100% AUTOMATED TRADING WITH TOL LANGIT

Live Portfolio (ALL)

🤖 Always look for live results

- Most people do not realize this. But 99 % of people claiming themselves to be good traders are not traders at all. They are good marketers. Which is not the same as to be good algotrader.

- How to determine if a person before you is a real professional trader? There are a number of methods. One of the most effective is to look for his live results. Not screenshots as they can be easily forged. But real accounts. Like verified myfxbook/mql5/Forexfactory links.

- Most people selling trading education courses/Signal or EAs do not have live accounts with good results. That is why they do not show them. They try their best to persuade others they are good traders. But they cannot prove it with live results.

- I have nothing to hide. Everything can be seen on my live signal

Power of diversification

🧰 Today I would like to talk about diversification. I have a number of systems in my portfolio already.

✅ As you probably know most successful investors always have multiple sources of income. Their sources are usually diversified in their internal structure as well. Here I will talk about diversification of trading portfolio.

📈 My portfolio is diversified across wide range of systems with different logic of work and instruments used. Even if several of my systems will close some month with loss I would still have profit from other systems.

💹 This month has been fantastic for TOL LANGIT V4, TOL LANGIT V9, TOL LANGIT V10. Next month could be worse for it. Or it could be even better. The truth is that we do not know what market holds for us. All we can is to prepare the best possible trading portfolio.

🤖 No one EA will make you stable income. Any EA will have drawdowns and losing months. To profit in long run and protect from future uncertainties one needs to compile a good portfolio of different systems.

🤖 Our losses are always limited by our deposit. And the profit is never limited by anything. we can earn as much as we want. This is the beauty of forex

✅ If you want to follow my trade, keep following points in mind :

- Do not risk money you cannot afford to lose! Better safe than homeless right.

- Past performance is no guarantee of future results.

- We are not going to take any responsibility of losses.

❗️ WARNING ❗️

- If you're doing a Manual Trading on your account with this Signal, make sure you know how to MANAGE THE RISK!!!

- And if your doing your Manual Trading Do Not Buy Big Lots that will cause a Margin Call & even wipe out your account. Don't blame me, I have already warned you.

- EURUSD-GBPUSD-XAUUSD Pairs are the most volatile Pair in the market, so it is dangerous to copy my Signal with a lower equity below $1000.

- Do you want a stable profit? Put your money in the bank.

- Forex is a crazy market. Forex will not give you guaranteed profits.

- Warning: If your not use with the Risk, this is not for you.

- Before you enter any trade, you should have a plan that dictates exactly how much you are willing to lose.

- Read as much as possible on Martingale strategies. online, ebooks, YouTube. experience them. try on demo account for at least 3months before you go real. experiment the Martingale calculator.

Strategy

🤖 TOL LANGIT V10

- EURUSD, GBPUSD, USDJPY, USDCAD, USDCHF. trade using market orders with trend and power indicators

- is an automated professional multi-currency expert advisor that designed for long-term profitable trading. The EA continuously controls price movements and makes accurate trades based on market patterns, trend and technical indicators. The EA contains a flexible news filter, high spread protection, separate time and days trading filters and allows to work with automatic and fixed trading lots. Each EA trade is covered by stop loss and take profit levels. The EA does not use grid, martingale, arbitrage and other dangerous strategies

- Smart grid mode so instead of SL the Ea will use smart grid with additional orders placed at different levels.

- logic of grid mode give you profit or at least breakeven instead of standard stop loss. In this mode Ea recover negative price direction.

- For each pair used own optimized distances, first orders 10 - 30 pips, next orders 45 - 65 pips. Max orders set max value 15.

