A few weeks ago I came across an interesting theory about how to win 100% of all prop firm challenges using hedging. It caught my couriosity. While BFG9000 MT4 is being tested with live trades before its release, I decided to have a closer look at this idea.

How is it supposed to work?

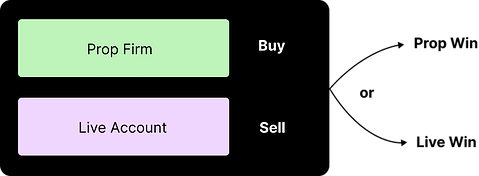

The basic idea is to feed a live account with contrary trades while trading the prop firm account. So when we place a buy-position on the prop firm, we open a sell-position on the live account.

Basic Math

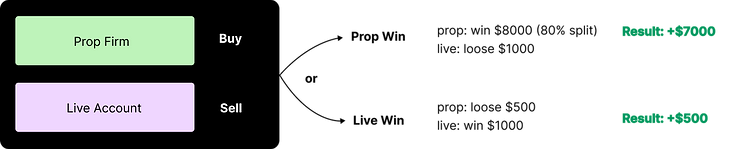

Let's see how the numbers look like. Assume, we buy a $100.000 challange for $500. When we loose 10k on the prop firm account, we win $1000 on the live account. If we win $10000 on the prop account, we loose $1000 on the live account. But receiving the profit share of 80%=$8000 minus the loss of $1000, we end up with $7000.

Real Math

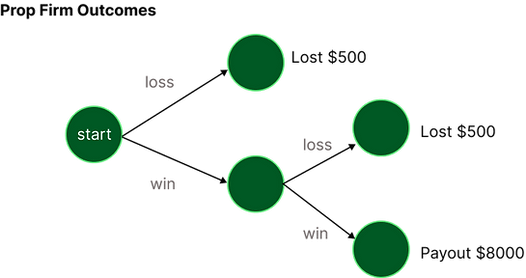

In the basic analysis above we did not consider the fact that the prop firms let you do a challenge first. Thus, you need to win twice in order to get to the 80% split. We it is rather a tree of possible outcomes. A tree like this:

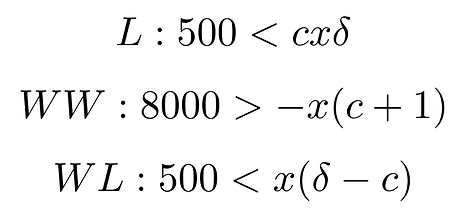

We have three possible outcomes: a) Loosing 500, b) loosing $500 and c) winning $8000. In the analysis later I will abbreviate these as a)=L, b)=WL and c)=WW

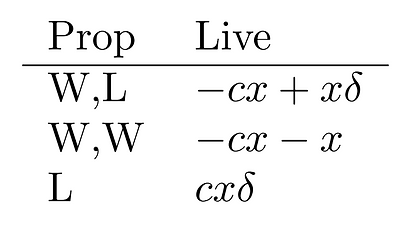

Also define x to be the amount of $ on the live account we hedge against loosing a prop firm account. In intro example I said we win $1000 in live if we loose on prop firm. That would be x=1000. We also might consider to hedge less or more during the challenge evaluaiton phase. That would be a factor c multiplied with x. The table below refers to all three possible outcomes, where we state the prop firm outcomes as WL, WW, or L.

Further, we say that when we win on the prop side, we loose cx on the live side. If we loose on the prop side, we win x on the live side.

Considering the loss of $500 on the prop side if we fail to reach the payout, it can be stated like the inequality below:

Case L

Just like in the introduction, we say that if we loose our challenge fee of $500 on the prop side, we gain x=$1000 on the live side. In case the prop firm allows less drawdown than the profit target (dd= δ * profit target) we use the δ to reflect this. Thus cxδ should be larger than the loss $500 on the prop side.

Case WW

If we win twice on the prop side, we loose the challange cx and the second hedge x on the live side. Thus the loss -x(c+1) on the live side should be smaller than the gain $8000 on the prop side.

Case WL

If we win on the prop side and then loose it again, we have -cx+δx on the live side.

Is there a good value for x and c?

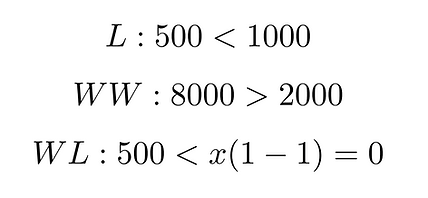

Let's do a simple test first with x=$1000, c=1 (same hedging ratio for challenge as for funded account) and δ=1 (max dd is same as the profit target).

L and WW are clear. But WTF is on WL? $500 is not less than 0! This means, there is no way to win 100% if we set x=$1000, c=1 and δ=1. 😿 Can we win with other c and δ?

Winning - can we?

The answer is YES! If we do not hedge 100% during the challenge we can win every time.

I built a smart excel sheet, where you can play around with numbers as you like. Here is one possible outcome:

Customers can download this excel sheet here

If you like this article, subscribe to my blog to get next articles automatically into your inbox

![[XAUUSD]: Weekly Liquidity Activation Points (timings), June 29 - July 3, 2026](https://c.mql5.com/6/1014/splash-preview-772062.png "[XAUUSD]: Weekly Liquidity Activation Points (timings), June 29 - July 3, 2026")