Forecast and levels for S&P 500 - page 40

European indices did not mark today a definite trend. The session was relatively quiet, with no big news, with investors taking advantage of the latest events (last week’s intervention by the President of the Fed and the recent agreement reached between the US and Mexico). Thus, the session was under low volatility and volume below the average observed in August.

Market View; World Stock

Eur/usd

EURUSD - Trends, Forecasts

European indices have today been the target of investors’ fears about emerging markets. The situation in Turkey is beginning to show signs of fragility. Yesterday, economic confidence hit the lows since March 2009 (in the midst of the global financial crisis), which led to a further decline in the Turkish Lira against the US Dollar. In the last 3 days, the Turkish currency depreciated by 6% against the US Dollar. Meanwhile in Argentina, Peso lost 8.15% even after President Macri announced that he was negotiating with the IMF on a loan of 50,000 M.USD, which should offset the country’s current inability to fund intentional markets. Since the beginning of the year, Argentino lost 45% of its value against the US Dollar. These two events, although uncorrelated, focused mainly on the securities most exposed to these two economies. In this sense, as Spanish banks BBVA and Santander, as well as Telefónica were particularly targeted by investor sales.

My forecasts by EURUSD,

Market View; World Stock

Daily Market Reviews by

The delicate phase that crosses Argentina and Turkey has generated turbulence in the exchange markets and by reflex in the financial markets as a whole. This instability has led to an escape of foreign capital from these countries, a move that further pressures their respective currencies.

Expert profiling conundrum -

Market View; World Stock

Forex market and its

The escalation of trade tensions between the US and China influenced the begining of the week, although some European markets managed to close on positive ground in a session that was marked by the closing of the North American market.

It's impossible to make

Market View; World Stock

Any questions from newcomers

The day was negative for most European markets, in a general context marked by fears about the situation in emerging markets and trade tensions between the US and China. Just like yesterday, automakers were among the worst performers, after over the weekend President Donald Trump said he was prepared to impose additional charges worth 200,000 M.USD on imports from China. Also on the sector weighed the deadlock that is marking the trade talks between the EU and the US, which are centered on the automotive industry.

Press review

Market View; World Stock

Forecast and levels for

The behavior of European stock exchanges continues to reflect investors' risk aversion. The day was marked by the start of talks between the US and Canada on a possible revision of the NAFTA agreement. In addition, some of the attention remains diverted to the news about customs tariffs on trade between the US and China. The banking sector was the only one to end up, as opposed to the technology that led the losses in sectoral terms, due to a series of reductions of recommendation. On the other hand, the German pharmaceutical Bayer depreciated, despite having reported a 3.90% increase in the results of the second quarter. In terms of economic indicators, in the Euro Zone, the PMI economic activity index stood at 54.50 in August, slightly above the expected 54.40. The same indicator, but for the services sector, stood at 54.40, as economists estimated. In Germany, the PMI for the services sector reached 55.0, compared to the expected 55.20.

Eur/usd

Technical and Market Analysis

World Stock Indexes Trading

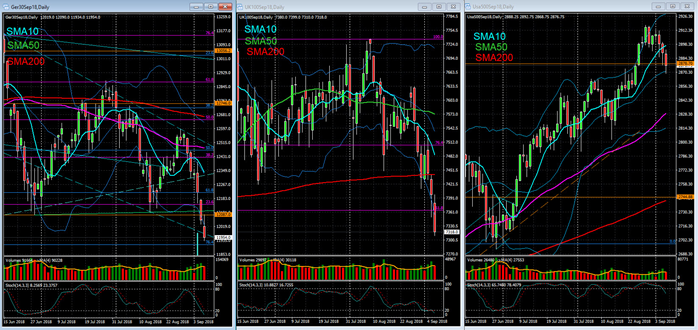

Stock Markets – Closing Note – 6 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

The trend of European markets in today's session was negative. Pressure from emerging markets as well as fears about US-China customs tariffs remain the main reasons for investors' increased risk aversion. Leading the losses were the technology sector, reflecting the behavior of US counterparts, and producers of raw materials. Above all, at this moment investors are questioning the future of emerging markets, including Argentina. Yesterday, members of the Government said they were confident about the new agreement with the IMF. However, issues related to Brexit remain as background. The German Government has stated that it is prepared for any scenario, including that of a "no-deal". The London Stock Exchange ended today with a loss of 0.91%.

