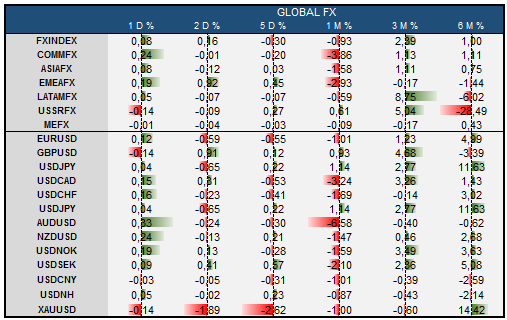

Rising US rate hike expectations supported by strong US domestic demand indications such as yesterday's housing data will keep the USD supported. However, markets are not viewing the rising chances of a Fed rate hike as a risk negative, yet. The US equity market saw its best daily gain since March with Financials no longer under-performing, suggesting that markets have gained conviction that the US economy can withstand higher rates. Indeed nominal US rates are well below the nominal expansion rate of its GDP, suggesting more credit and declining savings keeping US domestic demand conditions supported. The threat this US tightening cycle bears to the US economy does not come from the rates side. Instead, it will be the higher USD slowing the supply side of the economy. Weakening regional US survey data show a split between the weak supply side and the strong demand side of the US economy as manifested by strong housing and retail sales. Real Yields are Key. I believe that rising US real yields will be the catalyst for the higher USD. So far, it has been a risk-on related bullish USD story not boding well for Gold, which seems to be entering a broader correction. However, risk positive investors should not get too excited. Rising real US rates within a world of too much debt and regional overcapacity will be self-defeating.

On separate news, ECB ramps up balance sheet expansion by €21.3bn. This is the biggest increase since Apr on QE programme, total assets now €3.05trn. Price action has generally been supportive of USD, in developed markets EUR,CHF and JPY on yield differentials, AUD has gained some ground on commodity stabilization and higher short end local rates. CAD is still in a losing trend however 1,3150-1,3200 area has been a good resistance and commodities have given it some support. EMEA emerging markets have gained some ground from weakest levels, TRY has gained some ground on local news, RUB had been supported by oil, HUF and PLN have been supported mostly by the ECB. Overall picture remains USD supportive but risk aversion has faded a bit, CHY is losing ground but it seems government sanctioned devaluation is not hurting Asian currencies for now.