Week Ahead: Greece, BoE QIR, Short EUR/USD, Fade AUD Rallies

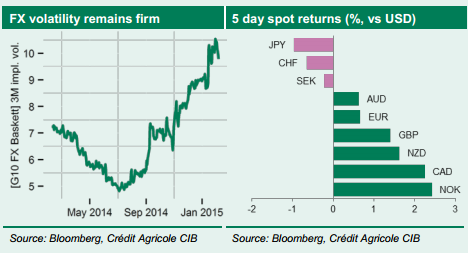

Continuing uncertainty related to Greece, the RBA surprisingly easing monetary policy, US labour data surprising positively, and intensifying speculation regarding the SNB trying to stabilise EUR/CHF at levels at around 1.05 have all been keeping FX volatility elevated this week.

Considering that speculative G10 FX positioning remains close to multi-month highs and as Greece will continue to attract investors’ attention, this is unlikely to change next week.

From a data-driven point of view, our FX Execution Mapper suggests that volatility will spike next Thursday, mainly on the back of Australian employment data and the Riksbank monetary policy announcement.

However, the Bank of England’s inflation report is likely to support such an outlook too. View-wise we favour buying USD dips against the JPY and the EUR. (see details on CA's short EUR/USD position here)

Elsewhere we believe that rallies should still be faded in commodity currencies such as the AUD and CAD. This is because commodity price developments are unlikely to stabilise sustainably in an environment of still-muted conditions in Asia and as weak growth prospects should keep respective central banks’ dovish monetary policy stances intact. (see CA's views on trading AUD next week here).

Last, but not least, expectations of rising UK growth to the benefit of further stabilising BoE rate expectations should keep the GBP a buy.

What we’re watching

Greece – next week’s developments in Greece will continue to attract investors’ attention. We expect any positive developments to have only limited currency impact from current levels as central-bank monetary policy expectations should ultimately prove the single currency’s main driver.

BoE inflation report – the central bank is likely to signal more constructive growth prospects. This combined with stable medium-term inflation expectations may lift the GBP further.

Australian employment – Weak business activity signals limited risk of next week’s labour data surprising positively. We favour selling AUD rallies.

US retail sales – Although a weaker-than-expected reading cannot be ruled out, the impact on Fed rate expectations is likely muted. (see CA's detailed US calendar for next week here)

Riksbank policy meeting – more constructive growth data has supported the SEK of late. However, still-weak price developments should maintain the risk of a more dovish Riksbank policy stance to the detriment of the SEK.

")