당사 팬 페이지에 가입하십시오

- 게시자:

-

Cristian David Castillo Arrieta

재무 및 국제 비즈니스 전문가로 재무 관리를 전공했습니다. MQL5와 Python 독학 개발자로서 알고리즘 트레이딩, 멀티에셋 포트폴리오 구축, 정량적 리스크 관리에 집중하고 있습니다.

재무 및 국제 비즈니스 전문가로 재무 관리를 전공했습니다. MQL5와 Python 독학 개발자로서 알고리즘 트레이딩, 멀티에셋 포트폴리오 구축, 정량적 리스크 관리에 집중하고 있습니다.

저의 작업은 개별 전략이 아닌 조율된 포트폴리오로 작동하는 Expert Advisor의 설계, 최적화 및 검증에 중점을 두고 있습니다. 상관관계 분석, 시간대 커버리지 매핑, 자산군 분산화를 적용하여 단일 상품이나 단일 접근 방식에 의존하지 않는 시스템을 구축합니다. - 조회수:

- 2291

- 평가:

- 게시됨:

-

이 코드를 기반으로 한 로봇이나 지표가 필요하신가요? 프리랜스로 주문하세요

프리랜스로 이동

이 코드를 기반으로 한 로봇이나 지표가 필요하신가요? 프리랜스로 주문하세요

프리랜스로 이동

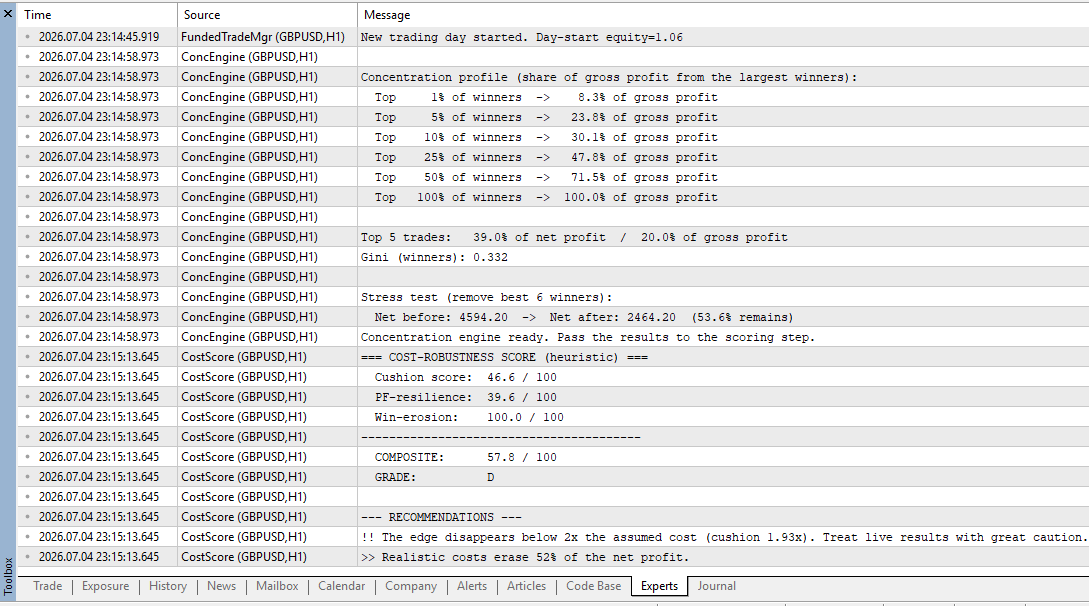

A backtest charges only the costs you assume. Net profit and profit factor are measured at that cost, so they never show how close the edge sits to the cost line. This tool answers the question directly: how much execution cost can the strategy absorb before its edge is gone?

The script reads a Date,Profit,Volume file (one row per closing deal) and prints a full report in the Experts tab:

- Breakeven cost per deal — the cost level at which the net profit reaches zero (the average edge per deal).

- Cushion — the multiple of an assumed realistic cost that the edge can absorb before the net hits zero.