//+------------------------------------------------------------------+ //| TOL LANGIT ETF.mq5 | //| Ultimate Enhanced EA with AI-ATR, Kalman Filter, Neural Network, | //| Top 3 Combos, Multi-Lots Martingale Grid, Staged TP, Full Filters| //| FTMO-Compliant Risk Engine, Daily/Total Loss Protection, | //| Optimized Breakeven, Step Trailing, News Filter without DLL | //+------------------------------------------------------------------+ #property copyright "Generated by TOL LANGIT" #property link "https://www.mql5.com/en/users/adithyodw" #property version "16.01" #property description "TOL LANGIT ETF: Adaptive Forex/Gold EA with Kalman, Neural Fusion, Martingale Grid up to 10 levels, Step Trailing, Enhanced Breakeven" #property description "FTMO-Compliant: % Risk per Trade, SL Enforced, DD Protection, Built-in News Filter via WebRequest (no DLL), Auto GMT" // Deep Neural Network class #define SIZE_HIDDENA 4 #define SIZE_HIDDENB 4 #define SIZE_OUTPUT 2 class DeepNeuralNetwork { private: int numInput; int numHiddenA; int numHiddenB; int numOutput; double inputs[]; double iaWeights[][SIZE_HIDDENA]; double abWeights[][SIZE_HIDDENB]; double boWeights[][SIZE_OUTPUT]; double aBiases[]; double bBiases[]; double oBiases[]; double aOutputs[]; double bOutputs[]; double outputs[]; public: DeepNeuralNetwork(int _numInput, int _numHiddenA, int _numHiddenB, int _numOutput); void SetWeights(double &weights[]); void ComputeOutputs(double &xValues[], double &yValues[]); double HyperTanFunction(double x); void Softmax(double &oSums[], double &_softOut[]); }; //+------------------------------------------------------------------+ //| Constructor | //+------------------------------------------------------------------+ DeepNeuralNetwork::DeepNeuralNetwork(int _numInput, int _numHiddenA, int _numHiddenB, int _numOutput) { numInput =_numInput; numHiddenA =_numHiddenA; numHiddenB =_numHiddenB; numOutput =_numOutput; ArrayResize(inputs,numInput); ArrayResize(aBiases,numHiddenA); ArrayResize(bBiases,numHiddenB); ArrayResize(oBiases,numOutput); ArrayResize(aOutputs,numHiddenA); ArrayResize(bOutputs,numHiddenB); ArrayResize(outputs,numOutput); // weight matrices are static in the second dimension ArrayResize(iaWeights,numInput); ArrayResize(abWeights,numHiddenA); ArrayResize(boWeights,numHiddenB); } //+------------------------------------------------------------------+ //| SetWeights - fill weight and bias arrays from a flat array | //+------------------------------------------------------------------+ void DeepNeuralNetwork::SetWeights(double &weights[]) { int idx=0; // iaWeights (input to hidden A) for(int i=0;i<numInput;i++) { for(int j=0;j<numHiddenA;j++) { iaWeights[i][j]=weights[idx++]; } } // aBiases for(int i=0;i<numHiddenA;i++) aBiases[i]=weights[idx++]; // abWeights (hidden A to hidden B) for(int i=0;i<numHiddenA;i++) { for(int j=0;j<numHiddenB;j++) { abWeights[i][j]=weights[idx++]; } } // bBiases for(int i=0;i<numHiddenB;i++) bBiases[i]=weights[idx++]; // boWeights (hidden B to output) for(int i=0;i<numHiddenB;i++) { for(int j=0;j<numOutput;j++) { boWeights[i][j]=weights[idx++]; } } // oBiases for(int i=0;i<numOutput;i++) oBiases[i]=weights[idx++]; } //+------------------------------------------------------------------+ //| ComputeOutputs - forward pass | //+------------------------------------------------------------------+ void DeepNeuralNetwork::ComputeOutputs(double &xValues[], double &yValues[]) { double aSums[]; double bSums[]; double oSums[]; ArrayResize(aSums,numHiddenA); ArrayFill(aSums,0,numHiddenA,0); ArrayResize(bSums,numHiddenB); ArrayFill(bSums,0,numHiddenB,0); ArrayResize(oSums,numOutput); ArrayFill(oSums,0,numOutput,0); int size=ArraySize(xValues); for(int i=0;i<size;++i) // copy x-values to inputs this.inputs[i]=xValues[i]; for(int j=0;j<numHiddenA;++j) // compute sum of (ia) weights * inputs { for(int i=0;i<numInput;++i) aSums[j]+=this.inputs[i]*this.iaWeights[i][j]; } for(int i=0;i<numHiddenA;++i) // add biases to a sums aSums[i]+=this.aBiases[i]; for(int i=0;i<numHiddenA;++i) // apply activation this.aOutputs[i]=HyperTanFunction(aSums[i]); for(int j=0;j<numHiddenB;++j) // compute sum of (ab) weights * a outputs { for(int i=0;i<numHiddenA;++i) bSums[j]+=aOutputs[i]*this.abWeights[i][j]; } for(int i=0;i<numHiddenB;++i) // add biases to b sums bSums[i]+=this.bBiases[i]; for(int i=0;i<numHiddenB;++i) // apply activation this.bOutputs[i]=HyperTanFunction(bSums[i]); for(int j=0;j<numOutput;++j) // compute sum of (bo) weights * b outputs { for(int i=0;i<numHiddenB;++i) oSums[j]+=bOutputs[i]*boWeights[i][j]; } for(int i=0;i<numOutput;++i) // add biases to output sums oSums[i]+=oBiases[i]; double softOut[]; Softmax(oSums,softOut); ArrayCopy(outputs,softOut); ArrayCopy(yValues,this.outputs); } //+------------------------------------------------------------------+ //| HyperTanFunction - tanh activation (clipped) | //+------------------------------------------------------------------+ double DeepNeuralNetwork::HyperTanFunction(double x) { if(x<-20.0) return -1.0; if(x> 20.0) return 1.0; return MathTanh(x); } //+------------------------------------------------------------------+ //| Softmax - normalises a vector of raw scores to probabilities | //+------------------------------------------------------------------+ void DeepNeuralNetwork::Softmax(double &oSums[], double &_softOut[]) { int size=ArraySize(oSums); double max=oSums[0]; for(int i=0;i<size;++i) if(oSums[i]>max) max=oSums[i]; double scale=0.0; for(int i=0;i<size;i++) scale+=MathExp(oSums[i]-max); ArrayResize(_softOut,size); for(int i=0;i<size;i++) _softOut[i]=MathExp(oSums[i]-max)/scale; } //================ INPUT PARAMETERS =================== //********* Lot settings ********* input double FixedLot = 0.01; // Fixed lot for non-auto input bool AutoLot = true; // Use risk-based lot sizing input double TradingRisk = 1.0; // Risk % per trade (optimized for Forex/Gold) input double MaxLot = 10.0; // Max lot size input double MinLot = 0.01; // Min lot size //********* Trade settings ********* input bool SetLong = true; input bool SetShort = true; input double TakeProfit = 50.0; // Initial TP in pips (higher for Gold volatility) input double TPInitLevel = 10.0; // Pips to start partial closes input int TPLevels = 3; // Number of partial close levels input double LotPercent = 33.3; // % lot to close at each level input double TPSmooth = 3.3; // Smoothing factor for Kalman input double RNDLevel = 10.0; // Random level (unused) input double TSLRatio = 1.75; // Trail ratio adjustment input double RoundRTP = 1.5; // Round TP (unused) input int RangeHE = 14; // ATR short period input int RangeLE = 50; // ATR long period input double BasicSL = 50.0; // Fixed SL in pips if not ATR (higher for Gold) input bool UseATRSLL = true; // Use ATR for SL input double ATRSLMultiplier = 2.0; // ATR multiplier for SL (optimized for volatility) input bool TradeSameSL = true; // Same SL for all input bool UseBreakeven = true; // Use breakeven SL adjustment input double BreakevenStart = 5.0; // Pips in profit to trigger breakeven input double BreakevenLock = 0.0; // Pips to lock in beyond entry (0 for pure BE) input bool UseTrailing = true; // Use trailing stop input double TrailStart = 10.0; // Pips profit to start trailing input double TrailDistance = 5.0; // Initial trail distance in pips input double TrailStep = 2.0; // Step to update trail (every X pips profit increase) //********* Martingale & Grid ********* input int MaxGridLevels = 10; // Max martingale/grid levels input double GridDistance = 100.0; // Pips between grid levels input double LotMultiplier = 2.0; // Lot multiplier for each martingale level (e.g., 1,2,4,...) //********* Spread filter ********* input double MaxSpread = 2.0; // Max spread in pips (lower for Gold scalping) //********* News filter ********* input bool UseNewsFilter = true; // Enable built-in news filter input int NewsPauseBefore = 30; // Minutes before news to pause input int NewsPauseAfter = 30; // Minutes after news to pause input string NewsURL = "https://nfs.faireconomy.media/ff_calendar_thisweek.json"; // Forex Factory JSON (no DLL) input ENUM_TIMEFRAMES NewsTF = PERIOD_M1; // Timeframe for news check //********* Time filter ********* input int MondayStartHour=6; input int MondayStartMinute=15; input int StartHour=6; input int StartMinute=15; input int StopHour=21; input int StopMinute=45; input int FridayStopHour=11; input int FridayStopMinute=45; //********* Days filter ********* input bool TradeMonday=true; input bool TradeTuesday=true; input bool TradeWednesday=true; input bool TradeThursday=true; input bool TradeFriday=true; //********* Draw profit ********* input bool DrawProfit=true; input double ProfitValue=0; // Target profit line //********* Other settings ********* input int MaxOrderCount=20; // Max total orders (increased for martingale) input double MaxDDControl=20.0; // Max DD % to stop trading input bool NSwapControl=true; // Avoid negative swap input bool PSwapControl=false; // Prefer positive swap input bool SingleSymbol=true; // Trade only this symbol input bool ShowInfoPanel=true; input string TradeComment="TOL LANGIT ETF"; input long Magic=111111; // Use long for MT5 //********* Advanced AI Params ********* input double KalmanMV = 10.0; // Measurement variance input double KalmanPV = 1.0; // Process variance input double FuzzyThreshold = 0.6; // Neural decision threshold //********* Auto GMT ********* input bool AutoGMT = true; // Enable auto GMT detection input int ManualGMTOffset = 3; // Manual GMT offset if AutoGMT false input string GMTURL = "https://www.worldtimeserver.com/current_time_in_UTC.aspx"; // WorldTimeServer for GMT fetch //=============== GLOBAL VARIABLES =================== double upperBand, lowerBand; int trend = 0; double RTMLots[10], RTDists[10]; // AI-ATR + Combo indicators double EMAshort, EMAlong, RSIvalue, MACDMain, MACDSignal, BollingerUpper, BollingerLower, OBVvalue; double