The great JPY-funded carry trade unwind has started and is not yet complete, suggesting JPY staying in demand. Price activity ahead of this weekend will tell us about the Street's positioning. Should USDJPY not rebound today as a result of risk reduction ahead of the weekend then we have to assume that short-term investors have not been participating in the JPY advance as much as hoped. Verbal intervention has come in again overnight with Finance Minister Aso calling rapid JPY moves "undesirable" and threatening action if required. We believe the verbal method is unlikely to develop the stabilizing impact on JPY. We cite two reasons. First, PM Abe's comment on Tuesday suggested to "refraining from arbitrary interventions in FX markets" and second investors putting the credibility of the BoJ into increasing doubt have reduced the effectiveness of verbal interventions. Abe’s comments were meant to be directed at China, with latest statistics showing Chinese based entities continuing to buy short-term Japanese money market securities, while the rest of the world was net selling. None the less, a JPY-weakening intervention ordered by the Fin Min and executed by the BoJ would not sit well with this recent comment by PM Abe and could undermine his international credibility ahead of the G7 meeting hosted by Japan in May.

The more USDJPY comes under pressure, the bigger the bearish impact on high-yielding currencies. Perversely, the falling USD against JPY causes USD to rally against EM currencies. It may be the falling USDJPY terminating the USD downside correction against high yielding currencies. Since the fall of USDJPY can be mainly explained by falling real yield differentials, the recent dovish comments by Yellen, moving US real yields, have contributed to the USDJPY sell-off. Abenomics is facing increasing headwinds via FX, which suggests that Japan has been a loser of dovish Fed commentary. Our bearish focus has returned back to EUR after seeing its inverse risk correlation breaking. This makes sense to us, given EMU’s net foreign liability position and EMU’s current account surplus easing, as indicating by the sharp weakening of net trade in Japan. UK’s PM Cameron's late admission about having invested in tax-efficient Panama may add to increasing populism in Europe, adding to Brexit fears and potential spill over effects on other EU members. The outcome of the Dutch referendum may be the clearest sign of flourishing populism within Europe, making it more difficult to agree to necessary structural reforms. Technically, EURUSD has developed a ‘negative divergence’ yesterday.

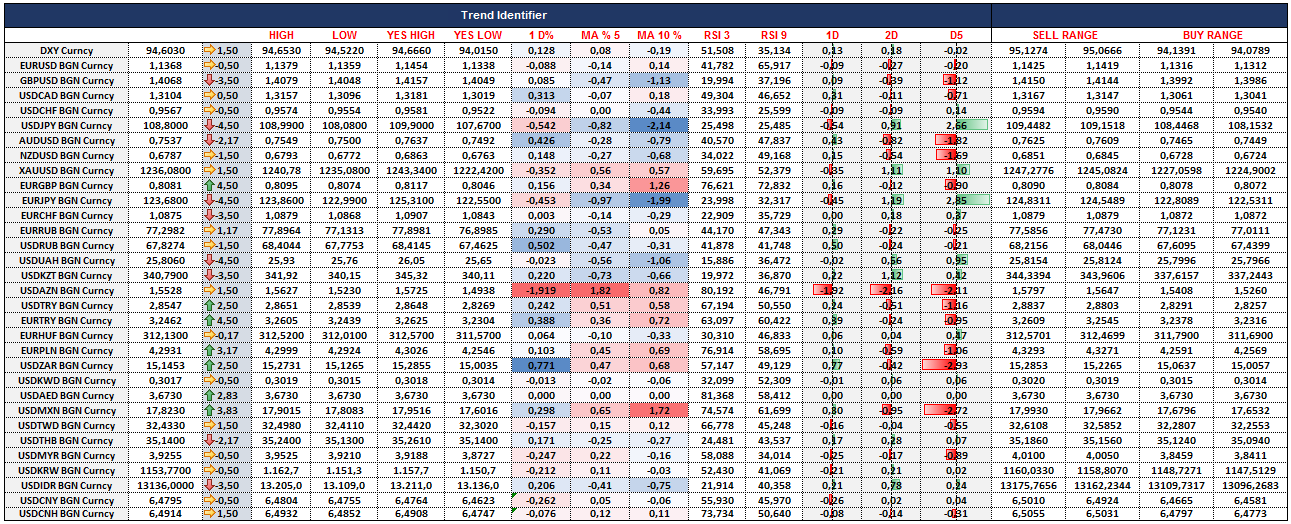

Looking at the price action, USDJPY and GBPUSD are trending lower with some strength however RSI’s are naturally in oversold levels. Emerging markets are mixed, the recent correction and the JPY and oil fuelled risk aversion has hit EFX and equities a bit. Weaker currencies TRY, PLN and MXN are hit by possible rate cuts, politics and possible Brexit fall out. Today should determine if the EMFX correction is indeed a correction or is a momentum gathering selloff.