Rejoignez notre page de fans

VWAP Lite - Volume Weighted Average Price - indicateur pour MetaTrader 5

- Vues:

- 32845

- Note:

- Publié:

- Mise à jour:

-

Vous manquez des opportunités de trading :

Vous manquez des opportunités de trading :- Applications de trading gratuites

- Plus de 8 000 signaux à copier

- Actualités économiques pour explorer les marchés financiers

Inscription Se connecterVous acceptez la politique du site Web et les conditions d'utilisation

Si vous n'avez pas de compte, veuillez vous inscrire -

Besoin d'un robot ou d'un indicateur basé sur ce code ? Commandez-le sur Freelance

Aller sur Freelance

Besoin d'un robot ou d'un indicateur basé sur ce code ? Commandez-le sur Freelance

Aller sur Freelance

Versions:

- 2016-06-15; v1.49; Code Improvement

- 2016-01-11; v1.47; Code Improvement

- 2016-01-11; v1.46; Code Improvement

- 2016-01-11; v1.45; Code Improvement

- 2015-12-29; v1.43; Initial Public Release

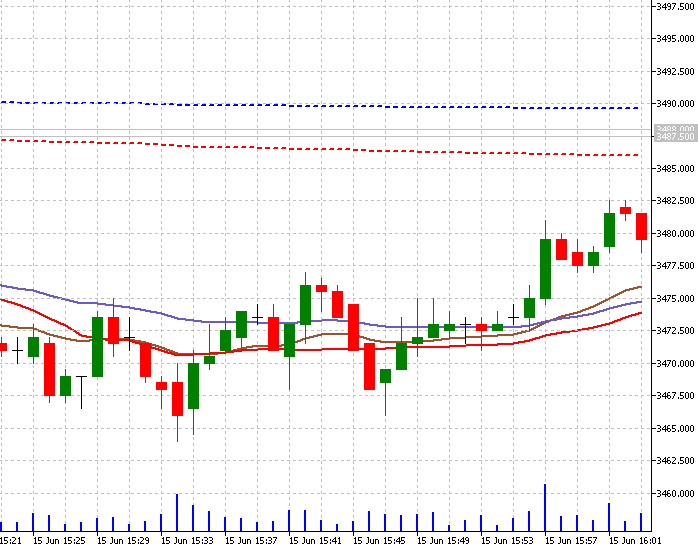

VWAP is an intra-day calculation used primarily by algorithms and institutional traders to assess where a stock is trading relative to its volume weighted average for the day. Day traders also use VWAP for assessing market direction and filtering trade signals. Before using VWAP, understand how it is calculated, how to interpret it and use it, as well the drawbacks of the indicator (http://traderhq.com/trading-strategies/understanding-volume-weight-average-price/).

This is a VWAP indicator based on the Investopedia description (http://www.investopedia.com/articles/trading/11/trading-with-vwap-mvwap.asp).

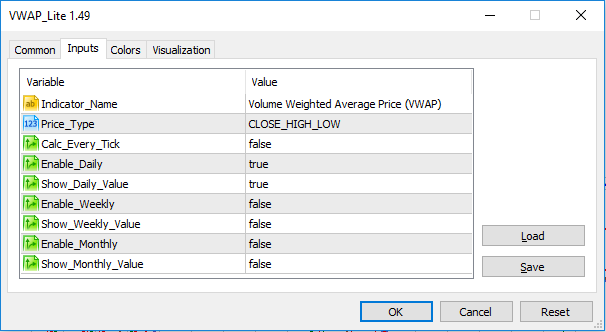

I've added three lines to this indicator. The principal is the VWAP Daily which is the calculation based on the intra-day values, there's the Weekly and the Monthly that is calculated based in the week and month starts respectively.

All three lines are independent. As default only the intra-day comes enabled, but you can enable the others in the properties panel.

Thanks for downloading this code. I will be waiting for your comments, vote and rating.

ManualTradeOnStrategyTester

ManualTradeOnStrategyTester

A simple way on how EA can link a manual order command from outside to use it in MetaTrader 5 Strategy Tester.

VWAP - Volume Weighted Average Price

VWAP is an intra-day calculation used primarily by algorithms and institutional traders to assess where a stock is trading relative to its volume weighted average for the day.

CIsSession - class to set time intervals (sessions)

CIsSession - class to set time intervals (sessions)

This simple class can be used to adjust, for example, trading ranges, or to enable / disable certain actions by time or day of the week.

Sentiment

Robot that trades the open sentiment of the market.