The US market was trading lower, with tech companies' performance negatively impacting the Nasdaq. Highlighting the losses of Amazon and Apple, as well as chip makers, such as Micron Technology. In terms of economic indicators, the ADP employment report showed that 163 000 jobs were created during August, an increase below the expected 200 000. Still on the labor market, the number of weekly applications for unemployment benefits reached 203 000, lower than the estimated 213 000. On the other hand, factory orders decreased 0.80% in July, after two months of increases and against an expected fall of 0.60%. On the other hand, orders for durable goods decreased 1.70% in July, in line with expectations. The ISM index for the services sector stood at 58.5 in August, compared to the previous 55.7 and the forecast 56.8.

World Stock Indexes Trading

Press review

EURUSD Technical Analysis 2015,

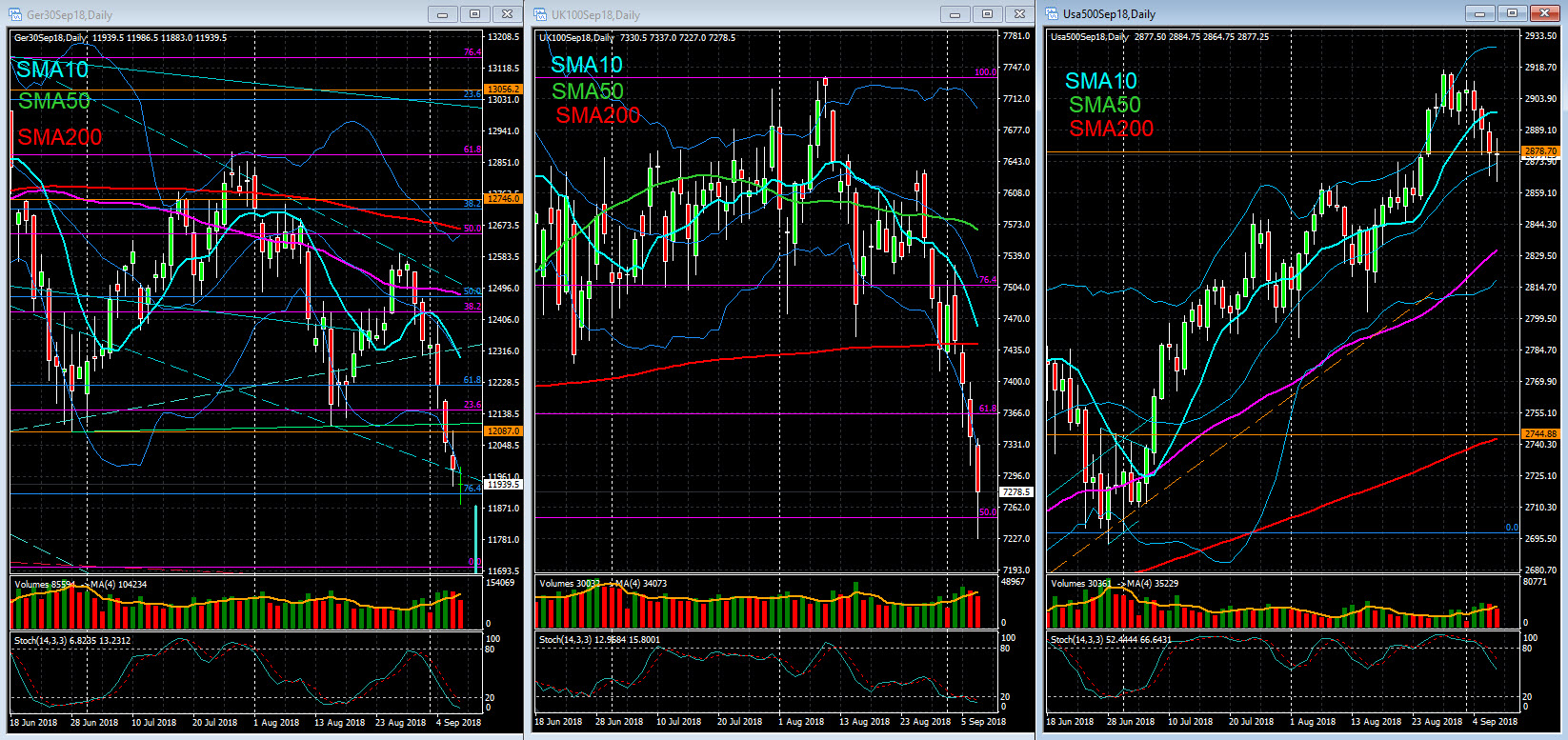

Stock Markets – Closing Note – 7 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