- Net and profit factor at the assumed cost — the whole record re-priced, plus a cost-sensitivity curve from 0 to 3 times the assumed cost.

- Win erosion — the winning deals that the assumed cost turns into losers.

- A composite score (A+ to F) combining the cushion, the profit-factor resilience, and the win erosion, with written recommendations.

Input. Place a CSV named in the input parameter (default Trades.csv) in the terminal MQL5\Files folder, with the header Date,Profit,Volume and one row per closing deal. The Volume column is optional: if it is missing, the cost is applied per deal rather than per lot. On the first run, if no file is found, the script generates a reproducible sample and analyzes it, so the output is visible immediately. The helper ExportCost.mq5 writes the file from the trade history: copy its function into your Expert Advisor and call it from OnTester(), or run it as a standalone script.

Parameters. InpFileName (the CSV to read); InpCostPerLot and InpCostFixed (the assumed per-lot and per-deal cost); InpCushionTarget (the cushion that scores full marks); InpThinMult (the thin-winner threshold); InpErosionTol (the win-erosion tolerance); InpWeightCushion, InpWeightPF, InpWeightErosion (the three dimension weights, normalized automatically).

The tool is written in pure MQL5. It needs no external libraries, no Python and no DLLs.

//+------------------------------------------------------------------+ //| CostSens.mq5 | //| Cost & Slippage Sensitivity Analyzer (MetaTrader 5)| //| Reads a per-closing-deal result file and measures how much | //| execution cost the edge can absorb: the breakeven cost per | //| deal, the cushion over an assumed cost, the profit factor | //| at that cost, and how many winners it erases, combined | //| into a heuristic robustness-to-cost score. | //+------------------------------------------------------------------+ #property copyright "Cristian David Castillo Arrieta" #property version "1.00" #property script_show_inputs #property description "Reads a per-closing-deal result file and measures how robust the edge is to execution costs." //--- Input parameters input string InpFileName = "Trades.csv"; // CSV file: Date,Profit,Volume (one row per closing deal) input double InpCostPerLot = 12.0; // Assumed round-turn cost per 1.0 lot (spread + commission + slippage) input double InpCostFixed = 0.0; // Assumed fixed cost per deal (e.g. minimum commission), account currency input double InpCushionTarget = 3.0; // Cushion (x assumed cost) that scores full marks on the cushion dimension input double InpThinMult = 1.0; // A winner is "thin" if its result <= InpThinMult x its assumed cost input double InpErosionTol = 0.20; // Win-erosion tolerance: this fraction of winners erased scores zero input double InpWeightCushion = 0.45; // Weight: cost-cushion dimension input double InpWeightPF = 0.30; // Weight: profit-factor-resilience dimension input double InpWeightErosion = 0.25; // Weight: win-erosion dimension //--- Aggregated report: every figure the analyzer prints lives here struct SReport { int nTrades; // total closing deals loaded from the file int nWinners; // deals with a positive result, before cost int nLosers; // deals with a negative result, before cost int nFlat; // deals with exactly zero result double grossProfit; // sum of the winning deals, before cost double grossLoss; // sum of the losing deals, before cost, as a positive number double netProfit; // gross profit minus gross loss, before cost double profitFactor; // gross profit / gross loss; -1.0 means undefined (no losing deals) double winRate; // winners as a percentage of all deals double sumVol; // total traded volume across all deals (lots) double avgEdge; // net profit per deal (net / nTrades) double assumedCost; // total assumed cost across all deals (the C1 baseline) double avgCost; // assumed cost per deal (assumedCost / nTrades) double breakeven; // breakeven cost per deal that zeroes the net (equals avgEdge) double cushion; // breakeven multiplier: the net reaches zero at cushion x the assumed cost double netAtCost; // net profit left at the assumed cost level double pfAtCost; // profit factor at the assumed cost; -1.0 means no losing deals left