Kalman Filter Forecasting

- Utilità

-

Christian Stern

As CEO of a Switzerland-based specialist company, I combine many years of experience in banking with deep expertise in developing high-quality MQL5 solutions. Our focus is on programming statistical tools for financial analysis and time-series evaluation that unite methodological precision with

As CEO of a Switzerland-based specialist company, I combine many years of experience in banking with deep expertise in developing high-quality MQL5 solutions. Our focus is on programming statistical tools for financial analysis and time-series evaluation that unite methodological precision with - Versione: 2.10

- Aggiornato: 14 giugno 2026

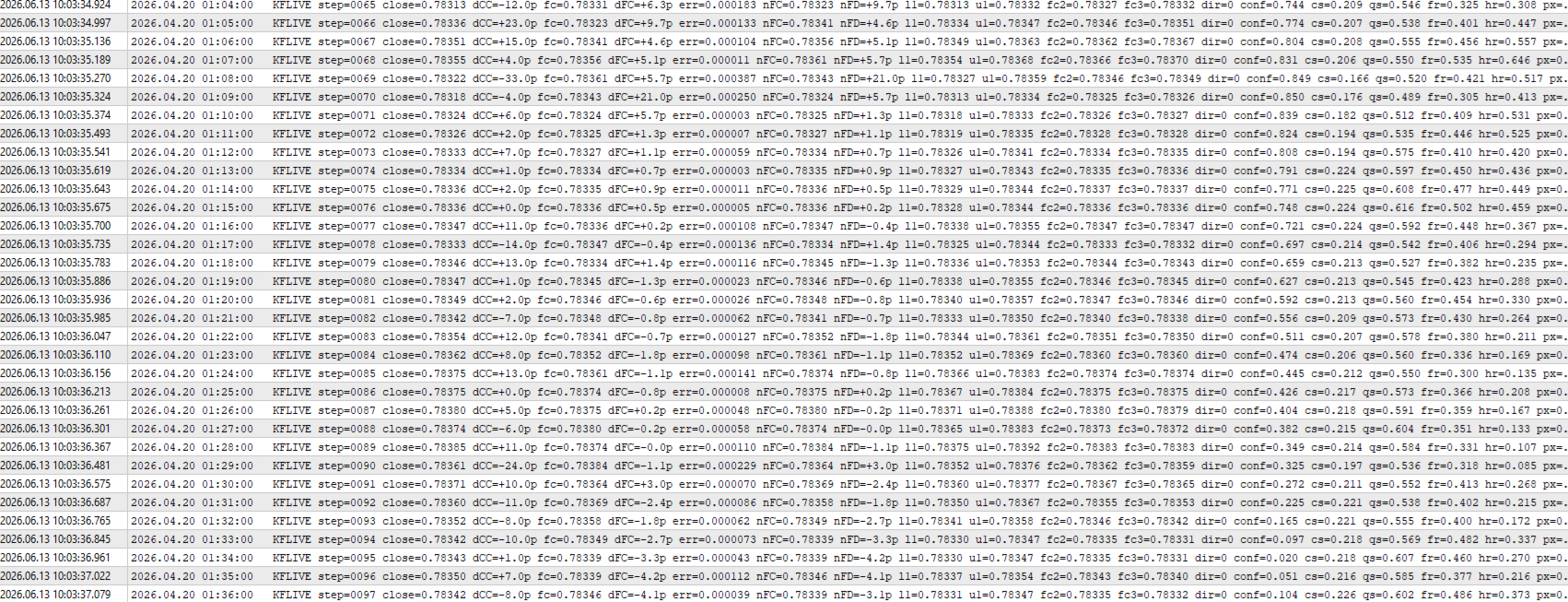

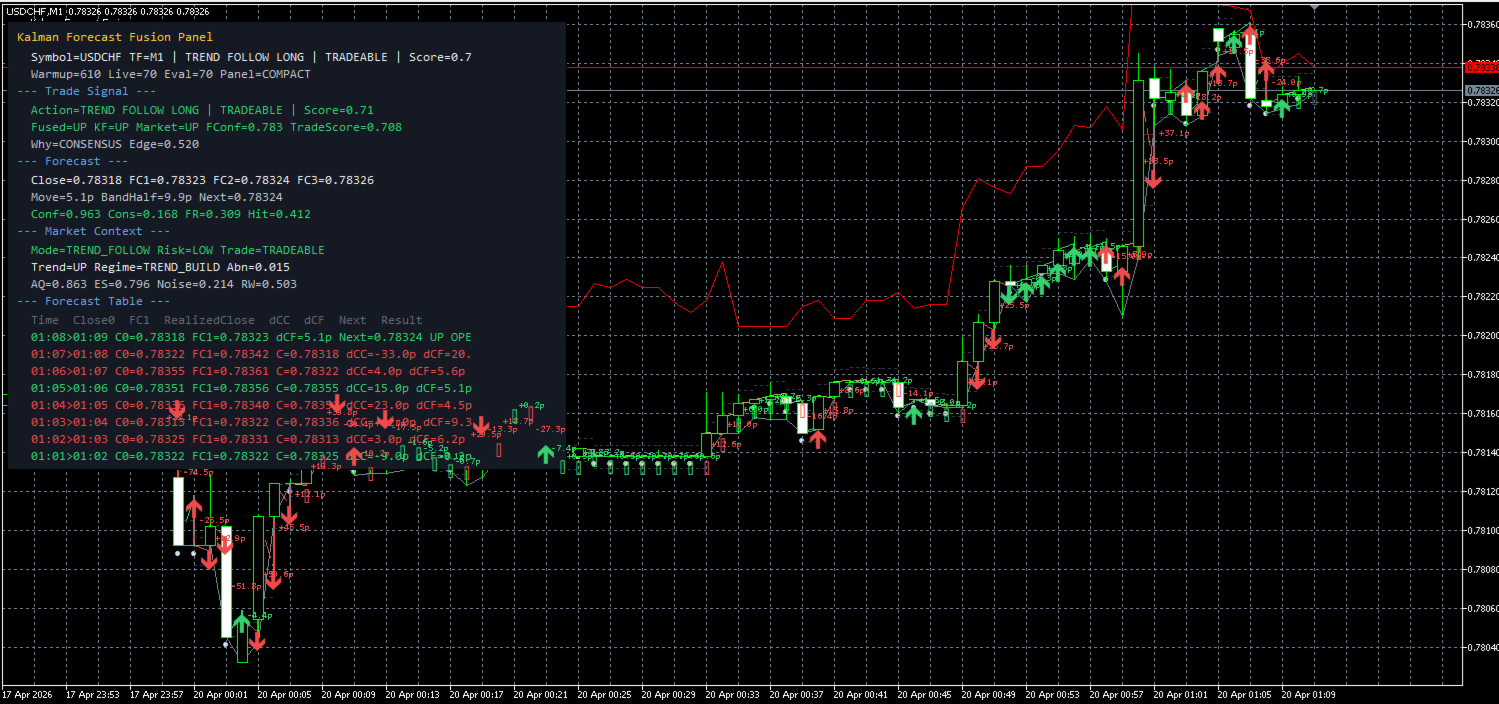

Kalman Forecast Helper is an advanced MQL5 Expert Advisor component designed to generate adaptive market forecasts, trend predictions, and trading signals for FX and other financial time series.

Powered by a proprietary Kalman filtering engine, the helper continuously analyzes incoming market data and delivers actionable forecast information that can be integrated directly into Expert Advisors, indicators, or quantitative trading systems.

After each update, the helper provides:

-

Multi-horizon forecasts (1 to 3 bars ahead)

-

Trend direction predictions

-

Confidence bands

-

Trading signals {-1, 0, +1}

-

Forecast quality ratings (A–F)

-

Internal model quality ratings (A–F)

Key Features

-

Adaptive forecasting for changing market conditions

-

Designed specifically for noisy and highly dynamic financial time series

-

Automatic confidence assessment for every forecast

-

Volatility-aware signal generation

-

Built-in trend detection and direction analysis

-

Multi-timeframe support

-

Self-monitoring model health and forecast reliability

-

Robust handling of outliers and market anomalies

Reliability & Stability

The helper incorporates multiple layers of numerical and statistical protection to maintain stable operation during periods of elevated volatility and rapidly changing market conditions.

