|

6+ 년도

경험

|

4

제품

|

96

데몬 버전

|

|

0

작업

|

1

거래 신호

|

0

구독자

|

재무 및 국제 비즈니스 전문가로 재무 관리를 전공했습니다. MQL5와 Python 독학 개발자로서 알고리즘 트레이딩, 멀티에셋 포트폴리오 구축, 정량적 리스크 관리에 집중하고 있습니다.

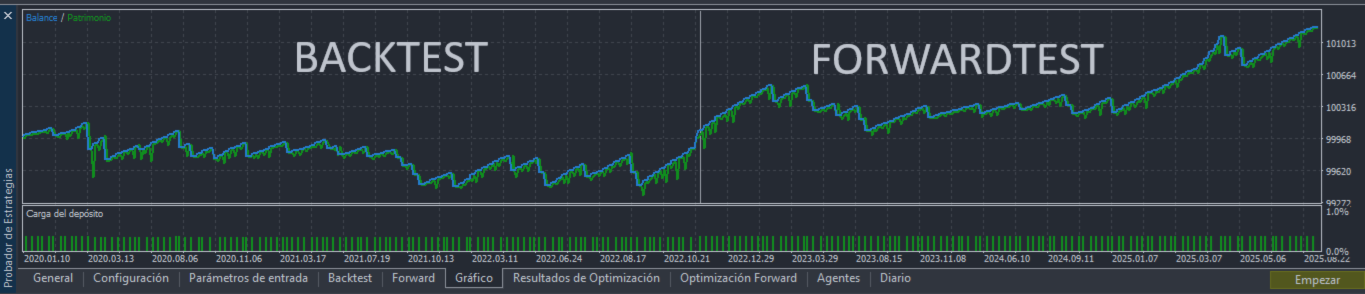

저의 작업은 개별 전략이 아닌 조율된 포트폴리오로 작동하는 Expert Advisor의 설계, 최적화 및 검증에 중점을 두고 있습니다. 상관관계 분석, 시간대 커버리지 매핑, 자산군 분산화를 적용하여 단일 상품이나 단일 접근 방식에 의존하지 않는 시스템을 구축합니다.

현재 외환, 지수, 귀금속, 에너지, 미국 주식을 아우르는 알고리즘 포트폴리오를 관리하고 있으며, 여러 세션과 타임프레임에서 동시에 운용하고 있습니다.

이 커뮤니티에서 기술 기사와 오픈소스 도구를 통해 제 경험을 공유하고 있습니다. "개별 EA 구축"에서 "포트폴리오 엔지니어링"으로의 전환이야말로 개인 투자자의 사고와 기관 투자자의 사고를 구분짓는 경계선이라 확신하며, 이 원칙이 제가 이곳에서 발행하는 모든 것의 지침이 됩니다.Has usado 75% de tu límit

저의 작업은 개별 전략이 아닌 조율된 포트폴리오로 작동하는 Expert Advisor의 설계, 최적화 및 검증에 중점을 두고 있습니다. 상관관계 분석, 시간대 커버리지 매핑, 자산군 분산화를 적용하여 단일 상품이나 단일 접근 방식에 의존하지 않는 시스템을 구축합니다.

현재 외환, 지수, 귀금속, 에너지, 미국 주식을 아우르는 알고리즘 포트폴리오를 관리하고 있으며, 여러 세션과 타임프레임에서 동시에 운용하고 있습니다.

이 커뮤니티에서 기술 기사와 오픈소스 도구를 통해 제 경험을 공유하고 있습니다. "개별 EA 구축"에서 "포트폴리오 엔지니어링"으로의 전환이야말로 개인 투자자의 사고와 기관 투자자의 사고를 구분짓는 경계선이라 확신하며, 이 원칙이 제가 이곳에서 발행하는 모든 것의 지침이 됩니다.Has usado 75% de tu límit