters

The live account started with $100,000, so we aligned the backtest parameters accordingly:

- Initial Capital: $100,000

- Leverage: 1:100

- Risk Level: 3

- EA Configuration: Both Algo 1 & 2 running simultaneously

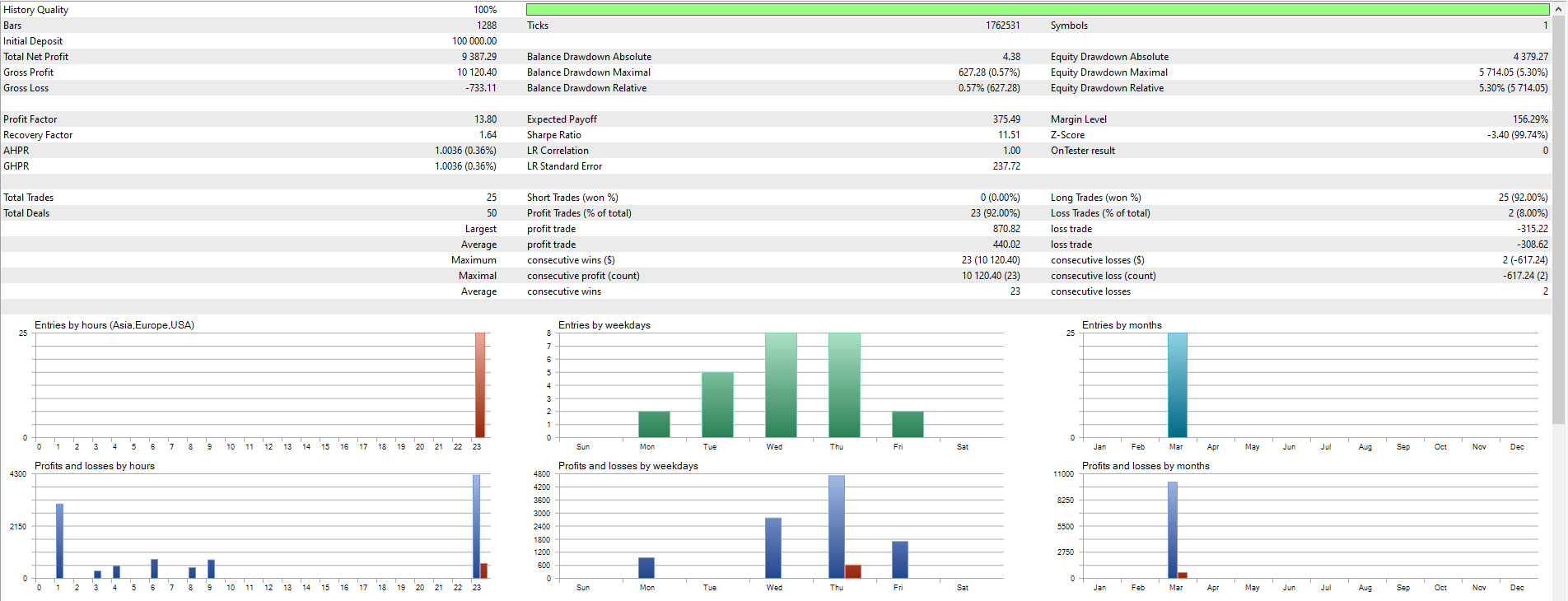

Backtest Results: Raw Data

Here’s a summary of the MT5 backtest results we obtained:

(Table Note: Specific figures aren’t included here, but a complete table would list key metrics such as:)