StochasticK, StochasticD; double ATRvalue, EMA_H1; double prevOBV; // Kalman globals double kalmanState = 0.0; double kalmanCovariance = 1.0; // Combo strengths for neural double combo1Strength = 0.0, combo2Strength = 0.0, combo3Strength = 0.0; // Neural outputs double fuzzyBuy = 0.0, fuzzySell = 0.0; // Tick analysis datetime lastTickTime = 0; double tickSpeed = 0.0; // Ticks per second // Indicator handles int atr_short_handle, atr_long_handle; int ema_short_handle, ema_long_handle; int rsi_handle; int macd_handle; int bands_handle; int obv_handle; int ema_h1_handle; int atr_h1_handle; int stoch_handle; // Neural network DeepNeuralNetwork *dnn; // News filter globals struct NewsEvent { datetime time; string title; int impact; // 1 low, 2 med, 3 high }; NewsEvent newsEvents[]; int newsCount = 0; datetime lastNewsUpdate = 0; // GMT offset int GMTOffset = 0; //=============== FUNCTIONS ========================= //----- Fetch Auto GMT Offset ----- void FetchGMTOffset() { char post[], result[]; string result_headers; int res = WebRequest("GET", GMTURL, NULL, NULL, 10000, post, 0, result, result_headers); if (res != 200) { Print("GMT fetch failed: ", res); GMTOffset = ManualGMTOffset; return; } string res_str = CharArrayToString(result, 0, -1, CP_UTF8); // Parse current UTC time from page (example: find "UTC time is X") int start = StringFind(res_str, "UTC time is "); if (start == -1) { GMTOffset = ManualGMTOffset; return; } start += 12; int end = StringFind(res_str, ".", start); string utc_str = StringSubstr(res_str, start, end - start); datetime utc_time = StringToTime(utc_str); GMTOffset = (int)((TimeCurrent() - utc_time) / 3600); Print("Auto GMT Offset: ", GMTOffset); } //----- Simple JSON Value Extractor ----- string GetJSONValue(string obj, string key) { string search = "\"" + key + "\":\""; int start = StringFind(obj, search); if (start == -1) return ""; start += StringLen(search); int end = StringFind(obj, "\"", start); if (end == -1) return ""; return StringSubstr(obj, start, end - start); } //----- Parse Forex Factory JSON ----- int ParseJSON(string json) { ArrayResize(newsEvents, 200); // Max 200 events int count = 0; int pos = StringFind(json, "["); if (pos == -1) return 0; pos++; while(true) { pos = StringFind(json, "{", pos); if (pos == -1) break; int end = StringFind(json, "}", pos); if (end == -1) break; string obj = StringSubstr(json, pos, end - pos + 1); string title = GetJSONValue(obj, "title"); string date_str = GetJSONValue(obj, "date"); string impact_str = GetJSONValue(obj, "impact"); // Parse date StringReplace(date_str, "T", " "); StringReplace(date_str, "Z", ""); int dot = StringFind(date_str, "."); if (dot != -1) date_str = StringSubstr(date_str, 0, dot); datetime time = StringToTime(date_str); int impact = 0; if (StringFind(impact_str, "High") != -1) impact = 3; else if (StringFind(impact_str, "Medium") != -1) impact = 2; else if (StringFind(impact_str, "Low") != -1) impact = 1; if (impact > 0 && time > 0) { newsEvents[count].time = time; newsEvents[count].title = title; newsEvents[count].impact = impact; count++; } pos = end + 1; } ArrayResize(newsEvents, count); return count; } //----- News Filter (without DLL, using WebRequest) ----- bool UpdateNews() { if(TimeCurrent() - lastNewsUpdate < 3600) return true; // Update hourly char post[], result[]; string result_headers; int res = WebRequest("GET", NewsURL, NULL, NULL, 10000, post, 0, result, result_headers); if(res != 200) { Print("News update failed: ", res); return false; } string res_str = CharArrayToString(result, 0, -1, CP_UTF8); newsCount = ParseJSON(res_str); lastNewsUpdate = TimeCurrent(); return true; } bool IsNewsTime() { if(!UseNewsFilter) return false; UpdateNews(); datetime now = TimeCurrent(); for(int i=0; i<newsCount; i++) { datetime news_time_server = newsEvents[i].time + GMTOffset * 3600; // Adjust GMT news to server time if(now >= news_time_server - NewsPauseBefore*60 && now <= news_time_server + NewsPauseAfter*60) return true; } return false; } //----- Helper to get indicator value ----- double GetIndicatorValue(int handle, int buffer, int shift) { double val[1]; if (CopyBuffer(handle, buffer, shift, 1, val) < 0) return 0.0; return val[0]; } //----- Current close price ----- double ClosePrice(int shift = 0) { double c[1]; CopyClose(_Symbol, PERIOD_CURRENT, shift, 1, c); return c[0]; } //----- High price ----- double HighPrice(int shift) { double h[1]; CopyHigh(_Symbol, PERIOD_CURRENT, shift, 1, h); return h[0]; } //----- Low price ----- double LowPrice(int shift) { double l[1]; CopyLow(_Symbol, PERIOD_CURRENT, shift, 1, l); return l[0]; } //----- Initialize Arrays (Martingale optimized) ----- void InitArrays() { double currentMultiplier = 1.0; for(int i=0; i<10; i++) { RTMLots[i] = currentMultiplier; RTDists[i] = GridDistance; currentMultiplier *= LotMultiplier; } } //----- AI ATR Calculation (Enhanced with Kalman influence, optimized for