Most European stock markets closed lower. Investor sentiment has remained conditioned by threats to trade relations between the US and its main partners (European Union, Canada and China). The banking sector remained under pressure. Deutsche Bank shares fell 1.48%, after news that the Chinese group HNA intends to sell its 7.60% stake. On the other hand, IAG's stocks have come down, in reaction to the British Airways statement that a computer-based attack, lasting several days, will have affected 380,000 cards. On the macroeconomic front, Eurostat reported today that the economies of the Eurozone and the European Union grew 2.10% in the second quarter, after 2.10% in the first three months of the year. Compared to the previous quarter, GDP in the Euro Zone and in the EU rose 0.40%.

Wall Street traded slightly without a definite trend, in a session marked by investor reaction to economic data at a time of uncertainty hanging over the US trade negotiations. In terms of economic indicators, the most awaited indicator of the day and week was the employment report, known today before the opening of the session. This publication has raised renewed fears about the conduct of monetary policy by the FED. During August, the US economy created 201,000 jobs, up from 190,000 expected and 157,000 in July, reflecting a growing economy that showed no signs of slowing down during the summer season. The annualized unemployment rate (currently at the lowest of the last 18 years) was 3.90%, down from 3.80% in July, but in line with expectations. But the biggest surprise came from wages, since it was observed in August a monthly increase of 0.40%, higher than the 0.20% forecast and the previous 0.30%. Year-on-year, the increase was 2.90% for the highest since June 2009.

Press review

Market View; World Stock

AUD/USD news

Stock Markets – Closing Note – 10 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

Today European stock markets ended positive. The banking sector led the gains, and such performance stood out in the Italian market. Intesa, Unicredit and Banco BPM rose more than 5%. In fact, as a reflection of recent days, several members of the Government of Rome expressed their intention to comply with the Community budgetary rules, the Italian stock market showed a relative overperformance, having registered a valuation of more than 2% and the yields of OT to keep up to a minimum of one month. In the political arena, investors also reacted today to the election results in Sweden and developments related to Brexit.

The US stock exchange started the week on a positive note, with shares of tech companies recovering from losses last week. Even so, attention remains focused on US-China trade relations, after Friday, Donald Trump raised the possibility of applying additional tariffs on Chinese products worth 267 M.USD. However, the US president said that Apple should change its production to the US to avoid being hit by customs tariffs imposed on Chinese imports.

World Stock Indexes Trading

Forex News (from InstaForex)

Market View; World Stock

Stock Markets – Closing Note – 11 Sep

Ger30, UK100 and SP500 are CFD’s, written over the Dax30, Footsie100 and S&P500 Index futures:

European markets have traded slightly today, with most sectors down. The sentiment was conditioned by confirmation by the World Trade Organization that it will respond to China's request for the country to obtain permission to impose sanctions against the US for failing to comply with anti-dumping measures of the international entity. Thus, in face of investors' concerns about the relations between these two countries, commodity producers ended up leading losses in sectoral terms, with a depreciation of around 1%. ArcelorMittal fell 1.98% after news of rising its bid to buy Essar Steel. On the other hand, Apple's suppliers (such as STMicroelectronics) were penalized by the statements of the American President. Donald Trump said that the technology company is being hampered by the tariffs imposed on Chinese imports. Meanwhile, oil prices in the United States rose to levels close to $ 68 a barrel in face of mounting fears about the hurricane approaching the US East Coast that could condition production of this raw material. In terms of economic indicators, in Germany, the ZEW sentiment index of financial agents was better than expected, as it stood at -10.6 in September, compared to the -13.0 expected.

The US market reversed to positive ground after starting lower in today's session. At stake was the performance of the technology sector.

Market View; World Stock

World Stock Indexes Trading

Press review

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register