Why My EA Scored 79.6 on AntiOverfit PRO while Others Fail: A Deep Dive into Quantitative Robustness

Introduction: The "Holy Grail" Illusion

In the MQL5 Market, thousands of Expert Advisors claim a 90% win rate and a near-vertical equity curve. To the untrained eye, these look like the "Holy Grail" of trading. However, professional quantitative traders know a bitter truth: Most of these EAs are victims of "Overfitting" or "Curve Fitting." They are meticulously tuned to match a specific historical price path that will never repeat in exactly the same way.

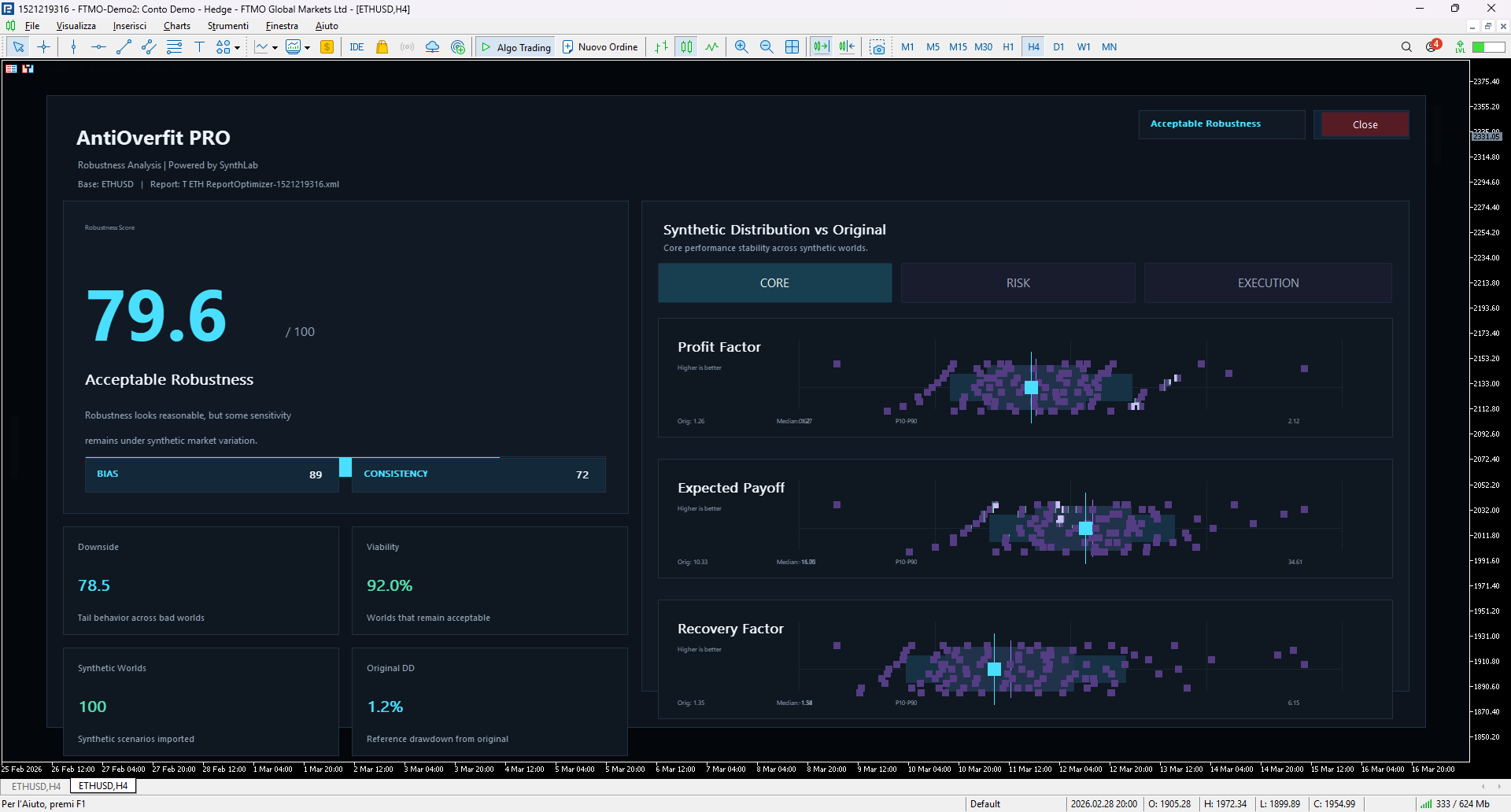

When these over-optimized systems face the real market—or a synthetic stress test—they crumble. This is why I was thrilled when a professional user recently tested my Turtle Trading Pro using AntiOverfit PRO, a leading-edge utility designed to detect algorithmic manipulation.

The result? A score of 79.6 on ETHUSD, and consistently high marks across XAUUSD and Forex. In an industry where most EAs struggle to reach a score of 60, this is a significant milestone. This article explores the science behind this robustness and why the "Turtle" logic remains superior in 2025.

Part 1: What is "Anti-Overfitting" and Why Does It Matter?

Standard MetaTrader backtesting tells you what would have happened on one specific historical path. But what if the market had opened 10 pips lower? What if the volatility in 2024 had started two months earlier?

AntiOverfit PRO uses a methodology similar to Monte Carlo Permutations but on steroids. It creates hundreds of "Synthetic Worlds"—plausible alternative market paths based on the statistical DNA of the real market.

-

A Score < 60: Indicates the EA is "Curve Fitted." It only wins because it "memorized" the specific past price action.

-

A Score > 70: Indicates "Acceptable Robustness." The EA’s logic is based on universal market principles that work across multiple parallel realities.

The 79.6 score achieved by Turtle Trading Pro on ETHUSD proves that its profitability isn't an accident of history; it’s a result of sound mathematical engineering.

Part 2: The Three Pillars of Robustness in Turtle Trading Pro

Why did Turtle Trading Pro succeed where others failed? The secret lies in its refusal to "guess" the price. Instead, it calculates Value and Momentum.

