Aurum Quant Engine

- Experts

-

Javed Ali Khan Patan

I am an independent trader and strategy developer with a deepening interest in market structure and systematic execution. My work focuses on designing trading systems that emphasize clarity, selective positioning, and controlled decision making rather than trade stacking or lot amplification

I am an independent trader and strategy developer with a deepening interest in market structure and systematic execution. My work focuses on designing trading systems that emphasize clarity, selective positioning, and controlled decision making rather than trade stacking or lot amplification - Versione: 1.10

- Aggiornato: 4 dicembre 2025

- Attivazioni: 5

Aurum Quant Engine

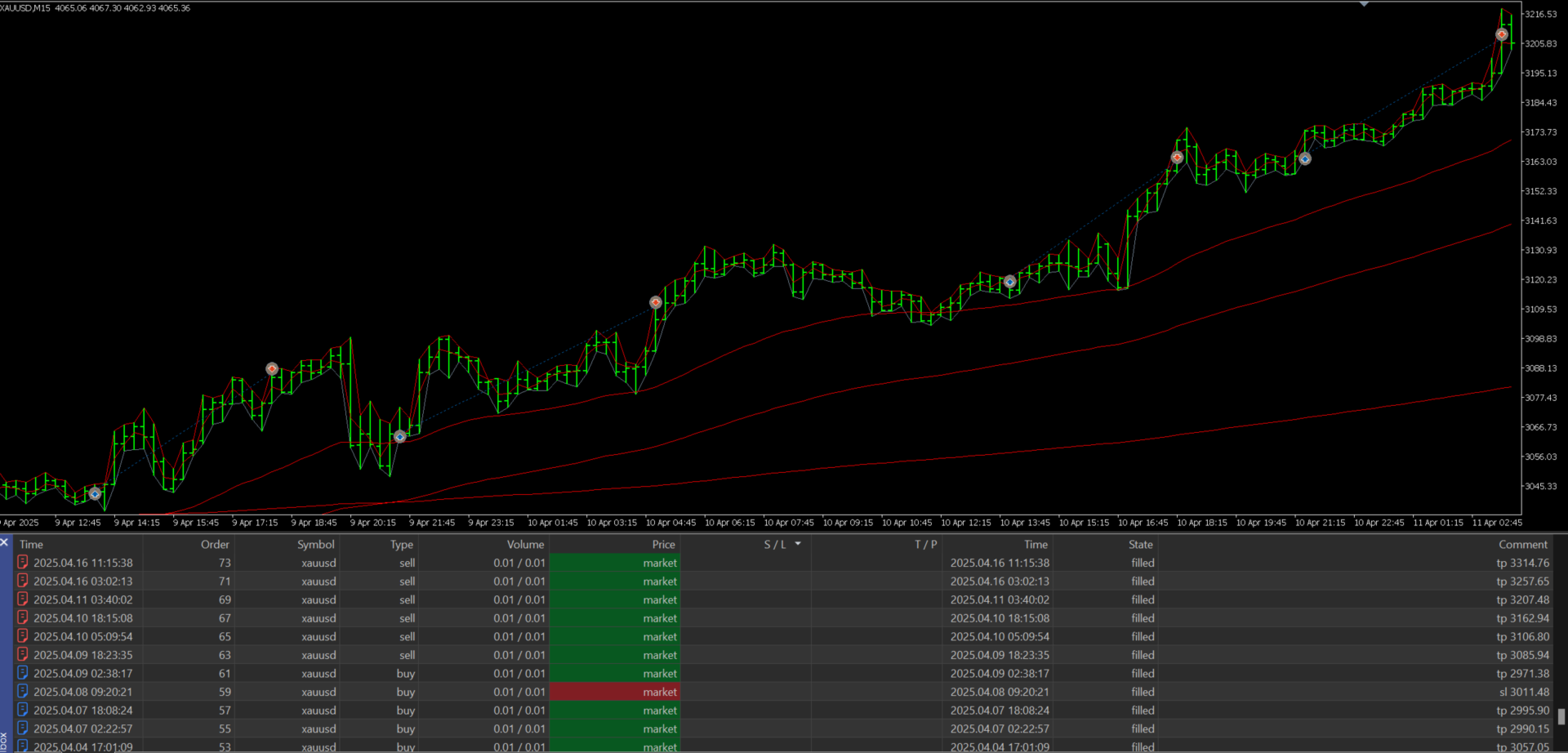

Aurum Quant Engine is a rule-based trading system designed to identify selective trade opportunities through structured market evaluation and controlled execution logic.

