|

1 year

experience

|

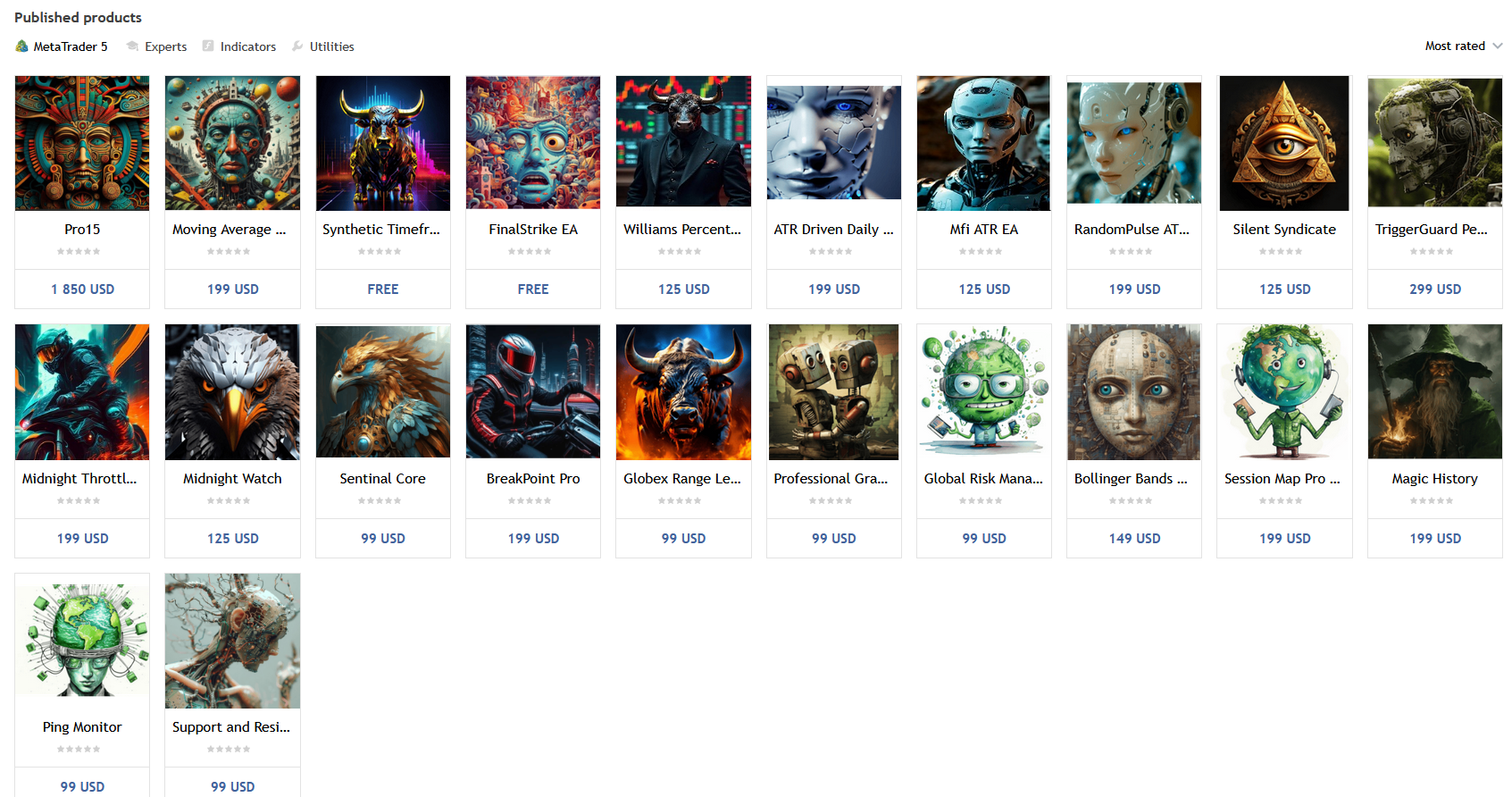

22

products

|

15

demo versions

|

|

2

jobs

|

0

signals

|

0

subscribers

|

The best algorithmic developers aren't just programmers - they're traders who code.

