Test 003: Day of the week as an entry factor / XAUUSD, EURUSD, SP500

I tested the hypothesis that the day of the week may influence the likelihood of either a reversal or a continuation of price movement during the next trading session. The idea is straightforward: if a consistent behavioral pattern emerges on specific weekdays, it could serve as the foundation for a systematic trading strategy.

The study began by testing a Friday reversal relative to Thursday on XAUUSD. After that, all weekday combinations were analyzed for both reversal and continuation patterns.

Test Conditions

- Instrument: XAUUSD

- Timeframe: D1

- Entry: in the direction of either a reversal or continuation relative to the previous day

- Exit: position closed at the end of the trading day

- Stop Loss: none

- Take Profit: none

- Filters: none

- Objective: evaluate the pure weekday effect without the influence of risk management or additional trading rules

Results

The first scenario tested was a Friday reversal following Thursday on XAUUSD, with no filters or additional settings applied.

| Model | Profit Factor | Win Rate |

|---|---|---|

| Base Model | 1.22 | 56% |

| Optimized Version | 1.31 | 50% |

Figure 1. XAUUSD base model: Friday reversal after Thursday

Even the base version demonstrated positive expectancy. This is an important observation, since the goal was not to maximize profitability from the outset, but rather to determine whether the effect exists at all.

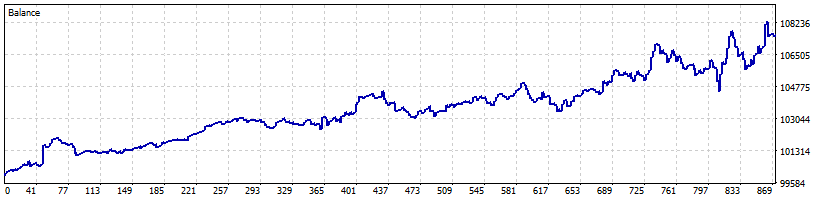

Parameter optimization increased the Profit Factor to 1.31. The improvement was relatively modest, suggesting that the main opportunity for further enhancement likely lies not in refining entry parameters, but in managing open positions more effectively.

Figure 2. XAUUSD optimized model with filters and stop management for the Friday-after-Thursday reversal pattern

Testing All Weekdays

After obtaining a positive result on gold, a full scan of all weekday combinations was conducted.

- no stop losses;

- no take profits;

- no filters;

- positions closed strictly at the end of the day.

This approach makes it possible to evaluate the existence of a reversal or continuation effect within the next daily candle without the influence of position management.

For XAUUSD, no other significant results were found. The Friday-after-Thursday reversal remained the only robust pattern. Most other weekday combinations either produced results close to break-even or failed to show a sufficient edge for practical trading.

EURUSD Results

The next instrument tested was EURUSD.

| Instrument | Pattern | Profit Factor | Win Rate |

|---|---|---|---|

| EURUSD | Friday reversal after Thursday | 1.28 | 56% |

The fact that similar results appeared across two different markets is quite intriguing. While this is not enough to claim a universal effect, the hypothesis clearly deserves further testing across additional instruments and longer historical periods.

Figure 3. EURUSD Wednesday reversal after Tuesday.

SP500 Results

| Instrument | Pattern | Profit Factor | Win Rate |

|---|---|---|---|

| SP500 | Wednesday reversal after Tuesday | 1.33 | 50% |

One aspect worth highlighting is the structure of the results. The win rate is only 50%, yet the average winning trade is approximately 30% larger than the average losing trade. This difference is what generates the system’s positive expectancy.

Figure 4. SP500 Wednesday reversal after Tuesday

Observations

The unfiltered base model already produces positive results for certain weekday combinations. This is encouraging because the effect is visible even before any additional enhancements are applied.

Interestingly, both XAUUSD and EURUSD highlighted the same pattern — a Friday reversal following Thursday. Given the different market dynamics of these instruments, this overlap is far from trivial.

SP500, on the other hand, exhibited its own distinct intra-week seasonality. This may indicate that weekday effects are highly dependent on the structure of the individual market being analyzed.

Conclusion

The Friday-after-Thursday reversal was confirmed on both XAUUSD and EURUSD, while the strongest result on the SP500 came from a Wednesday-after-Tuesday reversal.

Test reports: Thusday-Reverse-optimize-mfemae.zip

EA source code: CodeBase

Telegram: https://t.me/it_trader_channel

")

")