")

Global Market Situation Report: Wall Street Records vs. the "Hormuz Shock" and Central Bank Divergence (May 2026)

Global Market Situation Report: Wall Street Records vs. the "Hormuz Shock" and Central Bank Divergence (May 2026)

As of the close of May 1, 2026, the global financial landscape presents a fascinating paradox: while conflict in the Middle East maintains energy prices at critical levels, North American equity markets have reached new all-time highs, driven by an unprecedented technological earnings cycle. Nevertheless, the fragility of geopolitical negotiations and persistent inflationary pressures suggest a lingering "tail risk" environment for the remainder of the quarter.

1. Regional Analysis: Fundamental and Macroeconomic Drivers

North America: Resilience and Tech Dominance

The United States has demonstrated economic resilience far exceeding expectations. Despite war-related costs, Q1 GDP points to an annualized growth of 3%. Current focus remains on the Federal Reserve’s "hawkish hold" stance—maintaining interest rates while monitoring inflationary persistence.

-

Canada: The labor market shows signs of cooling, with unemployment hitting 6.7% in March, while the energy sector (oil sands) benefits from high global prices.

-

Mexico: Banxico is entering a potential rate-cutting phase to stimulate growth, leveraging the relative stability of the Peso against the Dollar (USD/MXN).

Europe: In the Stagflation Trap

The continent faces the highest risk of a "stagflationary shock." With Qatari LNG supplies disrupted, Eurozone inflation jumped to 3% in April.

-

United Kingdom: Inflation exceeds 5%, and the Bank of England (BoE) has warned that further rate hikes are inevitable if the energy shock persists. The FTSE 100 remains resilient due to its heavy weighting in mining and oil majors.

-

Germany & Italy: Industrial powerhouses are reeling from gas costs, facing a potential GDP contraction in Q2 2026.

Asia-Pacific: The Chinese Giant Awakes

China has managed to absorb the impact of the conflict better than anticipated, thanks to its vast strategic petroleum reserves and transition toward a green economy.

-

China: Q1 GDP grew 5.0% year-on-year, beating forecasts. However, domestic consumption remains the weak link, with retail sales growing a mere 2.4%.

-

Japan: The Yen (JPY) has plummeted to critical levels (near 160 against the dollar), triggering massive verbal and physical interventions by the Bank of Japan (BoJ).

Middle East: The Epicenter of Risk

The Strait of Hormuz remains under a partial blockade by the U.S. Navy against Iranian ports.

-

Saudi Arabia: The economy grew 2.8% in Q1, driven by non-oil sector expansion under Vision 2030, despite a 7.2% drop in crude production due to regional tensions.

2. Status of Major Assets and Currencies

| Symbol / Pair | Current Level / Price | Weekly Trend | Key Observation |

| DXY (Dollar Index) | 98.0 - 100.0 | Strong | Safe haven status + high rates |

| EUR/USD | 1.1750 | Stable | Pressured by EU economic weakness |

| USD/JPY | ~160.0 | Volatile | Massive BoJ intervention underway |

| GBP/USD | 1.36 | Bullish (10-wk high) | Supported by BoE hike expectations |

| Gold (XAU/USD) | $4,787 - $4,800 | Stable / High | Primary hedge against geopolitical risk |

| Bitcoin (BTC) | $73,000 | Under Pressure | Recent recovery hit by U.S. regulation |

