#1: When average is not enough. A new approach to gold night trading

#2: The DNA of a night system. Philosophy before performance - Trading Systems - 15 June 2026 - Traders' Blogs

#3: The numbers. Six years of gold, two risk profiles Part 01 - Trading Systems - 24 June 2026 - Traders' Blogs

#4: One system, three brokers. Backtesting, Part 02

System: NightScalper — Project #1. Part 4 of the launch series — July release. Previous: #1 When average is not enough · #2 The DNA of a night system · #3 The numbers.

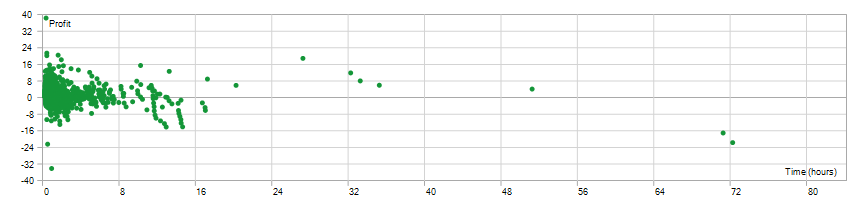

I named the obvious limitation myself: one broker, one symbol, one historical window. A single backtest, however clean, only proves the system worked on one feed.

So this post answers that directly. Same unchanged system, two additional brokers — TMGM and VT Markets — each on its own independent price feed, spread model and execution. The question is simple: when the broker changes, does the behaviour change with it?

What is the same, and what is not

Before any number, the honest part — because a comparison is only worth as much as its disclosed conditions.

The same across all three: the system (NightScalper, build V3.1a), the instrument (gold, XAUUSD), the timeframe, the fixed micro starting size, the account currency (EUR) and the deposit (€3,000). Nothing was re-tuned per broker.

What differs, and why it matters:

- The test window. Each broker only provides as much real-tick history as it holds. RoboForex reaches back to 2020. TMGM's data starts in 2024, VT Markets' in 2025. I tested the full length each broker offers — but that means the two newer brokers cover mainly the recent gold rally, while RoboForex additionally covers the 2020 crash and the 2022 cycle. The newer windows are, frankly, the easier years. I am pointing that out so you don't have to.

- The risk setting. The two new runs use the balance-scaled profile (position size grows with the account), where Part 01's reference column used a fixed size. Scaling raises the floating drawdown. So when you see a higher drawdown percentage below, that is the setting talking, not the broker.

The conditions

- System: NightScalper — Project #1 (build V3.1a)

- Instrument: Gold (XAUUSD)

- Data quality: 100% real ticks on both new brokers (TMGM ~187M ticks, VT ~179M ticks)

- Accounts: EUR, €3,000, 1:100 leverage

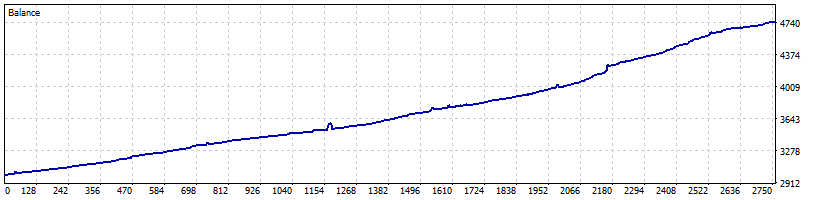

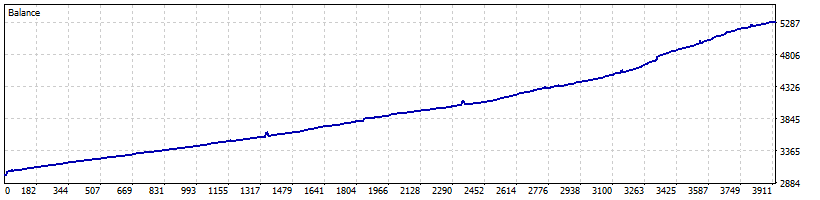

- Brokers / windows: RoboForex 2020–2026 · TMGM 2024–2026 · VT Markets 2025–2026

The result that matters most

TMGM and VT Markets ran on the identical setting — same risk profile, overlapping recent window — but on two completely different brokers. If broker conditions were a major hidden variable, this is where it would show. It does not.

| Metric | TMGM (2024–2026) | VT Markets (2025–2026) |

|---|---|---|

| Profit factor | 3.16 | 3.34 |

| Win rate | 77.79% | 77.51% |

| Equity drawdown (floating) | 8.93% | 8.03% |

| Recovery factor | 7.23 | 6.22 |

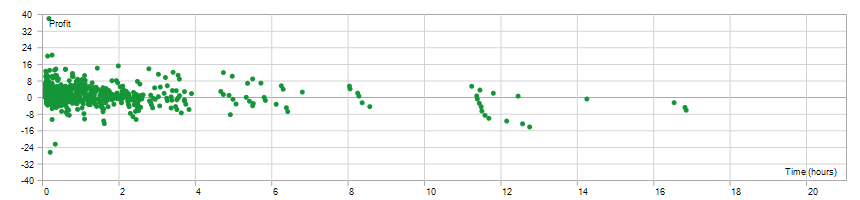

| Average hold time | ~1h | ~44m |

| Stop-out | none | none |

Two different brokers, two different feeds — and the character barely moves. That consistency is the entire point of Part 02.