double retention; // netAtCost / netProfit (0..1) int erased; // winners that turn into non-winners at the assumed cost double erosionRate; // erased / nWinners (0..1) double thinShare; // share of gross profit from winners within InpThinMult x their cost double cushionScore; // cost-cushion dimension of the score, 0..100 double pfScore; // profit-factor-resilience dimension of the score, 0..100 double erosionScore; // win-erosion dimension of the score, 0..100 double composite; // weighted composite score, 0..100 string grade; // letter grade from A+ to F }; //--- Globals double g_profit[]; // result of each loaded closing deal double g_vol[]; // volume (lots) of each loaded closing deal string g_date[]; // date of each loaded closing deal int g_n = 0; // number of deals currently loaded //+------------------------------------------------------------------+ //| Read a Date,Profit,Volume file (one row per closing deal) | //| Read as text and split each row on the comma, which tolerates | //| blank lines and stray spaces better than field-by-field reading. | //| The Volume column is optional: if it is missing or unparseable, | //| the volume defaults to 1.0, so a plain Date,Profit file also | //| works (the cost is then applied per deal rather than per lot). | //+------------------------------------------------------------------+ bool LoadTrades(string filename, double &profit[], double &vol[], string &dates[]) { int handle = FileOpen(filename, FILE_READ|FILE_TXT|FILE_ANSI); if(handle == INVALID_HANDLE) { PrintFormat("Could not open %s. Error: %d", filename, GetLastError()); return false; } int count = 0; bool firstLine = true; while(!FileIsEnding(handle)) { //--- Read one whole line and trim the surrounding whitespace string row = FileReadString(handle); StringTrimLeft(row); StringTrimRight(row); if(firstLine) // the first line is the header { firstLine = false; continue; } if(row == "") // skip blank lines continue; //--- Split "Date,Profit,Volume" into its fields string parts[]; if(StringSplit(row, ',', parts) < 2) continue; // need at least a date and a result StringTrimLeft(parts[0]); StringTrimRight(parts[0]); if(StringToTime(parts[0]) <= 0) // skip rows whose date does not parse continue; double value = StringToDouble(parts[1]); //--- The volume is optional; default to 1.0 when absent or non-positive double v = 1.0; if(ArraySize(parts) >= 3) { double parsed = StringToDouble(parts[2]); if(parsed > 0.0) v = parsed; } //--- Store the parsed deal count++; ArrayResize(profit, count, 512); ArrayResize(vol, count, 512); ArrayResize(dates, count, 512); profit[count - 1] = value; vol[count - 1] = v; dates[count - 1] = parts[0]; } FileClose(handle); return (count > 0); } //+------------------------------------------------------------------+ //| Net profit and profit factor at a cost multiplier | //| Each deal pays mult x (InpCostFixed + InpCostPerLot x volume). | //| Returns the net after cost; writes the profit factor to pfOut | //| (-1.0 when no losing deals remain after the cost is applied). | //+------------------------------------------------------------------+ double NetAtMultiplier(const double &profit[], const double &vol[], int n, double mult, double &pfOut) { double gp = 0.0, gl = 0.0; for(int i = 0; i < n; i++) { //--- The cost charged to this deal at the requested multiplier double cost = mult * (InpCostFixed + InpCostPerLot * vol[i]); double net = profit[i] - cost; if(net > 0.0) gp += net; // a deal that is still a winner after cost else if(net < 0.0) gl += -net; // a deal that is a loser after cost } pfOut = (gl > 0.0) ? gp / gl : -1.0; // -1 means no losing deals remain return gp - gl; } //+------------------------------------------------------------------+ //| Count the winners erased at a given cost multiplier | //| A winner is erased when its result no longer covers its cost. | //+------------------------------------------------------------------+ int CountErased(const double &profit[], const double &vol[], int n, double mult) { int erased = 0; for(int i = 0; i < n; i++) { if(profit[i] <= 0.0) // only deals that were winners can be erased continue; double cost = mult * (InpCostFixed + InpCostPerLot * vol[i]); if(profit[i] - cost <= 0.0) // the cost wipes out