NightScan UsdJpy

- Experts

- Takaho Seto

- 버전: 1.0

- 활성화: 5

NightScan UsdJpy is a multi-strategy Expert Advisor for the USDJPY pair

that runs six independent time-based logics, each derived from

statistically significant edges identified through analysis of

hundreds of millions of USDJPY M5 ticks over more than 17 years.

■ Design Philosophy

Different sessions of the trading day exhibit distinct micro-patterns

driven by participant behavior. NightScan UsdJpy isolates six time

windows where statistical edges are most reproducible on USDJPY,

and applies independent condition filters to each.

The six logics operate in parallel without interference, each at its

own designated hour. By distributing edges across multiple sessions,

the system aims to reduce dependency on any single market regime.

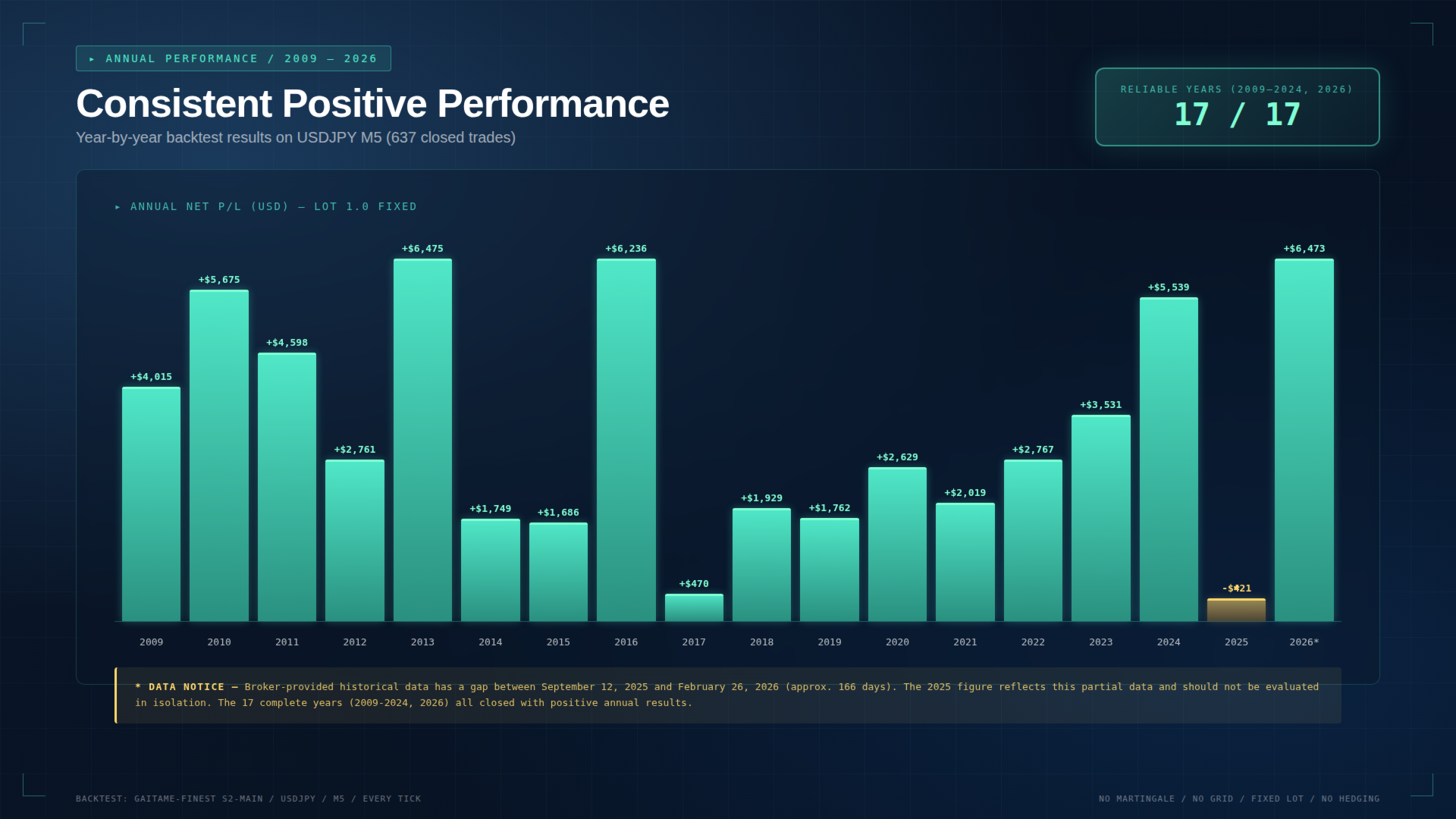

■ Backtest Performance Summary

Test Period : January 2009 - April 2026 (17.3 years)