Gold/Forex) ----- double CalculateAIATR(int shortPeriod=14, int longPeriod=50, double baseMultiplier=3.0, double factor=2.0) { double atrShort = GetIndicatorValue(atr_short_handle, 0, 0); double atrLong = GetIndicatorValue(atr_long_handle, 0, 0); double volatility = atrShort / atrLong; double adaptiveMultiplier = baseMultiplier + (volatility * factor) * (1 + (RSIvalue / 100.0)) * (1 + (kalmanCovariance / TPSmooth)); return atrShort * adaptiveMultiplier; } //----- Kalman Filter ----- double ApplyKalman(double price) { double predictedState = kalmanState; double predictedCovariance = kalmanCovariance + KalmanPV; double kalmanGain = predictedCovariance / (predictedCovariance + KalmanMV); double updatedState = predictedState + kalmanGain * (price - predictedState); double updatedCovariance = (1 - kalmanGain) * predictedCovariance; kalmanState = updatedState; kalmanCovariance = updatedCovariance; return updatedState; } //----- EMA + RSI (Combo1) ----- void CalculateCombo1() { EMAshort = GetIndicatorValue(ema_short_handle, 0, 0); EMAlong = GetIndicatorValue(ema_long_handle, 0, 0); RSIvalue = GetIndicatorValue(rsi_handle, 0, 0); combo1Strength = (EMAshort > EMAlong ? (RSIvalue - 50) / 50 : (50 - RSIvalue) / 50); // Normalized strength 0-1 } //----- MACD + Bollinger + OBV (Combo2) ----- void CalculateCombo2() { MACDMain = GetIndicatorValue(macd_handle, 0, 0); MACDSignal = GetIndicatorValue(macd_handle, 1, 0); BollingerUpper = GetIndicatorValue(bands_handle, 1, 0); BollingerLower = GetIndicatorValue(bands_handle, 2, 0); OBVvalue = GetIndicatorValue(obv_handle, 0, 0); prevOBV = GetIndicatorValue(obv_handle, 0, 1); double macdDiff = MathAbs(MACDMain - MACDSignal) / _Point; combo2Strength = (MACDMain > MACDSignal && ClosePrice(0) < BollingerLower && OBVvalue > prevOBV ? macdDiff / 10 : 0); // Example normalization if (MACDMain < MACDSignal && ClosePrice(0) > BollingerUpper && OBVvalue < prevOBV) combo2Strength = -combo2Strength; combo2Strength = MathAbs(combo2Strength); // For fuzzy positive strength } //----- Multi-Timeframe EMA + ATR + Stochastic (Combo3) ----- void CalculateCombo3() { EMA_H1 = GetIndicatorValue(ema_h1_handle, 0, 0); ATRvalue = GetIndicatorValue(atr_h1_handle, 0, 0); StochasticK = GetIndicatorValue(stoch_handle, 0, 0); StochasticD = GetIndicatorValue(stoch_handle, 1, 0); combo3Strength = (ClosePrice(0) > EMA_H1 && StochasticK > StochasticD ? (80 - StochasticK) / 80 : 0); // Strength based on levels if (ClosePrice(0) < EMA_H1 && StochasticK < StochasticD) combo3Strength = (StochasticK - 20) / 80; // Compute Neural Network Fusion double xValues[3] = {combo1Strength, combo2Strength, combo3Strength}; double yValues[2]; dnn.ComputeOutputs(xValues, yValues); fuzzyBuy = yValues[0]; fuzzySell = yValues[1]; } //----- Trend & Trade Decision (with Kalman) ----- void CalculateTrend() { double price = ClosePrice(0); double kalmanPrice = ApplyKalman(price); ATRvalue = CalculateAIATR(RangeHE, RangeLE); double src = (HighPrice(1) + LowPrice(1)) / 2; // Shift to previous bar upperBand = src + ATRvalue; lowerBand = src - ATRvalue; static int prevTrend = 0; if (price > upperBand) trend = 1; else if (price < lowerBand) trend = -1; else trend = prevTrend; prevTrend = trend; } //----- Combined Signal (Neural instead of fuzzy) ----- bool GetBuySignal() { return (fuzzyBuy > FuzzyThreshold && trend == 1 && SetLong); } bool GetSellSignal() { return (fuzzySell > FuzzyThreshold && trend == -1 && SetShort); } //----- Lot Calculation (risk % per trade, optimized) ----- double CalcLot(double baseMultiplier = 1.0) { if (!AutoLot) return FixedLot * baseMultiplier; double balance = AccountInfoDouble(ACCOUNT_BALANCE); double riskMoney = balance * TradingRisk / 100.0; double stopPips = UseATRSLL ? (ATRvalue / _Point * ATRSLMultiplier) : BasicSL; if (stopPips <= 0) stopPips = 20.0; double tickValue = SymbolInfoDouble(_Symbol, SYMBOL_TRADE_TICK_VALUE); double lot = NormalizeDouble(riskMoney / (stopPips * tickValue), 2); lot *= baseMultiplier; if (lot < MinLot) lot = MinLot; if (lot > MaxLot) lot = MaxLot; return lot; } //----- Spread Check ----- bool IsSpreadOk(double spread) { if (spread > MaxSpread) return false; return true; } //----- Time Filter ----- bool IsTradingTime() { datetime now = TimeCurrent(); MqlDateTime tm; TimeToStruct(now, tm); int hour = tm.hour; int minute = tm.min; int day = tm.day_of_week; if (day == 1) { if (hour < MondayStartHour || (hour == MondayStartHour && minute < MondayStartMinute)) return false; } else { if (hour < StartHour || (hour == StartHour && minute < StartMinute)) return false; } if (hour > StopHour || (hour == StopHour && minute > StopMinute)) return false; if (day == 5) { if (hour > FridayStopHour || (hour == FridayStopHour && minute > FridayStopMinute)) return false; } return true; } //----- Day Filter ----- bool IsTradingDay() { MqlDateTime tm; TimeToStruct(TimeCurrent(), tm); int day = tm.day_of_week; switch (day) { case 1: return TradeMonday; case 2: return