Rejoignez notre page de fans

KAMA - indicateur pour MetaTrader 5

- Vues:

- 13067

- Note:

- Publié:

-

Vous manquez des opportunités de trading :

Vous manquez des opportunités de trading :- Applications de trading gratuites

- Plus de 8 000 signaux à copier

- Actualités économiques pour explorer les marchés financiers

Inscription Se connecterVous acceptez la politique du site Web et les conditions d'utilisation

Si vous n'avez pas de compte, veuillez vous inscrire -

Besoin d'un robot ou d'un indicateur basé sur ce code ? Commandez-le sur Freelance

Aller sur Freelance

Besoin d'un robot ou d'un indicateur basé sur ce code ? Commandez-le sur Freelance

Aller sur Freelance

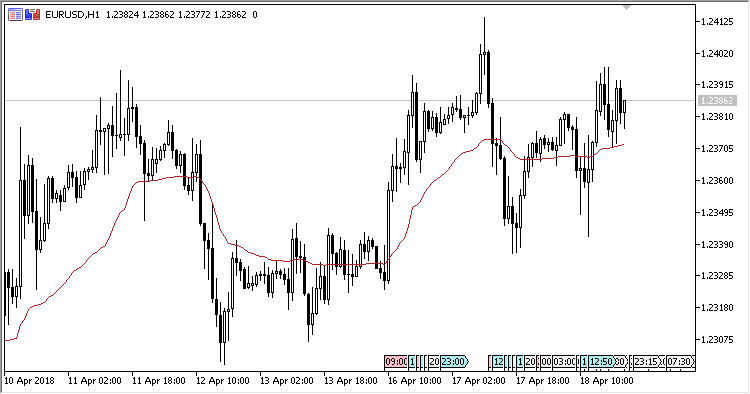

The Kaufman Adaptive Moving Average is a version of the adaptive moving average based on the exponentially smoothed moving average combined with the original methods of detecting and applying volatility as a dynamically changing smoothing constant.

The indicator has two input parameters:

- Period - calculation period;

- Applied price - price used for calculations.

Calculations:

KAMA[i] = KAMA[i-1] + sc * (Price[i] - KAMA[i-1])

where:

sc = (er * 0.6015 + 0.0645) * (er * 0.6015 + 0.0645), er = Abs(Price[i] - Price[i-Period+1]) / Sum1, and Sum1 = Sum(Abs(Price[i] - Price[i-1])) from (i-Period+1) to i

Traduit du russe par MetaQuotes Ltd.

Code original : https://www.mql5.com/ru/code/20502

Price Impulse

Price Impulse

The EA waits for the price to pass XXX points within NNN ticks.

N-_Candles_v7

The Expert Advisor searches for N identical candlesticks in a row. It buys on bullish candlesticks and sells on bearish ones. The account type is taken into consideration, i.e., whether it is a netting or a hedging one.

SSIFT

Smoothed Stochastic Inverse Fisher Transform.

Volume_Accumulation

Indicator of volumes accumulated.