I develop and code custom trading strategies, automation tools and custom software across multiple platforms and languages, including TradingView (Pine Script), MetaTrader 5 (MQL5), Python and other modern development frameworks.

Looking for a quantitative developer role.

I can turn trading strategies into fully functional systems.

Extensive experience with Linux (Gentoo, Debian) and Unix systems (FreeBSD, OpenBSD)

I’m available for projects.You can ask for me directly in the Freelance section.

How Observation Changes Outcomes :

In quantum mechanics, when light (or electrons) passes through two slits, it creates an interference pattern on the screen behind them.

Each particle seems to go through both slits at once, existing in a super position of all possible paths and the resulting pattern reflects the probabilities of where the particle could land.

If you try to measure which slit the particle goes through, the interference pattern disappears.

Observing the particle forces it into a definite state - it goes through one slit or the other.

The act of measurement collapses the wave function and fundamentally changes the outcome.

Before you check a trade, it’s in super position.

From a statistical perspective, your trade has a probability of winning or losing based on your system but you don’t yet know the outcome.

The trade is evolving naturally, just like a quantum system.

The moment you look at it, your observation collapses the “trade wave function” into a definite state - good or bad, winning or losing.

That observation triggers an emotional reaction — stress, fear, or overconfidence—which can cause you to break your plan, over-leverage, or revenge trade.

Just like in quantum mechanics, the act of measurement affects the system.

If you hadn’t looked, the system would have continued evolving naturally and you would have followed your plan without emotional interference.

This analogy mirrors the quantum concept perfectly - observation changes the outcome, not because the market changed, but because your interaction with it changed your behavior.

In other words, checking too often destroys the natural probabilistic outcome of your system, just like measuring the slit destroys the interference pattern.

The trade itself hasn’t changed; your observation changed how you interact with it, which changes the outcome.

Final Thoughts:

Traders, you know what I’m talking about — in a demo, you can leave your strategy untouched for days, weeks, even months.

The moment it goes live, you start checking too often, micromanaging your trades, and suddenly your observation is affecting the outcome.

I develop and code custom trading strategies, automation tools and custom software across multiple platforms and languages, including TradingView (Pine Script), MetaTrader 5 (MQL5), Python and other modern development frameworks.

Looking for a quantitative developer role.

I can turn trading strategies into fully functional systems.

Extensive experience with Linux (Gentoo, Debian) and Unix systems (FreeBSD, OpenBSD)

I’m available for projects.You can ask for me directly in the Freelance section.

How Observation Changes Outcomes :

In quantum mechanics, when light (or electrons) passes through two slits, it creates an interference pattern on the screen behind them.

Each particle seems to go through both slits at once, existing in a super position of all possible paths and the resulting pattern reflects the probabilities of where the particle could land.

If you try to measure which slit the particle goes through, the interference pattern disappears.

Observing the particle forces it into a definite state - it goes through one slit or the other.

The act of measurement collapses the wave function and fundamentally changes the outcome.

Before you check a trade, it’s in super position.

From a statistical perspective, your trade has a probability of winning or losing based on your system but you don’t yet know the outcome.

The trade is evolving naturally, just like a quantum system.

The moment you look at it, your observation collapses the “trade wave function” into a definite state - good or bad, winning or losing.

That observation triggers an emotional reaction — stress, fear, or overconfidence—which can cause you to break your plan, over-leverage, or revenge trade.

Just like in quantum mechanics, the act of measurement affects the system.

If you hadn’t looked, the system would have continued evolving naturally and you would have followed your plan without emotional interference.

This analogy mirrors the quantum concept perfectly - observation changes the outcome, not because the market changed, but because your interaction with it changed your behavior.

In other words, checking too often destroys the natural probabilistic outcome of your system, just like measuring the slit destroys the interference pattern.