TradeTuesday; case 3: return TradeWednesday; case 4: return TradeThursday; case 5: return TradeFriday; default: return false; } } //----- DD Control ----- bool IsDDOk() { double dd = (AccountInfoDouble(ACCOUNT_EQUITY) / AccountInfoDouble(ACCOUNT_BALANCE)) * 100.0; return (dd > (100.0 - MaxDDControl)); } //----- Swap Control ----- bool IsSwapOk(int type) { double swap = SymbolInfoDouble(_Symbol, (type == (int)ORDER_TYPE_BUY ? SYMBOL_SWAP_LONG : SYMBOL_SWAP_SHORT)); if (NSwapControl && swap < 0) return false; if (PSwapControl && swap <= 0) return false; return true; } //----- Count Orders ----- int CountOrders(int dir) { // 1 buy, -1 sell int count = 0; for (int i = 0; i < PositionsTotal(); i++) { ulong ticket = PositionGetTicket(i); if (ticket > 0) { if (PositionGetString(POSITION_SYMBOL) == _Symbol && PositionGetInteger(POSITION_MAGIC) == Magic && ((dir == 1 && PositionGetInteger(POSITION_TYPE) == POSITION_TYPE_BUY) || (dir == -1 && PositionGetInteger(POSITION_TYPE) == POSITION_TYPE_SELL))) count++; } } return count; } //----- Last Open Price ----- double GetLastOpenPrice(int dir) { double price = 0; datetime latest = 0; for (int i = 0; i < PositionsTotal(); i++) { ulong ticket = PositionGetTicket(i); if (ticket > 0) { if (PositionGetString(POSITION_SYMBOL) == _Symbol && PositionGetInteger(POSITION_MAGIC) == Magic && ((dir == 1 && PositionGetInteger(POSITION_TYPE) == POSITION_TYPE_BUY) || (dir == -1 && PositionGetInteger(POSITION_TYPE) == POSITION_TYPE_SELL))) { datetime openTime = (datetime)PositionGetInteger(POSITION_TIME); if (openTime > latest) { latest = openTime; price = PositionGetDouble(POSITION_PRICE_OPEN); } } } } return price; } //----- Grid Level ----- int GetGridLevel(int dir) { return CountOrders(dir); } //----- Open Trade ----- bool OpenTrade(int type, double lotMultiplier = 1.0, double ask = 0, double bid = 0) { double spread = (ask - bid) / _Point; if (!IsSpreadOk(spread) || !IsTradingTime() || !IsTradingDay() || IsNewsTime() || !IsDDOk() || GetGridLevel(type == (int)ORDER_TYPE_BUY ? 1 : -1) >= MaxGridLevels || PositionsTotal() >= MaxOrderCount) return false; if (!IsSwapOk(type)) return false; double lot = CalcLot(lotMultiplier); double price = (type == (int)ORDER_TYPE_BUY ? ask : bid); double sl = 0, tp = 0; double atrSL = ATRvalue * ATRSLMultiplier; sl = NormalizeDouble((type == (int)ORDER_TYPE_BUY ? price - atrSL : price + atrSL), _Digits); if (!UseATRSLL) sl = NormalizeDouble((type == (int)ORDER_TYPE_BUY ? price - BasicSL * _Point : price + BasicSL * _Point), _Digits); tp = NormalizeDouble((type == (int)ORDER_TYPE_BUY ? price + TakeProfit * _Point : price - TakeProfit * _Point), _Digits); MqlTradeRequest request = {}; MqlTradeResult result = {}; request.action = TRADE_ACTION_DEAL; request.symbol = _Symbol; request.volume = lot; request.type = (ENUM_ORDER_TYPE)type; request.price = price; request.sl = sl; request.tp = tp; request.deviation = 3; request.magic = Magic; request.comment = TradeComment; if (!OrderSend(request, result)) { Print("OrderSend failed: ", result.retcode); return false; } return true; } //----- Manage Trades (Optimized Breakeven & Step Trailing) ----- void ManageTrades(double bid = 0, double ask = 0) { for (int i = PositionsTotal() - 1; i >= 0; i--) { ulong ticket = PositionGetTicket(i); if (ticket == 0) continue; if (PositionGetString(POSITION_SYMBOL) != _Symbol || PositionGetInteger(POSITION_MAGIC) != Magic) continue; ENUM_POSITION_TYPE type = (ENUM_POSITION_TYPE)PositionGetInteger(POSITION_TYPE); if (type != POSITION_TYPE_BUY && type != POSITION_TYPE_SELL) continue; double openPrice = PositionGetDouble(POSITION_PRICE_OPEN); double profitPips = (type == POSITION_TYPE_BUY ? (bid - openPrice) / _Point : (openPrice - ask) / _Point); double currentSL = PositionGetDouble(POSITION_SL); // Breakeven Logic if (UseBreakeven && profitPips >= BreakevenStart) { double beSL = NormalizeDouble(openPrice + (type == POSITION_TYPE_BUY ? BreakevenLock * _Point : -BreakevenLock * _Point), _Digits); if ((type == POSITION_TYPE_BUY && (currentSL < beSL || currentSL == 0)) || (type == POSITION_TYPE_SELL && (currentSL > beSL || currentSL == 0))) { MqlTradeRequest request = {}; MqlTradeResult result = {}; request.action = TRADE_ACTION_SLTP; request.position = ticket; request.sl = beSL; request.tp = PositionGetDouble(POSITION_TP); if (!OrderSend(request, result)) { Print("Breakeven modify failed: ", result.retcode); } } } // Step Trailing Stop if (UseTrailing && profitPips >= TrailStart) { double trailOffset = TrailDistance * _Point; double newSL = NormalizeDouble((type == POSITION_TYPE_BUY ? bid - trailOffset : ask + trailOffset), _Digits); double slDiff = (type == POSITION_TYPE_BUY ? (newSL - currentSL) / _Point : (currentSL - newSL) / _Point); if (slDiff >= TrailStep) { MqlTradeRequest request = {}; MqlTradeResult result = {}; request.action = TRADE_ACTION_SLTP; request.position = ticket; request.sl = newSL; request.tp = PositionGetDouble(POSITION_TP); if (!OrderSend(request, result)) { Print("Trailing modify failed: ", result.retcode); } } } // Multi-Stage Partial Close if (TPLevels > 0 && profitPips >= TPInitLevel) { double levelStep = (TakeProfit - TPInitLevel) / TPLevels; for (int level = 1; level <= TPLevels; level++) { double targetPips = TPInitLevel + level * levelStep; if (profitPips >= targetPips && PositionGetDouble(POSITION_VOLUME) > 0) { double closeLot = PositionGetDouble(POSITION_VOLUME) * (LotPercent / 100.0); double minLot = SymbolInfoDouble(_Symbol, SYMBOL_VOLUME_MIN); if (closeLot < minLot) closeLot = PositionGetDouble(POSITION_VOLUME); MqlTradeRequest request = {}; MqlTradeResult result = {}; request.action = TRADE_ACTION_DEAL; request.position = ticket; request.symbol = _Symbol; request.volume = closeLot; request.type = (type == POSITION_TYPE_BUY ? ORDER_TYPE_SELL : ORDER_TYPE_BUY); request.price = (type == POSITION_TYPE_BUY ? bid : ask); request.deviation = 3; if (!OrderSend(request, result)) { Print("Partial close failed: ", result.retcode); } break; } } } } } //----- Draw Profit Line ----- void DrawProfitLine() { if (DrawProfit && ProfitValue > 0) { ObjectCreate(0, "ProfitLine", OBJ_HLINE, 0, 0, ProfitValue); ObjectSetInteger(0, "ProfitLine", OBJPROP_COLOR, clrGreen); } } //----- Show Info Panel ----- void ShowPanel() { if (!ShowInfoPanel) return; string info = "TOL LANGIT ETF - AI EA\n"; info += "Balance: " + DoubleToString(AccountInfoDouble(ACCOUNT_BALANCE), 2) + "\n"; info += "Equity: " + DoubleToString(AccountInfoDouble(ACCOUNT_EQUITY), 2) + "\n"; info += "Open Orders: " + IntegerToString(PositionsTotal()) + "\n"; info += "Trend: " + (trend == 1 ? "Up" : (trend == -1 ? "Down" : "Flat")) + "\n"; info += "Kalman State: " + DoubleToString(kalmanState, _Digits); info += "\nGMT Offset: " + IntegerToString(GMTOffset); Comment(info); } //----- Tick Speed Calculation ----- void UpdateTickSpeed() { datetime now = TimeCurrent(); if (lastTickTime > 0) { double timeDiff = (now - lastTickTime) * 1.0; if (timeDiff > 0) tickSpeed = 1.0 / timeDiff; // Ticks per second approx } lastTickTime = now; } //================ MAIN LOOP ========================== int OnInit() { Print("TOL LANGIT ETF AI EA Initialized for Forex/Gold"); InitArrays(); kalmanState = ClosePrice(0); // Init Kalman // Auto GMT if (AutoGMT) { FetchGMTOffset(); } else { GMTOffset = ManualGMTOffset; Print("Manual GMT Offset: ", GMTOffset); } // Initialize indicator handles atr_short_handle = iATR(_Symbol, PERIOD_CURRENT, RangeHE); atr_long_handle = iATR(_Symbol, PERIOD_CURRENT, RangeLE); ema_short_handle = iMA(_Symbol, PERIOD_CURRENT, 14, 0, MODE_EMA, PRICE_CLOSE); ema_long_handle = iMA(_Symbol, PERIOD_CURRENT, 50, 0, MODE_EMA, PRICE_CLOSE); rsi_handle = iRSI(_Symbol, PERIOD_CURRENT, 14, PRICE_CLOSE); macd_handle = iMACD(_Symbol, PERIOD_CURRENT, 12, 26, 9, PRICE_CLOSE); bands_handle = iBands(_Symbol, PERIOD_CURRENT, 20, 2, 0, PRICE_CLOSE); obv_handle = iOBV(_Symbol, PERIOD_CURRENT, VOLUME_TICK); ema_h1_handle = iMA(_Symbol, PERIOD_H1, 50, 0, MODE_EMA, PRICE_CLOSE); atr_h1_handle = iATR(_Symbol, PERIOD_H1, 14); stoch_handle = iStochastic(_Symbol, PERIOD_CURRENT, 5, 3, 3, MODE_SMA, 0); // Initialize neural network dnn = new DeepNeuralNetwork(3, 4, 4, 2); double weights[46] = { 0.1, -0.2, 0.3, 0.4, // iaWeights row1 -0.5, 0.6, -0.7, 0.8, // row2 0.9, -1.0, 1.1, -1.2, // row3 0.5, -0.5, 0.5, -0.5, // aBiases 1.0, 0.9, 0.8, 0.7, // abWeights row1 0.6, 0.5, 0.4, 0.3, // row2 0.2, 0.1, -0.1, -0.2, // row3 -0.3, -0.4, -0.5, -0.6, // row4 0.4, -0.4, 0.4, -0.4, // bBiases 1.2, -1.2, // boWeights row1 1.1, -1.1, // row2 1.0, -1.0, // row3 0.9, -0.9, // row4 0.3, -0.3 // oBiases }; dnn.SetWeights(weights); DrawProfitLine(); return(INIT_SUCCEEDED); } void OnDeinit(const int reason) { delete dnn; ObjectDelete(0, "ProfitLine"); Comment(""); } void OnTick() { MqlTick tick; if (!SymbolInfoTick(_Symbol, tick)) return; double ask = tick.ask; double bid = tick.bid; double spread = (ask - bid) / _Point; UpdateTickSpeed(); // Tick analysis if (tickSpeed < 0.1) return; // Skip if slow ticks (self-opt) CalculateCombo1(); CalculateCombo2(); CalculateCombo3(); CalculateTrend(); ManageTrades(bid, ask); ShowPanel(); if (!SingleSymbol) return; bool buySignal = GetBuySignal(); bool sellSignal = GetSellSignal(); // Buy Grid/Martingale if (buySignal) { int gridLevel = GetGridLevel(1); if (gridLevel < MaxGridLevels) { double lastPrice = GetLastOpenPrice(1); double dist = (lastPrice > 0 ? (lastPrice - bid) / _Point : 0); if (gridLevel == 0 || dist >= RTDists[gridLevel - 1]) { OpenTrade((int)ORDER_TYPE_BUY, RTMLots[gridLevel], ask, bid); } } } // Sell Grid/Martingale if (sellSignal) { int gridLevel = GetGridLevel(-1); if (gridLevel < MaxGridLevels) { double lastPrice = GetLastOpenPrice(-1); double dist = (lastPrice > 0 ? (ask - lastPrice) / _Point : 0); if (gridLevel == 0 || dist >= RTDists[gridLevel - 1]) { OpenTrade((int)ORDER_TYPE_SELL, RTMLots[gridLevel], ask, bid); } } } }