the gain erased++; } return erased; } //+------------------------------------------------------------------+ //| Share of gross profit held by "thin" winners | //| A thin winner sits within InpThinMult x its assumed cost, so a | //| small rise in cost can erase it; this share is the gross profit | //| that lives close to the cost line. | //+------------------------------------------------------------------+ double ThinWinnerShare(const double &profit[], const double &vol[], int n, double grossProfit) { if(grossProfit <= 0.0) return 0.0; double thin = 0.0; for(int i = 0; i < n; i++) { if(profit[i] <= 0.0) continue; double cost = InpCostFixed + InpCostPerLot * vol[i]; if(profit[i] <= InpThinMult * cost) thin += profit[i]; } return thin / grossProfit * 100.0; } //+------------------------------------------------------------------+ //| Print the cost-sensitivity curve as a small ASCII chart | //| Each row is a multiple of the assumed cost; the bar is scaled to | //| the net profit at zero cost, so the decay is easy to read. | //+------------------------------------------------------------------+ void PrintCostCurve(const double &profit[], const double &vol[], int n, double netZero) { double mults[] = {0.0, 0.5, 1.0, 1.5, 2.0, 2.5, 3.0}; Print("Cost-sensitivity curve (net profit as the assumed cost is scaled up):"); Print(" xCost Cost/deal Net ProfitFactor"); for(int k = 0; k < ArraySize(mults); k++) { double pf; double net = NetAtMultiplier(profit, vol, n, mults[k], pf); double perDeal = mults[k] * (InpCostFixed + InpCostPerLot * (n > 0 ? AvgVolume(vol, n) : 0.0)); int bars = (netZero > 0.0) ? (int)MathRound(40.0 * MathMax(net, 0.0) / netZero) : 0; string bar = ""; for(int b = 0; b < bars; b++) bar += "#"; string pfText = (pf < 0.0) ? "n/a" : StringFormat("%.2f", pf); PrintFormat(" %4.1f %8.2f %8.2f %s |%s", mults[k], perDeal, net, pfText, bar); } } //+------------------------------------------------------------------+ //| Average volume across the loaded deals (lots) | //+------------------------------------------------------------------+ double AvgVolume(const double &vol[], int n) { if(n <= 0) return 0.0; double s = 0.0; for(int i = 0; i < n; i++) s += vol[i]; return s / n; } //+------------------------------------------------------------------+ //| Generate a synthetic per-deal file so the script runs by itself | //| The seed is fixed, so the demo is reproducible. The set is shaped| //| to land on a believable middle grade rather than a perfect pass. | //+------------------------------------------------------------------+ bool EnsureSampleFile(string filename) { int handle = FileOpen(filename, FILE_WRITE|FILE_TXT|FILE_ANSI); if(handle == INVALID_HANDLE) { PrintFormat("Could not create sample %s. Error: %d", filename, GetLastError()); return false; } FileWriteString(handle, "Date,Profit,Volume\n"); MathSrand(20260601); // fixed seed: the demo is reproducible int trades = 200; datetime t = StringToTime("2026.01.05"); int todayLeft = 1 + (int)(MathRand() % 3); // 1-3 deals on the first day int bigIdx[] = {17, 53, 96, 134, 178}; // a few large winners, spread out int thinIdx[] = {8, 27, 49, 70, 88, 110, 129, 150, 171, 190}; // small winners costs can erase for(int i = 0; i < trades; i++) { //--- Volume first, so the call order stays stable across branches double vol = 0.10 + (MathRand() % 6) * 0.10; // 0.10..0.60 lots //--- Decide what kind of deal this is bool isBig = false, isThin = false; for(int b = 0; b < ArraySize(bigIdx); b++) if(bigIdx[b] == i) { isBig = true; break; } if(!isBig) for(int b = 0; b < ArraySize(thinIdx); b++) if(thinIdx[b] == i) { isThin = true; break; } double profit; if(isBig) profit = 110.0 + (i % 4) * 25.0; // engineered large winner else if(isThin) profit = 1.0 + (MathRand() % 5); // small winner the cost can erase else { double u = (double)MathRand() / 32767.0; if(u < 0.58) profit = 15.0 + (double)MathRand() / 32767.0 * 66.0; // ordinary winner else profit = -(20.0 + (double)MathRand() / 32767.0 * 52.0); // loser } //--- Write the row and advance the calendar by 1-3 deals per day MqlDateTime dt; TimeToStruct(t, dt); string ds = StringFormat("%04d.%02d.