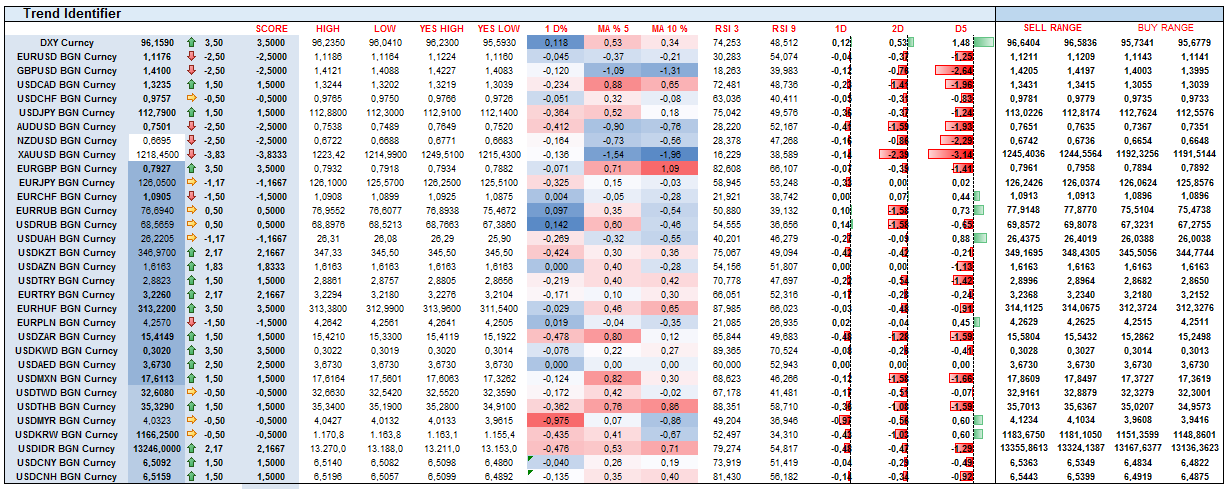

USD is expected to remain bid, with the potential to end the week at levels consistent with a reversal formation in technical terms. Conditions for USD gaining further ground are almost perfect. First, the position adjustment of USD long positions seems to have completed, with latest data showing hedge funds cutting their bets on further USD gains to the lowest level since 2014. Second, USD trades at a discount relative to rate differentials. For instance, the US 10-year government bond yield premium over Japan's is around 205bp today - the most since September 2014 - and more than 40bp higher than the low seen on February 11 and 13bp higher than last week's low. Today’s US release of February durable goods orders has the potential to push USD up again should this report come in strong. The generally hawkish Fed’s Bullard suggested that an April Fed rate hike may be justified. Looking at the price action, Gold has been the weakest in this USD reversal environment, HUF has been weak due to the recent rate cut and dovish central bank. Commodities have lost some ground but hardly reversed tehir trends. AUD, NZD and CAD have retreated from highs but it is still to early to call this a trend reversal just by looking at the price action. Emerging markets are mostly in a neutral zone, in Asia KRW has weakened significantly and it seems US data will decide if this is a real reversal or not.

")