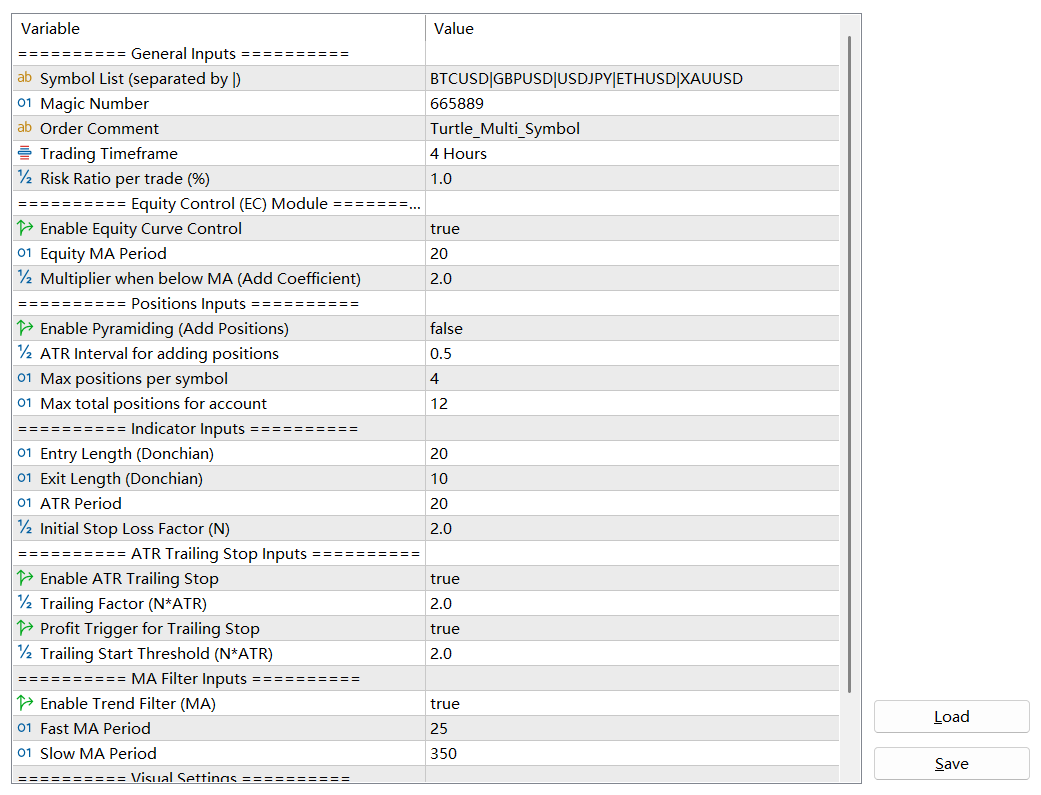

1. The N-Value (ATR) Volatility Anchor

Most EAs use a fixed pip stop-loss (e.g., 30 pips). This is a death sentence for robustness. A 30-pip move in a quiet market is a major reversal, but in a volatile market, it’s just noise.

Turtle Trading Pro uses the ATR-based N-Value to calculate every position.

-

In high-volatility periods, the EA widens stops and reduces lot sizes.

-

In low-volatility periods, it tightens stops and increases lot sizes.

This ensures the dollar-risk per unit of volatility remains constant, allowing the EA to pass synthetic tests that fluctuate in volatility.

2. Donchian Breakout: The Purest Trend Logic

Breakout trading is inherently robust because it doesn't rely on lagging indicators. A breakout above a 20-day high is a factual statement of market strength. By using modernized Donchian channels, Turtle Trading Pro aligns itself with the path of least resistance. Synthetic market tests cannot "trick" a breakout system easily because the logic is binary: If the barrier breaks, the trend starts.

3. The EMA 25/350 Institutional Filter

To achieve a score above 70, an EA must have an "Anchor." We use a Dual-EMA (25 and 350 periods) on the H1/H4 timeframes. This ensures that the EA only takes breakouts that are aligned with long-term institutional flow. By ignoring "counter-trend" noise, the EA avoids the "churn" that usually ruins an overfitted system's equity curve during synthetic stress tests.