%02d", dt.year, dt.mon, dt.day); FileWriteString(handle, StringFormat("%s,%.2f,%.2f\n", ds, profit, vol)); todayLeft--; if(todayLeft <= 0) { t += 86400; todayLeft = 1 + (int)(MathRand() % 3); } } FileClose(handle); PrintFormat("Sample file %s created with %d deals.", filename, trades); return true; } //+------------------------------------------------------------------+ //| Build the full report from the loaded deals | //+------------------------------------------------------------------+ void BuildReport(const double &profit[], const double &vol[], int n, SReport &r) { //--- Tally winners, losers, flats and the gross figures (before cost) r.nTrades = n; r.nWinners = 0; r.nLosers = 0; r.nFlat = 0; r.grossProfit = 0.0; r.grossLoss = 0.0; r.sumVol = 0.0; for(int i = 0; i < n; i++) { r.sumVol += vol[i]; if(profit[i] > 0.0) { r.nWinners++; r.grossProfit += profit[i]; } else if(profit[i] < 0.0) { r.nLosers++; r.grossLoss += -profit[i]; } else r.nFlat++; } //--- Core figures, all before cost r.netProfit = r.grossProfit - r.grossLoss; r.profitFactor = (r.grossLoss > 0.0) ? r.grossProfit / r.grossLoss : -1.0; // -1 = undefined r.winRate = (n > 0) ? 100.0 * r.nWinners / n : 0.0; //--- The assumed cost baseline and the per-deal edge r.assumedCost = 0.0; for(int i = 0; i < n; i++) r.assumedCost += InpCostFixed + InpCostPerLot * vol[i]; r.avgCost = (n > 0) ? r.assumedCost / n : 0.0; r.avgEdge = (n > 0) ? r.netProfit / n : 0.0; r.breakeven = r.avgEdge; // per-deal cost that zeroes the net //--- The cushion: net profit reaches zero at cushion x the assumed cost r.cushion = (r.assumedCost > 0.0) ? r.netProfit / r.assumedCost : 0.0; //--- The net and the profit factor at the assumed cost (multiplier 1.0) r.netAtCost = NetAtMultiplier(profit, vol, n, 1.0, r.pfAtCost); r.retention = (r.netProfit > 0.0) ? r.netAtCost / r.netProfit : 0.0; //--- Win erosion and the thin-winner share at the assumed cost r.erased = CountErased(profit, vol, n, 1.0); r.erosionRate = (r.nWinners > 0) ? (double)r.erased / r.nWinners : 0.0; r.thinShare = ThinWinnerShare(profit, vol, n, r.grossProfit); //--- Dimension scores (higher means more robust to cost). Factors are inputs. double ct = MathMax(1.0001, InpCushionTarget); // guard the denominator r.cushionScore = MathMax(0.0, MathMin(100.0, 100.0 * (r.cushion - 1.0) / (ct - 1.0))); if(r.profitFactor < 0.0) // no losers at all: fully resilient r.pfScore = 100.0; else if(r.profitFactor <= 1.0) // not profitable even before cost r.pfScore = 0.0; else if(r.pfAtCost < 0.0) // no losers left after cost r.pfScore = 100.0; else r.pfScore = MathMax(0.0, MathMin(100.0, 100.0 * (r.pfAtCost - 1.0) / (r.profitFactor - 1.0))); double et = MathMax(0.0001, InpErosionTol); // guard the denominator r.erosionScore = MathMax(0.0, MathMin(100.0, 100.0 * (1.0 - r.erosionRate / et))); //--- Normalize the weights so the result does not depend on their sum double wc = MathMax(0.0, InpWeightCushion); double wp = MathMax(0.0, InpWeightPF); double we = MathMax(0.0, InpWeightErosion); double wsum = wc + wp + we; if(wsum <= 0.0) { wc = 0.45; wp = 0.30; we = 0.25; wsum = 1.0; Print("Warning: weights were non-positive; reverting to the 0.45 / 0.30 / 0.25 default."); } wc /= wsum; wp /= wsum; we /= wsum; //--- Composite score and its letter grade r.composite = r.cushionScore * wc + r.pfScore * wp + r.erosionScore * we; if(r.composite >= 90) r.grade = "A+"; else if(r.composite >= 80) r.grade = "A"; else if(r.composite >= 70) r.grade = "B"; else if(r.composite >= 60) r.grade = "C"; else if(r.composite >= 50) r.grade = "D"; else r.grade = "F"; } //+------------------------------------------------------------------+ //| Print a profit factor, handling the undefined (no-loss) case | //+------------------------------------------------------------------+ void PrintProfitFactor(string label, double pf) { if(pf < 0.0) PrintFormat("%sn/a (no losing deals)", label); else PrintFormat("%s%.2f", label, pf); } //+------------------------------------------------------------------+ //| Script entry point | //+------------------------------------------------------------------+ void OnStart() { Print("========================================"); Print(" COST & SLIPPAGE SENSITIVITY ANALYZER v1.0"); Print(" How much execution cost can the edge absorb?"); Print("========================================"); //--- Load