All three side by side

Net profit in euros is not directly comparable here — the windows differ and the risk settings differ — so it is shown only for completeness, not as a ranking.

The comparison that is meaningful is the behaviour: profit factor, win rate, floating drawdown, recovery.

| Metric | RoboForex 2020–2026 | TMGM 2024–2026 | VT Markets 2025–2026 |

|---|---|---|---|

| Profit factor | 2.77 | 3.16 | 3.34 |

| Win rate | 75.96% | 77.79% | 77.51% |

| Equity drawdown (floating) | 5.73%* | 8.93% | 8.03% |

| Recovery factor | 10.98 | 7.23 | 6.22 |

| Net profit (EUR) | +3,129 | +2,307 | +1,754 |

*RoboForex used the fixed-size profile in Part 01; the lower drawdown reflects that setting, not a "safer" broker. On the scaled profile, floating drawdown settles around 8–9% across both new brokers.

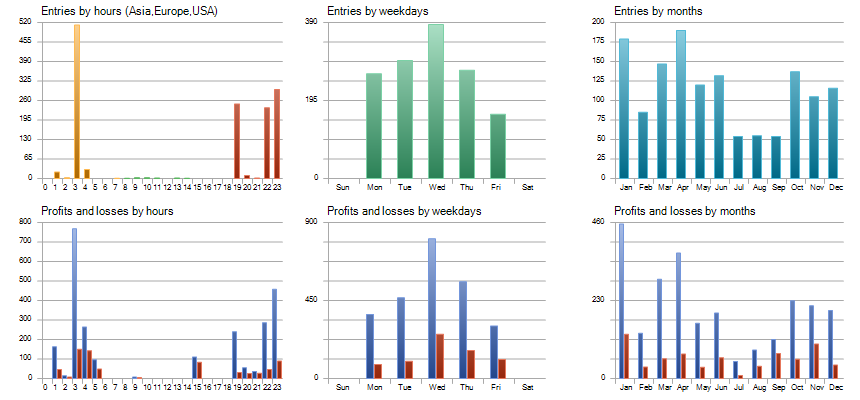

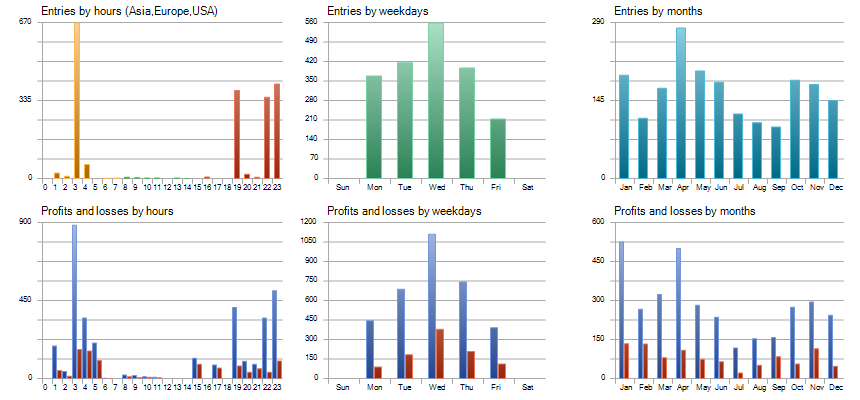

The win rate sits in a tight band — roughly 76% to 78% — across three independent brokers and three different time spans. The profit factor stays comfortably above 2.7 everywhere. The floating drawdown is consistent within each setting. Nothing here depends on one broker's quirks.

What this does and does not prove

It does show that the system's behaviour is not an artefact of a single broker's feed. Change the execution environment, and the profile holds.

It does not erase the caveats — and these are real:

- The two newer windows lean heavily on the gold rally. A longer history on those brokers would be a harder test, and I will run it when the tick data allows.

- It remains one symbol. Gold is the system's home, by design — but it is still a single market.

- A backtest models the past. It is evidence of consistency, not a promise of the future.

The point

Part 01 showed the system works. Part 02 shows it does not depend on where it runs. Three brokers, three windows, one unchanged system — and a profile you can recognise in all three.

No system is risk-free. A backtest is not a promise. Past performance does not guarantee future results.

Live observation continues, and more forward data will follow before the July release.

")

![[XAUUSD]: Weekly Liquidity Activation Points (timings), June 29 - July 3, 2026](https://c.mql5.com/6/1014/splash-preview-772062.png "[XAUUSD]: Weekly Liquidity Activation Points (timings), June 29 - July 3, 2026")

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}