Foreign Exchange Arbitrage

Arbitrage exploits a price difference between two or more markets to make money with zero risk.

Sporting bets are perhaps the easiest example. Given a sporting event with two possible outcomes you look for an opportunity where two book makers give slightly different odds and try to expoit it. For example, consider a case with two outcomes, say Federer vs. Nadal. One bookie offers odds of 5/2 on Federer, whereas another offers odds of 3/5 on Nadal. If I bet £32 on 5/2, and £68 at 3/5 then regardless of the outcome I'm guaranteed to make a little money (a minimum of 8% in this case. £32 at 5/2 odds gives me $112 and £68 at 3/5 gives me £108). Wikipedia's page on arbitrage betting explains it better than I can!

Foreign exchange (forex) markets are another opportunity for the arbitrageur. By finding mispriced currencies you can get money for nothing. For example I could transfer my money from GBP to USD via CHF and end up with a profit if someone got these exchange rates wrong! Now all I need to do is find a way of finding these opportunities and I'll be rich!

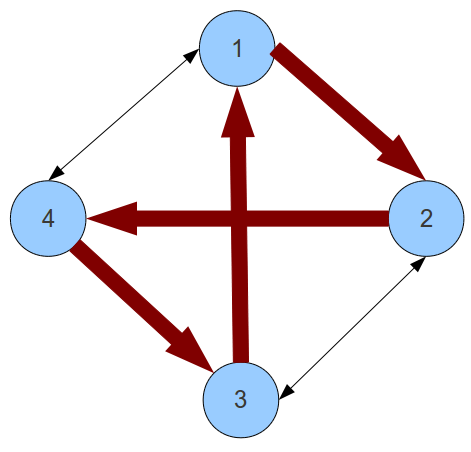

In the graph below we can make a trade 1 -> 2 -> 4 -> 3 -> 1 and make a profit.

- A recurrence relation or recursive algorithm for expressing the answer

- Show that the recursive version is bounded by a small polynomial

- An order of evaluation for the reccurence that means you always have partial results available when you need them.

We can define the arbitrage problem recursively. First we label the nodes as being number from 1 to N. TheshortestPath(i,j,k) gives the shortest path from i to j using only nodes 1 to k as intermediate nodes. The base case is shortestPath(i,j,0) where the value is simply the edge weight between i and j. The recursive relation isshortestPath(i,j,k) = min(shortestPath(i,j,k-1), shortestPath(i,k,k-1) + shortestPath(k,j,k-1). The recurrence relation just says that each new node that we consider only helps if there is a shortest path that goes through it.

In order to code this up in Haskell we'll need some representation of a graph. A graph is simply a collection of vertices and some edges. In order to make things easier I've said that each vertice should be an enum and have an integer representation.