Aurum Quant Engine focuses on controlled trade selection through contextual evaluation rather than reactive signal generation. It assesses market conditions, directional intention, and price behavior stability before allowing execution. This helps reduce premature entries and promotes structured positioning across varying market conditions.

Part of an early controlled release. Further development may involve licensing revisions, including restricted or paid access for subsequent versions.

💬 If you find the system useful, your review or feedback on the MQL5 page would be greatly appreciated it helps me improve and continue refining the project.

Trade Logic Foundation

The system does not rely on isolated indicator events. It evaluates broader trading conditions, confirming whether the environment supports structured and controlled trade execution. This approach adds consistency to decision-making while preserving the internal logic and proprietary design of the strategy.

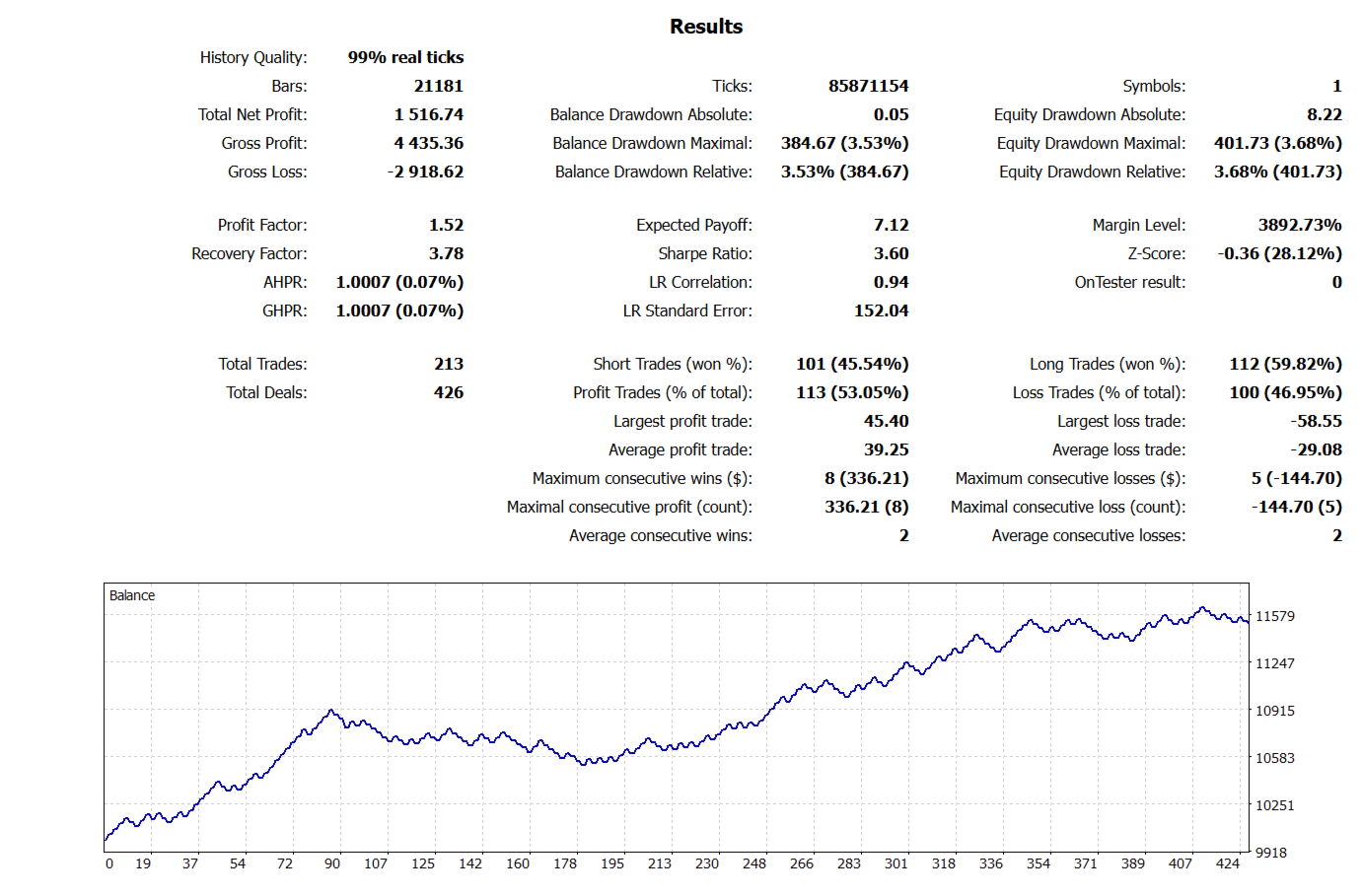

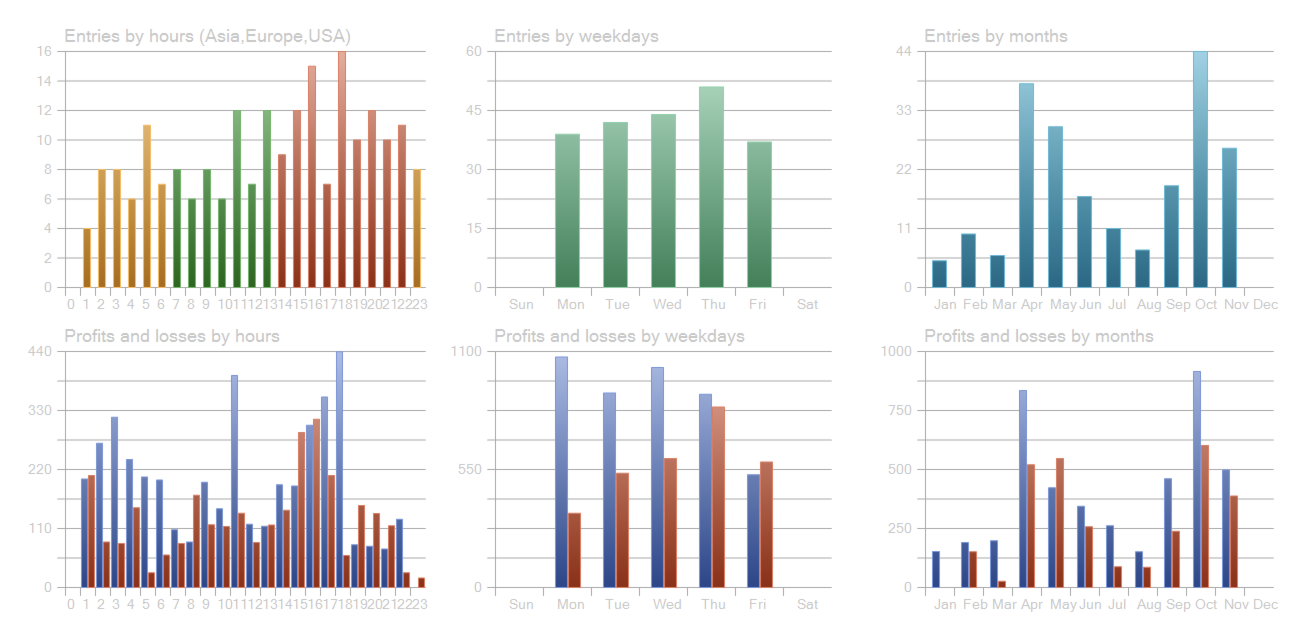

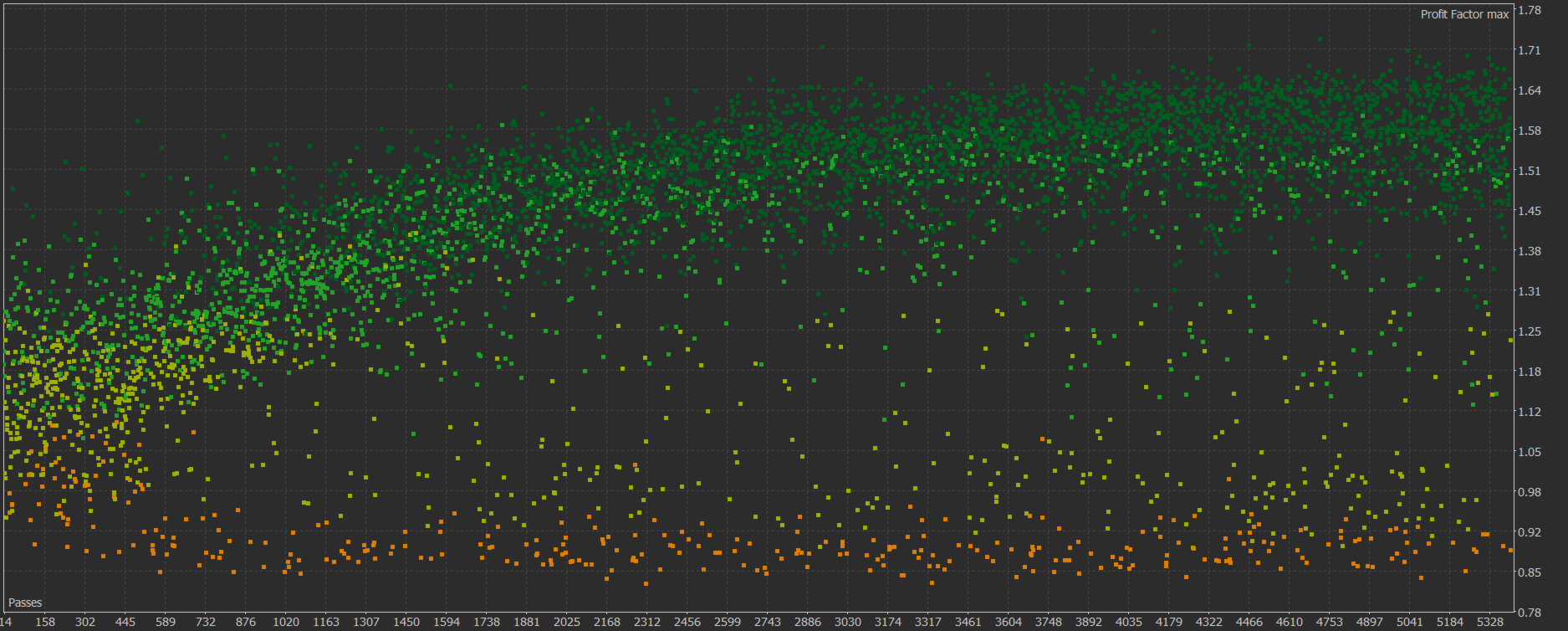

Performance Reference:

All results shown in backtest screenshots were generated using a fixed volume of 0.01 lot per trade, without martingale, grid, averaging, or compounding. The equity growth is based solely on strategic execution, not position scaling.