the deals, or build and load a sample set if none is found if(!LoadTrades(InpFileName, g_profit, g_vol, g_date)) { Print(">> File not found or empty. Generating a sample set..."); if(!EnsureSampleFile(InpFileName)) { Alert("Could not create the sample file."); return; } if(!LoadTrades(InpFileName, g_profit, g_vol, g_date)) { Alert("Could not load the sample file."); return; } } g_n = ArraySize(g_profit); if(g_n < 20) // too few deals for the figures to be meaningful { Alert("At least 20 deals are required (results are more reliable with 100+)."); return; } SReport r; BuildReport(g_profit, g_vol, g_n, r); Print("\nNote: this works at the closing-deal level. A position closed in several"); Print("deals (partial exits) is several rows, and each exit deal pays its own cost."); if(r.netProfit <= 0.0) // the analysis needs a profitable set to make sense { Print("\nNet profit is not positive before cost; the cost analysis needs a profitable set."); PrintFormat("Net: %.2f | Deals: %d", r.netProfit, r.nTrades); return; } //--- Headline figures Print("\n=== STRATEGY (before added cost) ==="); PrintFormat(" Deals: %d (%d winners, %d losers, %d flat)", r.nTrades, r.nWinners, r.nLosers, r.nFlat); PrintFormat(" Win rate: %.1f%%", r.winRate); PrintFormat(" Net profit: %.2f", r.netProfit); PrintProfitFactor(" Profit factor: ", r.profitFactor); PrintFormat(" Total volume: %.2f lots (avg %.2f per deal)", r.sumVol, AvgVolume(g_vol, g_n)); PrintFormat(" Edge per deal: %.2f", r.avgEdge); //--- The assumed cost and the cost curve PrintFormat("\n=== ASSUMED COST: %.2f per lot + %.2f fixed (%.2f per deal on average) ===", InpCostPerLot, InpCostFixed, r.avgCost); Print(""); PrintCostCurve(g_profit, g_vol, g_n, r.netProfit); //--- The cost sensitivity results Print("\n=== COST SENSITIVITY ==="); PrintFormat(" Breakeven cost per deal: %.2f (the edge per deal)", r.breakeven); PrintFormat(" Cushion: %.2fx the assumed cost", r.cushion); PrintFormat(" Net at the assumed cost: %.2f (%.0f%% of the original net)", r.netAtCost, r.retention * 100.0); PrintProfitFactor(" Profit factor at cost: ", r.pfAtCost); PrintFormat(" Winners erased at cost: %d of %d (%.1f%%)", r.erased, r.nWinners, r.erosionRate * 100.0); PrintFormat(" Thin-winner gross share: %.1f%%", r.thinShare); Print(" (One-sided: only cost rises, so the net and the profit factor are meant to fall.)"); //--- Score Print("\n========================================"); Print(" COST-ROBUSTNESS SCORE (heuristic)"); Print("========================================"); PrintFormat(" Cushion score: %.1f / 100", r.cushionScore); PrintFormat(" PF-resilience: %.1f / 100", r.pfScore); PrintFormat(" Win-erosion: %.1f / 100", r.erosionScore); Print("----------------------------------------"); PrintFormat(" COMPOSITE: %.1f / 100", r.composite); PrintFormat(" GRADE: %s", r.grade); Print(" (Heuristic for ranking and quick comparison, not a statistically validated measure.)"); Print("========================================"); //--- Recommendations: each one is driven by a specific weakness Print("\n--- RECOMMENDATIONS ---"); if(r.cushion < 2.0) PrintFormat("!! The edge disappears below 2x the assumed cost (cushion %.2fx). Treat live results with great caution.", r.cushion); else if(r.cushion < 3.0) PrintFormat(">> The cushion is only %.2fx the assumed cost. A modest rise in spread or slippage materially cuts the result; build in margin before trading live.", r.cushion); if(r.profitFactor > 0.0 && r.pfAtCost > 0.0 && r.pfAtCost < 1.4) PrintFormat(">> At the assumed cost the profit factor falls to %.2f. The edge is thin once realistic costs are paid.", r.pfAtCost); if(r.retention < 0.70) PrintFormat(">> Realistic costs erase %.0f%% of the net profit (%.2f -> %.2f).", (1.0 - r.retention) * 100.0, r.netProfit, r.netAtCost); if(r.erosionRate >= 0.10) PrintFormat(">> %.0f%% of winning deals turn into losers at the assumed cost. The result leans on marginal winners.", r.erosionRate * 100.0); if(r.cushion >= 3.0 && r.pfAtCost >= 1.5) Print("++ The edge absorbs several times the assumed cost and keeps a healthy profit factor. It looks robust to execution costs."); Print("\nAnalysis complete."); } //+------------------------------------------------------------------+

