Fundamental Forecast for Australian Dollar: Neutral

Wild Week For The Aussie

After hitting a fresh 2014 high during Tuesday’s session and briefly probing above the 95 US cent handle, the Australian Dollar ended the week as the worst performer against its US counterpart. While a dismal set of trade balance figures took the wind out of the currency’s sails, the real blows came from a fresh round of AUD jawboning by RBA Governor Glenn Stevens and a bumper set of US Non-Farm Payrolls data. The sharp decline on Thursdays was the largest pip value fall for the AUD/USD this year.

Australian Data Unlikely To Shift RBA Policy Expectations

June employment figures headline the docket for local data over the

week ahead with economists tipping a tick higher in the unemployment

rate to 5.9 percent. An upside surprise to the jobs added figure or

unanticipated decline in the headline unemployment rate could yield a

spike higher for the Aussie. However, follow-through may prove limited,

given the Reserve Bank of Australia is unlikely to shift their policy

preference until more consistent signs of progress in the labor market

are witnessed.

Local Consumer and Business Confidence figures as well as Housing Finance

data round out the noteworthy economic data on tap for the week. While

consumer sentiment has sagged over the first half of the year,

business confidence has shown some surprising resilience. On balance

the leading indicators paint a patchy picture of the health of the

Australian economy, which reinforce the notion that the cash rate is

set to remain on hold over the near-term.

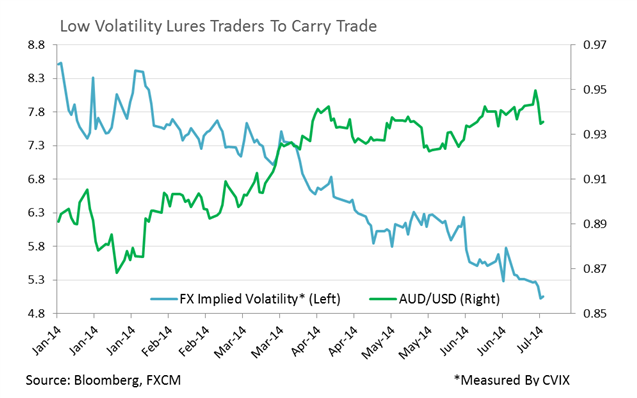

Low Vol. Environment Offers Aussie A Source of Support

One of the important themes that continues to offer the high-yielding

currencies their bearings is the persistent low volatility environment,

which has raised the appeal of the carry trade. Implied volatility in

the FX market (measured by CVIX) hit a fresh low this week, suggesting

traders are pricing in a low probability of a major economic disruption

occurring in the near-term, which may continue to lure traders to the

Aussie.

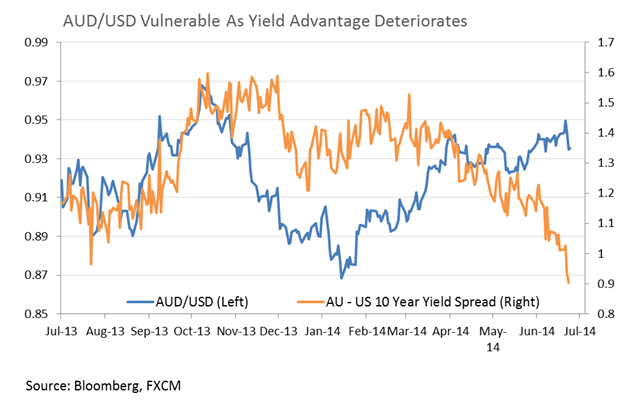

However, as investors have continued to pile into the long Aussie trade

over the past several months, the currency’s yield advantage over its

US counterpart has weakened considerably. The Australian 10 year bond

spread narrowed to its lowest since October 2006 on Friday (see chart

below). This makes the carry trade a relatively less attractive

proposition, which may in turn reduce investor’s appetite for the

Aussie.

")