RavenQuant Daybreak EA for SP500

- Experts

- Versão: 1.14

- Ativações: 5

Fully automated intraday volatility-breakout EA for the US500 - MetaTrader 5

Overview

RavenQuant Daybreak is a fully automated, rules-based trading system for the US500 (S&P 500). It captures the market's most decisive intraday moments, trading breakouts in both directions with a hard stop loss on every position and an automatic, risk-based compounding engine.

- 100% mechanical - no martingale, no grid, no risky averaging.

- Solid stop loss on every trade - risk is defined before each entry, never naked.

- Regime-change flexible - adapts to trending, choppy, bull and bear markets and keeps working through news and downturns.

- Risk-based position sizing with 5 selectable risk profiles and a broker-independent exposure ceiling that de-risks the account as it grows.

- Built-in order splitting that beats the broker's max-lot cap, so big balances keep compounding.

- Session anchored to New York time and auto-converted to any broker's server clock (daylight saving handled all year).

- Easy to use and prop-firm friendly.

Performance

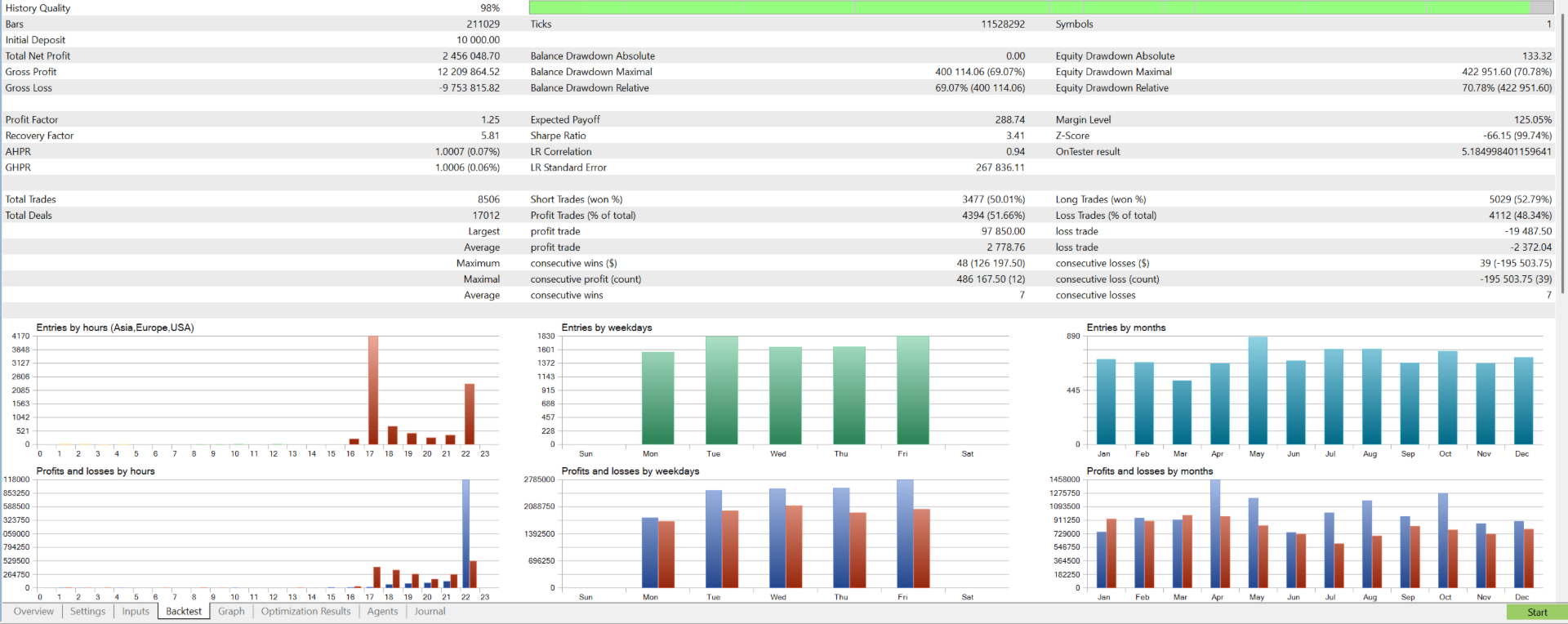

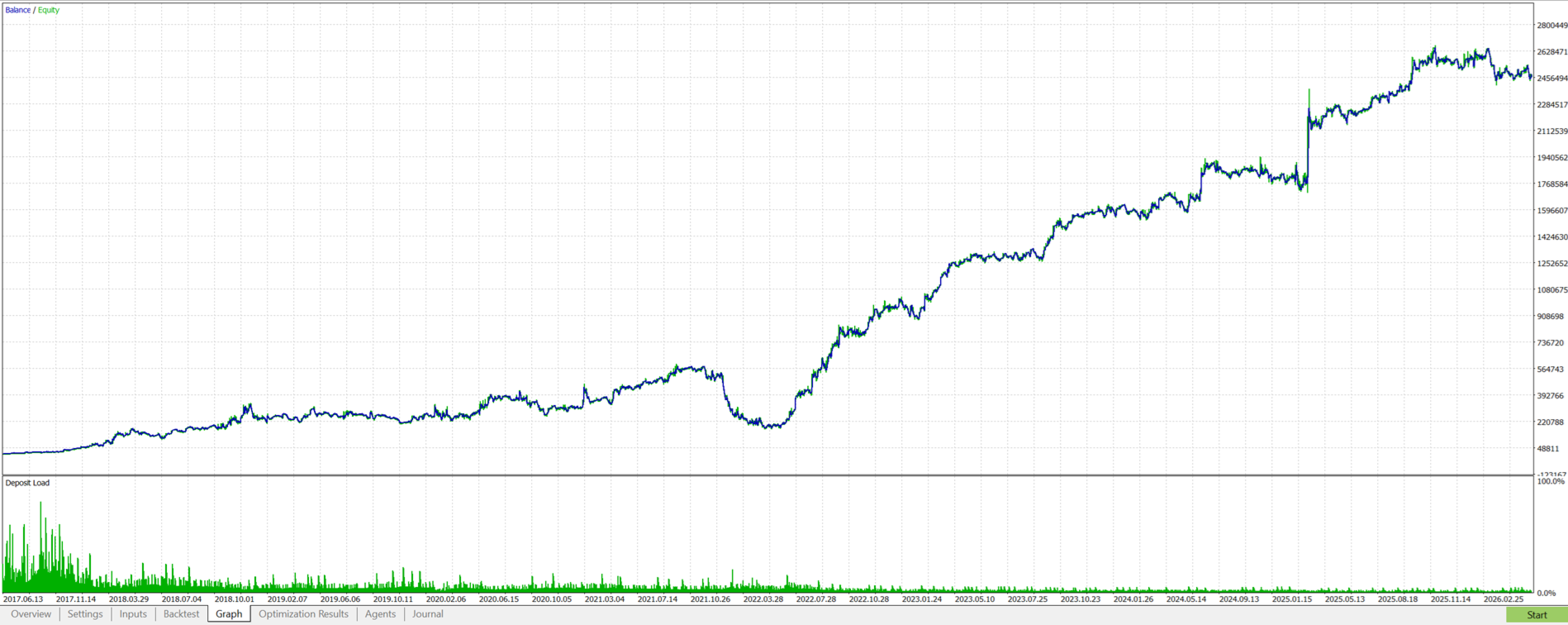

Latest backtest on US500 with the v3 engine (Opening-Range Breakout + end-of-day reversal module), Jun 2017 - Jun 2026 (~9 years, 98% modelling quality), starting deposit $10,000, on the high-risk profile with risk-based compounding:

| Total net profit* | Total return* | CAGR* | Profit factor* | Sharpe ratio* |

|---|---|---|---|---|

| $2,456,049 | +24,560% | ~84% | 1.25 | 3.41 |

That turned $10,000 into roughly $2,466,000 over ~8,506 trades (win rate ~52%, recovery factor 5.81). The trade-off is a deep maximum drawdown of ~70% - this is the high-risk profile (Risk profile = Very high), which maximizes growth at the cost of large equity swings.

This EA ships configured for the MEDIUM risk profile (see the RavenQuant_Daybreak_US500_Production_MEDIUM.set preset). The medium profile trades the exact same logic with a smaller exposure ceiling, so expect proportionally lower profit AND a substantially smaller drawdown with a smoother curve. The figures above are the high-risk ceiling, not the shipped default. Backtests are historical, not a promise (see disclaimer).

How to start

- Load the ready-made preset RavenQuant_Daybreak_US500_Production_MEDIUM.set (in the Strategy Tester / EA inputs use "Load").