EA KCI Embeded Sniper

EA KCI Embeded Sniper

The KCI Embedded Sniper is an algorithmic trading solution designed for high-precision reversal entries. Unlike conventional Expert Advisors that rely on external indicator dependencies (which often suffer from thread desynchronization and latency), this EA features a fully embedded Kinetic Compression Index (KCI) engine. By transplanting the entire mathematical framework of the KCI—calculating Velocity Quotients, Kinetic Displacement, Energy Dispersion, and Phase Velocity—directly into the EA’s core logic, we have eliminated "asynchronous lag." The result is a lightning-fast sniper engine that validates market exhaustion (Singularity) and momentum extremes (Williams %R) with micro-second precision, operating solely on completed bars to ensure zero-repaint performance.

KCI Standard: A Pure Kinematic Computing Engine for Market Singularity Detection

KCI Standard: A Pure Kinematic Computing Engine for Market Singularity Detection

The Kinetic Compression Index (KCI) is a custom oscillator designed to detect market exhaustion and localized compression events. By calculating its kinematic metrics internally rather than relying on external standard indicator handles, the KCI reduces overhead and simplifies buffer management for Expert Advisor (EA) integration. This article details the mathematical foundation, system architecture, buffer mapping, and practical integration guides for developers looking to implement this tool in MetaTrader 5.

Accelerator Oscillator (AC)

The Acceleration/Deceleration Indicator (AC) measures acceleration and deceleration of the current driving force.

MACD Signals

Indicator edition for new platform.