Features include:

-

Adaptive noise estimation

-

Outlier detection and filtering

-

Automatic model recovery mechanisms

-

Forecast consistency monitoring

-

Dynamic confidence adjustment

-

Advanced numerical stability safeguards

Typical Applications

-

Expert Advisors

-

Algorithmic trading systems

-

Signal generation

-

Trend-following strategies

-

Market regime detection

-

Quantitative research

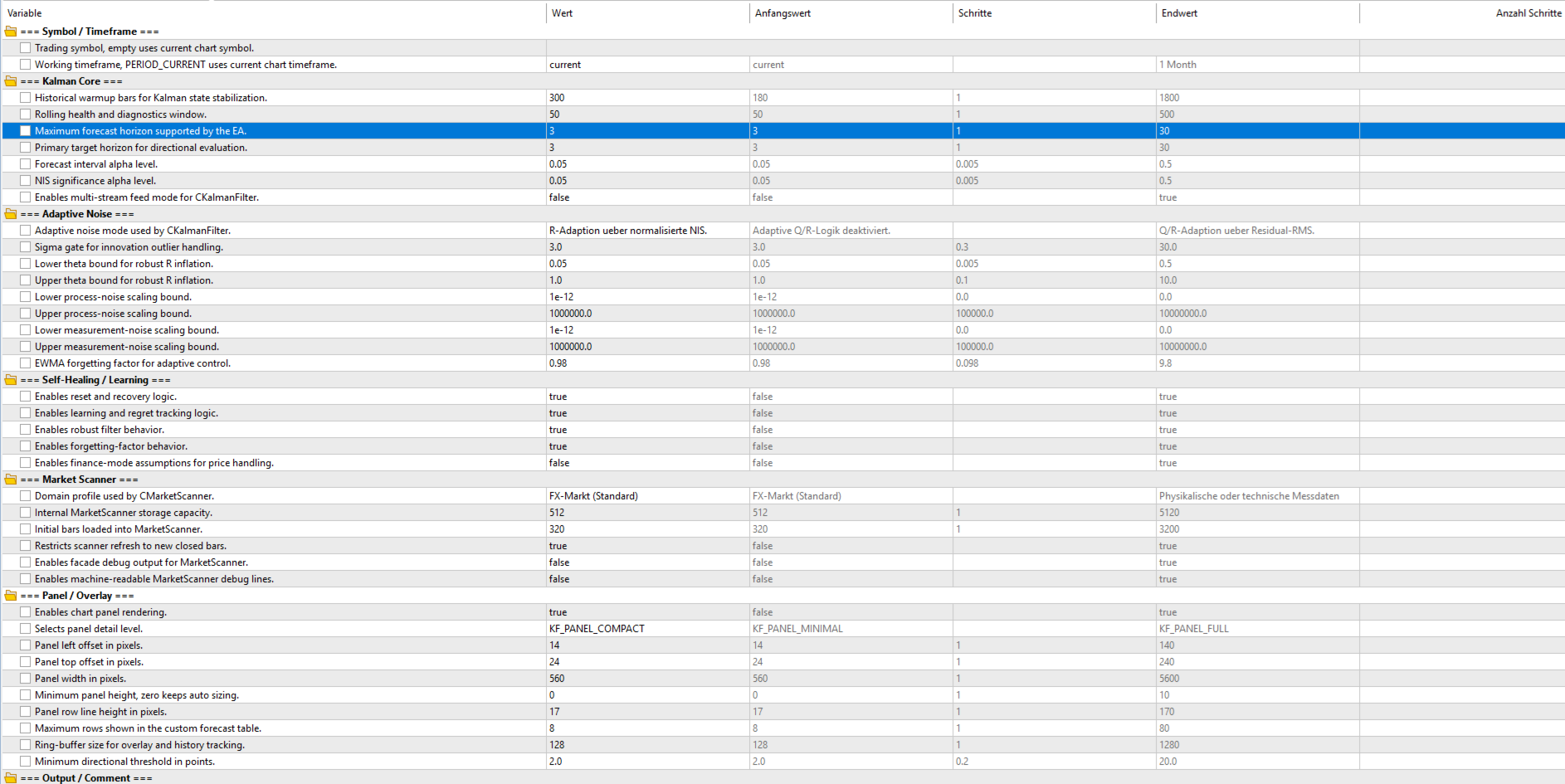

The forecasting engine used by this helper is based on the proprietary CKalmanFilter technology. Developers interested in licensing the standalone CKalmanFilter library for custom projects may request separate licensing information.