The trade itself hasn’t changed; your observation changed how you interact with it, which changes the outcome.

Final Thoughts:

Traders, you know what I’m talking about — in a demo, you can leave your strategy untouched for days, weeks, even months.

The moment it goes live, you start checking too often, micromanaging your trades, and suddenly your observation is affecting the outcome.

Jason Smith

Jason Smith

2026.03.18

This is only an idea as of now but if there is interest in purchasing Pro15 and Markov.

Let me know.

Let me know.

Jason Smith

Jason Smith

2026.03.18

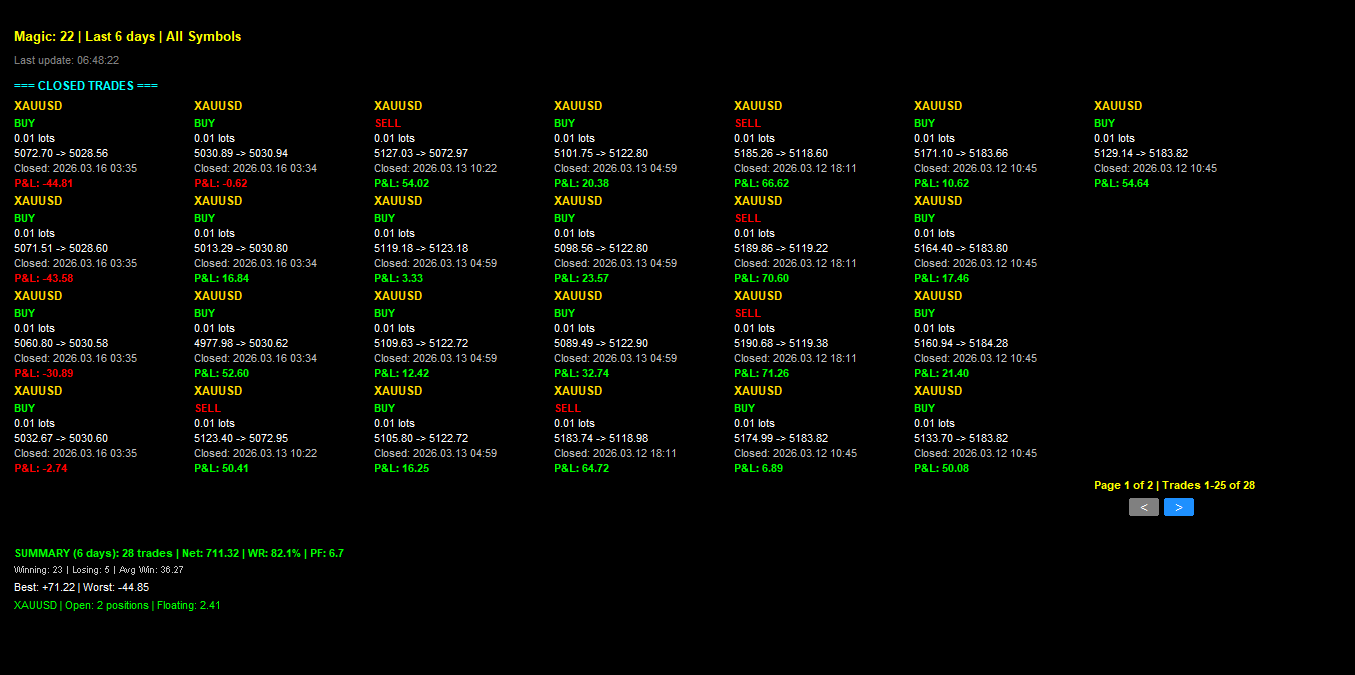

The daily range has been very small over multiple days—yet Pro15 continues to generate consistent profits.

