Here we are. It’s June 23rd and everything is set for the big drama: the EU In/Out Referendum. Here are the levels for the day after, when we will get the results.

Here is their view, courtesy of eFXnews:

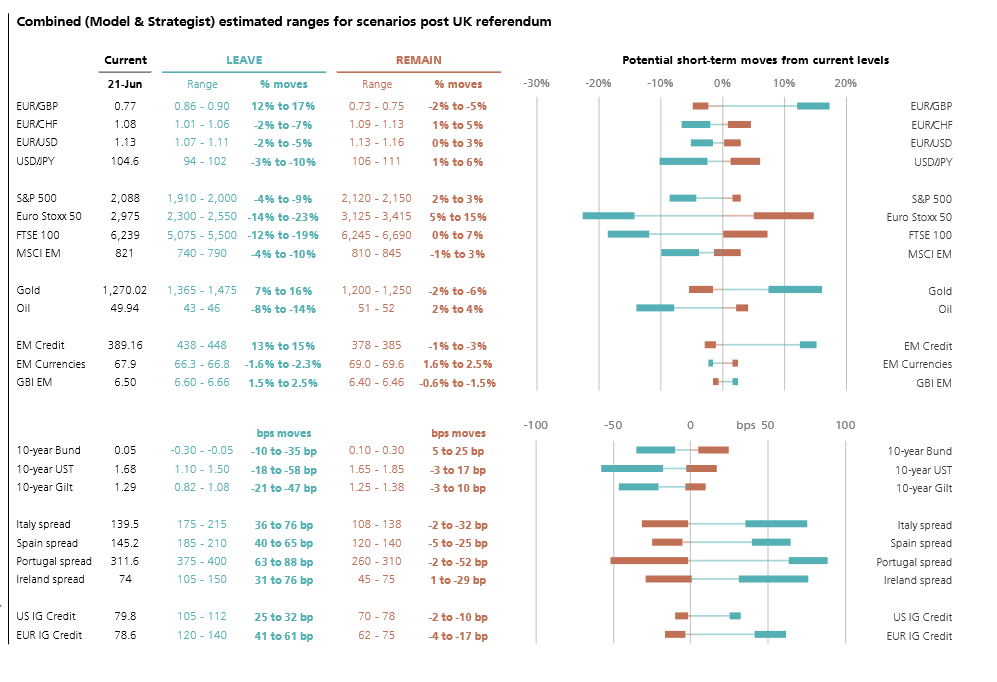

In an attempt to reduce the uncertainty, we try to benchmark “levels for the day after”. To be sure, we are not trying to predict where markets will trade in the hours that follow such a big event. There could be liquidity-driven dislocations, price spikes and large reversals. Rather, we attempt to answer a slightly easier question: at what level would we buy or sell each key asset class upon a Remain and a Leave scenario? At what level are the relevant risks likely priced in?

To do this, we ran a simple exercise. First, we computed a simple, model-based simulation across assets. The main assumption of this exercise was that the relationships between market-based “probabilities” of Brexit, the level of EUR/GBP, and the pricing of risks across assets persist. This served as a base-case. Then, we surveyed our strategists, who offered a more informed view of the balance of risks to different assets on a fundamental basis. The table on the following page shows the average range based on the two exercises.

In short:

1. In a vote to leave, GBP would come under significant pressure, while risk currencies (CHF and JPY) benefit. Potential policy responses limit the degree of strength. We expect the effects on EUR/USD to be relatively muted.

2. The payout for Bonds is asymmetric. In a vote to remain, yields would rise but not significantly, and mostly in the Euro-area core. Upon “Leave”, the path of least resistance is for yields to drop substantially, especially in the UK & the US.

3. The bond yield/policy cushion, combined with the healthy distance from the macro shock, implies less downside for the S&P than for the FTSE or Eurostoxx upon “Leave”. Upon “Remain”, the S&P could plausibly make fresh highs.

4. Euro-area periphery yields and corporate credit spreads have significant room to widen in a decision to leave, although temporarily perhaps before a policy response is triggered. The upside is capped in an event to “stay”.

5. Risk sentiment swings may affect emerging market assets, but much less so relative to Euro-area and UK assets, given the cushion from lower US yields.

6. Lastly, we anticipate limited pass-through to Oil prices. The broad decline in US real rates creates more upside than downside in Gold prices.

")