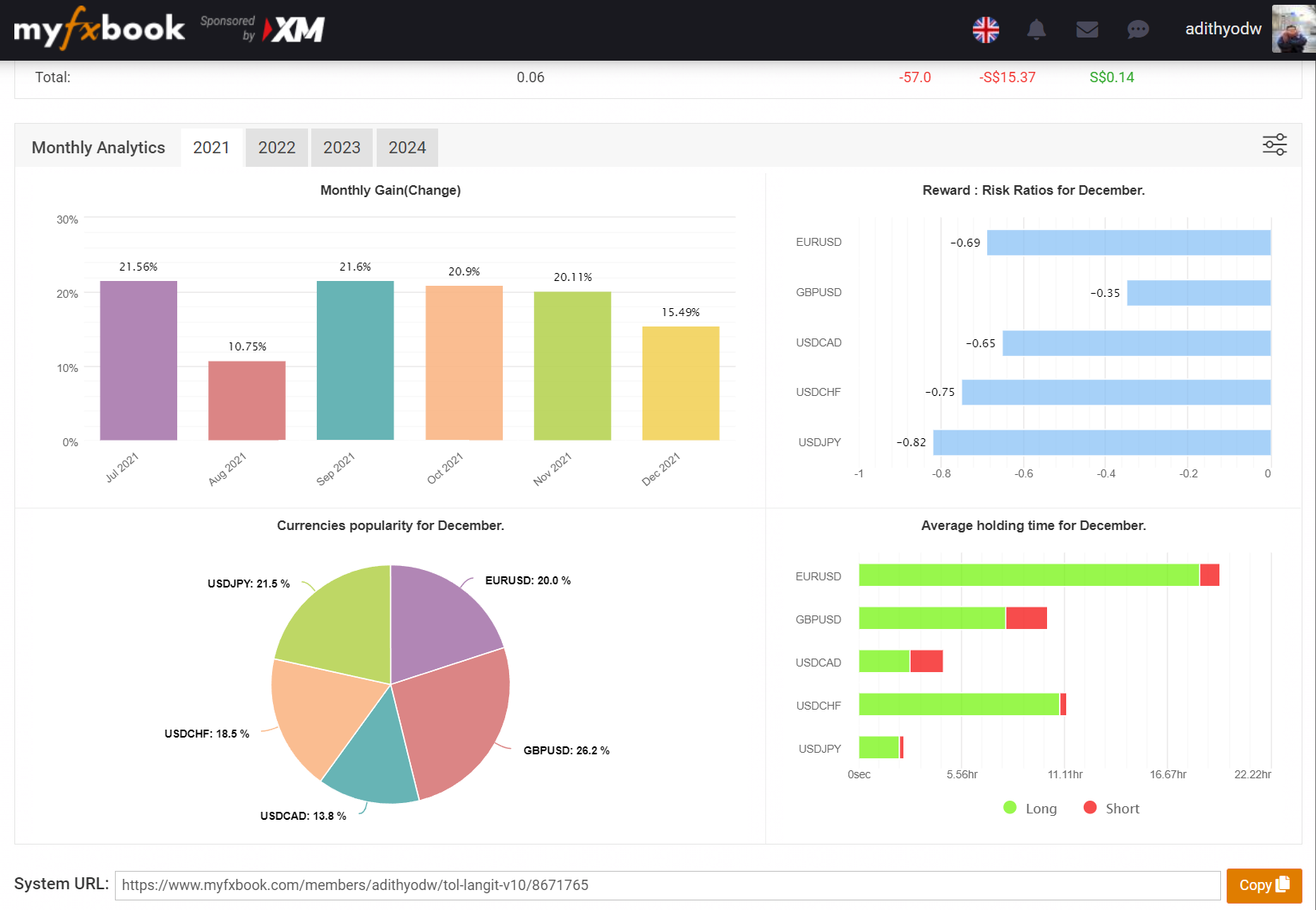

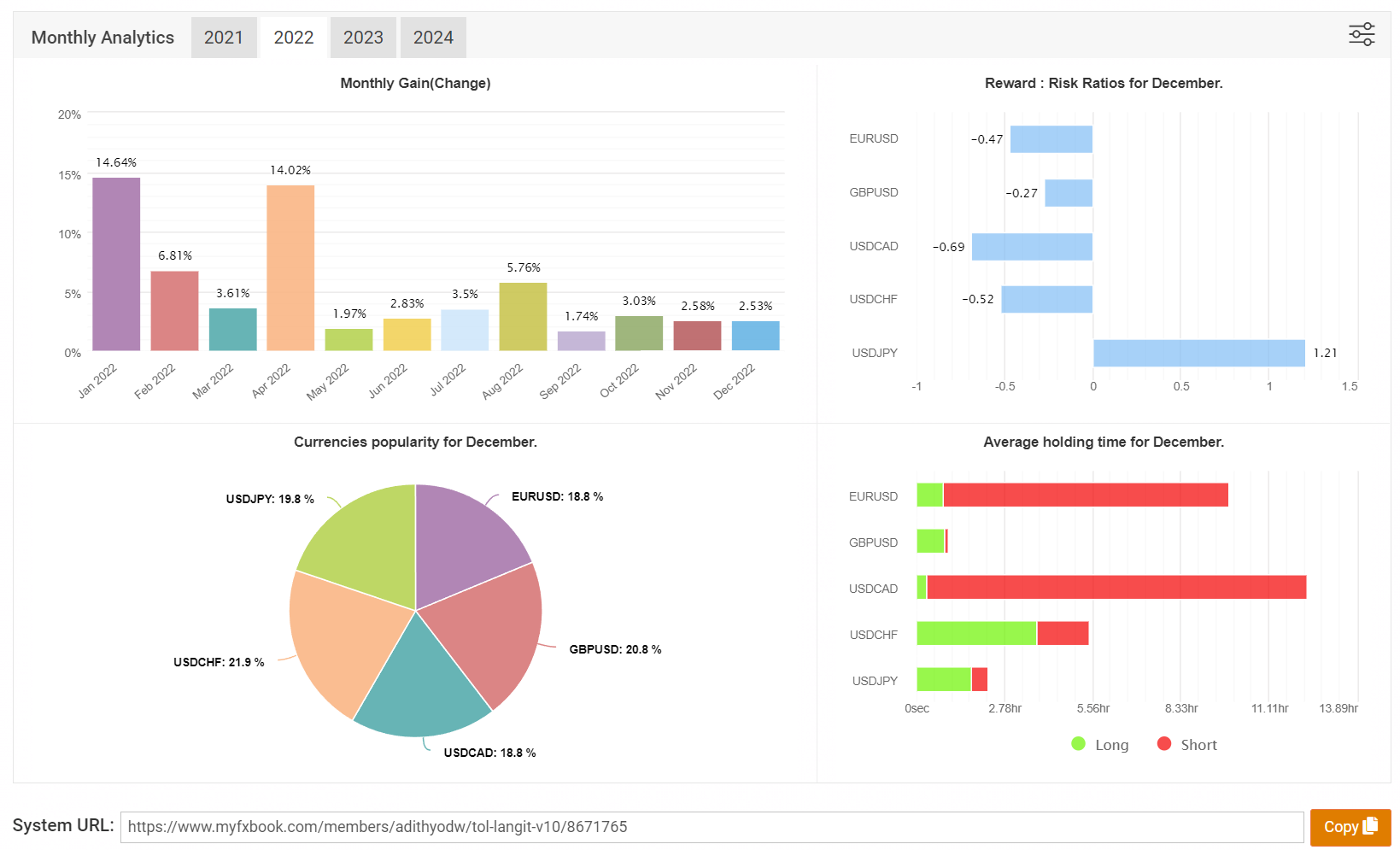

TOL LANGIT - 2021 - 2025

I don’t need to talk much—let the numbers do the talking.

Here’s the performance of Tol Langit V10 from 2021 to 2024:

2021: 110.41%

2022: 63.02%

2023: 39.16%

2024: 57.74%

Don’t trust anyone claiming to be a trader without a live MQL5 or Myfxbook account from a legit Tier 1 broker. No live account? That’s 100% bullshit.

🤖 Contact Info

MQL Profile

https://www.mql5.com/en/users/adithyodw/seller

Telegram Channel

Recommended Broker

https://icmarkets.com/?camp=49934

Trading Guide")