Trump Policy Guessing Game Continues, Pound to Look Past UK GDP

Trump Policy Guessing Game Continues, Pound to Look Past UK GDP

Talking Points:

- British Pound unlikely to find strong lead in 4Q UK GDP data

- Trump-watching continues to preoccupy the financial markets

- An augmented “Trump trade” narrative may be taking shape

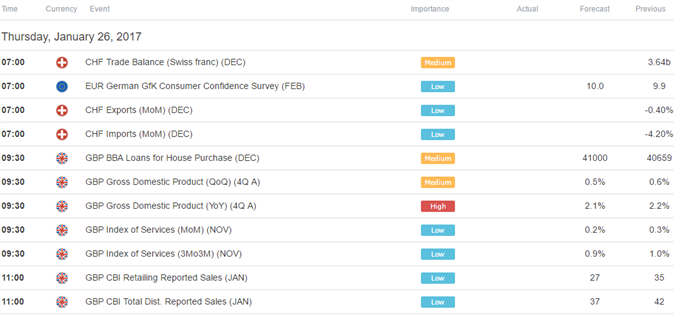

The British Pound outperformed in overnight trade, seemingly not bothered by an approaching UK GDP report that is expected to show growth slowed in the fourth quarter. The figures are expected to reveal output grew at an on-year rate of 2.1 percent, a downtick from the 2.2 percent expansion scored in the three months to September 2016.

Sterling’s resilience appears to reflect the markets’ increasingly sanguine Brexit outlook. The currency has mounted a swift recovery after Prime Minister Theresa May stuck a conciliatory tone in a speech outlining her vision for the UK/EU divorce mid-month. With that in mind, it would probably take a significantly worse than expected GDP print – an unlikely outturn given recent news flow – to truly sink the UK unit.

Later in the day, a smattering of second-tier US economic data releases is due to cross the wires but the outcomes are likely to pass below the radar as Trump-watching continues to preoccupy investors. Stocks rose yesterday in what the newswires claimed was the return of the so-called “Trump trade” but the US Dollar curiously did not participate in the rally.

The greenback rallied alongside shares in the six weeks after Mr Trump’s surprise election on bets that an expansionary fiscal policy (including new spending on infrastructure, lower corporate taxes and deregulation) will make for richer earnings and boost inflation, spurring the Fed to hike rates more aggressively. The “corporate earnings” bit appeared in yesterday’s price action; the “rate hikes” one did not.

This might imply an evolving view of what a Trump White House may ultimately mean. Deregulation and lower corporate taxes may boost the bottom line but that does not necessarily translate into stronger economy-wide growth, especially if higher trade barriers – another feature of the Trump platform – prove to crimp consumption. The Fed may be far more timid in this case, perhaps explaining soggy USD performance.

On balance, it is far too early to make broad generalizations. A day or two of price action is hardly indicative of a market-wide shift in traders’ assessment of the President’s would-be policy path. Still, the emerging dynamics bear close monitoring and most market participants will likely remain too consumed with hammering out a baseline Trump-era narrative to pay much attention to relatively minor data points.

Asia Session

European Session