Metric | Description |

|---|---|

Net Profit | Total profit generated during the backtest period. |

Total Trades | Number of trades executed by the EA. |

Balance DD Max | Largest drop in account balance. |

Equity DD Max | Largest drop in equity. |

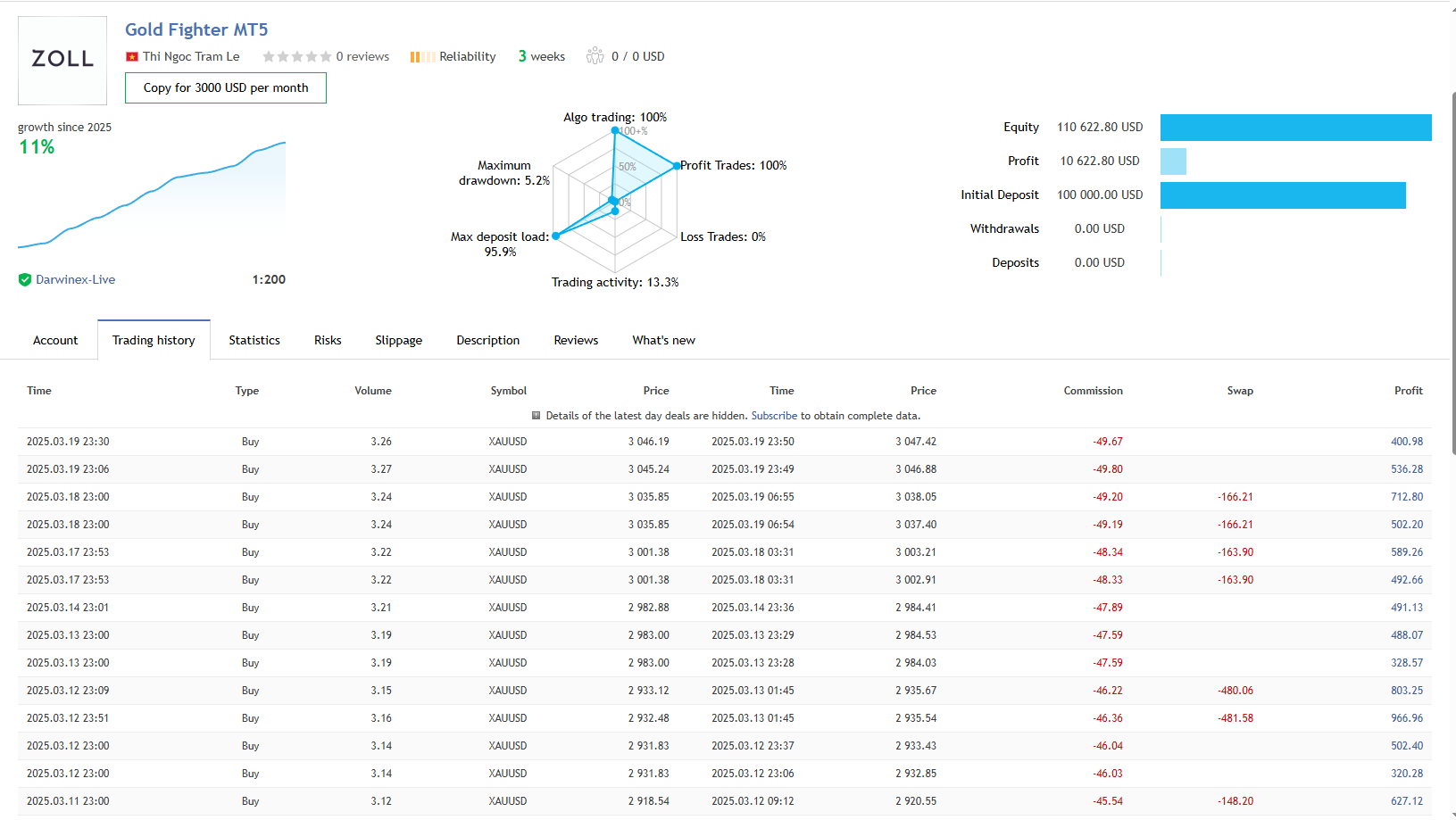

Additionally, we reviewed data from the live trade account. The profit shown there, after accounting for commission and swap fees, slightly exceeded the backtest results, offering an interesting comparison.

Key Observations

Backtest results, no matter how impressive, are only past references and don’t guarantee future performance. However, backtesting on live data, especially over a recent period like from March 2nd to March 21st, 2025, provides unique authenticity. Unlike cherry-picked historical tests, this method reflects real market challenges—volatility, slippage, and all.

This approach avoids “painting” the past with idealized results. Instead, it offers an unfiltered look at how an EA like Example EA behaves in a live environment, giving traders a more reliable benchmark for evaluation.

Why This Matters

Transparency in testing is vital for understanding an EA’s strengths and limitations. Sharing results from live data isn’t about proving superiority—it’s about providing a practical example of how backtesting can align with real-world performance. Traders can use this method to assess any EA they’re considering, gaining confidence in their analysis.

Final Thoughts

We hope this discussion and the backtest data shed light on the importance of testing EAs on live trade periods. If you’d like to explore this further, consider reviewing the results table (once filled with specific figures) or applying similar backtesting techniques to other EAs. Feel free to share your thoughts or questions in the comments below.

Let’s keep learning and sharing knowledge to become better, more informed traders. Here’s to successful trading and thoughtful decision-making!

Files:

Backtest_MT5.png

61 kb

Live_Trade.png

93 kb

")

")

{kind=link}

{kind=link}