")

Fundamental Market Analysis for July 1, 2026 (EURUSD, GBPUSD, USDJPY)

Events to watch today:

15:15 EET. USD - ADP Non-Farm Employment Change

16:00 EET. USD - Federal Reserve Chair Kevin Warsh will deliver a speech

17:00 EET. USD - ISM Manufacturing PMI

EURUSD:

Preliminary June inflation estimates from the euro area’s largest economies came in weaker than expected. Inflation slowed in Germany, France and Italy, while lower energy prices have reduced the risk of renewed price pressures. This creates more room for the ECB to avoid rushing into another rate increase following its June decision.

Markets are assigning a low probability to another ECB move at the next meeting. In the United States, US Treasury yields have risen, while expectations of a Federal Reserve rate increase by September have strengthened. A resilient US labour market and firmer inflation concerns continue to support the US dollar, widening the policy contrast with the euro.

Eurozone-wide inflation data may provide further clarity, but the current slowdown in price growth across the region gives the ECB greater scope to pause. Lower oil prices are also easing energy-related pressure, while US employment data will remain an important test for Federal Reserve expectations. As long as this backdrop remains in place, EURUSD may stay under pressure, and the sell scenario remains consistent with the fundamental outlook.

Trading idea: SELL 1.1415, SL 1.1445, TP 1.1325

Events to watch today:

15:15 EET. USD - ADP Non-Farm Employment Change

16:00 EET. USD - Federal Reserve Chair Kevin Warsh will deliver a speech

16:00 EET. GBP - BOE Governor Andrew Bailey Speaks

17:00 EET. USD - ISM Manufacturing PMI

GBPUSD:

Sterling enters July after revised UK economic data failed to ease concerns about the resilience of domestic demand. GDP expanded by 0.6% in the first quarter, but household disposable income declined, while April figures pointed to weaker momentum at the start of the second quarter. This may limit the economy’s ability to absorb high borrowing costs for an extended period.

The Bank of England kept its rate unchanged at 3.75% in June. However, calmer inflation and lower household inflation expectations reduce the need for further policy tightening in the near term. At the same time, changes in government have added uncertainty around fiscal policy. Markets will assess whether the new administration can balance stimulus plans with confidence in public finances.

The market backdrop remains challenging for GBPUSD. Higher US Treasury yields and stronger Federal Reserve rate expectations increase the appeal of the US dollar. Sterling could receive support from signs of stronger consumer spending or renewed services inflation, but recent data have not yet provided that confirmation. The base case therefore favours the US dollar and allows for further downside in the pair if the current news flow persists.

Trading idea: SELL 1.3250, SL 1.3280, TP 1.3160

Events to watch today:

15:15 EET. USD - ADP Non-Farm Employment Change

16:00 EET. USD - Federal Reserve Chair Kevin Warsh will deliver a speech

17:00 EET. USD - ISM Manufacturing PMI

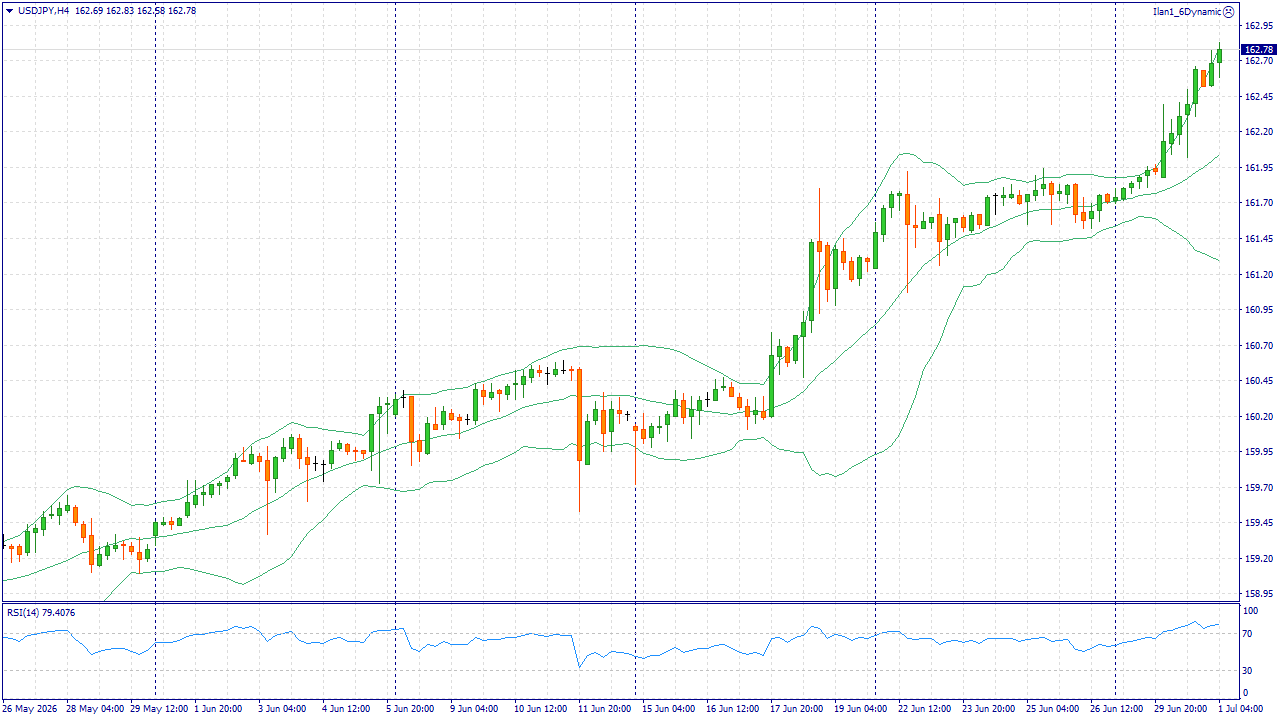

USDJPY:

USDJPY has reached multi-year highs alongside rising US Treasury yields. The two-year yield remains near 4.17%, while markets have increased the probability of a Federal Reserve rate hike by September. Ahead of the upcoming labour market data, this reassessment continues to support the US dollar, as a resilient jobs market reduces expectations of near-term policy easing.

The Bank of Japan continued policy normalisation in June and left the door open to further adjustments if inflation remains sustainable. However, the gap between US and Japanese interest rates is still substantial. Lower oil prices improve conditions for Japan as an energy importer, but they do not eliminate demand for carry trades. For the yen, Federal Reserve expectations and signals from the Bank of Japan remain more important.

The risk of action by Japanese authorities remains elevated. Officials continue to signal readiness to respond to excessive currency moves, while the approaching US holiday period could reduce market liquidity. However, there have been no new confirmed measures or stronger official warnings, while US Treasury yields continue to rise. The fundamental advantage therefore remains with the US dollar, although labour market data and statements from Tokyo could quickly change the outlook.

Trading idea: BUY 162.75, SL 162.35, TP 163.95

Our company provides an opportunity to earn income not only from your trading. By attracting clients within the affiliate program, you can get up to $30 per lot!

You can find more analytical information on our website.

")