3. Sector Analysis: Leading Symbols and Companies

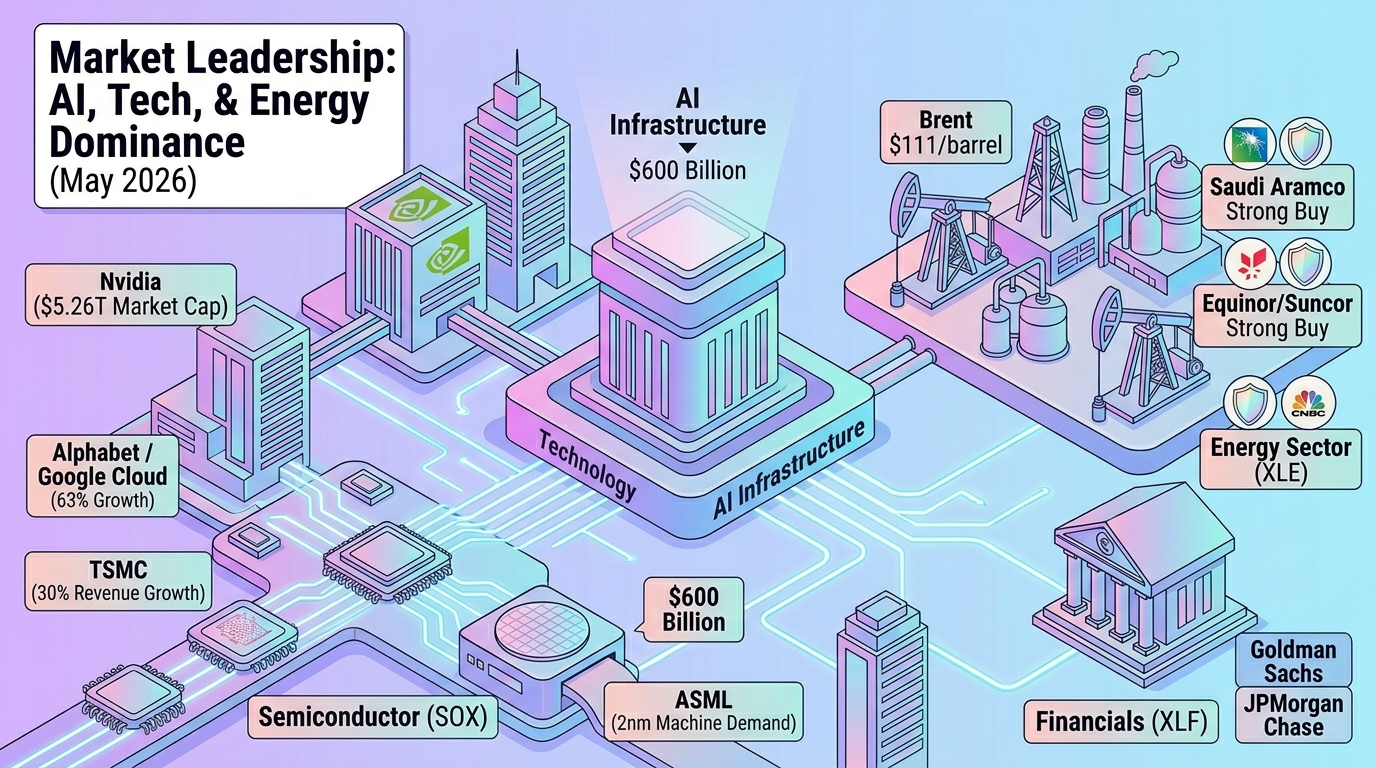

Technology (XLK / QQQ)

The engine of the current market. AI infrastructure spending is projected at $600 billion for 2026.

-

Nvidia (NVDA): Record market cap of $5.26 trillion; dominates the AI chip market.

-

Apple (AAPL): Reported $111.2 billion in revenue with record Q1 iPhone sales.

-

Alphabet (GOOGL): 63% explosive growth in Google Cloud driven by AI integration.

Energy (XLE)

The sector has regained leadership following the collapse of temporary truces. Brent Crude is trading at $111/barrel.

-

Saudi Aramco: Reported attempted attacks on its Ras Tanura refinery, increasing the risk premium.

-

Exxon Mobil (XOM) & Chevron (CVX): Beat expectations despite lower annual net profits due to hedging positions.

-

Equinor (EQNR) & Suncor (SU): Rated as "Strong Buy" due to cost discipline and resilient production.

Financials (XLF)

Wall Street majors kicked off earnings season with strength, benefiting from high brokerage and trading volatility.

-

Goldman Sachs (GS): Estimated EPS of $16.48; viewed as the financial "luxury bellwether."

-

JPMorgan Chase (JPM): Maintains solid guidance on the back of Net Interest Income (NII).

Semiconductors (SOX)

A critical sector for national security and AI advancement.

-

TSMC (TSM): Raised 2026 revenue guidance to 30% growth despite geopolitical headwinds.

-

ASML: Poised for record 2026 revenue driven by 2nm machine demand.

-

Samsung: Record revenue of 133.9 trillion KRW, though facing historic labor strikes.

4. Relevant News and Immediate Outlook

-

Iran’s Peace Proposal (May 1): Iran presented a 14-point plan demanding total U.S. withdrawal from the region and the collection of tolls in Hormuz. President Trump has labeled the proposal "unsatisfactory," raising the likelihood of military re-escalation.

-

Earnings Season: Next week features key results from Netflix, Walt Disney, and TSMC, which will determine if the "relief rally" has the fundamentals to sustain itself.

-

Crypto Regulation (GENIUS Act): The U.S. has accelerated the transition toward a government-issued digital currency by 2027, forcing a shakeout of unregulated stablecoins.

-

International Summits: The Trump-Xi Jinping meeting (May 14-15) will be the most significant geopolitical event of the year, with potential agreements on tariffs and Chinese neutrality in the Iran conflict.

Conclusion

The market remains in a state of "cautious optimism" in North America, but "high alert" in Europe and Asia. The bifurcation between companies effectively monetizing AI versus those merely spending on it will sharpen in the coming months. The recommended strategy remains diversification into real assets (Gold), high-quality tech, and energy, while maintaining high USD liquidity to buffer against sudden disruptions in the Strait of Hormuz.

")

")