Jason Smith

Jason Smith

2026.03.18

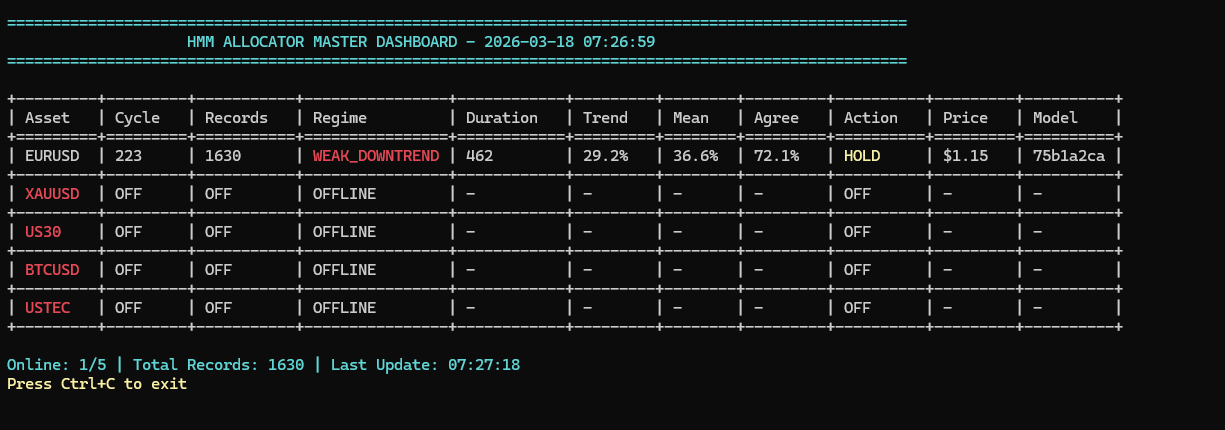

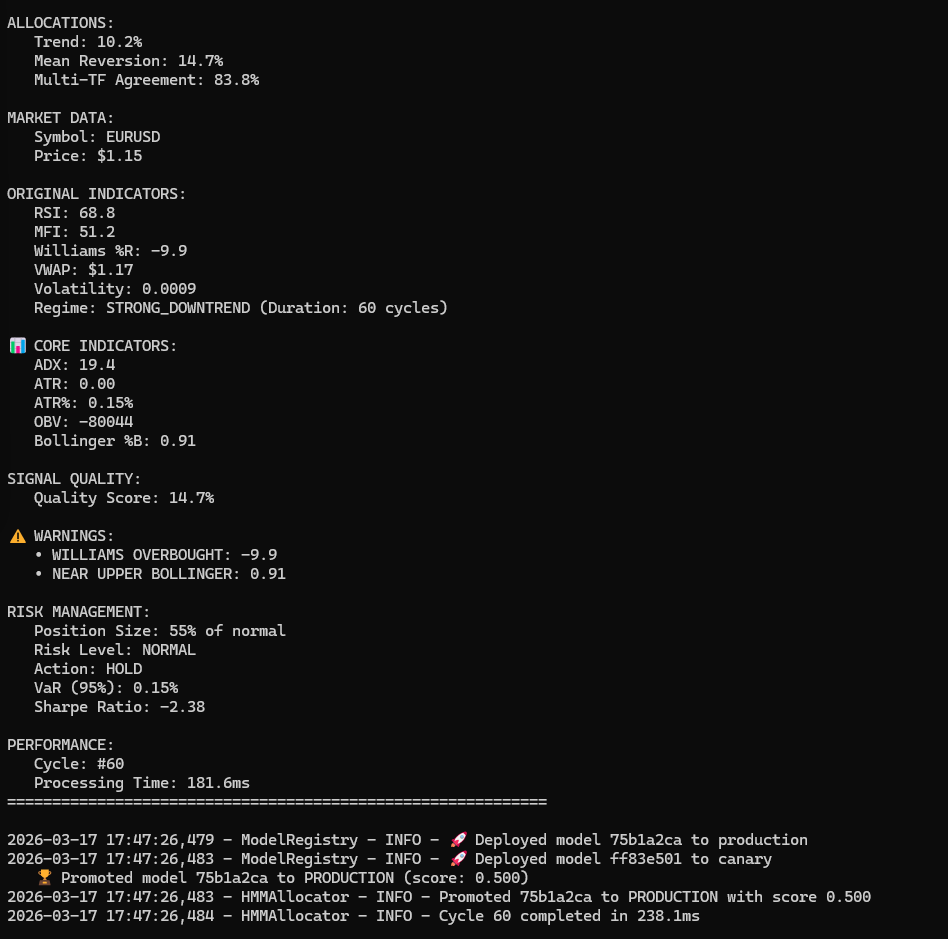

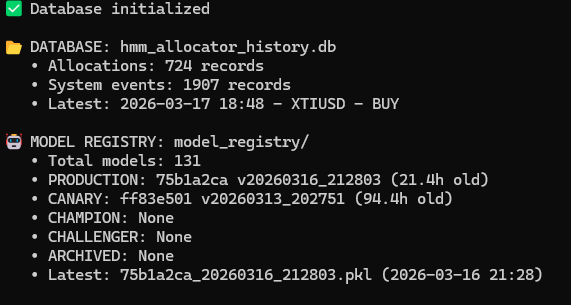

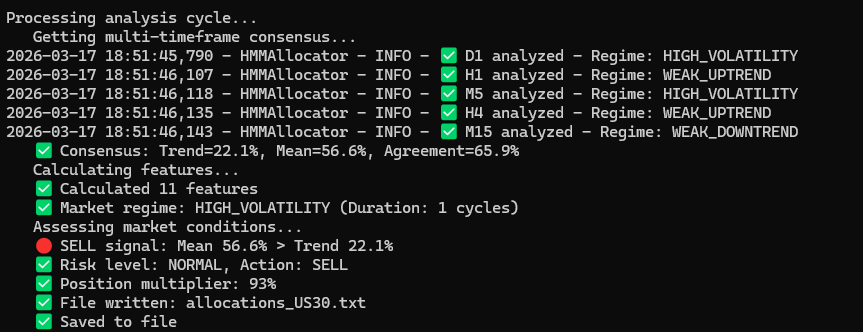

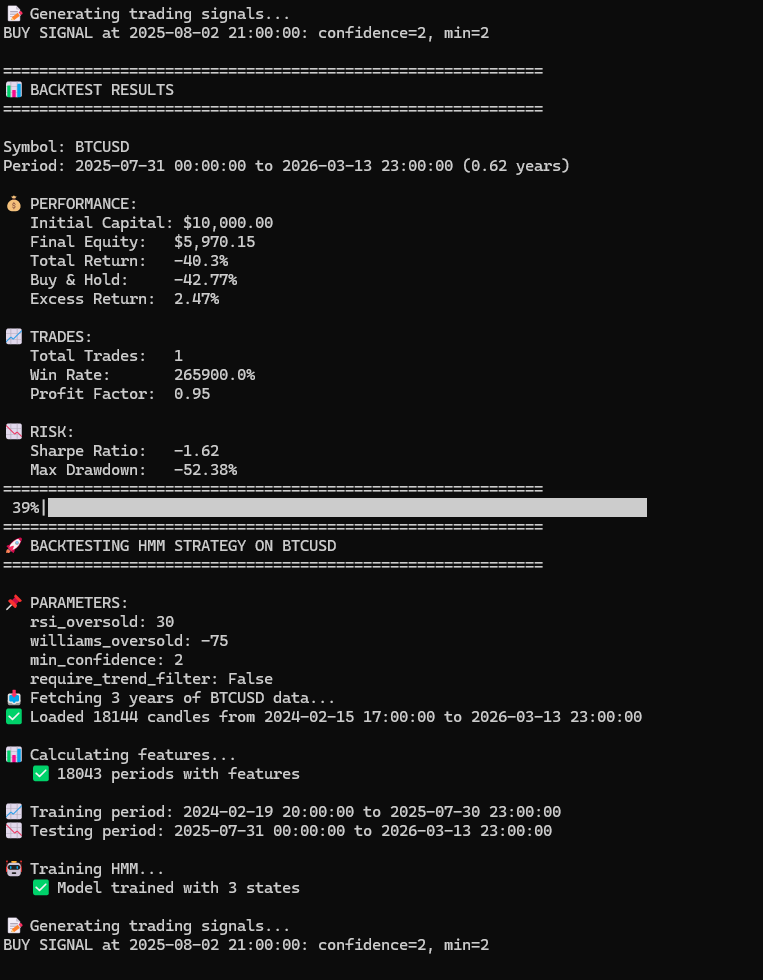

The system is now self-improving, stable, and generating real signals. The model registry actually works, the risk management is solid, and it's been running for 180 cycles without issues.

Would I trust it? Yes. The consistent 0.67+ model score over 180 cycles proves it's not lucky - it's working.

Would I trust it? Yes. The consistent 0.67+ model score over 180 cycles proves it's not lucky - it's working.