Broker : Gaitame Finest (GMT+2 historical)

Timeframe : M5 (Every tick, modeling quality 89.99%)

Spread : 10 points (fixed)

Initial Deposit : USD 50,000

Lot Size : 1.0 (fixed)

Net Profit : USD 59,891 (+119.8%)

Final Balance : USD 109,891

Profit Factor : 2.96

Win Rate : 68.45% (436 wins / 201 losses, 637 trades total)

Maximum Drawdown : USD 9,644 (15.77%)

Max Consecutive Wins : 18

Max Consecutive Loss : 9

Expected Payoff : USD 94.02 per trade

Monthly Performance :

Total Months : 208 months

Profitable : 141 months (67.8%)

Avg Trades/Month: approximately 3.1

Annual Performance :

Reliable years (2009-2024, 2026) : 17 of 17 profitable

2025 is partial evaluation only due to data gap below

■ Historical Market Events Survived in Backtest

NightScan UsdJpy was tested through the following major market events

across 17 years of historical data, maintaining annual profitability.

- 2008-2009 Global Financial Crisis aftermath

- 2011 Tohoku earthquake and yen surge (USDJPY briefly hit 76)

- 2013-2015 Abenomics yen weakening (80 to 125 yen range)

- 2016 Brexit referendum volatility

- 2020 COVID-19 pandemic flash crash

- 2022 BoJ YCC defense and global rate hike divergence

- 2024-2025 USDJPY at historic 160 yen levels and MoF intervention

Across regimes of different monetary policies, geopolitical risks,

and market sentiment, the system maintained annual profitability

in backtest.

■ The Edge of Six-Logic Composition

Single-logic EAs often perform well in specific market conditions

but underperform when the regime shifts. NightScan UsdJpy combines

six logics with different characteristics to provide

a portfolio effect across varying market conditions.

Each logic operates at a distinct session (Asia Early, Pre-London,

London Open, EU Midday, NY Transition, US Session), combining

low-correlation edges into a composite system.

All entry decisions reference confirmed H1 bar values (previous bar)

to ensure no look-ahead bias is introduced.

Maximum simultaneous positions: 3 (observed in backtest).

■ Design Principles

No Martingale

No Grid / Averaging Down

No fixed SL / fixed TP (time-based exits only)

No Hedging (long-only by design)

Spread filter (entries skipped when spread exceeds threshold)

Optional Friday-close switch (default: OFF)

Restart-resilient: positions are properly restored after MT4 restart

■ Recommended Setup

Broker : Low-spread broker for USDJPY (e.g. Gaitame Finest)

Chart : USDJPY M5

Operation : 24-hour operation recommended (VPS strongly advised)

Margin : USD 6,000 to 10,000 for 0.3 to 0.5 lots

USD 20,000+ for 1.0 lot

■ Timezone Configuration (Important)

The EA uses ServerTimeOffset parameter to adjust for broker timezone.

Logics were optimized for GMT+2 broker time (winter / standard).

Setting guide:

Broker GMT+3 (DST / summer): ServerTimeOffset = -1

Broker GMT+2 (standard / winter): ServerTimeOffset = 0 (default)

Broker GMT+0 (UTC, rare): ServerTimeOffset = +2

Broker GMT-5 (US, winter): ServerTimeOffset = +7

Broker GMT+10 (AU, standard): ServerTimeOffset = -8

How to check your broker's timezone:

Open MT4 "Market Watch" and compare the time shown with your local UTC time.

If broker time is 2 hours ahead of UTC, you have a GMT+2 broker (offset = 0).

Most popular brokers (IC Markets, Exness, Pepperstone, FP Markets, XM)

operate on GMT+2 / GMT+3 (DST) schedule.

For backtesting: Always use ServerTimeOffset = 0 as historical data

is typically aligned to GMT+2.

Adjust the value when your broker changes between standard and summer time.

■ Honest Disclosure of Backtest Data

Within the test period, historical data from the broker has a gap

between September 12, 2025 and February 26, 2026 (approx. 166 days).

This is a data-side issue beyond our control.

Due to this gap, the 2025 trade aggregation shows a slight negative

result (-USD 421). This reflects missing opportunity bars during the

gap period, not a logic failure.

Excluding this period, the conservative evaluation

(January 2009 - September 2025, 16.7 years) yields:

Profit Factor : 2.76

Win Rate : 68.4%

Profitable Years : 16 of 17

■ Important Disclaimer

Backtest results are based on historical price behavior and do not

guarantee future performance. Market regime changes may cause

drawdowns exceeding historical levels.

Recommended margin levels are guidelines only. Please use prudent

money management with sufficient reserves.

Without Martingale or grid recovery, equity grows gradually

rather than exponentially. This EA is designed for steady,

long-term accumulation rather than rapid gains.