- Attach RavenQuant Daybreak to a US500 chart (timeframe M15 or finer).

- Set the broker time (see Setup) and confirm the session window on the on-chart panel.

- Pick your risk profile and risk % to match your account and risk tolerance.

- Run it live on a VPS, preferably close to your broker's server.

Note on session times: the preset is set for a typical EET broker (winter GMT+2). Because brokers use different server times and daylight-saving rules, the session hours may need slight fine-tuning for your broker - set your broker's winter GMT offset (or use "Server time" mode) and confirm the window shown on the on-chart panel. See the manual for per-broker examples.

Setup

| Item | Recommendation |

|---|---|

| Symbol / pair | US500 (S&P 500 index CFD) |

| Chart timeframe | M15 or finer (the EA uses its own internal timeframes) |

| Broker | Low-cost / low-spread (e.g. ICT Trading, Fusion Markets); EET brokers work great |

| Account type | Hedging (required for order splitting & pyramiding; netting merges them into one position) |

| VPS | Recommended - preferably close to the broker's server |

| Minimum balance | Works from small deposits (a few hundred $) on low-risk profiles or fixed lot; larger balances compound faster. |

| Leverage | 1:100+ (1:200 comfortable for higher risk profiles) |

Broker time: enter session times in New York (ET) and set your broker's winter GMT offset - or, if your broker's clock is already on New York time, just use "Server time" mode and type the hours directly. Full examples in the manual.

Sample time config (by broker server clock)

The session is defined in New York (ET) time; the EA converts it to your broker's server clock. The offset you enter is your broker's server timezone - the time shown in MetaTrader's Market Watch - not the country you live in. You always type the ET hours (09:00 / 10:00 / 15:30); the EA does the conversion.

| Broker server clock | Time reference | Winter GMT offset | EU daylight saving |

|---|---|---|---|

| EET - GMT+2 winter (most brokers, incl. Capital.com) | New York time | 2 | true |

| New York (ET, e.g. US brokers) | Server time | - (ignored) | - (ignored) |

| London (UK, GMT+0 winter) | New York time | 0 | true |

| Central Europe / Spain (CET, GMT+1 winter) | New York time | 1 | true |

Your location does not matter - only your broker's server clock does. Example: if you live in Spain but trade through a broker whose server is EET/GMT+2 (like Capital.com), use offset 2 (the top row) - not the CET row. To find your offset, open Market Watch, read the server time, compare to UTC, and round to the whole hour (measured in summer, subtract 1 for the winter offset). Then confirm the window shown on the on-chart panel.

Recommended settings (US500)

The EA ships with these as defaults, so a fresh load is already production-ready:

| Setting | Value |

|---|---|

| Time reference | New York time (set your broker winter GMT offset) |

| Range build start / end | 09:00 / 10:00 |

| Close-all time | 15:30 |

| Position sizing | Lot per balance |

| Risk % per trade | 5.0 |

| Risk profile | Medium (balanced); High/Very high for aggressive growth, Low/Very low for smoother equity |

| Exit mode | Breakeven + trailing |

| Breakeven / Trailing / Step / Hard TP | 2.0 / 1.0 / 1.5 / 4.0 |

Key features

- Very easy to use - install on the chart, pick a risk profile, done.

- Hard stop loss and take-profit logic on every trade.

- No grid / no martingale / no reckless risk management.

- Strong results over the full available US500 history.

- Beats the broker lot cap via automatic order splitting.

- Prop-firm friendly with selectable drawdown via risk profiles.

- Works on small accounts too - from a few hundred dollars on low-risk profiles or fixed lot; scales up smoothly as you add capital.

Documentation

Risk disclaimer. *Performance figures are hypothetical results from a historical backtest of the EA on its highest (Very high) risk profile - not the medium profile this product ships with (US500, Jun 2017 - Jun 2026, 98% modelling quality, $10,000 starting deposit, risk-based compounding, ~70% maximum drawdown). They do not represent real trading and were obtained with the benefit of hindsight. Past and simulated performance is not indicative of future results. High returns come with significant equity swings and a real risk of substantial loss; lower-risk profiles trade more conservatively. Trading leveraged products such as CFDs and indices carries a high level of risk. RavenQuant Daybreak is a trading tool, not financial advice or a guarantee of profit. Only trade with money you can afford to lose.

RavenQuant Daybreak - Intraday Volatility Breakout (US500) - MetaTrader 5 - (c) 2026 RavenQuant