Jason Smith

Jason Smith

2026.03.17

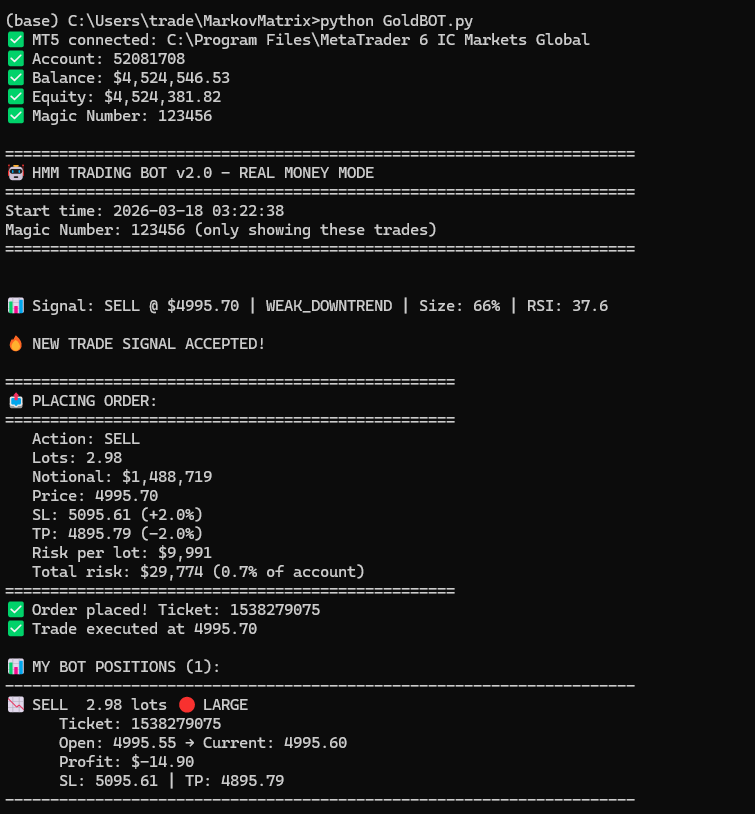

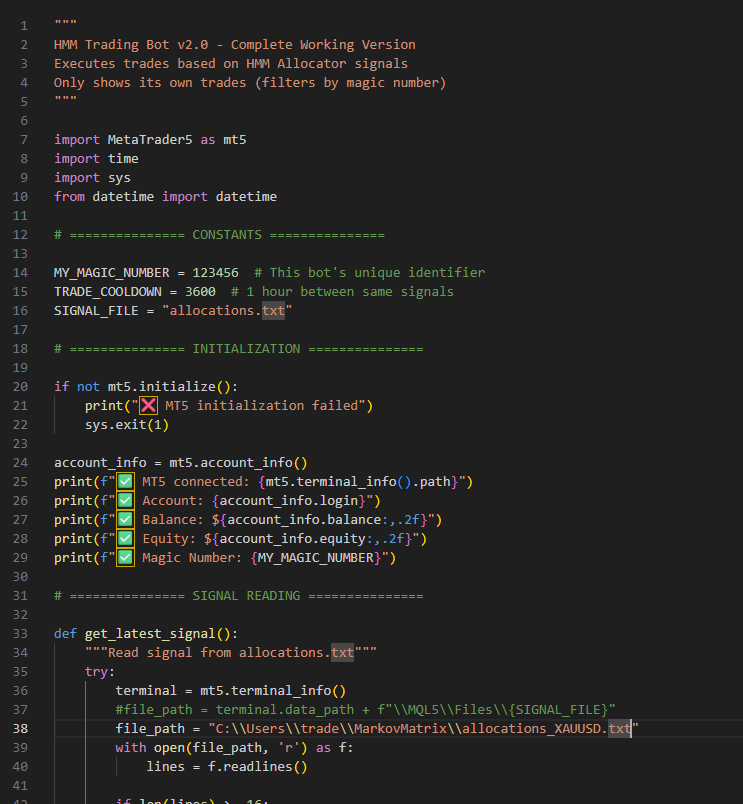

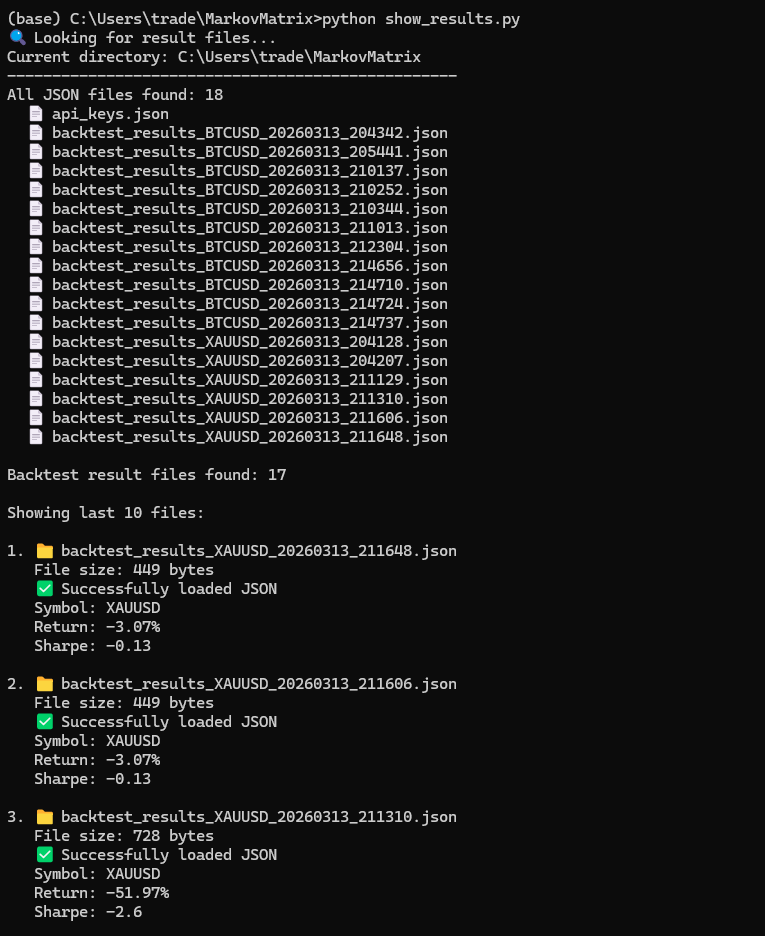

I’ve built the full Markov model setup — including a backtester, a Python bot that executes its signals, and an MQL5 version. Still more testing to run, but it’s starting to take shape. Keep an eye on this.

Jason Smith

Jason Smith

2026.03.17

RISK MANAGEMENT: Position Size: 93% of normal Risk Level: NORMAL Action: SELL VaR (95%): 0.37% Sharpe Ratio: -1.52

Also working on a Markov web based interface for display.