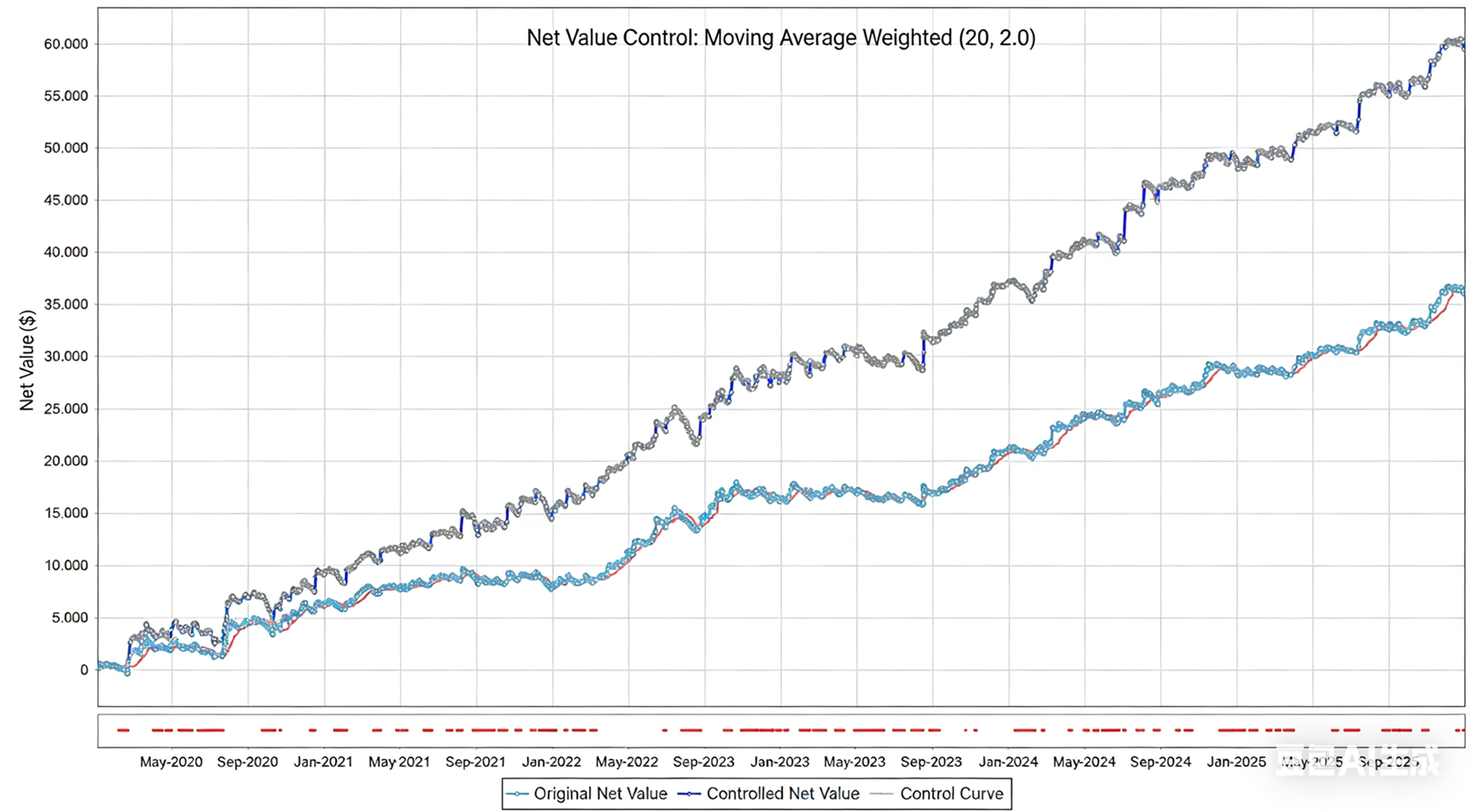

Part 3: Equity Control (EC)—The Autonomous Layer

A major factor in our high scores is the Equity Control Module. While standard EAs continue trading blindly through their own drawdowns, Turtle Trading Pro (EC Edition) monitors its own performance curve.

When the system recognizes it is "out of sync" with current market conditions (Equity < Equity MA), it reduces risk. When it’s "in sync," it boosts the recovery. This "self-awareness" is what professional traders look for in a "Non-Manipulative" system. It treats the equity curve as a secondary asset to be traded with discipline.

Part 4: Prop Firm Readiness—Why Robustness is Non-Negotiable

For traders using FTMO, Topstep, or other Prop Firms, robustness is the difference between a payout and a banned account. Prop Firms look for "Consistent Trading Behavior."

-

Overfitted EAs often produce "random" spikes that flag risk management systems.

-

Robust EAs, like Turtle Trading Pro, show a clear relationship between risk and reward.

Based on feedback from professional users, we are now introducing a Trade Randomization Module. This adds a subtle "jitter" to entry times and slippage parameters (within milliseconds and points), ensuring that each user has a unique "Digital Footprint." This is the ultimate evolution for the Prop Firm environment, combining our 79.6 robustness score with account-level anonymity.

Conclusion: The Era of Transparency

The "Price is too low" comment from our users is a testament to the value of transparency. In a market full of "black boxes," Turtle Trading Pro stands as a transparent, high-robustness tool designed for those who understand that trading is a game of probabilities, not certainties.

We don't promise 100% win rates. We promise a system that has been scientifically proven to be non-manipulative, robust, andcross-asset ready.

🔗 Explore the System: Turtle Trading Pro on MQL5 Market

")

![[XAUUSD]: Weekly Liquidity Activation Points (timings), June 22-26, 2026](https://c.mql5.com/6/1013/splash-preview-771790.png "[XAUUSD]: Weekly Liquidity Activation Points (timings), June 22-26, 2026")