Risk Management and Governance

• Optional Trailing Stop-Loss — automatically adjusts SL upward as price moves in your favor, locking in gains and reducing exposure

• Daily Loss Limit Protection to pause trading automatically after a defined drawdown threshold

• Single-position control to avoid stacking, over-exposure, or uncontrolled pyramiding

• MagicNumber-based position isolation for conflict-free multi-EA usage

• Absolutely no martingale, grid, averaging, or multiplier-based systems — performance is driven by strategy logic, not position sizing

This structure supports disciplined deployment across personal, funded, and evaluation-based environments.

Execution Characteristics

• Designed for reliable performance in both backtesting and live trading

• No intrabar recalculation or repainting

• Compatible with both Netting and Hedging account types

• Slippage and symbol precision handled internally

• Maintains execution consistency across different market instruments

Input Parameters Overview

• Lot Size, Stop Loss, Take Profit, and optional Trailing Stop-Loss for dynamic risk control

• Configurable SMMA structure and smoothing parameters

• Entry and exit filtering options (trend, momentum, pattern confirmation, higher-timeframe bias)

• Optional timing features that act only on confirmed bar closes

• Daily loss protection with adjustable value threshold

• MagicNumber, Slippage, and individual Long/Short trade enabling

Usage Notes

• Recommended for medium-volatility timeframes (M15 to H4)

• Real-tick backtesting (99% modelling) suggested for reliable evaluation

• Compatible with Forex, metals, indices, and synthetic symbols

• Settings may be refined depending on instrument characteristics

Default settings are pre-configured and tested for XAUUSD on the M15 timeframe (0.01 lot).

This setup can be used directly for evaluation. For other symbols, SL/TP and filtering parameters can be adjusted to match volatility.

For assistance with instrument setup, feel free to contact me via MQL5 private chat.

Disclaimer

This system follows a structured method to improve decision consistency, but financial markets are uncertain by nature. Historical results and backtests illustrate how the system has behaved in past conditions, yet future performance may differ. Responsible risk allocation, testing, and informed usage are recommended.

L'utente non ha lasciato alcun commento sulla valutazione.